Welcome back to another edition of The Weekly Systematic Setup. As we wrap up July, markets are digesting a whirlwind of geopolitical tensions, AI-driven disruptions, and shifting economic signals. This week, we’re diving into the convergence of themes like AI infrastructure demands, energy bottlenecks, commodity plays amid China risks, and defense sector tailwinds, all informed by fresh insights from recent reports. We’ll break down key rotations, update our high-conviction ideas, and outline actionable setups. Remember, our systematic lens focuses on regimes, relative strength, and cycle analogies to navigate this volatile landscape.

Key drivers I’m thinking about this week:

- Fed Rate Cut (and livestream?)

- AI-Energy Nexus: AI’s power hunger is real, data centers could demand nation-state levels of energy by 2030 (per Morgan Stanley). Bottlenecks in power grids and uranium supply are creating alpha opportunities in nuclear and infrastructure plays.

- Geopolitical Overhang: Ukraine risks (Pokrovsk potential fall) and China/Taiwan tensions (stockpiling signals) add volatility. Oil’s +12% since April defies bearish headlines, hinting at supply crunches ahead.

- Crypto Parallels: BTC/ETH rotation mirrors equities, ETH ETFs inflows hit $2B, with corporates holding $1.5B+ ETH. No meme mania yet means room to run.

- EU Tariff deal: done

- China: “Friends”…who dominate rare earth exports, mining and supply.

- Japan: 2nm chip production was something Taiwan had a corner on. Japan, a place that is one of the best manufacturing countries in the world and about 53,000 US active duty troops stationed there. And we are currently producing 4nm chips in Arizona (where I live) with 3nm and 2nm chips manufacturing coming on line soon, is it imperative that the US defend Taiwan?

Market Overview: Rotations (?) Amid Regime Shifts

We’re still in the early to mid innings of a bull market, but we are watching for rotations. Large-cap leaders (MAG7 and AI infra) continue to dominate, but mid-caps and select small-caps are showing signs of life, echoing crypto cycles where BTC leads before alts catch fire.

