Before we start here’s a link to a coronavirus cheat sheet I put together yesterday. It has all of the key data and resources I’m using to track the spread of the pandemic. I’ll be updating it regularly as new info comes in.

There a few main takeaways at this point (1) the situation is evolving rapidly and there remains a good deal of uncertainty; so we must stay humble in our assumptions (2) most experts seem to now agree that the virus’s fatality rate is likely to come down significantly from current estimates of 3.4% to somewhere between 0.1% and 0.5% — for comparison, the seasonal flu has a fatality rate of less than 0.1% and (3) even at these lower fatality rates the virus is expected to greatly stress the current resources of our healthcare system.

From a purely economic and market standpoint, the risk now seems to mostly be concentrated in our response to the virus as well as the lasting behavioral impacts on the consumer. School closures, canceled events, and quarantined clusters are likely to persist for the foreseeable future though there’s credible reasons to hope that warmer weather brings slight relief from the virus to the Northern hemisphere.

The market is forward-looking though and will look past these near-term events if the narrative begins to take hold that the all-in costs of this virus are significantly lower than first expected — this remains a big if and I suspect it’ll take a few weeks, if not longer, to get there.

In addition, the recent 50bps rate cut from the Fed along with the global calls for boosting fiscal spending, in response to the virus, certainly don’t hurt the bull case for stocks.

Which brings us to today.

After the technical damage done to the charts following February’s large bearish engulfing candle, my base case is that markets will need some time to digest the move and build up support before it can make a move for a new high.

Therefore I expect a period of extended sideways chop with a downward bias.

However, with the improving optics around the coronavirus along with a few of the charts I’m about to show you, I’m willing to start adding some risk at these levels because at the very least I think we may get a tradeable bottom.

Now onto the charts.

A couple weeks ago I was pointing to the SPX’s elevated forward PE ratio as one of the many reasons to be cautious on the market. Back then it was trading near a cycle high of roughly 20x. Following the selloff, it’s now around 18x next year’s earnings.

Equities don’t trade in a vacuum. Like everything else in this world, their value is relative. That’s why one of the key indicators I track is the rate of change of US BAA corporate yields. Rising yields mean bonds become more attractive on a relative basis to stocks leading to tightening financial conditions and vice-versa.

The BAA yield RoC is nearing all-time cycle lows. Note the other two times it’s been near these levels it has coincided with the start of major bull legs….

The SPX’s dividend yield’s spread to the 30-year Treasury is at its second widest point in history; with only the depths of the GFC beating it.

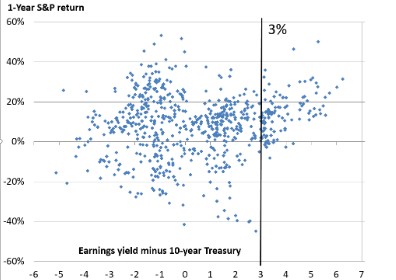

But since US corporates prefer buybacks over dividends, let’s use the earnings yield to gauge the equity risk premium (SPX earnings yield – US10yr) on offer.

At 3.8% it’s the fattest its been since early 2016.

According to Bloomberg, “Historically, when the equity risk premium climbs above three percentage points, the S&P 500 is all but guaranteed to post a positive return in the next 12-months”. TINA (there is no alternative) can be a hell of a drug for equities in a zirp world.

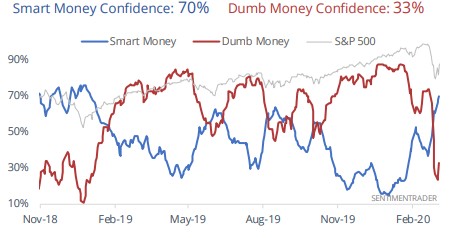

And finally, SentimenTrader’s Smart/Dumb confidence spread is back at levels that were last seen at the start of 2019, right before the rally.

I’ll be honest, I don’t have anywhere near the conviction to buy here that I did, say last October or back in Dec/Jan 19’.

Sometimes in this game, the odds are clearly stacked and sometimes… not so much. The great thing about trading and investing is that, unlike poker, we don’t have to pay an ante. We can sit out completely and wait for our setup.

Personally, the above is enough for me to start testing the waters on the long-side by adding some risk. There’s a few individual stocks with great setups and strong fundamentals which give us killer risk-reward entry points. I’ll be sending out a write-up on these names to Collective members later this afternoon.

Keep your head on a swivel and manage your risk.

Thank you for reading.