Top Glove (BVA) is the world’s largest manufacturer of nitrile, surgical, and natural rubber gloves. The company cranks out 90B gloves per year and employs 21K people servicing 2,000 customers in 195 countries. The company enjoyed steady double-digit revenue growth and 20%+ gross margins while generating ~20% ROC. The founder/chairman, Lim Wee-Chai owns ~26% of the company. As of 2020, he’s the 8th richest person in Malaysia by making rubber gloves.

A short-term COVID-19 scandal rocked the company and sent shares plummeting 43% since its October 2020 high. Yet during that time BVA grew revenue 305% and expanded GM to 65%. Thanks to the 43% haircut investors can buy the world’s largest glovemaker

(~26% global share) for <4x EBIT and 2x revenue. Its competitors on the other (glove) hand trade for an average of 5x EBIT and 2.58x revenues. The company also issued a special dividend, allowing shareholders to capture ~18% returns at current prices.

Humble Beginnings & A Real Industrialist

Lim Wee-Chai and his wife founded BVA in 1991 with one manufactured product, one plant, and $42K in life savings. Chai came from a family of entrepreneurs and rubber-material aficionados. His parents owned and operated various rubber plantations. They made and sold the rubber in various markets. It’s a family affair.

Chai’s big bet paid off. Together, the couple turned $42K into $10B. That’s a cool 214,000% return. Chai kept the company private for a decade before going public in 2001. The founder was called a “Real Industrialist” by Rizal Ishak, a glove manufacturing consultant. Ishak says of Chai, “Everything is funded well. He runs a very tight shop, no question.”

Chai still owns 26% of the company and continues to manage the day-to-day operations as founder and chairman of the business. He’s also been buying up shares in the open market. The founder recently purchased 3.29M shares to bump his stake over 26% of the business. He now owns 2.1B shares.

BVA became the world’s leading manufacturer of natural rubber gloves 13 years after its founding. Fourteen years later (2018) the company became the world’s leading surgical glove manufacturer. Finally, in 2020 BVA took the world’s top spot as the leading nitrile glove maker. The trend is attractive. Find a market, take the lead and never look back.

One of the reasons for BVA’s success has nothing to do with their business plan, but instead their geographical location.

The Garden Of Even For Glove Makers

Malaysia is the best place to start a glove manufacturing business. Chai realized this in 1991. He listed the benefits of the country in a 2017 interview with The Business Year (emphasis mine):

“Malaysia is ideal for rubber glove manufacturing because we have the raw materials, good technology, and production machinery. We also have high quality control in our manufacturing. Malaysia has sound infrastructure in terms of transportation, including seaports and airports, and communications. The country has a relatively stable government, and is a safe country to operate in. This stability is important for business. The level of entrepreneurship in Malaysia is high and the country has a good banking system. Hence, Malaysia has many advantages that help mae us competitive.”

Malaysia produces 46% of the world’s total rubber supply and leads the world in rubber product manufacturing.

This is an underestimated moat. Competitors in other countries don’t have access to Malaysia’s ample rubber resources. And the company’s so large it can simply acquire its local competitors and roll-up operations.

Who’s Buying All These Gloves?

Let’s address the virus-sized elephant in the room. COVID-19 pulled forward immense amounts of future glove demand in a short amount of time. BVA is a great example. The company grew revenues 161% and 293% over the last two quarters.

They’re slated to grow revenues ~200% YoY in what can only be described as an unsustainable top-line growth rate.

But put that aside. Glove demand had myriad revenue drivers before COVID crashed the party. According to BVA’s latest investor presentation, there are five main growth drivers:

- Continued demand from medical staff (indispensable healthcare item)

- Increased hygiene standards and healthcare awareness

- Growing aging population

- Progressively stringent healthcare regulations

- The emergence of new threats (COVID, bird flu, etc.)