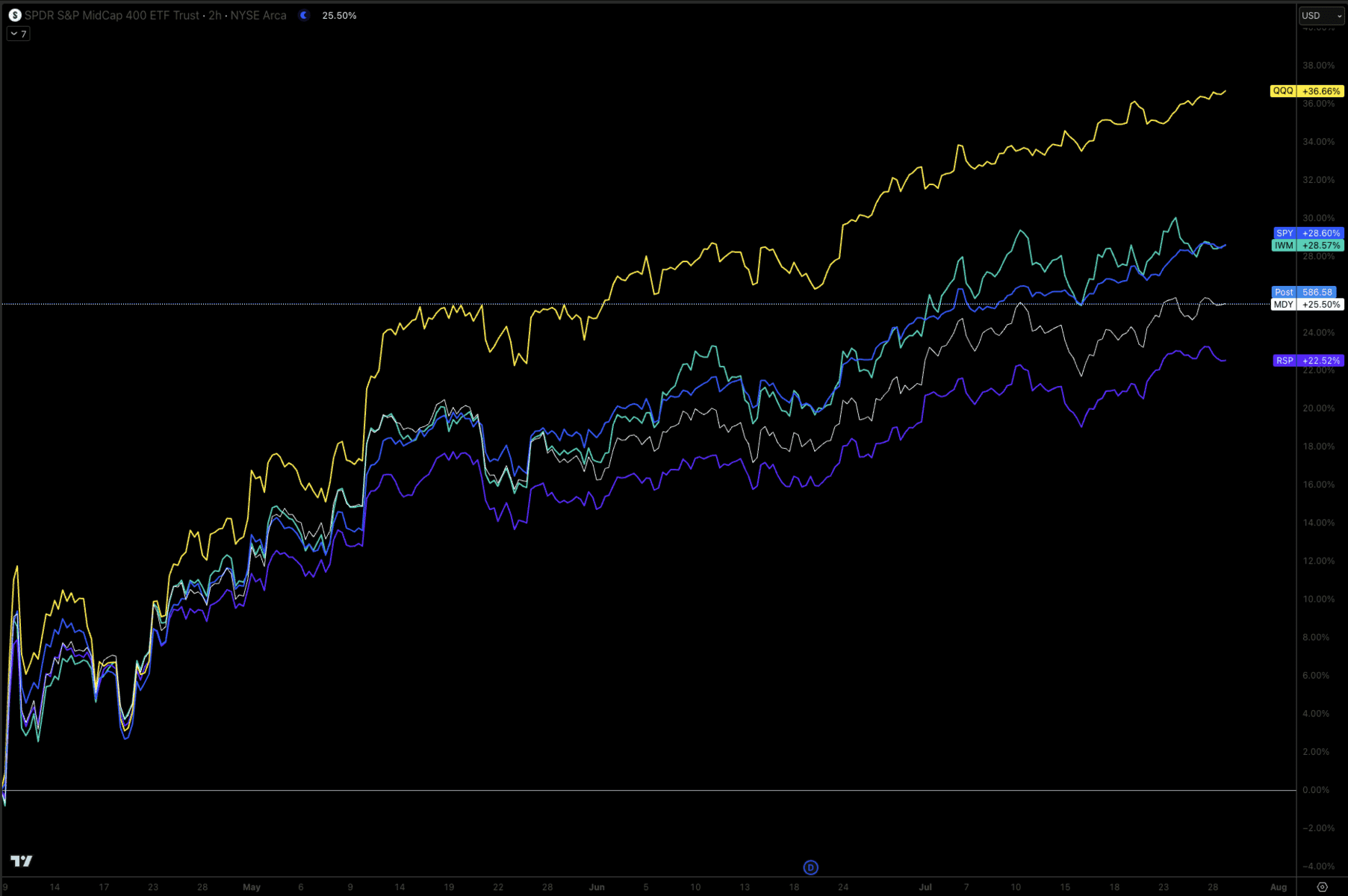

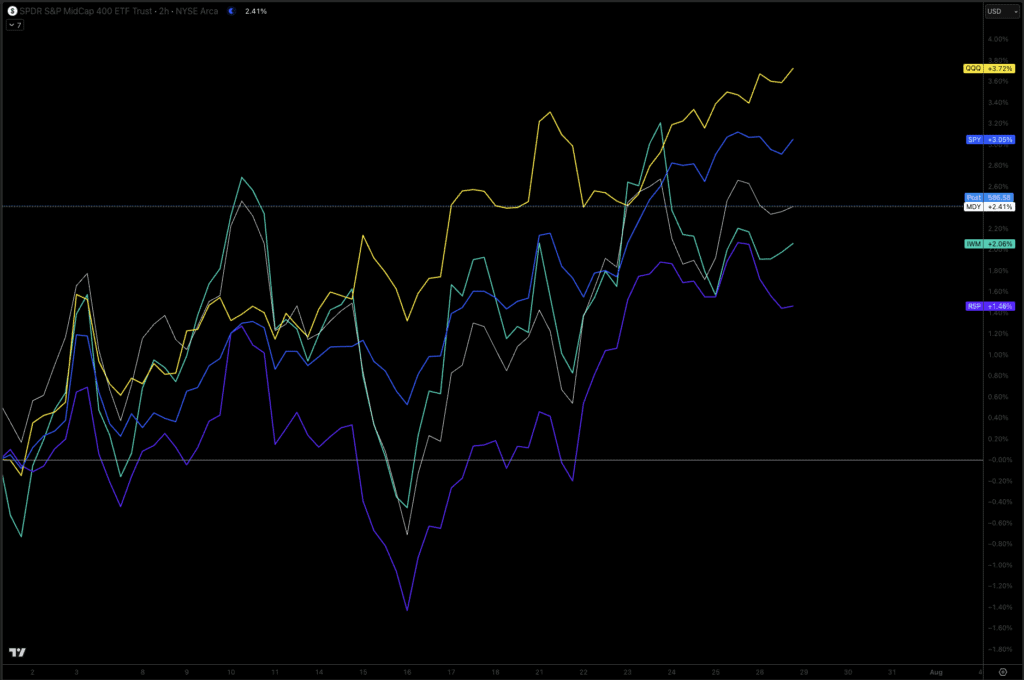

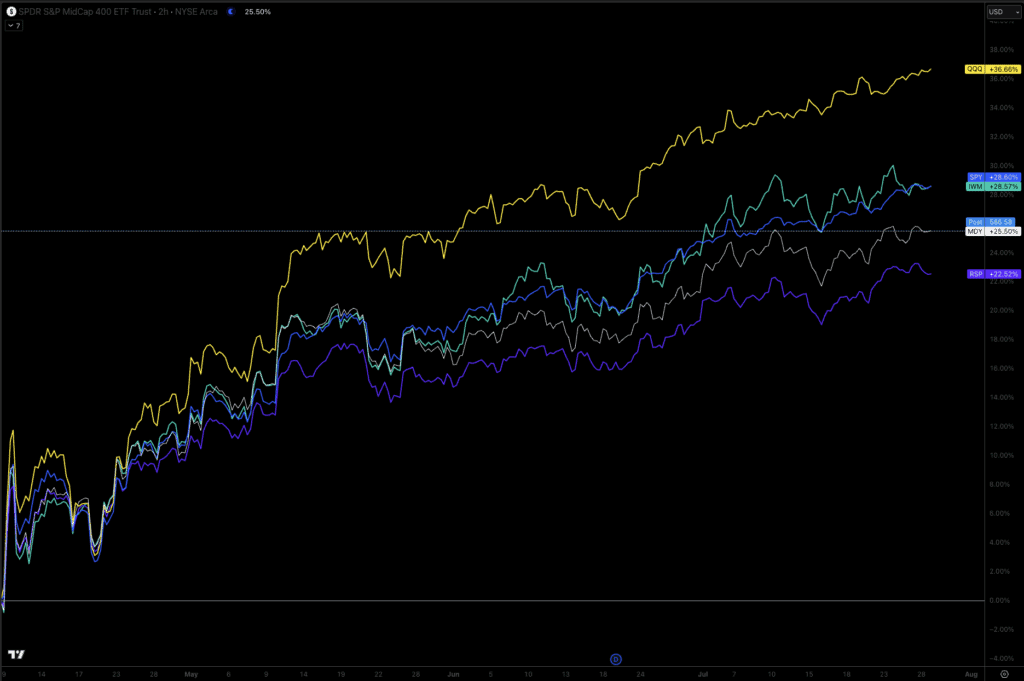

The S&P 500 (SPY) is up ~3% MTD, Nasdaq (QQQ) ~3.7%, while equal-weight S&P (RSP) lags at ~1.4%. This divergence screams “winners take most,” but it’s healthy: capital is flowing to quality before broadening.

This is since July 1, 2025.

