***The following is an excerpt from a report sent out to Collective members over the weekend***

As for what I think now, I believe that the health, economic, and market impact of the coronavirus will be much greater than most people are now conveying. For example, the profit losses for businesses are likely to be many trillions of dollars so that governments protecting just the companies would cost a significant percentage of that amount of money. Additionally, the amount of money to protect just those individuals who will be devastated by the virus will also be enormous.

To do that, fiscal policymakers (I.e., heads of state and legislators) will have to create massive amounts of spending and distributions of money that will be distributed as “helicopter money.” That is happening now in many ways such as President Trump’s $1,000 checks to people. Where will that money come from? The fiscal policymakers don’t have that money because they don’t create it (the central banks create it), so they will have to borrow that enormous amount of money at a time when lenders don’t have much money to lend because most people and companies are losing money. That will drive up interest rates, which would be even more devastating for everyone. Central banks will then have to decide if they will let interest rates rise or print a lot of money to buy those bonds.

As they are faced with that choice, they will have no choice but to print money and buy a lot of government debt to hold interest rates down the way they did in the war years. So now all eyes are on central banks to see if they will do that. This is the big paradigm shift that I previously spoke about.

Ray Dalio wrote the above in a post on Linkedin this past week (link here). While Dalio has become somewhat of a whipping boy on the Twittersphere these last few weeks due to the walloping his Pure Alpha fund has taken, he’s dead-on in regards to the seriousness of the economic impact this virus will have on the world.

And while the future is multi-path dependent, we now have enough data points to know that what we’re living through is extraordinary, it will be talked about in history books 50-years from now. It’s a major paradigm shift that will reshape the world in unfathomable ways, both for better and worse.

While we’re going to cover some of the more immediate impacts today, let’s first do a brief overview of where we’re at in the progression of COVID-19 and what the current best-educated guesses are as to how the next 3,6, and 12 months will look.

I updated the COVID-19 Cheat Sheet a few days ago with the latest numbers and resources I’m tracking (here’s the link).

The situation is evolving quickly and there are so many opposing hot takes out there that it’s easy to get overwhelmed or point to data to confirm a bias. The reality is that no-one knows where exactly we’ll be in 6-months time, there’s just too much non-linearity to hold a hard opinion with confidence.

It’s a great time to put your Bayesian hat on and work on updating your priors daily because that’s how fast the information flow is changing. A useful shortcut for this is to regularly check in on the Good Judgement COVID-19 Dashboard (link here).

This is the forecasting project put together by Phillip Tetlock author of the must-read book Superforecasting. The predictions are updated daily and are “aggregated from forecasts by professional Superforecasters, who qualified by being in the most accurate 2% of forecasters from a large-scale, government-funded series of forecasting tournaments that ran from 2011-2015 and, since then, by being in the top handful of forecasters from Good Judgment’s public forecasting platform.”

This allows us to harness the wisdom of crowds, specifically the wisdom of a crowd that is particularly good at forecasting, to get a sense of how the severity skew of this thing is evolving. Here’s a summary of what the current median forecasts are projecting:

-

- Between 53 million and 530 million total COVID-19 cases worldwide by March 31, 2021.

- Between 800,000 and 8 million total COVID-19 deaths worldwide by March 31, 2021.

- Between 2.3 million and 23 million total cases of COVID-19 in the US by March 31, 2021.

- Between 35,000 and 350,000 COVID-19 deaths in the US by March 31, 2021.

These forecasts have been creeping higher over the last few weeks as more information becomes known. The range is considerable even within each bucket and that’s because the cone of plausible outcomes is wide and the situation is incredibly reflexive… much of the outcome is dependent on the actions we take now.

The most recent credible research points to two practical options for tackling the virus; neither of them painless. These are (1) mitigation and (2) suppression. Imperial College published a paper last week where they modeled the outcomes for each approach and discuss the pros and cons. Here’s a link to their paper as well as a link to a good laymen’s summary of their findings by MIT Technology Review.

I’ll explain the core of their findings here along with what we should expect as policy in the coming months.

-

- Mitigation: This approach is focused on “flattening the curve” through targeted isolation of active cases and quarantining households.

- Suppression: This approach uses a broad range of measures such as widescale shutdowns of non-essential businesses, forced at-home seclusion, and closing of all schools/universities.

Mitigation is intended to be a speedbump in order to buy the healthcare system precious time and spread out the onslaught of severe cases. Suppression aims to stop the virus dead in its tracks.