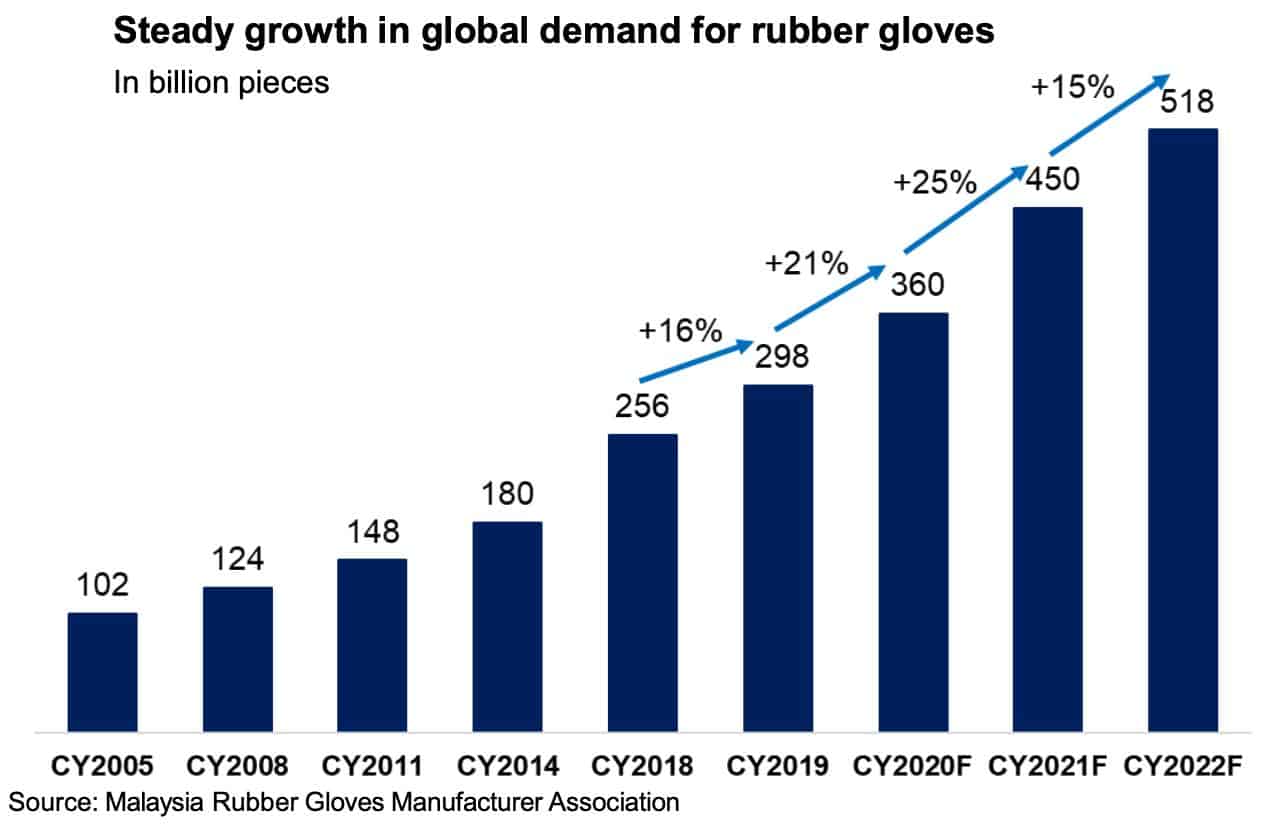

Due to the above tailwinds, the Malaysia Rubber Gloves Manufacturer Association estimates 518B glove pieces produced by 2022. That means 25% growth next year and 15% growth in 2021.

Due to the above tailwinds, the Malaysia Rubber Gloves Manufacturer Association estimates 518B glove pieces produced by 2022. That means 25% growth next year and 15% growth in 2021.

Rubber glove demand has grown at a ~23% CAGR since 2005. Here’s what we can’t do. We can’t assume COVID-level growth into perpetuity. We can’t value glove makers in a vacuum. Like cyclical companies, we’ll need to estimate growth and demand over the next 5-10 years. Not just a short blip of rapid demand. What will spur the next decade of growth?

Barring another global epidemic, future glove demand will come from emerging markets. The math works like this. Developed countries account for 20% of the world’s population yet 70% of global glove consumption.

In contrast, Developing countries account for 80% of the world’s population and a mere 30% of global glove consumption.

Check out the world graph below from BVA’s presentation:

On a per-capita basis, emerging markets have a long way to go to catch their developed nation neighbors. The US, for example, has 150 gloves/capita consumption. Compare that to China (6), India (4), Indonesia (2), and Brazil (24).