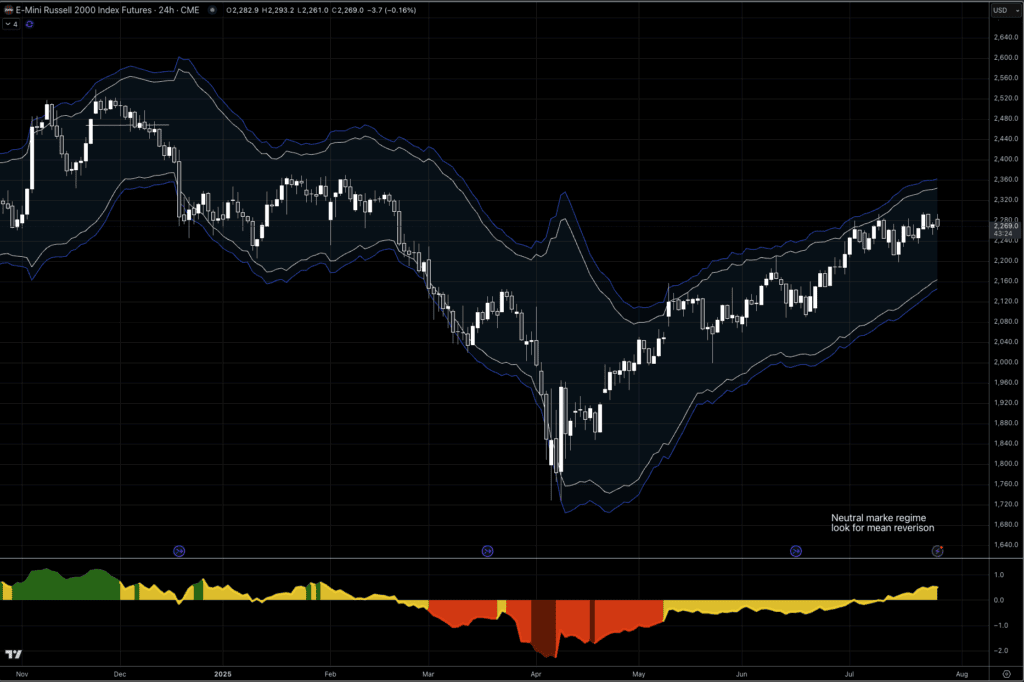

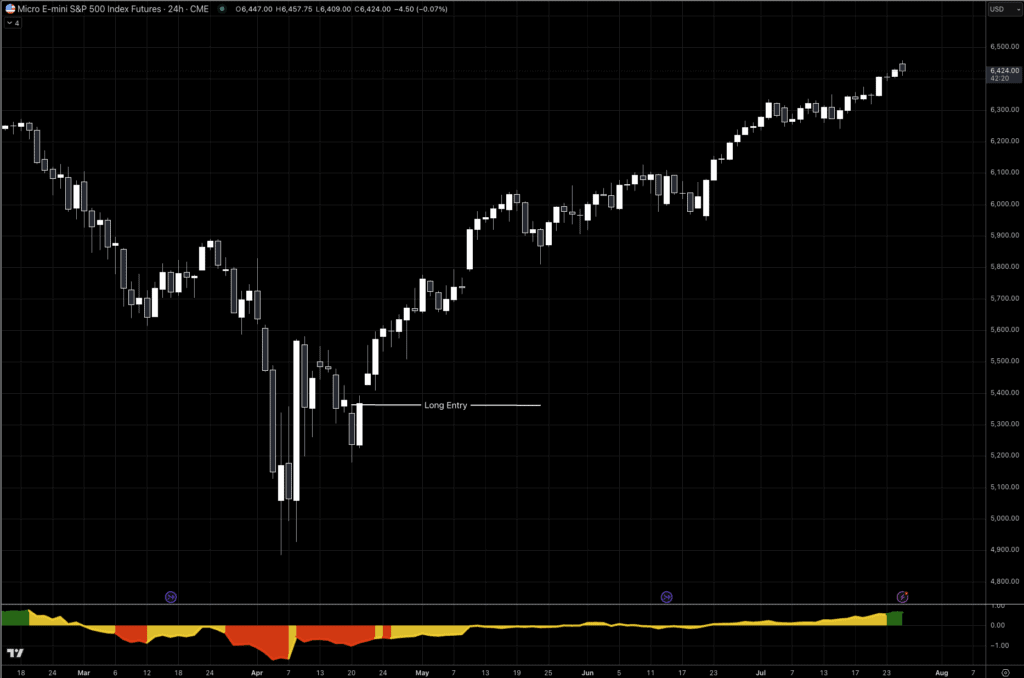

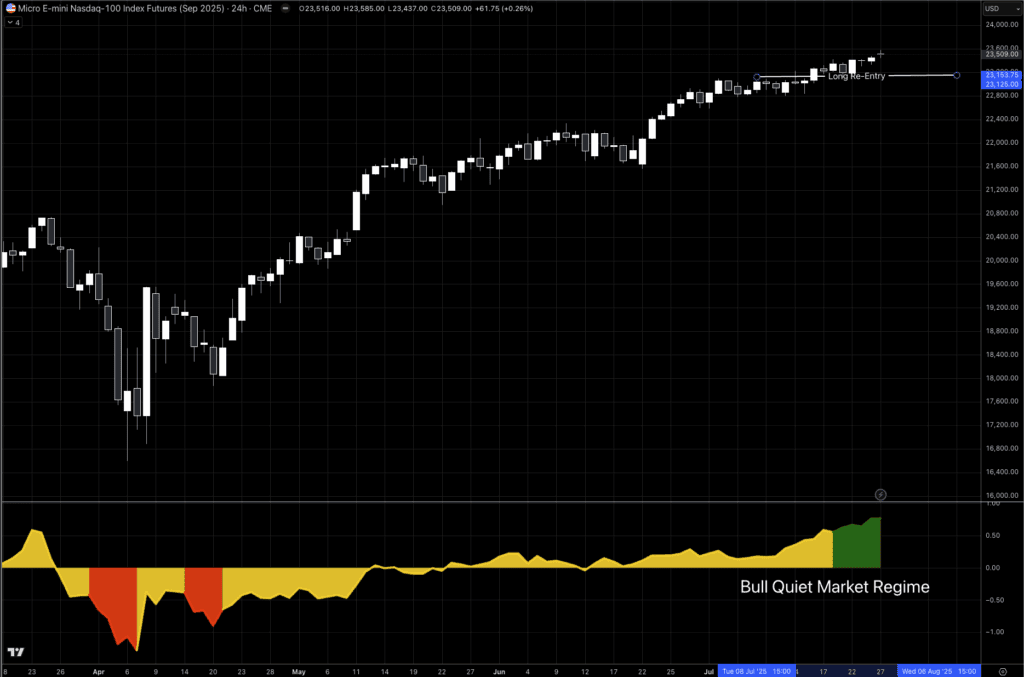

SQN regime check:

Russell 2000 remains Neutral Market Regime – We were short Russell last week but got stopped out of that short for a 50 Basis Point loss on the trade.

S&P 500 just entered Bull Quiet – we got long in April and remain in this position with no exit in sight.

NASDAQ 100 Bull Quiet Regime – We added to equity long exposure via NQ Futures between May and early July, exiting to tighten up volatility. The Macro Ops portfolio re-entered long two weeks ago and will look to increase this position as the trend continues.

