Last year (almost to the day), I wrote a Long Pull titled “Building Confidence in APM.V & Getting More Bullish on PGMs.”

Here’s a snippet from the piece (emphasis mine):

“The PGM trade feels like a Molotov cocktail ready to explode. Think about it:

- The popular narrative of “EVs are the future. We won’t need ICE cars” destroyed PGM prices.

- Low PGM prices eliminated the incentive to increase supply, so all the significant producers closed mines, laid off workers, and hunkered down.

- Large speculators played the EV narrative thesis by shorting (in record size) palladium and platinum futures.

- No investor wants to touch a PGM stock trading at its lows.

Auto OEMs are now blatantly telling you that ICE engines will be around for another 5-10 years! This destroys the popular PGM narrative and unwinds the above trade.”

APM has played out well, but until last week, the PGM thesis didn’t. Prices couldn’t (or wouldn’t) break out of their trading ranges. Sibanye-Stillwater (SBSW) – often viewed as the token PGM trading vehicle – made new lows, and everyone thought EVs would rule the world.

Things look very different today. SBSW is up 130% from its trading-range lows, and palladium and platinum are up 31% and 56% over the past six months, respectively.

As I mentioned in last week’s Long Pull, our goal is to own the stuff that is working (i.e., Relative Strength Leaders) in our highest conviction industries and themes. It’s not more complicated than that.

This week, I update my PGM thesis using our new Investment Process Framework and pitch Valterra Platinum (VALT.LSE) as one of the best ways to play this leading thematic.

Before we dive into the piece, a quick note: We’re opening up our Macro Ops Collective enrollment until the end of the year.

The Collective is our premier service, offering discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders and investors dedicated to mastery.

We’re having a decent year (+25%), catching a few significant themes, discovering a few stocks nobody had heard of, and avoiding any major mistakes.

If you’re interested in our Trifecta Lens Framework and trading philosophy or want to eliminate the guesswork of position sizing, risk management, and market noise, check us out.

Click below and sign up.

Join The Collective

Alright, onto the piece.

Relative Strength Leaders: The Metals Complex

There are three parts to our “new” Investment Process:

- Weekly screen for relative strength leaders in all our key thematic areas across 6M and 1YR time frames.

- Develop a basket approach to portfolio construction and stock selection to express our key thematic areas.

- Optimize the portfolio to have the highest weighting in the leading relative strength names within the leading key thematic areas.

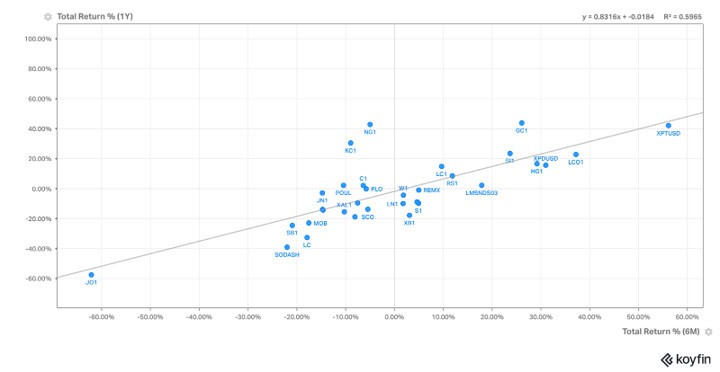

With that in mind, I present the following Koyfin Scatter Plot.

We should own the metals in the upper right-hand corner of the chart above. That means:

- Platinum: NICU, SPPP, SLP, VALT

- Cobalt: None

- Palladium: NICU, SPPP, SLP, VALT

- Copper: NICU, ARG, EMO.V

- Gold: IDR, APM

- Silver: APM

I’m surprised to see cobalt in there … but that research is for another Long Pull 🙂

PGMs represent our largest position within our Metals Complex thematic, with 15% notional exposure. That is what we want – to have the most significant weighting in the things that are working the best.

