One of the most valuable mental models we use in our global macro research process is Merill Lynch’s Investment Clock.

It’s a simple yet useful framework for understanding the various stages of a business cycle and which asset classes perform best in each stage. A similar framework is used at Bridgewater Associates, one of the most successful hedge funds of all time.

We’ll break down the Investment Clock and apply it to the current market to see which assets are likely to perform best going forward.

The Investment Clock Phases Explained

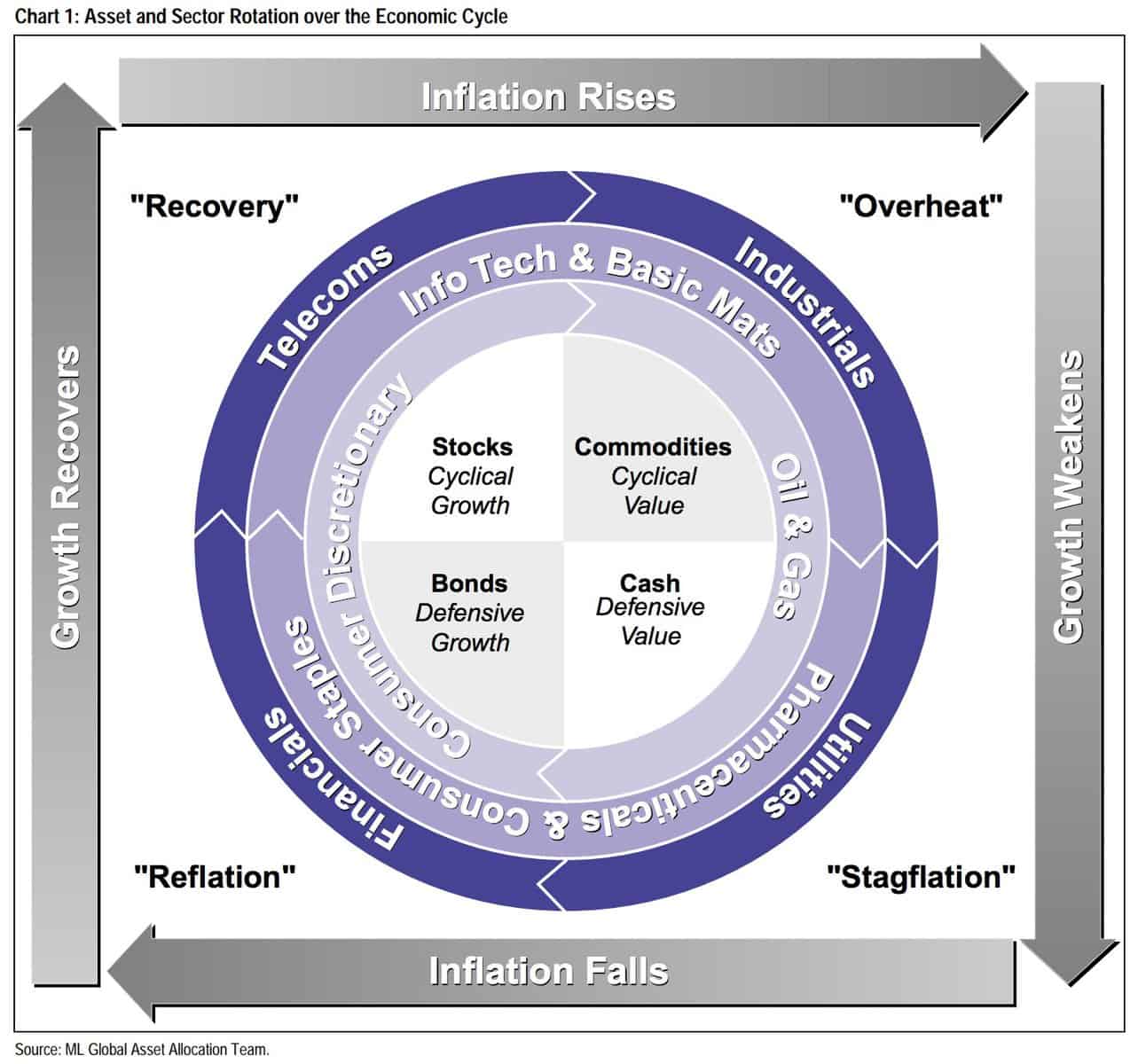

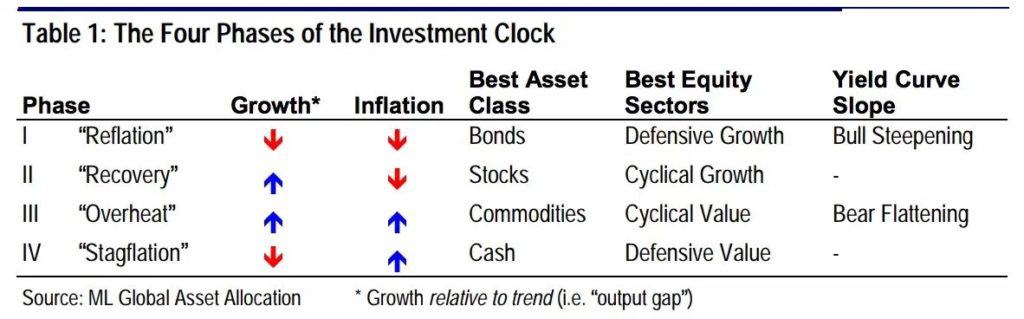

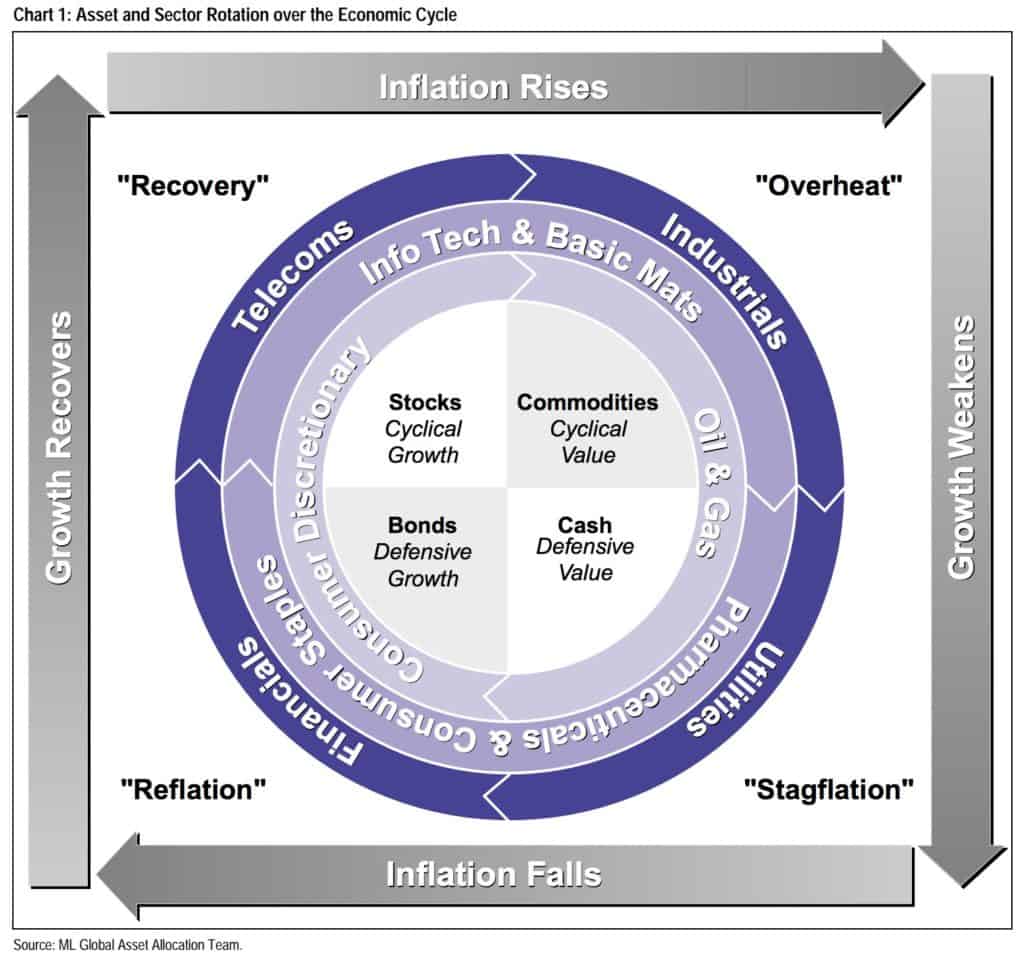

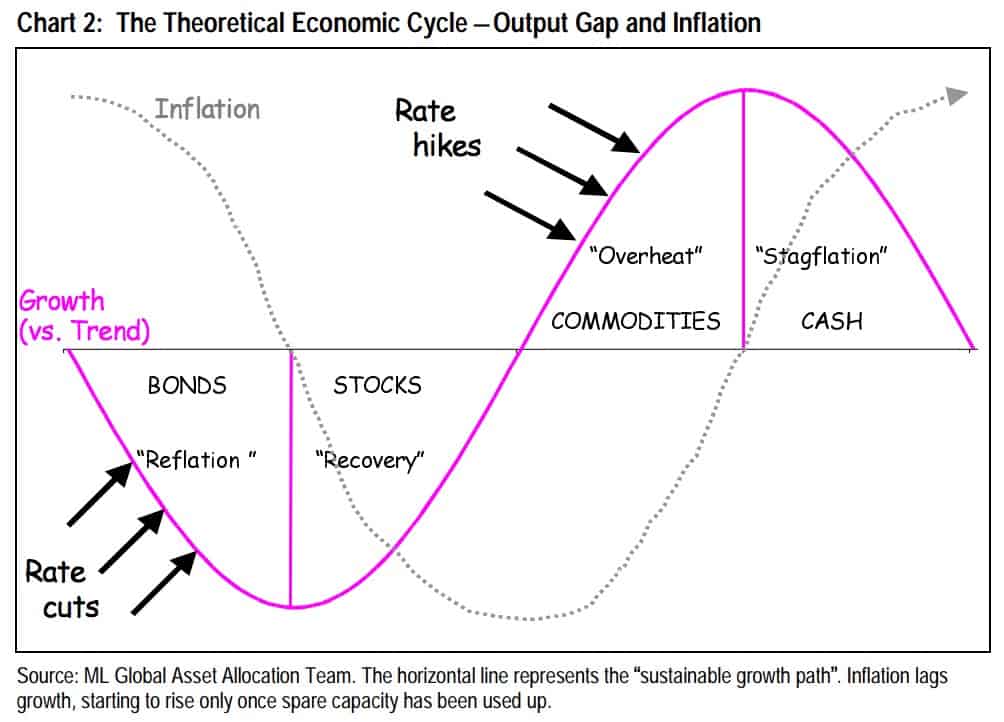

The Investment Clock splits the business cycle into four phases. Each phase is comprised of the direction of growth and inflation relative to their trends. You can see these four phases in the chart below via Merrill Lynch.

Here’s a breakdown of the four phases:

1) The Reflation Phase

Growth is sluggish and inflation is low. This phase occurs during the heart of a bear market. The economy is plagued by excess capacity and falling demand. This keeps commodity prices low and pulls down inflation. The yield curve steepens as the central bank lowers short-term rates in an attempt to stimulate growth and inflation. Bonds are the best asset class in this phase.

2) The Recovery Phase

The central bank’s easing takes effect and begins driving growth to above the trend rate. Though growth picks up, inflation remains low because there’s still excess capacity. Rising growth and low inflation is the goldilocks phase of every cycle. Stocks are the best asset class in this phase.

3) The Overheat Phase

Productivity growth slows and the GDP gap closes causing the economy to bump up against supply constraints. This causes inflation to rise. Rising inflation spurs the central bank to hikes rates. As a result, the yield curve begins flattening. With high growth and high inflation stocks still perform but not as well as in phase 2. Volatility returns as bond yields rise and stocks compete with higher yields for capital flows. In this phase, commodities are the best asset class.