According to the findings of the paper, if the virus were just left to spread it would kill 2.2 million people in the US and 500 thousand in Britain by the end of summer. Using a mitigation strategy, they conclude that the two countries would at best be able to cut these numbers in half. And this doesn’t account for the higher fatality rate that would result from our healthcare systems being overwhelmed. Which, as the paper points out, would be catastrophic.

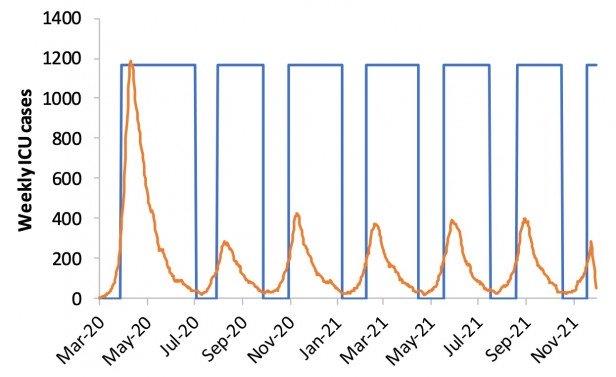

The Imperial College researchers found that even under the best mitigation strategy we’d still end up with a surge of critical care patients 8x larger than what the US or UK healthcare systems can cope with. The chart below illustrates this point. The red line is the current number of ICU beds.

This is why most countries are opting for the suppression strategy. Suppression is what China implemented in Wuhan and which brought the spread of the virus to a halt — at least temporarily and at a great economic cost.

One of the problems with this approach is that by keeping infection rates low it leaves many people susceptible to the virus. And as long as someone in the world has the virus, breakouts will keep reoccurring without drastic measures to control them.

Take the case of “Patient 31” in South Korea for example. South Korea did an excellent job of containing its initial outbreak but then a single infected patient unknowingly went on to infect hundreds of others, spawning another outbreak which led to the formation of many new clusters. The NYT has a great series of interactive graphs that show how easily this virus makes its way around the world (link here).

To avoid this, countries must ratchet up suppression measures each time the disease resurfaces. This is exactly what the team at Imperial College proposes doing. Every time admissions to intensive care units (ICUs) begin to spike, we enact extreme social distancing measures which we then relax once admissions begin to fall. Here’s how that approach would look.

MIT Technology Review explains the approach as the following (emphasis by me):

The orange line is ICU admissions. Each time they rise above a threshold—say, 100 per week—the country would close all schools and most universities and adopt social distancing. When they drop below 50, those measures would be lifted, but people with symptoms or whose family members have symptoms would still be confined at home.

What counts as “social distancing”? The researchers define it as “All households reduce contact outside household, school or workplace by 75%.” That doesn’t mean you get to go out with your friends once a week instead of four times. It means everyone does everything they can to minimize social contact, and overall, the number of contacts falls by 75%.

Under this model, the researchers conclude, social distancing and school closures would need to be in force some two-thirds of the time—roughly two months on and one month off—until a vaccine is available, which will take at least 18 months (if it works at all). They note that the results are “qualitatively similar for the US.”

As of right now, our baseline should be to expect roughly 18-months of rolling suppression measures. This is huge. Never in history has anything like this been done before. It’s going to stress the global economy and financial system in ways that’s never been seen. It’s also completely necessary as it’ll save the most lives and prevent our healthcare systems from total overwhelm.

Can this outlook change over the next month? Absolutely… we’re in unchartered waters and the situation is incredibly fluid. This is just the best guess we have at the moment and so should be our baseline; one we’ll continue to update daily as new info comes in.

The Volatility Machine: Small Business Balance Sheets

Macro is just an aggregate of what happens at the micro-level. And it’s at the micro where we’re most susceptible to cascading shocks.

Consider the following points.

The US economy is 80% service-based. This means much of our economy is dependent on in-person shopping, gatherings, face to face meetings etc…