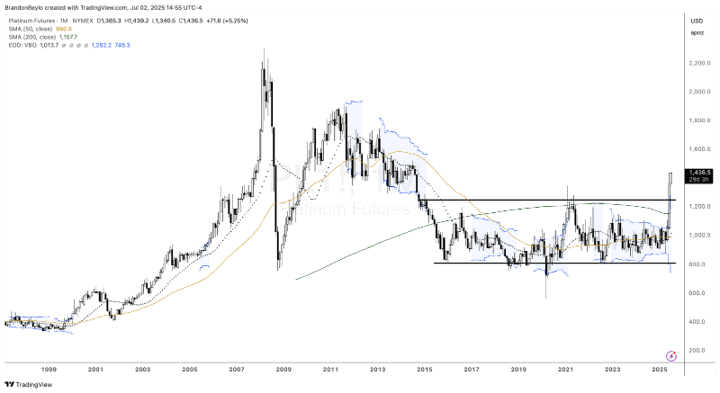

Look at the platinum and palladium charts.

These are charts you want to own, and I found the final PGM name to add to our basket: Valterra Platinum (VALT.LSE).

Valterra Platinum (VALT.LSE): The World’s Best PGM Producer

Valterra Platinum (VALT) is a newly independent PGM producer spun out of Anglo American in May 2025.

It is the world’s largest integrated platinum group metals (PGMs) miner, with operations concentrated in the Bushveld Complex of South Africa and the Great Dyke of Zimbabwe.

The company’s asset portfolio includes several long-life mining complexes (all 100%-owned) covering platinum, palladium, rhodium, iridium, ruthenium, osmium, and associated base metals (nickel, copper, cobalt).

Here’s the pitch: VALT is the world’s largest and lowest-cost PGM producer, with hundreds of years of mine life remaining from its 600 million ounces of reserve endowment. Assuming ~$1,800/oz for PGM prices, VALT would generate $2.6B in annual pre-tax cash flow at an $11B EV for a 23% FCF yield. It’s a world-class asset with unmatched reserve potential, trading like a distressed junior producer. The company pays out 40% of its cash in dividends. VALT should command a mid-cycle EBITDA multiple of 7- 8x, putting fair value around $18B – $20B (nearly 100% upside).