Chart Spotlight: SPY vs. RSP vs. QQQ vs IWM vs MDY (Since April Lows)

Leaders continue to lead since the April lows, note the low volatility trend in $QQQ.

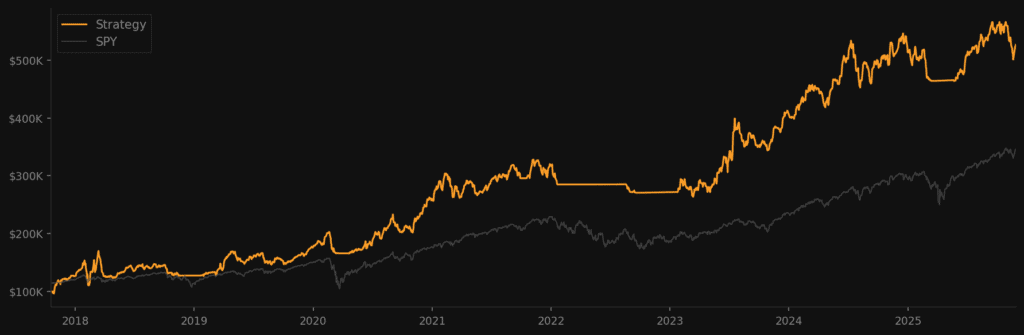

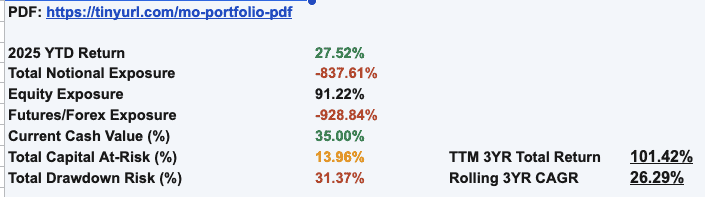

Returns YTD – Macro Ops Portfolio

Asset Class Breakdown

Equities: Stick with Winners, Eye Rotations

In a world where software is free (AI essentially has made it free) the MAG7 leaders are the ones with the war chest to divert spend from software developers to paying for infrastructure.