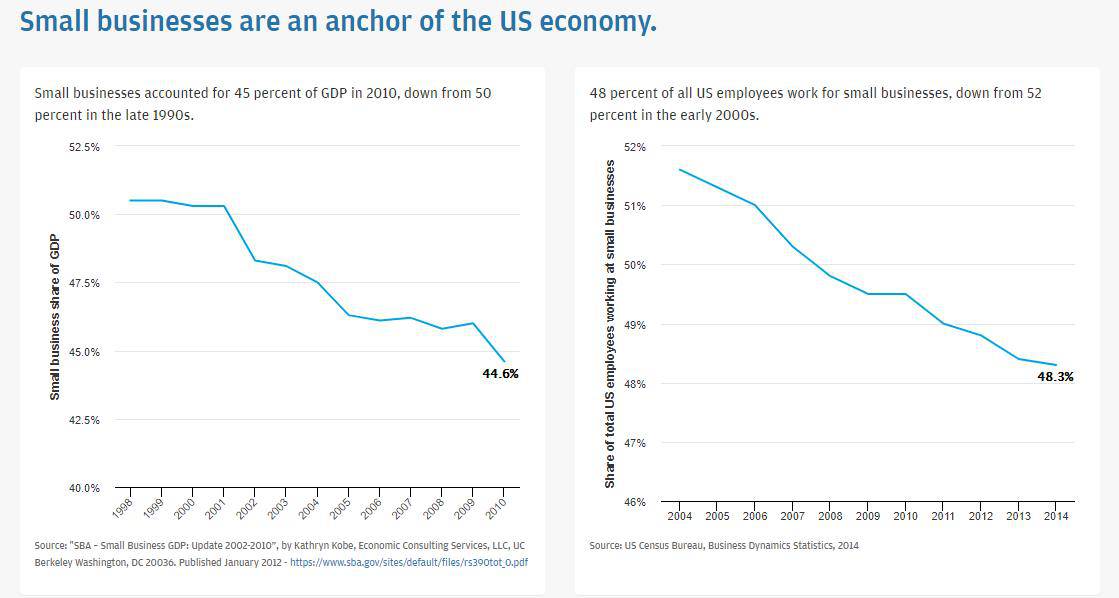

Small businesses contribute roughly 45% to our GDP, comprise 88% of total businesses, and employ approximately half of the US labor force (charts from JPM).

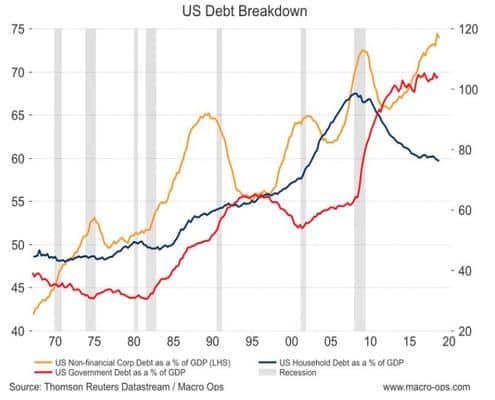

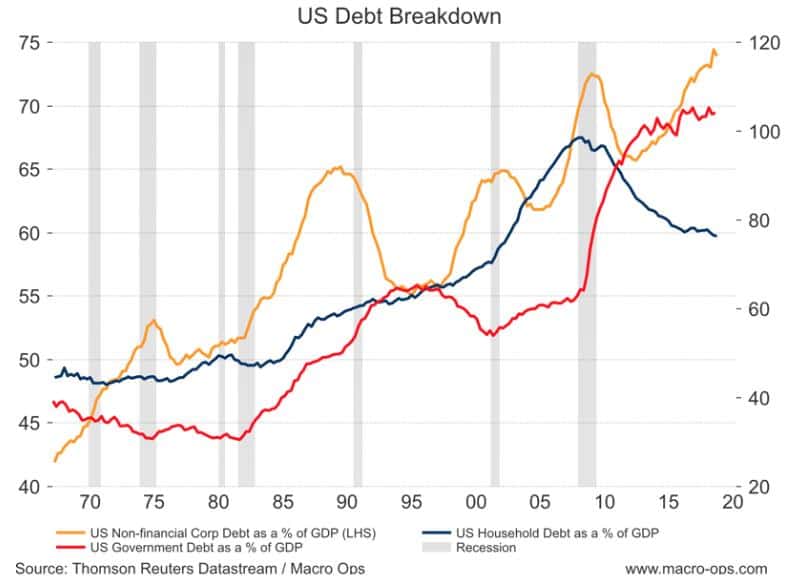

Corporate debt as a percentage of GDP is the highest its ever been.