4) The Stagflation Phase

GDP growth slows but inflation remains high (sidenote: most bear markets are preceded by a 100%+ increase in the price of oil which drives inflation up and causes central banks to tighten). Productivity dives and a wage-price spiral develops as companies raise prices to protect compressing margins. This goes on until there’s a sharp rise in unemployment which breaks the cycle. Central banks keep rates high until they reign in inflation. This causes the yield curve to invert. During this phase, cash is the best asset.

Reading The Investment Clock

Below is a chart that illustrates the four phases of the Investment Clock together:

Here’s the following from Merrill Lynch on which asset classes outperform during each Investment Clock phase:

- Cyclicality: When growth is accelerating (North), Stocks and Commodities do well. Cyclical sectors like Tech or Steel out-perform. When growth is slowing (South), Bonds, Cash and defensives outperform.

- Duration: When inflation is falling (West), discount rates drop and financial assets do well. Investors pay up for long duration Growth stocks. When inflation is rising (East), real assets like Commodities and Cash do best. Pricing power is plentiful and short-duration Value stocks outperform.

- Interest Rate-Sensitives: Banks and Consumer Discretionary stocks are interest-rate sensitive “early cycle” performers, doing best in Reflation and Recovery when central banks are easing and growth is starting to recover.

- Asset Plays: Some sectors are linked to the performance of an underlying asset. Insurance stocks and Investment Banks are often bond or equity price sensitive, doing well in the Reflation or Recovery phases. Mining stocks are metal price-sensitive, doing well during an Overheat.

Pretty simple, right?

Now let’s apply this framework to where we are today.

Analyzing The GDP Gap

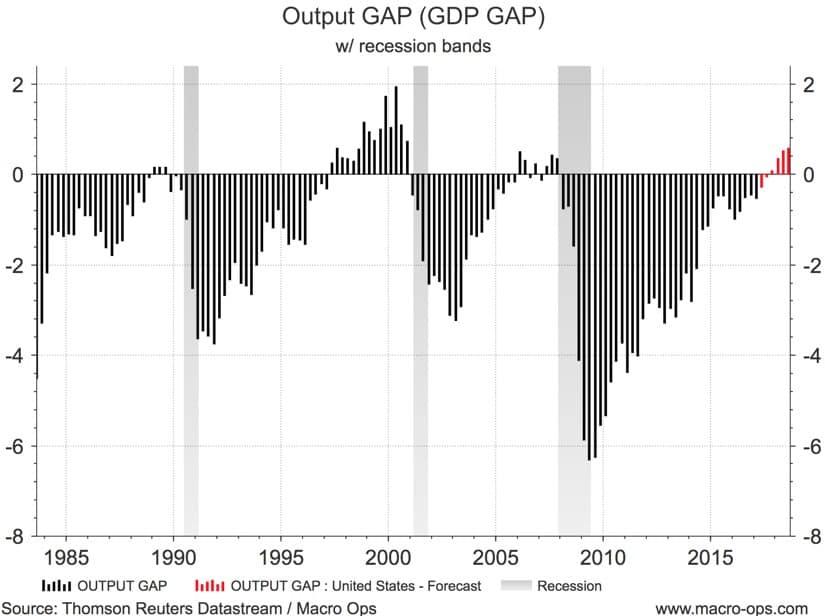

A good place to start is by looking at the GDP gap. GDP or “output gap”, measures the difference between the economy’s actual GDP and its potential, when producing at full capacity.

The zero line represents full economic capacity, or a closed GDP gap. When the reading is positive (above the zero line), it means the economy is producing at above trend capacity. This causes inflation to rise and drives the central bank to hike rates. This is why a recession (marked by the vertical grey bands) follows after each subsequent period of above capacity production.

Some guesswork goes into figuring out what the economy’s potential gdp is — and actual gdp, for that matter — but we don’t need exactness. We’re just concerned with the bigger picture. And looking at the chart, it’s reasonable to say that the economy is operating near full capacity, but not yet above it.

This means we’re in the later phases of the cycle but not at the end.