MAG7/AI infra remains the core, Oracle’s +52% cloud revenue and +115% multi-cloud uptake underscore the boom.

But rotations to mid-caps (e.g., software via BofA DevSecOps survey: +11% budgets, AI in 61-80% workflows) signal broadening.

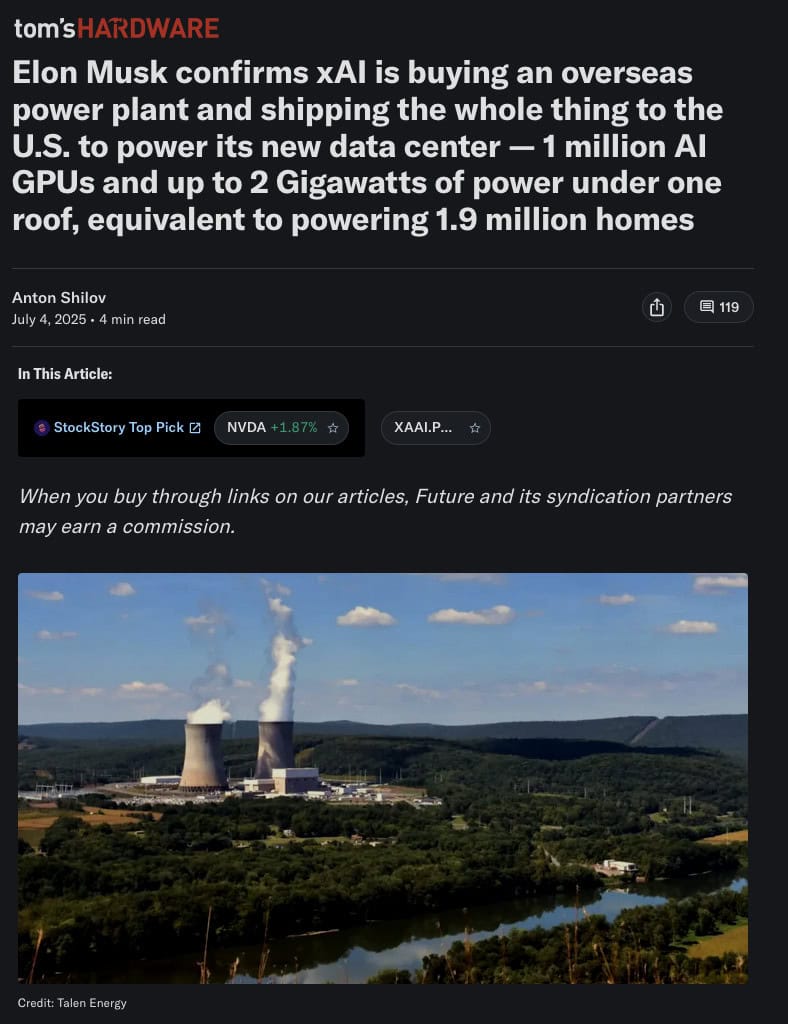

Elon buying an overseas power plant.

