- Indices: Likely the bottom is in, longed SPY options (discretionary)

- Metals: No positions

- Energy: No positions

- Currencies: No positions

- Bonds: No positions

- Ags and Softs: Short Corn.

- Crypto: Long Bitcoin

Commentary

Earlier this week I wrote a post to our Collective Members that’s based off my major market bottom SQN Velocity tool. The S&P 500 bottomed last Monday.

I also shared it in a Tweet that you can read here and the previous instances of this tool signaling the bottom reference lows here.

I personally took a long discretionary position with $SPX options in my PA, which is not part of the Macro Ops portfolio.

The Quant Portfolio is also still in very high cash positions.

Here are Alex’s Macro thoughts going into this week…

The Volatility Breakout System (VBO)

This week my business partner Alex and I were speaking about low volatility systematic trading and how well it has performed during the recent period.

We run multiple systems within our portfolio, designed to keep volatility low and the trend in our equity curve rising in a smooth manner, and to keep us safe during periods of high volatility/crashes like the past few weeks.

He asked me to share some insights and the logic behind one of our longest running systems, specifically the Vol Breakout System (VBO).

I categorize it as a Fast Trend system, meaning it catches trends early but also exits them early.

This works well with setting up the other types of systems we run, slow trend, fast mean reversion and slow mean reversion, because either a fast trend turns into a more durable long term trend or it fails and mean reverts.

They are complementary systems to each other.

First, let’s talk about the VBO setup.

The idea is that volatility (price action based % change) has been squeezed into a very tight range, and we measure this with Bollinger Bands and Keltner Channels.

When the Bollinger Bands fit inside the Keltner Channels, that indicates a squeeze of volatility.

With the very tight range, mean reversion traders have become accustomed to placing limit orders and the tops and bottom of the ranges for reversals, with stop losses just outside the top and bottom of the ranges if they are wrong.

Also with tight ranges, breakout traders have orders placed above the ranges to take the trades if those ranges are broken.

Essentially there are larger than normal orders waiting just outside this range, and when these levels are breached, it causes a cascade of orders to be filled quicker than normal.

That opens the door for more active momentum traders to get alerted by rapidly rising prices on higher volume (in the case of longs), to join the party.

When all of this happens together we get the VBO (Volatility Breakout) trade.

It doesn’t work in all market regimes and on every asset.

We run it on a universe of 30 futures symbols, in 4 out of the 5 market regimes.

It doesn’t work at all in the Bear Volatile regime.

Additionally, using our market regimes, we adjust risk per trade and where we take profits, because the way we measure the different market regimes is by price volatility.

You can read more about how we use Market Regimes in this post.