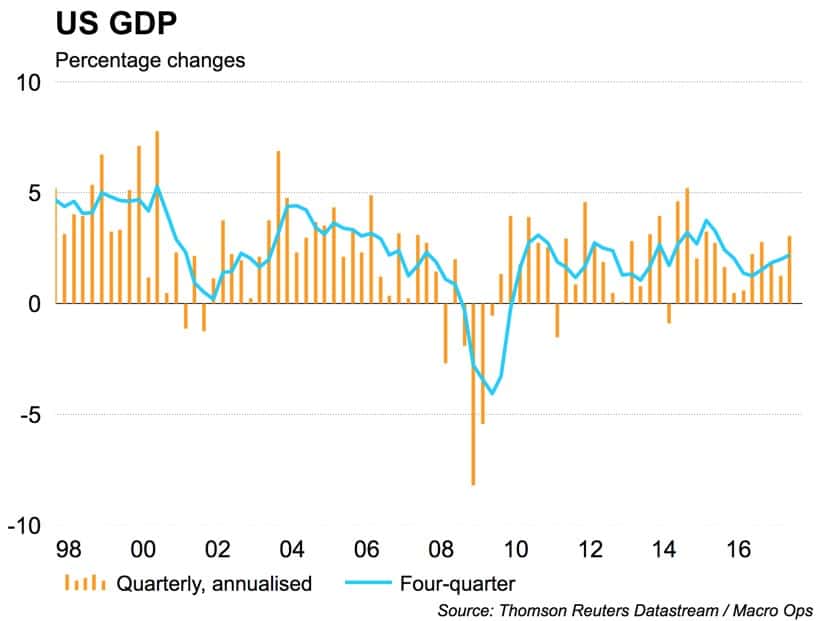

A look at GDP shows that growth remains firm and is trending up.

So we have one part of our equation. We know that growth is trending up and GDP gap is tight but not yet above capacity.

Analyzing US Inflation

Now we have to figure out the other variable; inflation.

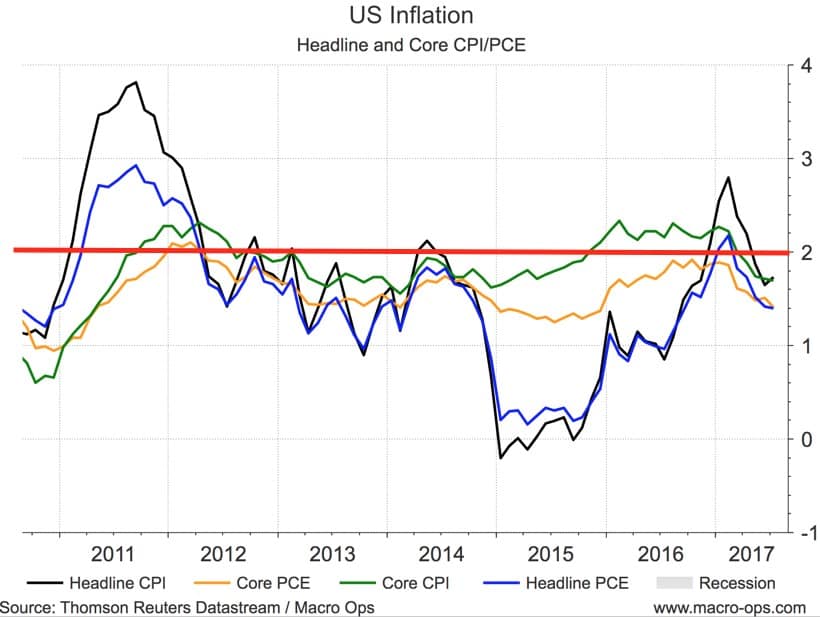

Inflation peaked earlier in the year and has since turned down below the Fed’s 2% target. Depending on the measure, inflation is currently between 1.4 and 1.7%.

We’re less concerned with the absolute value as we are with the trend and where it’s headed.

