Today we’ve got a guest post from Srivatsan “Sri” Prakash. Sri is the host of the Market Champions podcast dedicated to interviewing the best and the brightest in finance and economics. His thoughts can be found on Twitter @SrivatsPrakash.

The stories coming out of Sri Lanka and Pakistan are absolutely devastating. Yet, it may provide an idea of what could happen to other emerging market economies. Here is an excellent thread by Atif Mian on what is happening in Pakistan.

Let’s explore this idea further.

Where do we start?

When analyzing emerging markets, it’s best to start in the 1980s. Some of today’s emerging markets crunch smells like the 80s. We then watched as Latin American countries barely survived a major debt crisis.

These countries leveraged their explosive, oil-drive growth to attract billions of dollars from foreign investors in the 60s and 70s. There was similarly a feedback loop in the direction of getting more credit:

Country borrows money => Invests in Infrastructure => Sees higher growth rate => Creditors willing to lend more money => Country borrows more money

Where did it go wrong back then?

Much of the debt was in US Dollars, making it very difficult to service, considering Mexico had borrowed against future oil reserves. They were betting that oil prices would remain high, leading to higher revenues allowing them to pay their creditors back. Easy enough, right?

Until oil prices cratered faster than an Elon Musk monogamy promise. This dynamic is interesting because many emerging markets are typically dependent on commodity exports (as well as imports!).

For example, Brazil is a significant exporter of soft commodities, including coffee and orange juice. Similarly, South Africa is heavily reliant on platinum and other industrial commodities.

On the other hand, places like India and China rely on oil and copper. This becomes a problem when the prices of these commodities begin to rise (if imported) or fall (when exported).

Latin American debt went from about $75B to $315B between 1975 and 1983 (a 4x increase!)

The 1970s saw interest rates rise in many domestic worlds as a countermeasure to fight inflation. Yet, this inadvertently increased interest payments for these countries – for all practical purposes, the Fed sets the interest rate for the entire world, not just the United States.

The broader issue was that lending to Latin America slowed down, leading to a slowdown in the rate of lending – with commercial banks. These loans were typically short-term, and so just as the Latin American economies took a beating, the loans were due- the worst combination of both worlds.

Another problem with emerging markets is the existence of a pegged currency system. You can learn more about this system here.

This was characteristic of the collapses of currencies like the Chilean Peso, pegged to the US dollar back in 1982. The broader issue here was that the peg forces a currency’s value to remain stationary regardless of whether or not it’s overvalued.

And the 1990s…

2000-2006 was a better time for emerging markets broadly, where many governments liberalized trade and capital markets, albeit primarily driven by China and India. Countries did learn the value of stockpiling foreign exchange reserves. This was driven by China’s voracious demand for commodities, leading to higher commodity prices. These prices ended up being reflected in higher revenues for many of these countries (as previously mentioned are commodity reliant).

Remember that the lessons learned from previous emerging markets crises came in handy regarding the slow 2010s, which were weathered broadly through more innovative policy.

It is worth noting that post-2020, very few countries have defaulted, like Lebanon and Argentina. This has led to additional debt binging by emerging market governments.

Interesting, the emerging market bond ETF is at levels below March 2020:

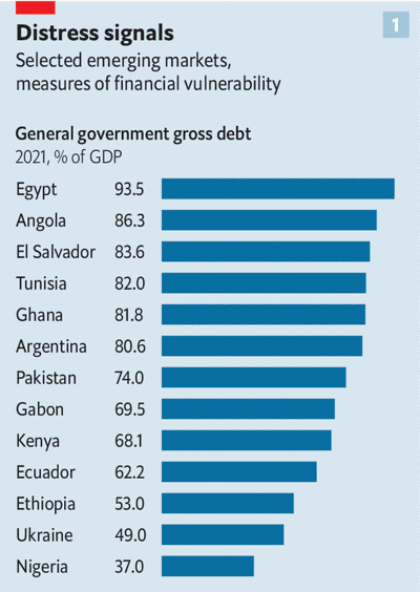

A decent way to measure the indebtedness of countries is to look at the debt/GDP ratios, and here they are for some emerging markets:

What is worth noting about the Sri Lankan and Pakistani episodes is that they are driven not only by debt and commodities but also by political pressure. Politics plays an increasingly large role in deciding the functioning of the economy, which is true, especially in emerging markets.

What could be next for emerging markets?

As previously mentioned, emerging markets are driven mainly by commodity prices, politics, the dollar/interest rates, and debt dynamics.

What we’re observing in places like Sri Lanka is what happens when a catalyst to disaster happens – the motivation here was rising import prices.

What happens when other emerging markets see a similar dynamic hit hard? India has the strengths of having a stable government and relatively stable federal politics. Similarly, China – has the CCP ruling with an iron grip.

The Economist recently published a piece here, and here’s a quote from it:

“The combination of heavy debt burdens, slowing global growth, and tightening financial conditions will be more than some governments can bear. One set of potential victims comprises the poorest economies, which have been less able to borrow in relatively safe ways—in their own currencies, for example—and which, because of the pandemic, were already vulnerable. Among 73 low-income countries eligible for debt relief under a g20 initiative, eight carry public-debt loads, which the imf has deemed to be unsustainable, and another 30 are at high risk of falling into such a situation. Debt problems in these countries pose little threat to the global economy; together, their GDP is roughly equivalent to that of Belgium. Yet they are home to nearly 500m people, whose fates depend on whether their governments can afford to invest in basic infrastructure and public services.”

Then there are the troubled middle-income economies in the mold of Sri Lanka, which are more integrated into the global financial system. Through policy missteps and bad luck, they have been exposed. Overall, 15 countries default or have sovereign bonds trading at distressed levels. They include Egypt, El Salvador, Pakistan, and Tunisia.”

This simply shows that many of the poorer emerging markets will end up having some sort of debt crisis. In contrast, the largest ones – China and India, have massive piles of stockpiles of FX reserves.

I hope this piece helped highlight some of the risks that exist to emerging markets today and what/how they may pose a threat to the global economy!