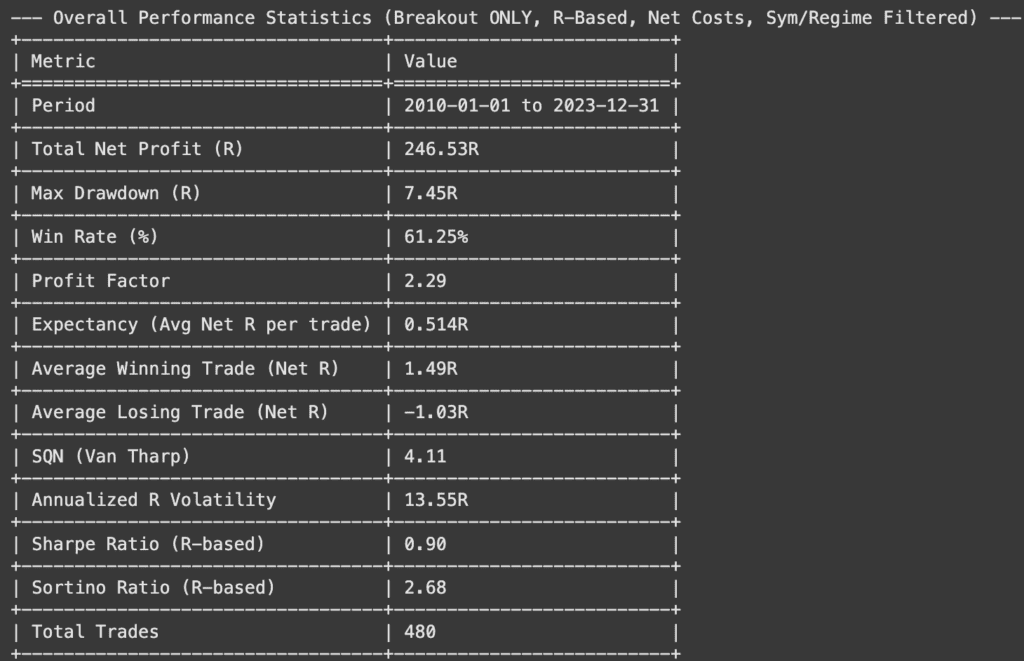

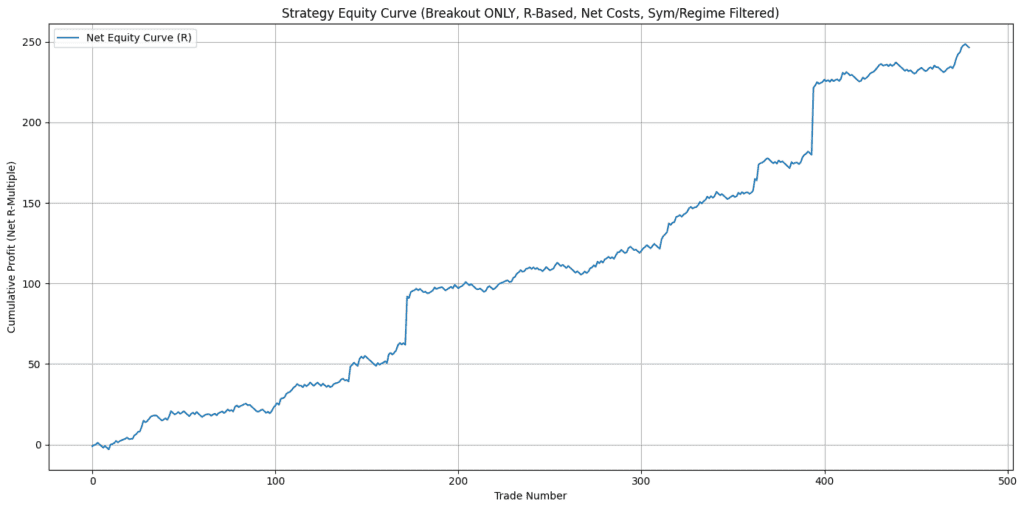

I ran a backtest of the VBO system on the 30 futures universe from 2010 to 2023 and here’s our results. Note that we are using R (risk) based results, not $ (dollar) based results.

There are periods where it goes sideways, periods where it goes down, and yes there were a few pretty big trades in there.

I want to be clear here, this is not a holy grail system that works all the time in every market.

For example, it does not work well with Nasdaq, S&P 500 and the Dow, which is odd because those indices have super strong trends.

But it does great with Russell 2000, which is more of a start and stop type of index.

That’s the point of this, it offers returns that are different from just buy and hold (beta) of the market.

Returns

- Quant Portfolio is up +3.4% on the year (change from last week -2.0%).

- Macro Discretionary portfolio is up +7.15% on the year, from a YTD high of over 15%. (change from last week -0.35%)

- SPX is down -8.81% on the year (change from last week +8.69%).

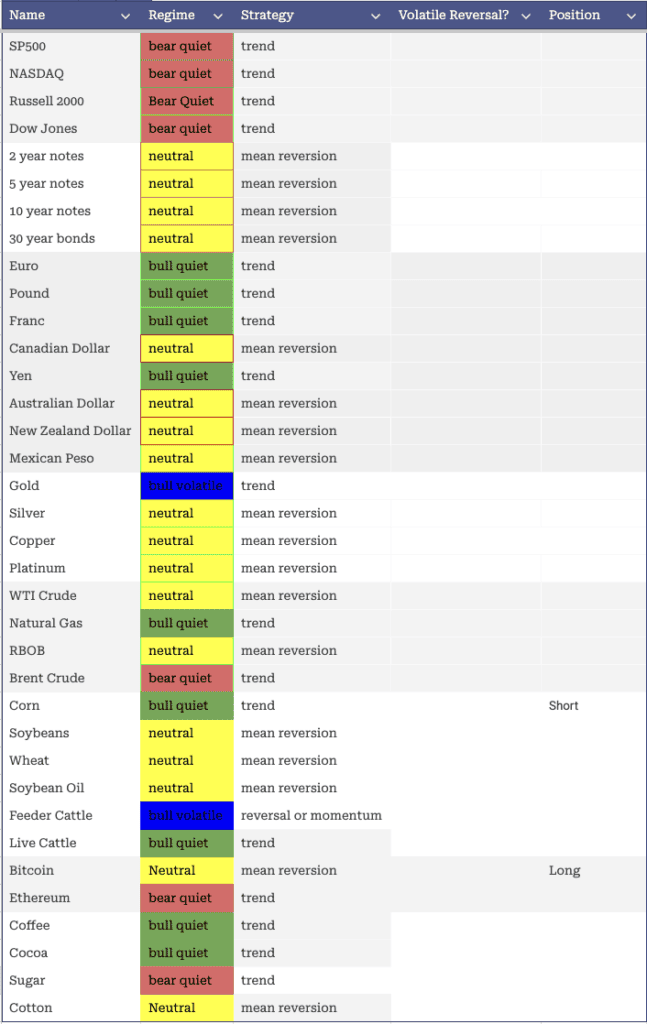

Regimes

Current Positions

Short $ZC (Corn) – Mean Reversion

Long $BTCUSD (Bitcoin) – Mean Reversion

Setups for next week

Metals-

Watching for Curvy Mean reversion long setups

Equities-

No setups in US Indices – Major market bottom signal fired, will be looking for mean reversion or fast trend systems to step in on the long side. The big issue is risk management, due to the large ranges lately.

Energy-

Watching for Curvy Mean reversion long setups

Ags-

Currently in Corn but not seeing anything else

Crypto-

Currently long Bitcoin a curvy mean reversion long.

If you are interested in the strategies that I use.

And you can work with me on building out your trading business in the Trading Thunderdome

Until then, stay disciplined.