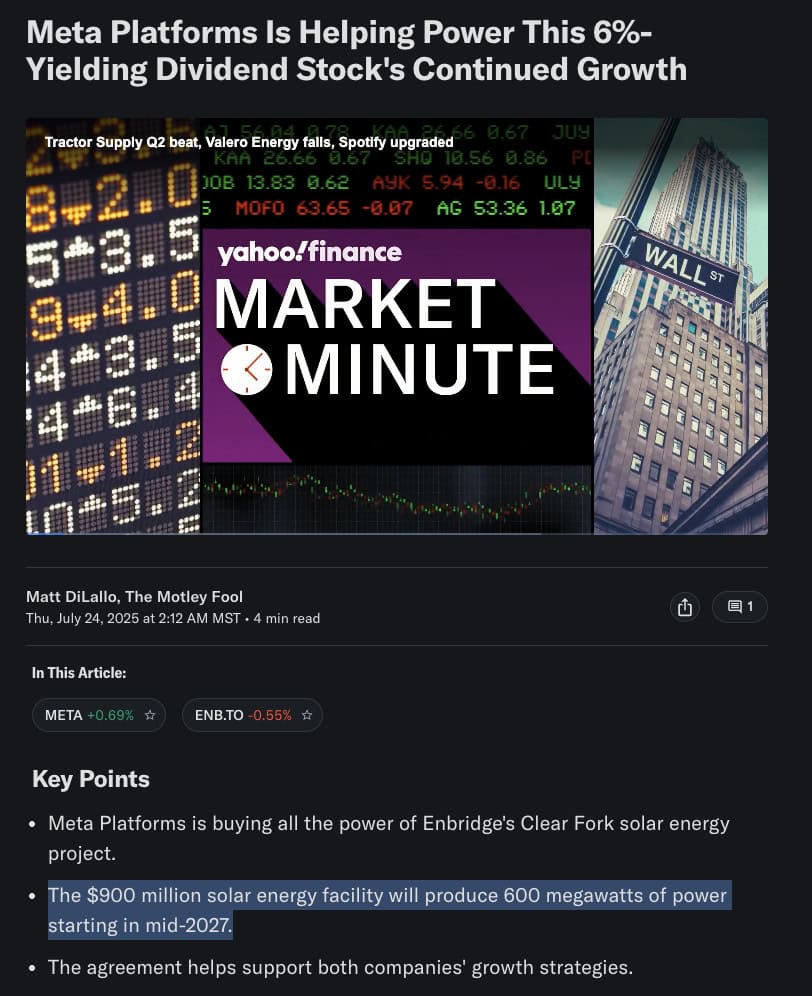

Meta is buying 600 Megawatts of Solar power

I live in Arizona, and the data center growth is palpable:

Meta’s Mesa Data Center:

A five-building, 960,000 sq ft facility is under construction in Mesa, representing an $800 million investment.

Google’s Expansion:

Google is also building a data center in Mesa, further solidifying the area’s status as a tech hub.

Stream Data Centers’ Hyperscale Campus:

In Goodyear, Stream Data Centers is developing a 157-acre campus with the potential for 280 MW of critical load.

Other Notable Projects:

Iron Mountain, NTT Data, Stack Infrastructure, and Aligned Data Centers are also expanding or building new facilities in the Phoenix metro area.

Why Arizona?

The state offers a business-friendly environment, including tax incentives, affordable land, and a skilled workforce, making it attractive for data center development, according to NOVVA Data Centers.

Energy & Nuclear: Powering the AI Beast

I continue to dig into the energy and energy security sectors.

AI data centers could add 62-128GW demand by 2028, straining grids.

Uranium’s structural deficit worsens, demand +20-40k tonnes of uranium by 2040.

Geopolitics: DRC/Rwanda peace unlocks minerals but risks violence; China’s stockpiling (crude reserves near full) signals Taiwan prep.

How Crypto Has the Potential to Suck All the Capital Out of Legacy Markets

In the evolving landscape of global finance, cryptocurrency is no longer a fringe experiment, it’s a black hole for capital, steadily pulling funds away from traditional, or “legacy,” markets like stocks, bonds, and commodities.

Crypto Treasury Companies

In 2025, we’re witnessing an institutional tidal wave: Bitcoin treasuries, tokenized assets, and stablecoin surges are reshaping how money flows. It’s a structural shift where crypto’s efficiency, liquidity, and borderless nature could drain trillions from outdated systems. But is this inevitable, or overhyped? Let’s break it down with data from recent analyses.

While Bitcoin (BTC) has long been the poster child for crypto treasuries, think Strategy’s (formerly MicroStrategy) massive holdings or Tesla’s early experiments, the narrative is evolving. By mid-2025, altcoins (alternative cryptocurrencies) are gaining traction as treasury assets, with public companies diversifying into Ethereum (ETH), Solana (SOL), Sui (SUI), Hedera (HBAR), Binance Coin (BNB), and others.

This shift isn’t just speculative; it’s driven by staking yields, faster transaction speeds, and blockchain-specific utilities that BTC lacks. As of today, corporate altcoin treasuries are estimated to hold billions, potentially accelerating crypto’s capital drain from legacy markets like equities and bonds. Let’s break it down.

Ethereum (ETH) leads the altcoin treasury wave, with public companies amassing over $3.2 billion (around 865,000 ETH) by early 2025. ETH staking rewards offer 3-5% yields (post-Merge), turning ETH into a cash-flow generator, unlike BTC’s pure store-of-value play. GS Crypto notes $1.5B in ETH bought by companies last month alone, with ETH ETFs inflows at $2B, corporate treasuries are the quiet force here.

Solana’s (SOL) low fees and high throughput make it a treasury contender, especially for DeFi-heavy firms. BeInCrypto reports SUI, HBAR, and SOL as top 2025 picks, with SOL uptake rising amid ecosystem growth. Staking yields ~6-8%, and its meme coin ecosystem (e.g., for viral marketing) adds utility. Public companies are amassing SOL for treasury diversification, per Yahoo. Axios notes firms pivoting to altcoins like SOL for risk-adjusted returns beyond BTC.