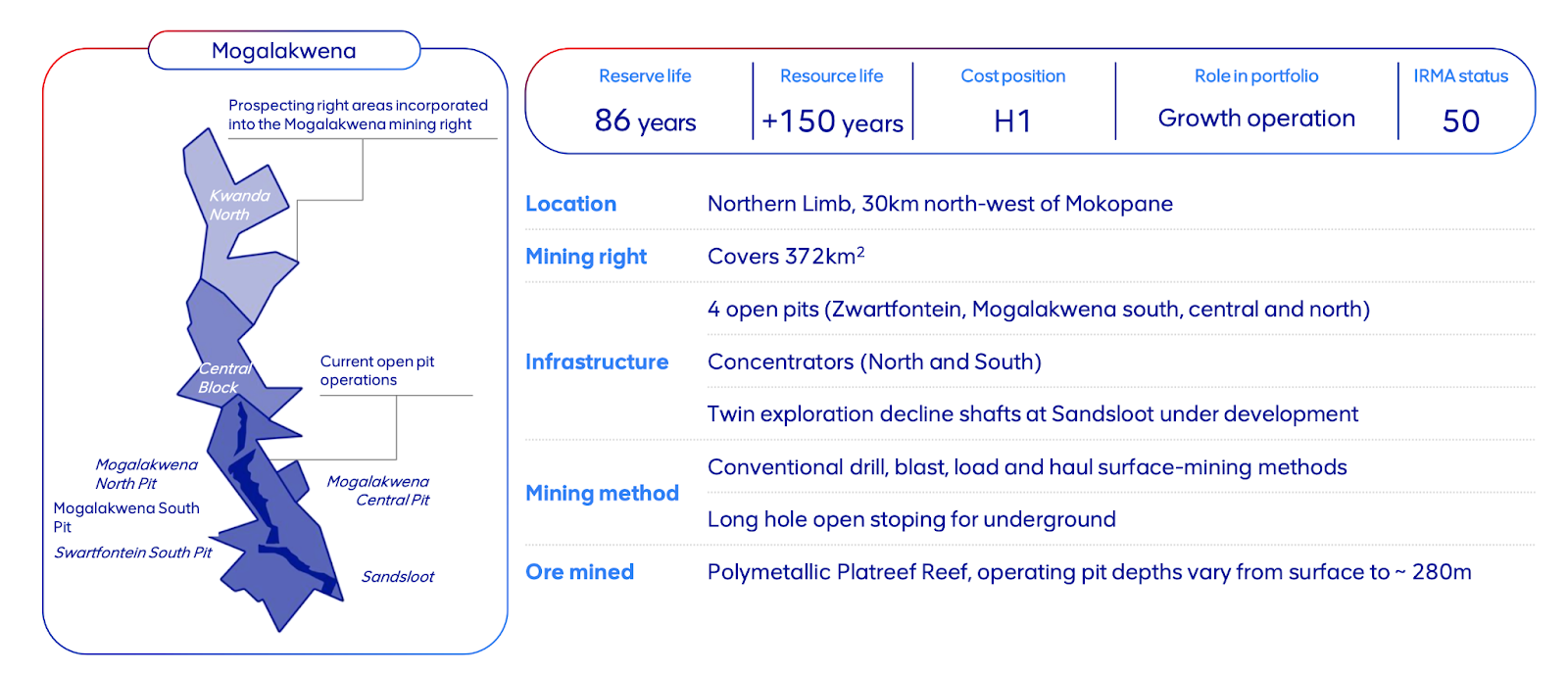

VALT’s Prize Asset: The Mogalakwena Mine

The Mogalakwena mine is the most impressive mine I’ve researched. It’s the world’s largest open-pit PGM mine, located on the northern limb of the Bushveld Igneous Complex (see below).

Pictures don’t do it justice – this thing is MASSIVE.

Any American football fans out there? If you stood at one end of the Mogalakwena Mine, you could fit over 25,600 football fields side by side before you reached the other end. It’s 40x larger than NY’s Central Park and twice the size of Manhattan.

The mine has 86 years of reserves and 150+ years of resources remaining. It produces ~1Moz/year of 3-4g/t PGMs through a mix of mostly open pit and underground mining at ~$900 – $1,000/oz AISCs.

VALT generates nearly $900M in free cash flow from Mogalakwena alone.

One interesting fact about Mogalakwena is that it integrates lower-grade open-pit ore with higher-grade underground ore. Over time, this results in higher average grades while maintaining cost discipline through the open pit scale economies.

The Amandelbult Complex

Amandelbult is an underground mining complex located on the western side of the Bushveld, comprising the Tumela and Dishaba mines. It’s higher-grade (5-6g/t) ore generates approximately $1,300/oz in revenue, making it one of the most profitable PGM mines in the world.

The complex has 46 years of reserves between Dishaba and Tumela, respectively, and another 75+ years of remaining resources.

