*** The following is an excerpt from a recent Market Note sent out to members of our Collective. To find out more about the Collective, click here***

I was chatting with a good friend and mentor the other day. We were catching up as we hadn’t spoken in a few weeks. He’s worked with a number of the greats and is now semi-retired and runs his family office. He’s one of the best traders I know. So, as usual, I was curious to hear his thoughts on markets.

I’m paraphrasing some parts but here’s what he said.

Alex… You know what I think? I think it’s really sunny here in Sveti Stefan. I think the cold beer I’m sipping while looking out over the Adriatic is absolutely delicious… The big question I’m wrestling with at the moment is whether I should eat steak or lobster for dinner, but to be honest, I’m probably just going to do both…

…In all seriousness, here’s my thoughts… I think, like we discussed the other month, that markets are toast, probably for the rest of the year. At least through summer into Fall… Look, inflation is a political problem. And it’s a big one with midterms coming up. That’s why Powell was called to the White House with hat in hand back in May. Inflation is too damn high and the buck has been passed to the Fed to fix it. And they only have blunt tools to do the job, all of which are basically hammer demand until something breaks…

And this is what they told us at the last meeting, right? That sealed the deal for me. They basically said that they intend to push us into recession in order to try and bring inflation down.

And, so, here we are… the delta on inflation has likely peaked. Supply pressures are easing and demand will continue to soften dramatically. But… the Fed is going to need consecutive months of lower inflation before they can even begin to signal a slower pace of tightening, let alone an end. Think about that for a second. Why would anyone in their right mind be buying aggressively here?

I don’t even necessarily agree with all the recession calls for this year. At least not in the US. Europe, yes, definitely, they’re toast. And are probably already in one. But while the US may not enter a technical recession soon, it’s sure going to feel like one.

And if we do enter one, it’ll probably be short-lived and fairly benign. The fiscal imbalances just aren’t there and quite a bit of air has already been taken out of this market. It’s hard to break your legs when you’re jumping from just the second story…

Profit margins are unsustainably high and are about to get squeezed. Earnings are coming down while estimates are ridiculously elevated, as you pointed out the other day.

And so, I don’t know. It’s a messy and noisy environment. Not a great risk/reward. I’m not sure I buy into the new secular inflationary regime. This isn’t the 70s. Demographics and debt couldn’t be more different. But this isn’t the last 30 years either.

The politics have changed dramatically. Politicians have discovered fiscal, so that’s a kind of a pandora’s box that has been opened and won’t be closed anytime soon — what’s happening in California right now is a case in point… So who the hell knows. The cone of probabilities has been blown out wide as you say.