The treasury game isn’t ETH/SOL-exclusive:

- SUI: Spotlighted in Mill City’s $450M raise; its Move language appeals to secure treasuries.decrypt.co BeInCrypto calls it a 2025 uptake leader.beincrypto.com

- HBAR: Hedera’s enterprise focus draws treasuries; CoinDesk reports BNB/HBAR rallies tied to treasury announcements.beincrypto.com

- BNB: Outperforming ETH/SOL in July 2025 (per CoinDesk), with CEA Industries and Liminatus Pharma building BNB treasuries ($500M raised).coindesk.com DWF Labs notes BNB’s yield farming perks.dwf-labs.com

- XRP: Ripple’s cross-border utility shines; Yahoo lists XRP in altcoin treasuries amid regulatory wins.

Tokenization: The Legacy Market Vampire

Crypto’s real weapon isn’t treassury companies, it’s tokenization, turning illiquid assets like real estate or art into tradable tokens. BIS’s 2025 Annual Report questions crypto’s role in next-gen finance but acknowledges its potential to redefine systems.

A SSRN paper on “Crypto and the Evolution of Capital Markets” argues crypto previews on-chain traditional assets, absorbing capital by slashing costs and boosting accessibility.

Risks and Counterpoints: Not a Total Vacuum… Yet

Ok, now for a dose of clarity from my end.

Crypto isn’t invincible, I’m aware. Volatility shocks (e.g., DeFi/AI drops of 91-81%) remind us of risks. Regulation looms, PwC highlights 2025 shifts integrating crypto into capital markets, potentially slowing the suck if rules favor traditional finance (tradfi).

And while Bitcoin decouples, correlations could re-emerge in downturns.

Trading crypto is viscous, especially if you are susceptible to believing what everyone on the internet tells you.

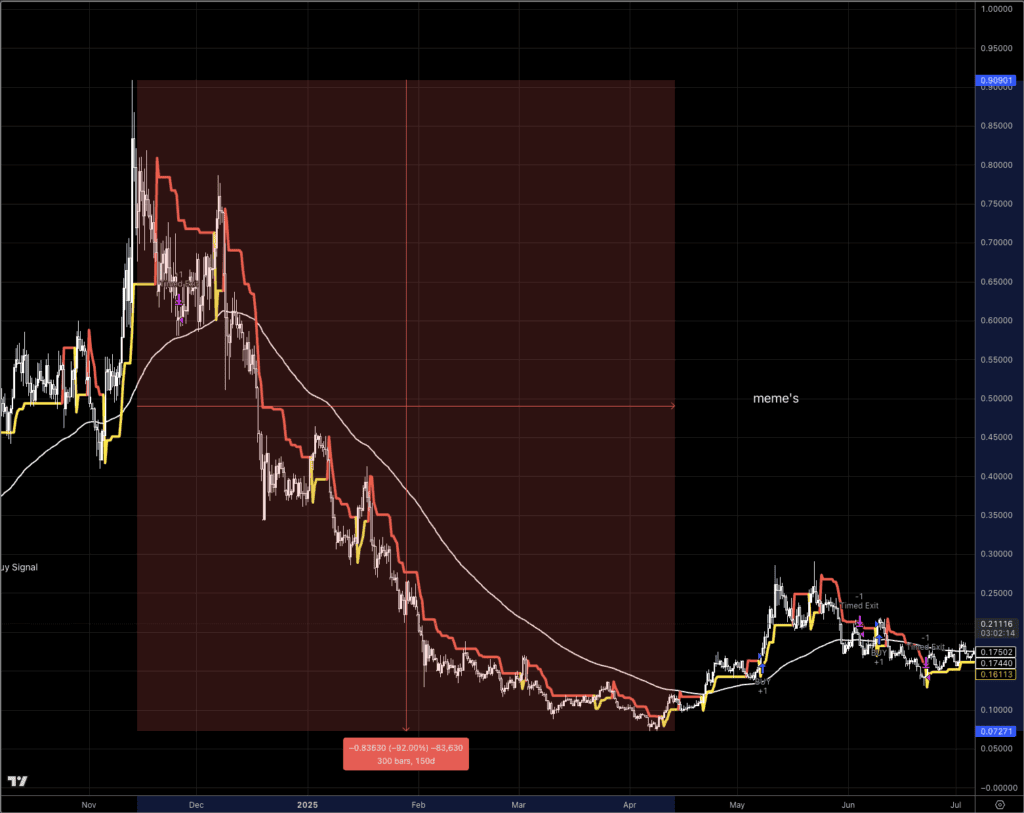

The large cap Meme coins sector lost -92% from post election highs to tariff lows.

