Vilfredo Pareto was an Italian economist born in the mid-19th century who made an interesting discovery about land ownership in Italy.

While surveying his Italian city he found that 80% of the land was owned by only 20% of the population. After further inquiry, he found that this 80/20 distribution was prevalent in other cities as well. And in fact, this 80/20 rule didn’t seem to apply just to land ownership; but also income distribution, and revenue origination streams. Pareto had stumbled upon a naturally occurring power law.

A power law, as known in mathematics, is a relationship between two quantities such that one is proportional to the fixed power of the other. Power laws are embedded in the very fabric of the universe; applying to the size of solar flares, the populations of cities, and the intensities of earthquakes to name only a few.

The 80/20 rule, now known as Pareto’s law is often used as a guiding principle in business and productivity decisions. Trading and investing profits adhere to this power law too. In fact, they follow an even more extreme distribution of 90/10. Meaning, amongst great traders and investors, 90% of their profits tend to come from 10% or less of their trades. Let’s look at the following from Ken Grant in his book Trading Risk:

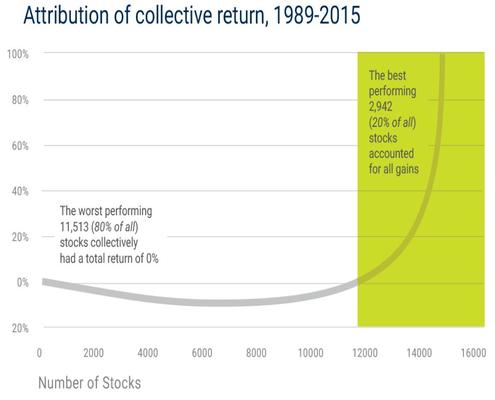

“Some years ago in my observation of P/L patterns, I noticed the following interesting trend: For virtually every account I encountered, the overwhelming majority of profitability was concentrated in a handful of trades. Once this pattern became clear to me, I decided to test the hypothesis across a large sample of portfolio managers for whom transaction-level data was available. Specifically, I took each transaction in every account and ranked them in descending order by profitability. I then went to the top of the list of trades and started adding the profits for each transaction until the total was equal to the overall profitability of the account.

“What I found reinforced this hypothesis in surprisingly unambiguous terms. For nearly every account in our sample, the top 10% of all transactions ranked by profitability accounted for 100% or more of the P/L for the account. In many cases, the 100% threshold was crossed at 5% or lower. Moreover, this pattern repeated itself consistently across trading styles, asset classes, instrument classes, and market conditions. This is an important concept that has far-reaching implications for portfolio management, many of which I will attempt to address here.

“To begin with, if we accept the notion that the entire profitability of your account will be captured in, say, the top 10% of your trades, then it follows by definition that the other 90% are a break-even proposition. Think about this for a moment: Literally 9 out of every 10 of your trades are likely to aggregate to produce profits of exactly zero. It almost makes you want to pack up your charts and go home, doesn’t it? Indeed, the main danger in being aware of this concept is the tendency to misinterpret its implications. For this reason, we want to be very careful about how we use the information in driving the portfolio management process and all of its components.

“Most people’s first reaction when they see their “90/10″ score is to assume that it is a problem that wants correcting. This is simply not so; and if they respond by trading less, concentrating their portfolio exclusively on what they feel to be their best ideas, they are likely to be disappointed by the results. The 90/10 rule is hard to overcome, and so I think the better way of looking at it is that you need the 90 to get the 10.

“To best understand this, let’s use a baseball analogy (why not, everyone else does). Think of the situation faced by a .300 hitter in baseball, who, even though he knows he’s going to be unsuccessful 70% of the time cannot simply decline to step up to the plate on the 7 out of 10 occasions where (statistically speaking) he isn’t likely to get a hit.

“Truth is, the 7 outs he makes in 10 at-bats are a necessary condition of his .300 batting average, and he can no more expect to be more successful by limiting his at-bats than you can expect to be successful in your trading by reducing your number of transactions. True, just as the batter may know that he does better against certain teams and pitchers and in certain parks than others, so will you as a portfolio manager have some insights into the conditions that are most conducive to maximum profitability – across individual names, market cycles, and other factors. However, in both cases, the individual in question cannot expect to gain any benefit through a lack of participation.

“Therefore, the principal lesson you should derive from 90/10 may well be that the lower 90% of your transactions, which are likely to sum up to zero P/L, are a critical component of your success. If properly analyzed, these trades can provide insights into the controllable elements of your portfolio management activities that can be enormously valuable to your bottom line. However, if you fight against this tide, you are likely to fall into a large group of market participants who have very useful skill sets but who inevitably become their own worst enemies.” (chart via Longboard Funds)

The Macro Ops Portfolio’s return distribution follows this 90/10 rule, as well — and this is very much by design.

The majority of our annual profits come from just a handful of trades throughout the year. Conversely, most of our trades/investments we enter (on average 75% of them) will effectively cancel one another out. We will have a lot of small losers and some small winners… and then we’ll have 3-5 massive winners that generally makeup over 90% of our bottom line.

This is a fundamental fact of successful trading and investing. Buffett, Soros, Druckenmiller, and Dalio all live by this same law of distribution. If you study their returns, the 90/10 rule is prevalent amongst all of the greats. One of the reasons why they’re “great” is because they have learned to actively embrace this truth and build their strategies in a way that exploits this power law to its full effect.

The fight against the natural distribution of returns is one of the most common failure points among traders and investors… it’s why 90% of traders fail to beat the market and only 10% succeed (ironic, right?). Over-optimization, trying to improve one’s win rate is a common trap and a loser’s game. Like Grant said, “you need the 90 to get the 10.”

90/10 distribution is also a product of creating asymmetry in one’s trades. Asymmetry is the result of finding opportunities and structuring trades in a way where the potential profit far exceeds the maximum loss. This is partially created by taking quick and small losses while giving winners much more room to run. It’s the timeless axiom “cut your losses short and let your winners run”.

Here’s Bruce Kovner on the reality of return distributions:

Michael Marcus taught me one other thing that is absolutely critical: You have to be willing to make mistakes regularly; there is nothing wrong with it. He taught me about making your best judgment, being wrong, making your next best judgment, being wrong, making your third best judgment, and then doubling your money.

Embracing these truths is one of the most difficult hurdles for traders and investors. Humans just aren’t wired for losing and a key to being a good trader is to be an excellent “loser”. And this is because a master trader will enter far more losing trades than winning ones. Mark Spitznagel recounts in his book The Dao of Capital how he was taught this lesson early on by his mentor Everett Klipp who told him “to be successful you have to love to lose.”

Amateurs want high win rates and think every next trade is going to be 5-bagger. The Master trader is infinitely patient and has enough faith in his method — gained through experience — that he remains cold and calculating and lets Pareto’s law work its magic.