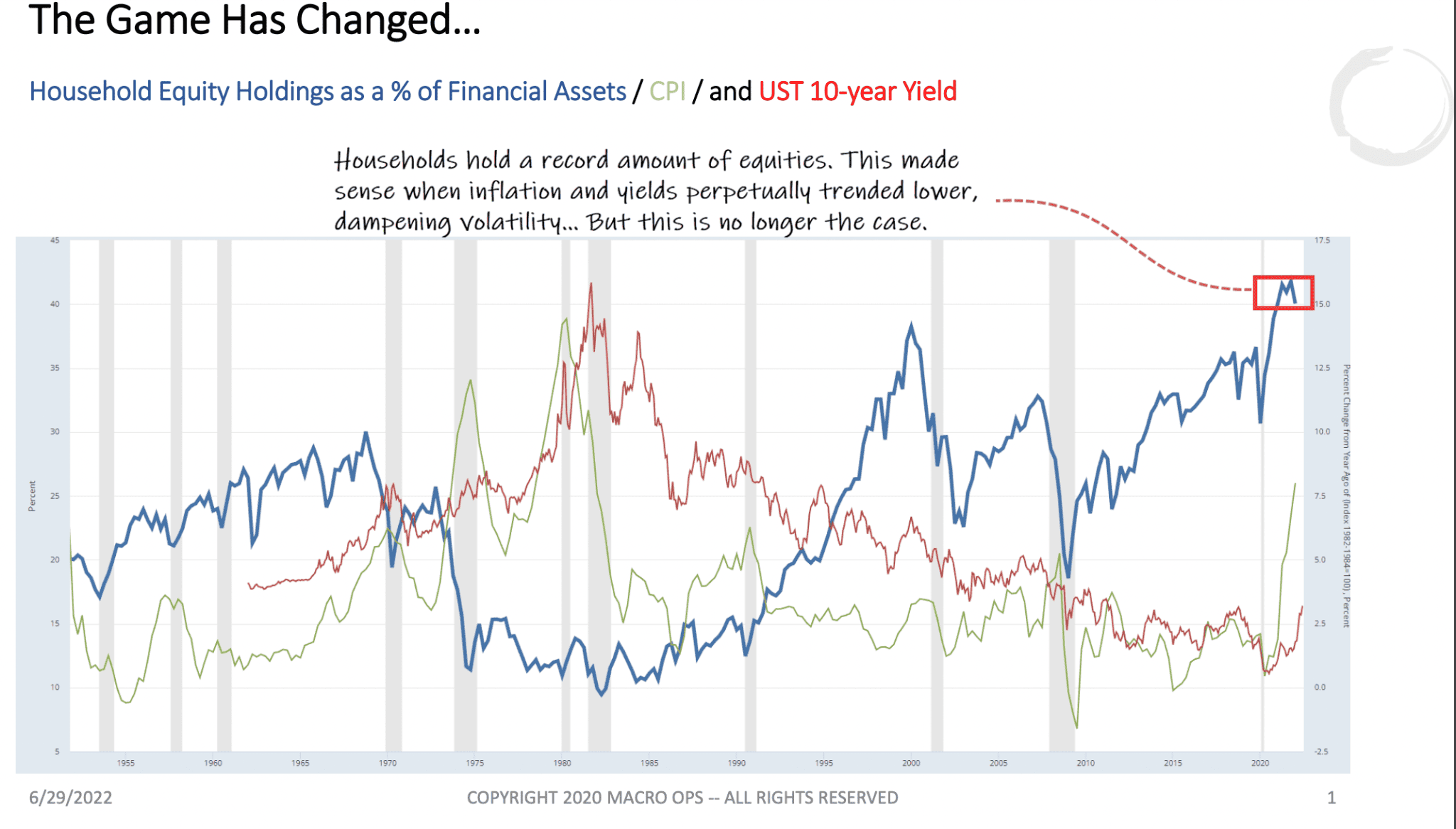

30yr Mortgage rates are over six and quarter! That’s going to freeze the housing market, which we’re already seeing signs of. US equity allocations are just coming off their all-time highs. If we are in a long inflationary regime, well that’s going to come down. Probably by a lot.

So that’s where I think we are. Could I be wrong and we hit a cyclical bottom next week? Absolutely… I’m wrong all the time. And this is one of the more exceptional macro environments I’ve ever experienced in my 30+ years in markets. So, you know, we gotta be flexible, of course.

But to me, the rest of summer at the very least will be messy. I just don’t see the light at the end of the tunnel, yet. Sure, markets are deeply oversold and multiples are a LOT more reasonable in aggregate. So we’ll probably get some large rallies here and there. But I don’t think the bottom is in. Far from it. I think we probably have another year of a slow grinding bear. More like the 2000s than 08’-09’ as I don’t see any systemic liquidity risks this time around.

So in my mind, this is a good time to get out and enjoy life, which is too short. Net out your book. Put stink bids in for your favorite names and go work on a tan and read some good books. It’s not often that markets give us a chance to take an extended vacation. So take some advice from someone who’s spent a lot of time chained to his desk and go live.

Success in this game is about long-term compounding. There’s layers to this truth. Giving yourself a break and stepping away from the screens, is one of them. It helps to keep the spirit young, the mind sharp, and the body fresh… My learning to be okay with taking a break. Being able to step away from the game from time to time. Is one of the reasons why I’m still around and playing it decently, after all these years… There’ll be a better market to come back to in the Fall, maybe not. We’ll see…

This is a good base case and in line with where I sit, though I’m not over-anchoring to anything. The signaling from the Fed over the last few weeks shifted the distribution of probable outcomes fairly significantly. They essentially told us they’re willing to engineer a recession in order to throttle demand and bring inflation to heel.

I don’t know, I still find myself a bit more hopeful than most. I’m uncomfortable being in the recession camp since it feels like it’s a pretty crowded narrative.

Also, we’re starting to see improvements. 5y,5y forward breakevens are already back below 18’ levels. Freight costs are plummeting, shipping/delivery times are coming down, commodity prices are falling, and every retailer over-ordered which means price cuts are coming, etc…

At the same time, just pulling back a bit and looking at this equity holdings chart and the turn in secular forces we’ve seen over the last few years (debt cycle/MP3, demographics are no longer deflationary, populist politics, deglobalization, etc…). And we have to at least be open to the idea that we’re in vastly new terrain going forward. I’ll write more on this soon in a separate note.