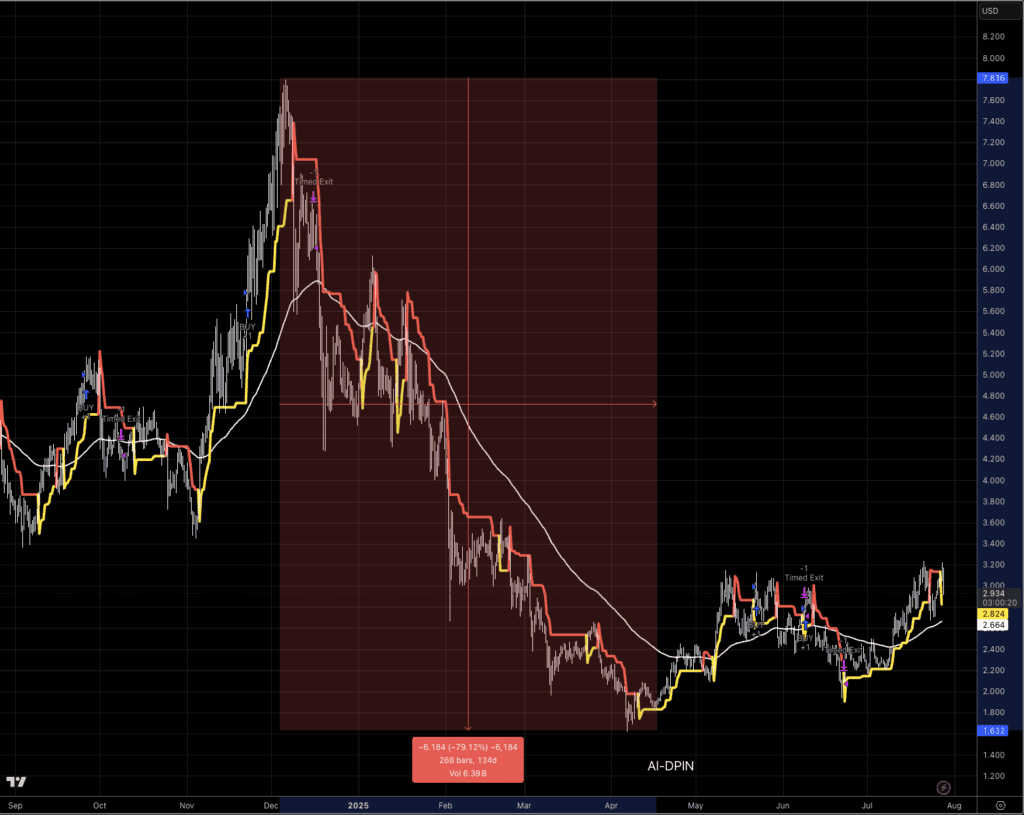

And the overhyped (especially in crypto) AI Sector took a beating, down -79% in the same period.

I have been trading crypto since 2014 and I don’t spend all night checking my phone/screens thrashing through all these down turns.

The Crypto Momentum system I run gets me in what’s moving, and gets me out, safely avoiding those massive drawdowns that everyone always gets sucked into from some narrative.

We catch the big moves, and sidestep the pain.

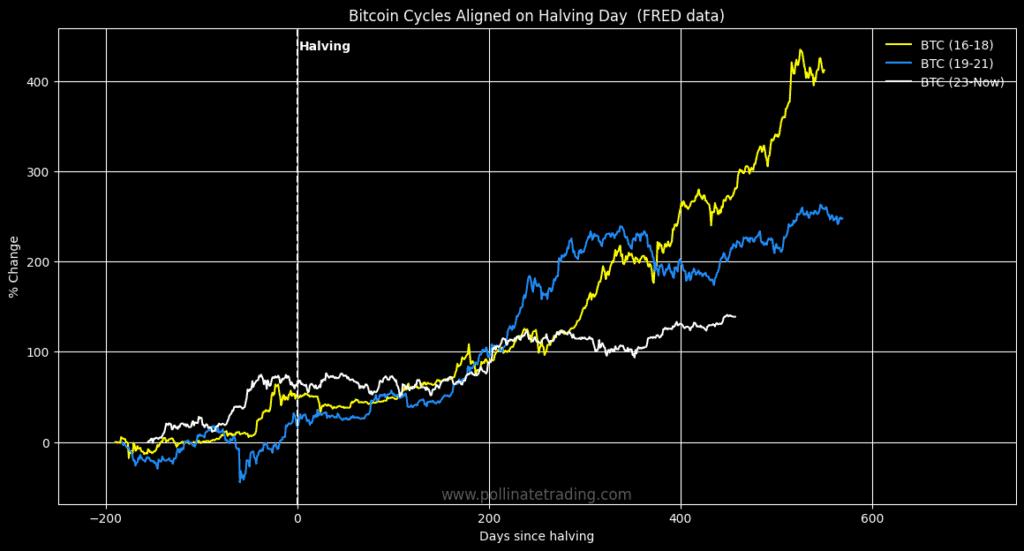

The Crypto bull markets tend to run hottest and bring the best returns in the latter part of the bull market (post halving cycle).

That’s where we are now, the white line is the current bull market, and the blue and yellow lines are previous bull markets.

That’s it for this week.