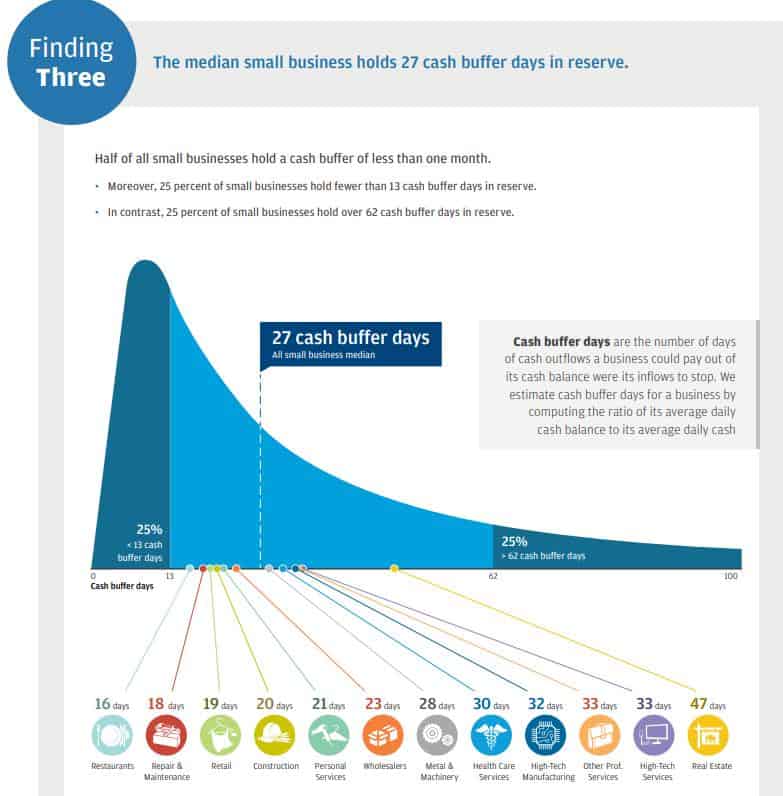

According to a study of US small businesses by JP Morgan, the median small business has less than 27 cash buffer days in reserve. And there’s a wide variance amongst industries. Healthcare services hold roughly 32 days of cash in reserve, while at restaurants just 16…

The study concludes that “Many small businesses may not have enough cash to continue operations in the face of a month-long loss of cash inflows due to an economic downturn or other negative shock”.

Put it all together and we get an economy that is largely dependent on social in-person interaction. It’s the most leveraged it’s ever been. Ever. In History. The average small business, which is the backbone of the economy, not only carries a lot of debt but also has less than a single month in cash reserves. We’re about to practice extreme seclusion — meaning no non-essential in-person interactions outside the home and closure of all non-essential businesses that require a physical presence — on a rolling basis for possibly 18-months.

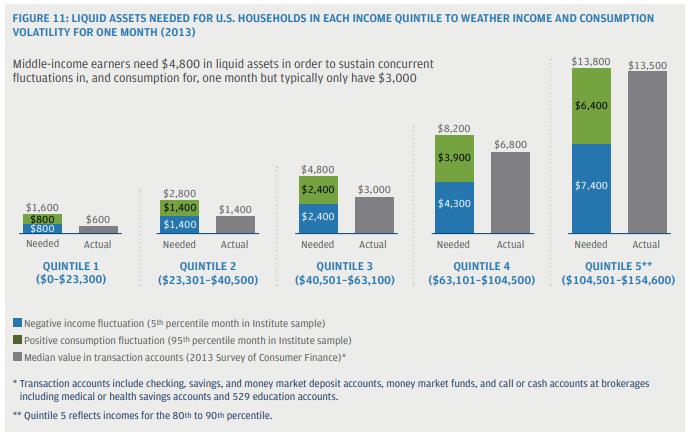

At an even more micro level, according to another report by JP Morgan, the typical US household — who’s also very levered up — holds less than $4000 in liquid assets. And here, just like small businesses, there’s wide dispersion and the data paints a stark reality. Nearly 30% of US adults have absolutely zero savings and only 1 in 4 have a rainy day fund but one that’s not enough to cover three months of living expenses.

At its roots, an economic system is just a collection of interlocking balance sheets. The more levered these balance sheets are the more dependent on cash flows the system is (ie, fragile). This is why it’s PARAMOUNT that governments act aggressively and quickly. Because it won’t take long for a feedback loop with disastrous effects to ripple through the system.

Even then, I’m not so sure they’ll be able to pull it off. The system is simply too large and too complex. And the potency of the cure that is needed will almost surely have unintended negative consequences — economic iatrogenic as Taleb might say.

I’ll be writing more on this in the weeks ahead. A particular point of interest and an area where I think will be the epicenter of this crisis, in more ways than one, is China. There are increasing signs that the property market may be beginning to falter. The government has exhausted its ability to leverage its way out of problems and the PBoC is buttoned in by the classic Mundell Flemming Trilemma.

Said another way, it’s going to be a long and wild ride in macro land. Better buckle up…

***The following is an excerpt from a report sent out to Collective members over the weekend***