Since sailing around the Mediterranean for the summer is out of the question for most of us (at least for now!). We can keep our net exposure low and wait for decent pitches to come down the plate. This is a lot of batting for singles and the occasional double. Being disciplined and ruthlessly managing our downside. Not exactly exciting trading but it is what it is…

The diminishing returns on information…

The VC firm Lux Capital puts out a pretty good free weekly, which you can check out here. One of their recent posts was on a favorite topic of mine. The diminishing — and sometimes negative — returns of accumulating more information in decision making. The post starts with (emphasis by me):

One of the most important cognitive tradeoffs we make is how to process information, and perhaps more specifically, the deluge of information that bombards us every day. A study out of UCSD in 2009 estimated that Americans read or hear more than 100,000 words a day — an increase of nearly 350% over the prior three decades (and that was before Slack and Substack!) It would seem logical that more information is always better for decision-making, both for individuals and for societies. Yet, that’s precisely the tradeoff: humans and civilizations must balance greater and better information with the limits of their rationalities.

The post gives an overview of Phillip Tetlock’s older book Expert Political Judgement. They discuss his ideas around Foxes (those who know many small ideas) and Hedgehogs (those who know one big idea really well) and how the former generally make for better forecasters.

You can read up more on the idea in this older but still very good explainer from Michael Mauboussin (link here). Also, here’s a summary of Tetlock’s Ten Commandments of Forecasting (access for Collective members only).

They couple Tetlock’s work with another book titled The Collapse of Complex Societies by Joseph A. Tainter. Different books, divergent fields, but both “converge around a central thesis: there is a marginal return to information, and it often reaches zero — or even negative — far earlier than we might expect.” You can read the piece here. It’s short. And worth reading in full.

This is a topic I’ve been thinking about. I’ve written about it in the past; The Perils of Too Much Information, Ditch The Predictions and Play The Odds, The Fallacy of Market Prediction, etc…

There’s the Paul Slavic research into the professional horse bettors. Where Slavic found that beyond a certain minimum amount (in this case 5 pieces of information about either the horses, jockeys, and/or track), additional information stopped adding to the bettor’s accuracy.

But, it did add to their confidence in their accuracy. So more information beyond a certain threshold drove confirmation bias but did not improve predictive accuracy at all. This led to overconfidence. These findings have been confirmed numerous times in follow-up studies.

Now, I imagine there are few fields where this idea is more pertinent than in trading and investing. Part of our job is to literally synthesize loads of information in the hopes of creating an information and/or analytical advantage.

We drink from a firehose of confirming and disconfirming facts and figures. Data points about where the economy is headed, what the Fed is doing, how the war in Ukraine is impacting Ag prices in South America, why again is cotton trading like an ARKK holding? What matters to me? What doesn’t? What’s true? What isn’t? And on and on…

At what point does more information become too much? And what types of information should we focus on and what types should we not?

I think about all the smart fund managers who made a name for themselves over this past cycle by leveraging into growth names. Many of them have gone, or are very nearly about to go, belly-up. They’ve given back all of their excess returns over the last 5-7 years in the span of just 12 months.

And I’m not saying “smart” sarcastically either. Many of these guys are genius-level bright. They knew their companies inside and out. They modeled the shit out of everything and had researched their theses to the bone. You talk to any of them on the phone for long enough and listen to them pontificate about the risk/reward of their favorite holdings and it was nearly impossible to come away and not want to load the boat with the shares yourself.

These names are now down -70%+.

But hey, maybe a few of these get back to all-time highs in a few years. Most will go nowhere for 5+ years due to Bubble Rotation dynamics. A few will go to zero.

So I can’t help but think that though they had a LOT of information. Quite literally encyclopedic level deep dives into their positions. They obviously didn’t have all of the important info. And the excess of non-essential “evidence” maybe gave them overconfidence. It maybe blinded them to incoming disconfirming evidence. All of which is a deadly mix in this game of markets.