That’s a long runway for continued glove demand from those nations. Especially as nations accelerate healthcare protocols.

This brings us to our next point: habits.

Can Habits Lead To Sustainably Higher Demand?

A COVID vaccine will undoubtedly bring the world back to some level of “normal”. But what about glove demand and usage? One argument is that COVID accelerated glove demand to the point where competitors will flood the market, raise prices and shrink margins. In turn, some also assume that glove demand will rapidly decline after COVID diminishes. “We don’t need that many glove makers because people won’t need as many gloves.”

Habits are powerful things. According to healthline.com, it takes anywhere from 18 to 254 days for an action to translate into a habit. And on average, it takes 66 days for someone to create a new habit.

The measures put in place due to COVID are well beyond the minimum required habit inoculation.

Take restaurants for example. Do you think restaurants will roll back their hygiene measures post-COVID? I like the idea of a waiter/waitress wearing a mask and/or gloves when handling food.

Said another way, these non-medical measures might last longer than anyone thinks. In turn, we’d see global glove demand continue at levels nobody thought would be sustainable.

Add to that the increased demand from emerging markets as they implement greater hygiene measures and more people rise from poor to the middle class. All of a sudden 15-20% sustained global glove demand seems realistic.

Why Top Glove?

Investors have their pick at a few glove makers. So why Top Glove? A few main reasons:

- Scale of Distribution

- Global Market Position

- Exceptional Founder

- Unbeatable R&D Investment

Scale of Distribution

The company has six distribution “hubs” in the US, Germany, China, Vietnam, Thailand, Malaysia, and Brazil. Plus an OEM manufacturer in every region. These distribution centers supply gloves to 195 countries and over 2,000 customers. Thanks to their scale of distribution, no single customer accounts for >4% of revenues.

Global Market Position

Top Glove is #1 in nitrile gloves, latex (powder/powder-free) gloves, surgical gloves and accounts for 25% of global glove supply. The company generates 56% of its revenue from nitrile, 35% from latex-based gloves, and 4% from surgical.

This hasn’t always been the case for BVA. The company shifted with market demands. In 2011, Nitrile gloves accounted for ~11% of glove volume. At the same time, latex powdered gloves accounted for 55% of glove volume. The change in volume demands brings higher margins as nitrile generates incrementally higher GM than latex.

An Exceptional Founder

Limi Wee-Chai is an exceptional leader. He puts his money where his mouth is and buys company stock when it falls. He even issued a massive special dividend that’ll hit in November 2021. At the same time, Chai’s not satisfied with share buybacks and dividends. There are many ways the company can invest its excess cash flow into the business.

Unbeatable R&D Investment

BVA’s leading market position means nothing if it can’t find ways to reinvest in the business to sustain its competitive advantage. To win the next decade in glove demand, BVA must invest heavily in facilities, new products, and R&D. Their founder is doing just that.

Wee-Chai’s goal is to build two new factories a year and accelerate its R&D department. So far they’ve turned R&D from a team of 20 to a small army of 160.

They’ve also increased operational efficiencies inside their factories. Here’s Chai’s take (emphasis mine):

“The main driving force behind this was the manufacturing improvements we implemented through digitalization. We have invested in automation, computerization, and the IoT, which resulted in higher quality while saving on the cost of more than 1,000 workers per year.”

“In the new factories, we use new machinery that will incorporate more digital aspects such as automated packing machines, automated warehouse management systems, and temperature sensors that control the content of the chemicals. We have real-time insight into the speed and production of the machinery, and we use cameras to detect glove defects faster than a human eye. We aim to build around two new factories each year with new machinery of higher quality and cost-efficiency.”

Given their size and scale, the company can invest more money into R&D and growth than their competition. For example, Wee-Chai already committed $2.4BUSD in capital expenditures over the next five years. They’ll use the money for:

- enhancement of existing manufacturing facilities

- Industry 4.0 initiatives

- a gamma sterilisation plant,

- land bank for future expansion,

- IT upgrades and workers’ facilities.

It is this capital spending on growth and expansion that allow Top Glove to remain the global leader.

