Everyone’s familiar with the classic 60/40 investment portfolio. If you’ve ever dealt with financial advisors, this is the standard allocation they’ll recommend. 60% of your money in the stock market, and 40% in bonds.

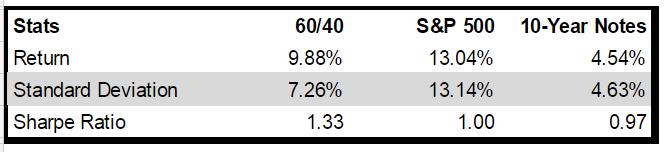

This has no doubt been a great strategy the past few years. Check out the statistics from Jan. 1 2010 to Jan. 1 2016 below:

The standard 60/40 portfolio grew an average of 9.88% per year. And not only that, but the Sharpe ratio was at a stellar 1.33!

The Sharpe ratio is a standard industry measure for calculating risk-adjusted return.

Sharpe ratio = (Mean portfolio return − Risk-free rate) / Standard deviation of portfolio return

It takes the average return, subtracts the risk free rate, and then divides that difference by the standard deviation. The result is the excess return per unit of volatility. It basically tells you how much risk and volatility you had to endure for that extra return.

A high Sharpe ratio means you’re getting more excess return for less risk. So the higher this ratio is, the better.

Most quantitative hedge funds shoot for a Sharpe near or above 1. So 1.33 is really something. Especially considering that it’s coming from a simple 60/40 portfolio…

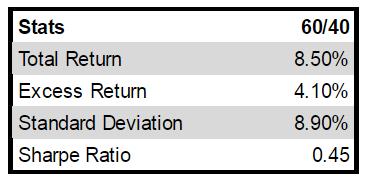

Now take a look at the statistics of a 60/40 portfolio from 1946 to now:

See the Sharpe ratio? It’s only 0.45… much lower than our current period’s Sharpe ratio of 1.33.

So our 70 year average is .45, but our current ratio over the last 6 years is 1.33.

What do you think will happen next? Do you believe we’ve reached a new era of permanently higher Sharpe ratios? An era where the new normal is high returns with low volatility?

Definitely not…

What goes up must come down. It’s a pretty good bet that the current 1.33 Sharpe ratio will revert back to the .45 long term average. Now you can do the math to find out what type of Sharpe ratios we need to print over the next decade to get back to this average, but long story short, it’s not pretty. Investors are in for a lot of pain as this number reverts back to the mean.

The worst part is that everyone has gotten used to this high return, low volatility environment. They aren’t prepared for the pendulum to swing back the other way. They never are. And that’s why we get boom/bust cycles and all the joy and misery that comes with them.

Going forward there are two possible scenarios that can play out which will send us back to our long-term average Sharpe ratio. The inflation scenario and the deflation scenario.

In the inflation scenario, bonds get killed.

Bonds as an asset class are very asymmetrically skewed right now. There’s a lot of downside, with not much upside.

As you know, when interest rates go up, bond prices go down. And at this point we’re near the zero bound in interest rates. There’s not much room for the Fed to maneuver to the downside. But the upside is wide open.

In general, longer term bonds (like the ones in a 60/40 portfolio) are more sensitive to interest rate changes than shorter term bonds. This is explained through the concept of “bond duration”, which we won’t go into right now.

What you do need to know is that there’s a lot of risk to the price of these bonds if interest rates move higher from here.

The Wall Street Journal has a tool you can use to test the effect of various interest rates on different dated bonds. It includes a variety of countries’ bonds with different terms, from Italy’s five-year, to the US 10-year, and even France’s 50-year.

If you take a look at the US 10-year, you can see that decreasing rates by half a percent will cause the bond to rally 5%. On the other hand, raising rates by 2% will cause the bond’s price to drop 17%.

This is what we mean by asymmetry. The risk-to-reward is skewed for long term bond holders. There’s a lot more downside risk than upside reward.

Inflation will come back. And when it does the Fed will be forced to raise rates. Once they do, we’ll see long term bonds get dumped. The rout in bond prices will be detrimental to the standard 60/40 portfolio and will effectively bring our current Sharpe ratio back down to earth.

The second possible scenario is the deflationary scenario. This is where we get the entire global system delevering to reach a manageable debt to income level. Cash becomes king in this environment. People will start hoarding their money, refusing to spend. This will in turn cause a deflationary loop where less spending leads to less corporate profits, meaning lower incomes for employees, which again leads to even less spending. Stocks will face huge price declines as corporate profits deteriorate and investors get rid of their shares. Risk assets in general will fall as investors find higher (and safer) returns in holding cash. The standard 60/40 portfolio will suffer as the equity decline plays itself out.

We believe the deflationary scenario has a highest possibility of occurring. But in either case, we see major problems brewing for those holding the standard 60/40 portfolio. As this portfolio reverts back to its long term average Sharpe ratio, investors will be in a world of pain.