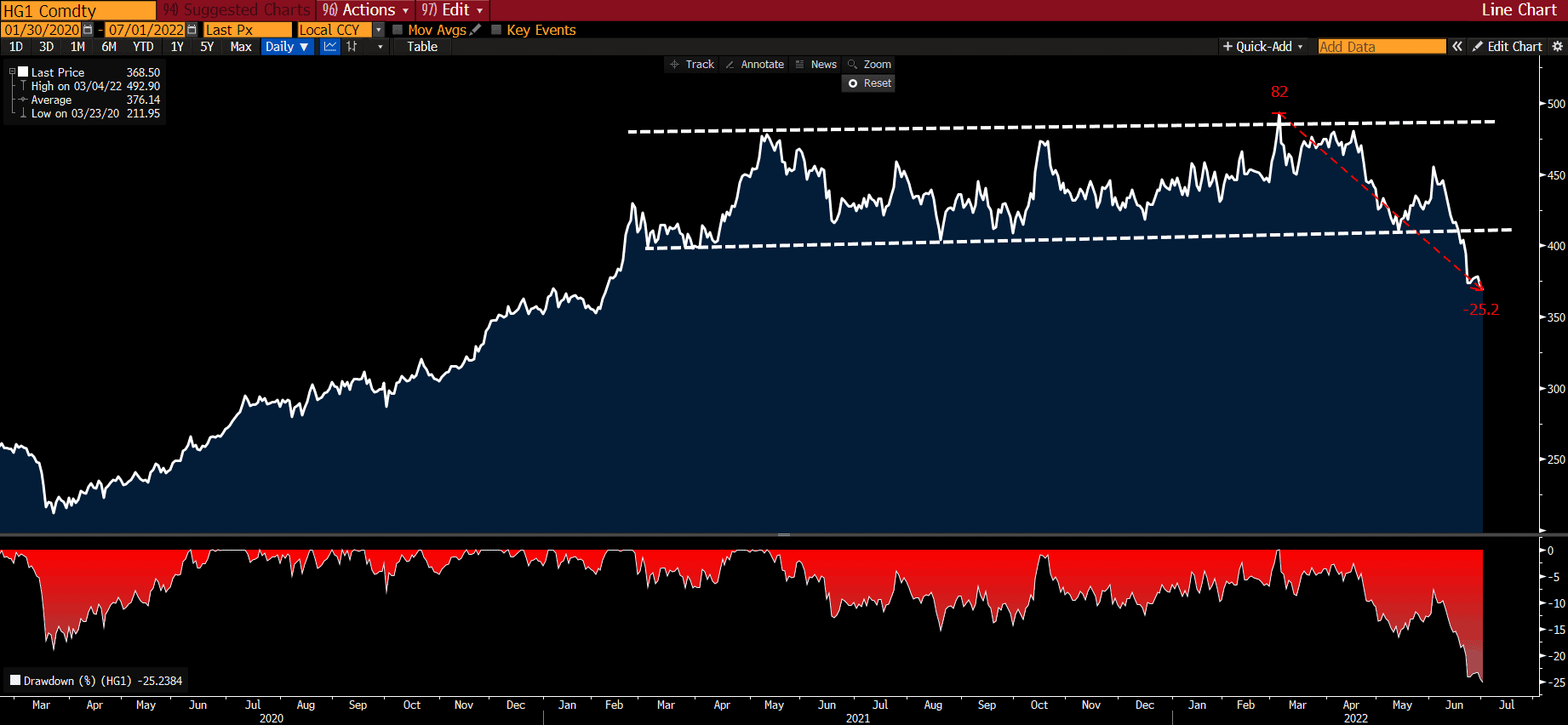

Another recent example is this Oddlots podcast from back in May. The episode is titled Why Copper May Be One of the Tightest Markets The World Has Ever Seen. The interview was with Goldman Sachs metals strategist Nick Snowdon.

Nick is a wicked smart guy. He knows the metals market better than you and I ever will. The interview is excellent. His argument is persuasive. Give it a listen. You’ll want to buy lots of copper afterward.

Since that episode was released, copper has fallen another 12%, kicking off a new bear trend. It’s probably going to trade much lower. This game is hard…

And this is a bit of a ramble. I’m just typing aloud here. But I think a pretty good rule of thumb is that once an investment thesis can be convincingly articulated, it’s too late. It’s in the price.

Once you see the talking heads persuasively opine on why such and such supply is tight and therefore XYZ asset has one way to go. It’s time to sell.

And, okay, maybe that’s only partly true. You at least want to weigh it against price. But the ultimate death knell for any asset is when there are very convincing popular arguments circling and yet the asset is trading like a two-legged dog.

The converse of this is the “No Sense Algorithm” that Adam Robinson talks about. I’ll share an excerpt here because it’s just so good (again, emphasis by me).

So, to return to investing, the second problem with trying to understand the world is that it is simply far too complex to grasp, and the more dogged our attempts to understand the world, the more we earnestly want to “explain” events and trends in it, the more we become attached to our resulting beliefs—which are always more or less mistaken—blinding us to the financial trends that are actually unfolding.

