Webster defines a linchpin as “a person or thing that holds something together: the most important part of a complex situation or system”. In global economics, there’s always a critical factor or “linchpin” on which everything rests.

Right now, that linchpin is the US dollar. Its movements will determine the fate of global markets. The USD trend is the biggest macro trend in the world. It affects everything from equities to commodities and bonds.

Usually these macro trends are tricky. They don’t move straight up or down. They ebb and flow. Retrace and rocket. They’re masters at faking investors out. This USD trend is no different. In hockey terms, you can consider USD the Pavel Datsyuk of trends. And right now, many investors are getting deked out.

Most investors don’t understand the importance of USD strength in driving global asset prices. That’s why they fail to recognize that the recent bullishness in various markets is a direct result of dollar weakness combined with a bear market hope jag rally. US equities have had a nice rebound. Oil has perked up. In general, things look like they’re stabilizing. At least in the eyes of most investors.

But what’s far more dangerous is that the Fed thinks markets look okay too. And the Fed controls interest rates. Seeing “stable” markets gives them the cover they need to raise rates again in the coming months, if not March and then June. This is the opposite of what other central banks around the world are doing. They’re busy trying to figure out new ways to ease.

This monetary divergence between the US and the rest of the world (ROW) will send the dollar rocketing higher. The USD strength will act as a piano drop on the head of markets and most commodities.

Look at the dollar below. You can see it’s been trading within a range for about a year now.

We expect the dollar to retrace another 2-5% to the bottom of, or just below, this range. This is a completely normal retrace within a larger macro trend. And in fact, it’s a healthy short-term reversal. Large trends like these need consolidation points where they can catch a breather. It’s key to shake out the weak hands. Once the selling pressure dissipates, these trends take off like bullets leaving a barrel.

The dollar will likely keep correcting until mid-March. That’s when the Fed, European Central Bank (ECB), and Bank of Japan (BOJ) all meet. The results of these meetings will send the dollar back on its rampage higher.

On the US side, we believe there is a 50/50 chance the Fed will raise rates.

One of the factors the Fed considers when making its decision, whether it admits it or not, is the strength of global markets. And what they’ll likely see in March on the oil side, is a “recovering” market. With oil looking healthier, a hike may seem reasonable.

But what many investors don’t understand, including the Fed, is that dollar strength has a huge effect on commodity prices. Commodities are priced in dollars. So when the dollar strengthens, commodities drop. The opposite also holds true. That means recent dollar weakness has helped oil prices rise.