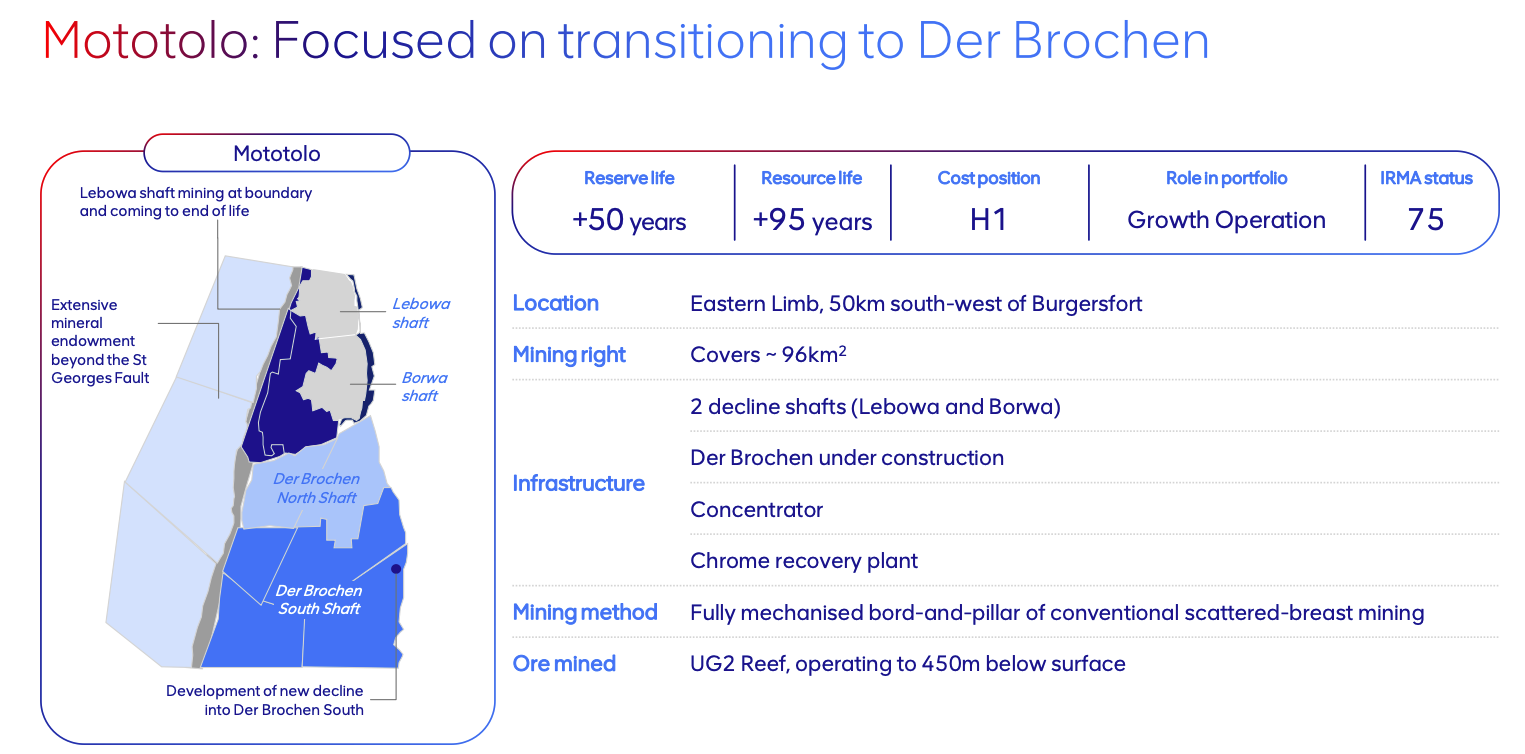

The Mototolo–Der Brochen Complex

The Mototolo mine (acquired by VALT in 2018) and the adjacent Der Brochen project, located on the eastern side of the Bushveld, have been combined into a single complex to replenish and expand ore from Der Brochen while winding down Mototolo’s Lebowa and Borwa shafts (see below).

Mototolo is another massive mine with over 50 years of reserves and more than 95 years of resources through underground operations. There’s also an AISC benefit from switching to Der Brochen ore. VALT estimates that AISCs at Mototolo will fall from ~$992/oz to $875/oz as the company shifts more production to Der Brochen (via higher chrome credits and operational efficiencies).

The company also operates the Unki mine, its smallest asset, which produces ~250,000 ounces per year. Finally, like APM, the company purchases ore from third parties to refine at its wholly-owned processing facilities (that adds another 0.9Moz – 1Moz).

On a consolidated basis, VALT produces ~3.0 – 3.4Moz/year of PGMs (Platinum: 44%, Palladium: 32%, Other: 24%).

Let’s discuss valuation and future cash flows.

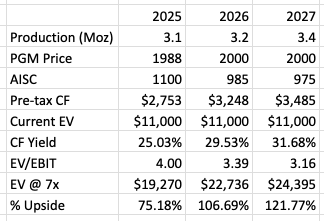

VALT’s Three-Year Outlook

Here’s my oversimplified 3YR model for VALT’s production and cash flow.

My 2025 PGM prices reflect today’s basket metals prices plus VALT’s split of metal production (see above). At current basket prices, VALT generates $2.75 billion in pre-tax cash flow (25% yield).

Should PGM prices stabilize at ~$2,000/oz, VALT would end 2027 with nearly $3.5B in pre-tax cash flow from expanded production at higher grades (remember they’re adding higher-grade underground ore to Mogalakwen). In other words, the stock trades at ~3x my estimate of 2027 EBIT.

Like I mentioned above, VALT is a Tier-1 producer with world-class assets at the lowest end of the cost curve. Those assets should trade around 7-8x mid-cycle earnings (comparable to prior cycle valuations), giving us ~121% upside from today’s prices.

Look, I don’t think VALT is a “multi-bagger” in the same way I view NICU, IDR, or APM (which was back at $0.72/share). But you can make 2-3x your money and get paid to wait for the PGM cycle to play out (VALT pays 40% of cash flow in dividends or ~$1.2B per year using the above scenario).

VALT offers the lowest-risk torque to higher PGM prices, and it should be a staple in any investor’s PGM basket.