Worse, we think we understand the world, giving investors a false sense of confidence, when in fact we always more or less misunderstand it. You hear it all the time from even the most seasoned investors and financial “experts” that this trend or that “doesn’t make sense.” “It doesn’t make sense that the dollar keeps going lower” or “it makes no sense that stocks keep going higher.”

But what’s really going on when investors say that something makes no sense is that they have a dozen or whatever reasons why the trend should be moving in the opposite direction . . . yet it keeps moving in the current direction. So they believe the trend makes no sense. But what makes no sense is their model of the world. That’s what doesn’t make sense. The world always makes sense.

In fact, because financial trends involve human behavior and human beliefs on a global scale, the most powerful trends won’t make sense until it becomes too late to profit from them. By the time investors formulate an understanding that gives them the confidence to invest, the investment opportunity has already passed.

And, sure. There’s also a timing component to all this.

I actually think Nick from Goldman is right. The copper supply issues are real. CAPEX has been entirely too low for the last decade. Especially if you think we’re going to get anywhere close to hitting these “green” energy targets. Lots of copper is needed to electrify everything. And copper mines take years to come online from their project start.

But that’s a looong lead time kinda thing. It’s Chinese housing, Fed tightening, and increasing recession risk — and a host of other variables we’re unaware of — driving demand in the interim. The oil market was supposed to be tight since 17’. It took nearly 5-years and negative prices to get us there. So, yeah. Some food for thought.

The time to buy copper will be when no one wants to. When there’s some really persuasive narratives about why copper is stuck in a glut and ain’t going nowhere.

This is where I think a lot of players get lost. They just can’t seem to quite grok the metagame. The fact that there often is no truth, truth. Or at least not on the timeframe most are operating on. You know, Graham’s voting versus weighing machines and all that jazz.So, yeah sure that company is dirt cheap. It can become much more so.

What’s your uncle point? What’s your honest-to-God holding period? Can you, or do you, have the stomach to endure the volatility to ride it out to see if you are in fact right?

The answers will be different for most. But it’s an important one for each of us to know.

Anywho, these are just things I’ve been wrestling with.

One of the reasons why is because I can make a convincing argument for being pretty bullish the market over the next 12 months. I can make a convincing argument for the bear side, as well. I can pull up data, leading indicators, expert forecasts on relevant figures, and so forth. All of which support whichever side I feel like arguing.

It’s not always like this. I often develop conviction on where the general trends are headed. That conviction is typically backed by just a few key inputs of information. The problem with these arguments… Is that I have to use a LOT of points to make them compelling. It’s too much. Which is why they’re weak arguments.

This brings us back to our original issue of the diminishing and sometimes negative returns of more information.

Most people unconsciously develop a bias and then consciously look to confirm it. Maybe they hear a persuasive narrative somewhere that gets that ball rolling downhill for them. Or maybe they’re down a lot and could really benefit personally, from a large rally so they can get out of their names at cost… Well, since we live in a world inundated with data and opinions, it’s never been easier to confirm that bias and support that narrative.

This is a central driver behind our Panta Rhei, Extremus idea right?

More information means more competing and compelling narratives, which means more uncertainty and, ultimately, more distrust, which leads to increasing variance within the social order.

I guess there are a few things we can take away from this.

- When noise vs signal is high and the cone of probabilities is wide. We’d do better by limiting our intake of information to what we know is true, to what we know works. For us, these are the few macro variables that are central to our process, technicals, and respecting the tape. Tracking sentiment, positioning, and the development of narratives.

- Embrace our fallibility and understand that overconfidence fosters the type of get-taken-out-of-the-game-for-good risks, that we really want to avoid.

- Follow a tested process, with tested inputs, that inform us when we deserve to have conviction and when we don’t.

I think this line from Bennett Goodspeed sums it all up pretty well. He wrote:

Why do investment professionals get such poor marks? The main reason is that they are victims of their own methodology. By making a science out of an art, they are opting to be precisely wrong rather than generally correct.

There are other lessons here I’m sure… I’m still noodling and plan to write more on the topic. If you have thoughts, disagreements, or additions to anything I said. Shoot them my way.

Now let’s talk about Big Balance Sheet Economics (BBSE), inflation, bonds, and a setup in a dollar pair…

***End of excerpt. Join our Collective to read more…***

Enrollment into our Collective closes Sunday at midnight. We’re offering a discount this go around, with a free month as I (Alex) will be at an ashram meditating for the next 30 days. So if you were thinking about joining up and checking us out, nows not a bad time to do it as you’ll get the first month free. I’ll be back in mid-August ready to get after it. As always, don’t hesitate to shoot me any Qs!***