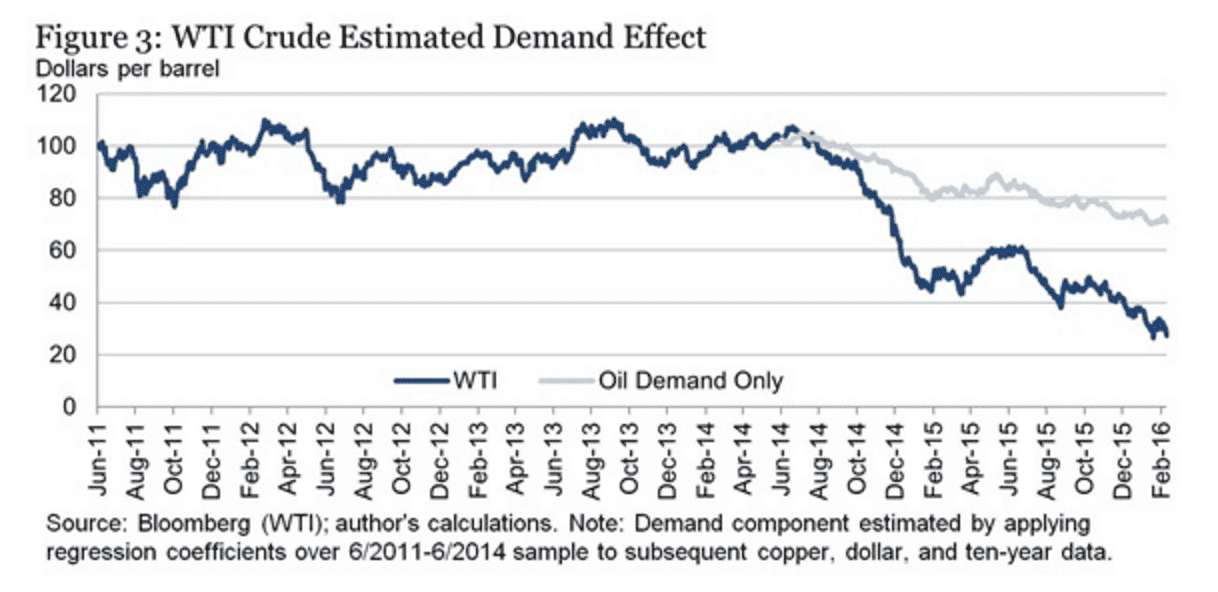

Take a look at the graph below. It isolates an estimate of the price of oil based only on demand. It then compares it to the real price of oil in the market.

You can see a significant difference between the two prices. The actual market price of oil severely undercuts demand estimates. This is because these estimates fail to incorporate the impact of USD strength. Dollar strength historically accounts for 30-50% of price movements in oil. Many investors miss this point.

So if the Fed thinks oil prices are recovering, and decides to hike, guess what happens. The dollar will strengthen and oil will tumble lower once again.

Oil’s rebound has also had the effect of helping equity markets. Less pain in the oil space means stronger oil companies. The resultant recovery in their share prices has helped lift indices.

Temporary dollar weakness also reduces pressure on multinational companies, which has helped boost their shares recently. As the dollar becomes stronger, US products become more expensive. This leads to less overseas demand. Not only that, but the profits companies are able to earn overseas have to be converted back into USD. A strong dollar makes that conversion rate an automatic tax on any profits. These factors have been hurting many companies’ bottom lines. A weaker dollar helps ease investors’ fears regarding this and encourages them to bid up share prices.

It’s also important to remember that we’re in a bear market. In a bear market, retraces occur frequently within the context of a larger downtrend. This is another reason the recovery in both the oil and equity markets is temporary. The trend will eventually resolve itself to the downside.

If the Fed believes the market’s current strength signals a recovery, and hikes, it will only accelerate a move lower, making things worse.