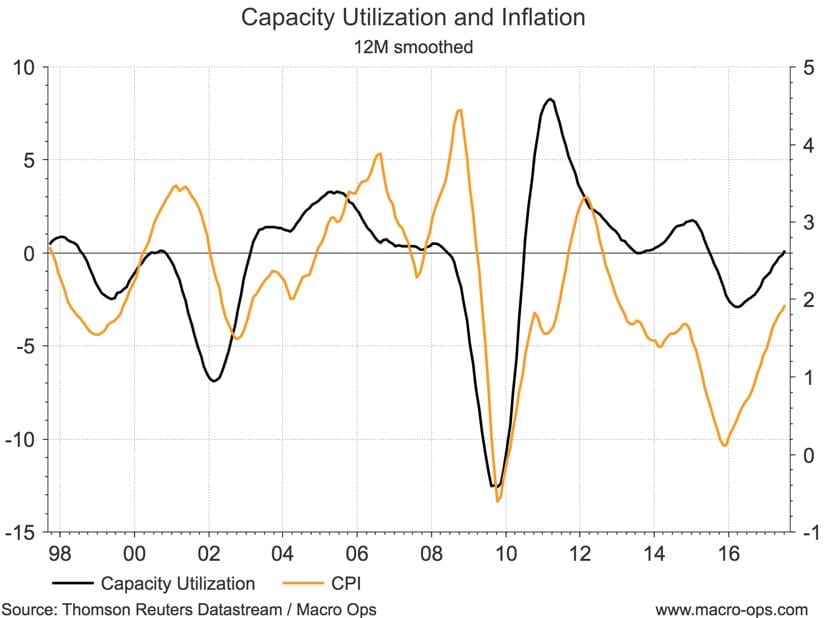

One tool we can use for that is capacity utilization.

Capacity utilization is another way to measure GDP gap. It’s useful because when the economy is firing on all cylinders it causes what’s called “demand-pull” inflation where demand exceeds supply which causes prices to rise.

The chart below shows the relationship. Both capacity utilization and CPI are smoothed over 12 months to shake out the noise. Capacity utilization leads inflation by 6-12 months.

As the business cycle advances, capacity utilization will continue to rise, pulling inflation up with it.

But inflation is a tricky ephemeral thing so it pays to look at a number of indicators to get a better idea of what’s going on.

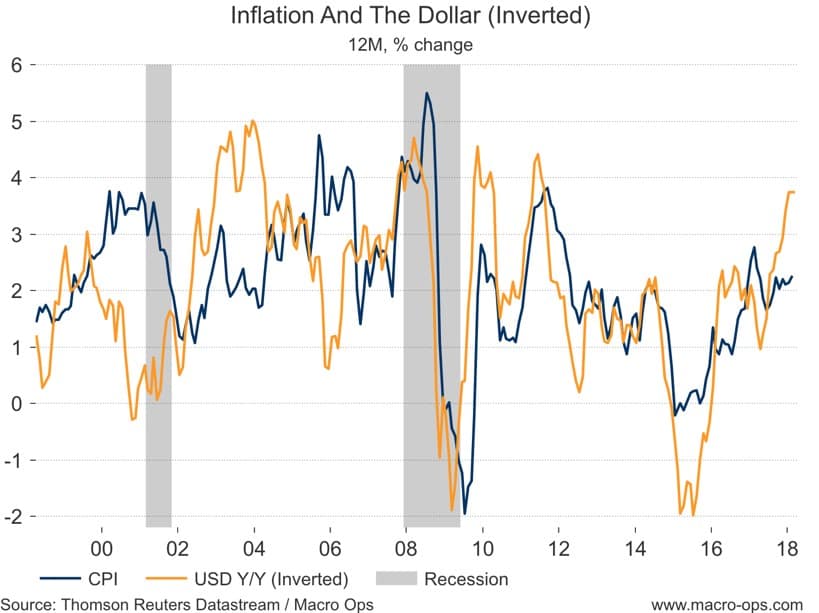

One of the best leading indicators of inflation is the relative change in the dollar. This is because the dollar is the world’s reserve currency. Most international trade is done in dollars. And commodities are priced in dollars.

When the US dollar falls it pushes commodities up. It also makes imports more expensive. Both of which drive inflation.

A great way to figure out where inflation is headed is by paying attention to where the dollar has been.

When you run a regression analysis, you’ll find that inflation and the dollar have a correlated relationship. Movements in inflation lag the greenback by two months on average.

You can see on the chart below we are due for a pop in inflation on the back of recent dollar weakness.