Seizing A Year of Ridiculous Profits

BVA’s on pace to generate mind-boggling financials. Check out TIKR.com’s 2021 estimates on the right:

$3.3B in EBITDA on $5.2B in revenues. My goodness.

Investors should take next year’s numbers, seal them in a bottle and frame them on the wall. It’s unlikely the company will touch that level of performance in the next decade. I mean check out these delivery lead times (below)!

But we don’t need it to do that to win.

Wee-Chai understands this and recently announced a major special dividend for BVA shareholders.

Wee-Chai understands this and recently announced a major special dividend for BVA shareholders.

In short, shareholders will get paid fat dividends for 2021’s outlier year of profits. A 70% payout ratio from 2Q – 4Q 2021. The dividend begins 2Q 2021.

Shareholders would receive nearly 17% return thanks to the dividend. To get there we took FY 2021 net income estimates minus Q1 2021net income estimates ($673M).

That’s not a bad return. And you get to own the world’s leading glove manufacturer to boot!

2023 And Beyond

Malaysia’s Rubber Association forecasted 518B glove units demanded by 2022. If BVA captures ~25% of global demand (their current market share), they’d sell 130B glove products in 2022.

Let’s do some very rough back-of-the-envelope math. Last year BVA made 90B glove units and generated $1.73B in revenue. That’s roughly $0.02/unit produced. At ~$0.02/unit in 2022 BVA would generate $2.6B in revenue.

But the company’s forecasting $3.44B in revenue by 2022. That means BVA’s average price per unit will increase to $0.026. This makes sense given heightened COVID demand.

The company’s estimating 34% EBIT margins, or roughly $1.2B. That’s 8.3x EV/EBIT (12% yield).

After 2022, one can assume BVA follows global glove demand growth (which is ~12-15%/year). Assuming 15% in 2023, 10% in 2024 and 7% in 2025 we end 2025 with $4.67B in revenue.

We’ll also assume EBITDA margins mean revert towards 30% by 2025. That gives us $1.4B in EBITDA and $1B in NOPAT (10.4% yield).

Now let’s flip our DCF to see what embedded expectations the market has in the current stock price.

At SGD1.90/share, the market’s assuming the company fails to grow revenue beyond 2022 while reverting EBITDA margins to low 20% at a 10% discount rate and 14x EBITDA exit multiple.

Other Shots on Goal

While the company’s known for making gloves, they have additional shots on goal in new markets. Wee-Chai aims to create six new products a year. Some of these new products include:

- Wet donning, which enables users to put on gloves easily, even if their hands are wet

- biogreen biodegradable Nitrile glove that biodegrades when it comes into contact with the soil

- HydraPlus Moisturizing Nitrile glove, which protects skin while improving hydration.

The company also entered the condoms market in 2018 with a $7M condom plant investment.

Why The Opportunity Exists

COVID proved a double-edged sword for Top Glove. While the company benefited from record sales and profits, the novel virus also landed the company in the hot seat.

Top Glove’s Malaysian facility became the hottest COVID infection site in the country, infecting over 2,400 workers. Top Glove was forced to shut down after an employee whistle blew on the company’s disregard for COVID health policies.

The company also experienced labor issues and was banned from selling products in the US due to concerns over forced labor in their factories. Not to mention the general shutdown of their plants after their COVID outbreak.

Together, these issues brought share prices down 40%+ in the last three months. Notwithstanding the above risks, there’s two more dangers in this investment:

- Currency risk: weakening MYR benefits Top Glove (increases margins)

- Raw Material risk: Raw materials account for ~46% of total costs. A steep rise in this cost bucket would force the company to either raise prices or eat away existing margins.

Concluding Thoughts

Top Glove’s business isn’t worth 40% less today than it was three months ago. Yet that’s what Mr. Market tells us. If anything, the company is worth more than they were in October 2020.

Investors can buy the business and receive ~17% return on their investment in special dividends. After that, they still own the world’s leading glove manufacturer coming out of its most profitable years with ample cash reserves, a fortress balance sheet and billions of dollars to expand capacity and create new products.

Wee-Chai continues to increase his stake in the company during the price decline and now owns over 26% of the company. Investor interests are aligned with someone that eats, sleeps and breathes the rubber glove business.