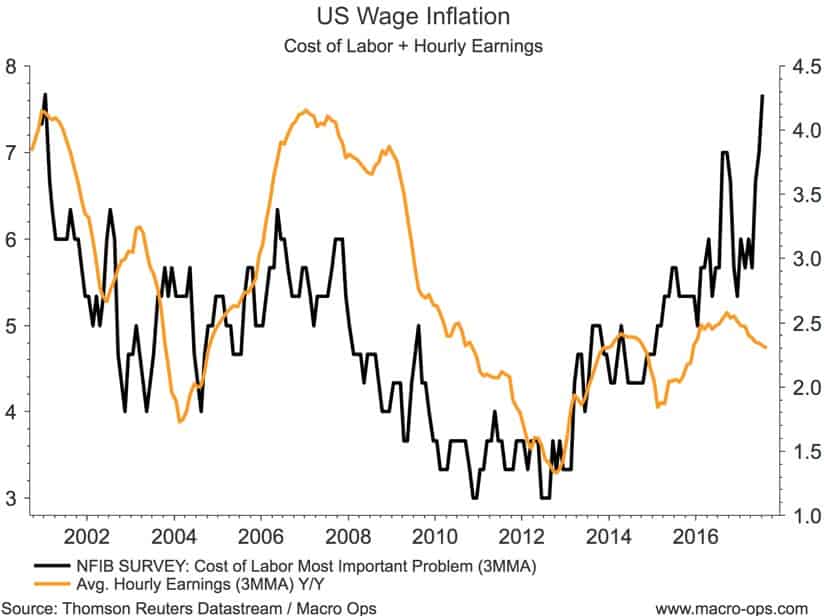

Capacity and the dollar are the largest drivers of inflation outside of extreme supply shocks such as the 73’ oil embargo. But we can always look at the wage data which is a lesser, though still important, data set for gaming inflation.

Labor is the largest input into production. Wages tend to be sticky but in the later stages of the cycle, the labor market tightens which drives up labor costs, as employers compete for scarce workers.

Recent wage growth has been disappointing but the data suggests that pressures are building under the surface which should lead to a pickup in wage growth very soon.

THe NFIB survey (NFIB is America’s largest small business association) indicates that the rising cost of labor is now, by far, the number one concern of owner/operators.

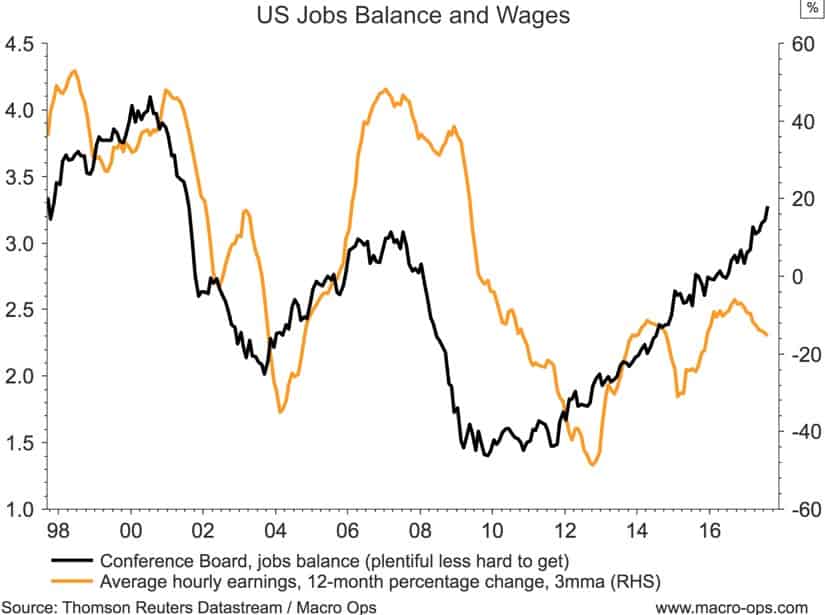

And the Conference Board’s jobs balance indicator has been trending higher too telling us jobs are becoming increasingly easier to get.

So now we have our second input in the Investment Clock. The economy is nearing full capacity and growth is trending up. Inflationary pressures are building which will pull inflation higher in the months ahead.

So Where Are We On The Investment Clock?

Positive Growth And Positive Inflation Put Us In Phase 3 Of The Cycle: “The Overheat phase”

To repeat, the overheat phase is where the GDP gap closes (which is happening) and the economy bumps up against capacity, causing inflation to rise.

The central bank hikes interest rates and bonds selloff causing the yield curve to flatten (also happening). With high growth and high inflation, stocks still perform but not as well as in phase 2. Volatility increases as higher yielding bonds compete with stocks for capital flows.

Commodities Perform The Best In This Phase Of The Investment Clock

Things like basic materials and industrial tend to also do well.

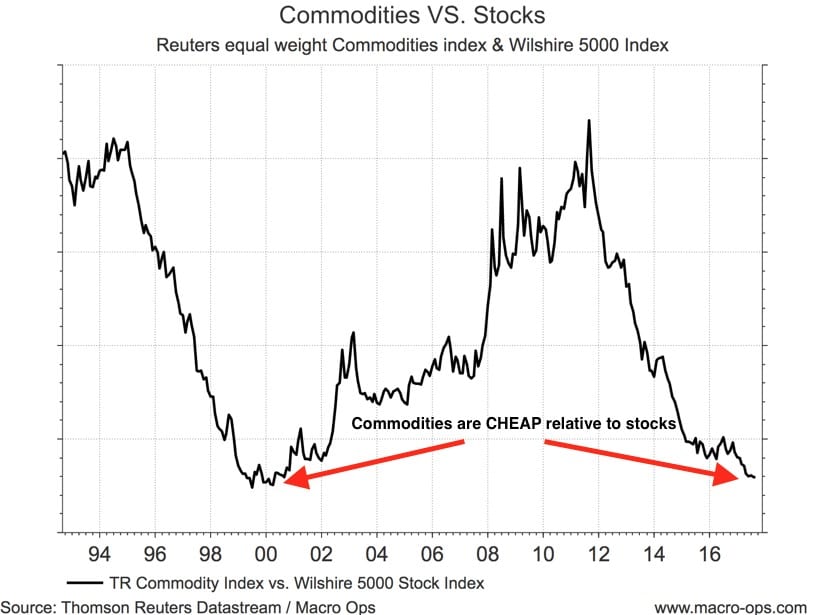

Take a look at the following chart showing commodities relative to stocks.

Commodities Relative To Stocks Are At Their Lowest Levels Last Seen In 2000. Which Also Happened To Be Right Before The Start Of A Major Bull Market In Commodities.

As we progress towards phase 4, inflation will continue to pick up and commodities and commodity related stocks, should begin outperforming the broader stock market.

This is what we’ll be focusing on in research pieces we’ll put out in the weeks ahead. We’ll be exploring commodity related plays that will benefit in a high growth, high inflation market — think miners, select emerging markets, agriculture and so on.

Conversely, the bond market will hit a rough patch as rates adjust up to the new inflationary environment.

And as this article goes to press, there’s been a number of developments that could have far reaching impacts on the market.

Stanley Fischer, the Fed’s Vice Chair, abruptly announced that he’ll be stepping down immediately. He’s one of Yellen’s closest associates and has helped balance out the more dovish voices in the FOMC.

President Trump now has three empty Fed chairs to fill. And he’s made his desire for a lower US dollar very clear through multiple twitter declarations. So it’s unlikely he’s going to install a hard money conservative into any of these slots.

Dovish dissent has been growing in recent months among FOMC members, from vocal members such as Kashkari and Brainard.

There’s the increasing possibility that the Fed board becomes overweight with policy doves. If so, this will have enormous policy implications for the market and especially the dollar.

It’d also make the bullish case for commodities that more convincing.

To learn more about how investment strategy at Macro Ops, check our our Trading Handbook here.

Summary:

- The Investment Clock consist of four phases (Reflation, Recover, Overheat, Stagflation)

- These phases are comprised of the trend rate direction in GDP and inflation

- The data currently points to an economy operating near full capacity with higher growth on the horizon

- It also suggests inflation will soon pick up due to capacity constraints, a weak dollar, and signs of coming wage inflation

- This puts us in stage 3 of the Investment Clock, the “Overheat” phase

- Commodities are the best asset class in this phase

- Commodities are historically very cheap relative to stocks