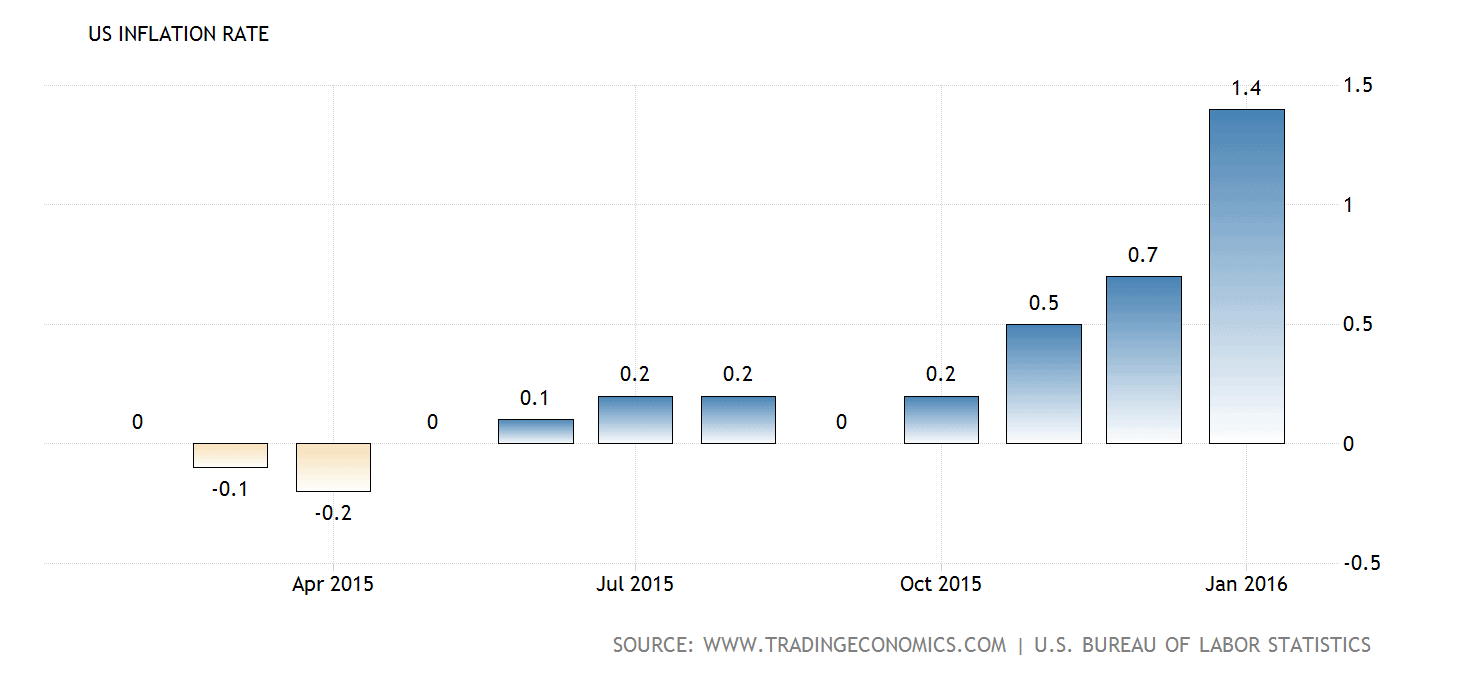

Another factor the Fed will consider before hiking is inflation. And as you can see below, the latest inflation numbers surprised to the upside.

Consumer prices were up 1.4 percent year-over-year, making a new 15 month high. Core inflation also reached its highest level in 4.5 years. Inflation numbers like these give the Fed even more evidence to raise rates.

The truth is, the Fed wants to hike. They have plotted four rate hikes this year. The market is pricing in zero. Investors are calling BS on the Fed’s rate path. The Fed’s policy of forward guidance looks like it’s coming back to bite them in the ass. Because of this, the Fed is likely to interpret any economic data with rose colored glasses — they want to be vindicated! And there is the added incentive to try and hike sooner than later so that the Fed has some dry powder for when the economy inevitably slips into recession again (which will likely be in the 4th qtr of this year).

But hiking now is not the right move for a weakening US economy. A hike will make the dollar stronger. And a stronger dollar is deflationary. We’re already in the middle of a global deleveraging. This will only add to the deflation caused by countries around the world as they deal with their debt loads. A strengthening dollar will be equivalent to throwing jet fuel on a growing house fire.

Other central banks around the world are trying to do the complete opposite of the Fed. They want to cut as much as possible. Take Japan for example. They tried to deal with their problems by introducing negative interest rate policy (NIRP). But the reaction was pathetic. The yen actually strengthened! Their plan to jumpstart inflation and spending failed miserably.

In a similar fashion, most other central banks are struggling to find new ways to help their economies. You can see below that there are almost $6 trillion worth of global bonds trading at negative yields.

40% of all government bonds in the world have now moved into that negative territory. Yet still nothing is happening.

Central banks are going to be forced to do something drastic to get their desired result. As the legendary Ray Dalio of Bridgewater recently explained:

Monetary Policy 3 will have to be directed at spenders more than at investors/savers. In other words, it will provide money to spenders and incentives for them to spend it. How exactly that will work has to be determined. However, we can say that the range will extend from classic fiscal/monetary policy coordination (in which debt to finance government spending will be monetized) to sending people cash directly (i.e., helicopter money), and will likely fall somewhere between these two (i.e., sending people money tied to spending incentives).

New policies will need to be directed at consumers. The idea of dropping money out of helicopters is a popular image that’s often depicted. It symbolizes central banks going nuclear with their monetary policies. They’ll have to print money like crazy and in the process destroy their currencies. We will see Central Bankers move closer to this in mid-March when the majors meet.

Money always flows to where it’s treated best. The Fed is trying to raise rates while other central banks are trying to cut. This will cause cash to flow to the cleanest dirty shirt… the US.

Investors will want dollars, which will exacerbate the dollar trend. And a stronger dollar leads to more deflation. It’s a dangerous reinforcing deflationary cycle that is nearly impossible to stop once it gets started. If the Fed understood this relationship better, they would wait on hiking. But with their credibility on the line, they will likely hike and cause the dollar to take off.

The primary driver of the dollar’s strength is global monetary policy divergence. We believe there’s a decent chance the Fed will hike, but even if they don’t, we’ll still get most of the same effects as if they did hike. And that’s because doing anything other than cutting rates will be at odds with the rest of world. Holding rates steady would still be considered “tightening” when compared to other countries. Especially when their central banks are experimenting with things like NIRP. This divergence will send the dollar higher.

Here’s what we see happening in various markets as this situation plays out.

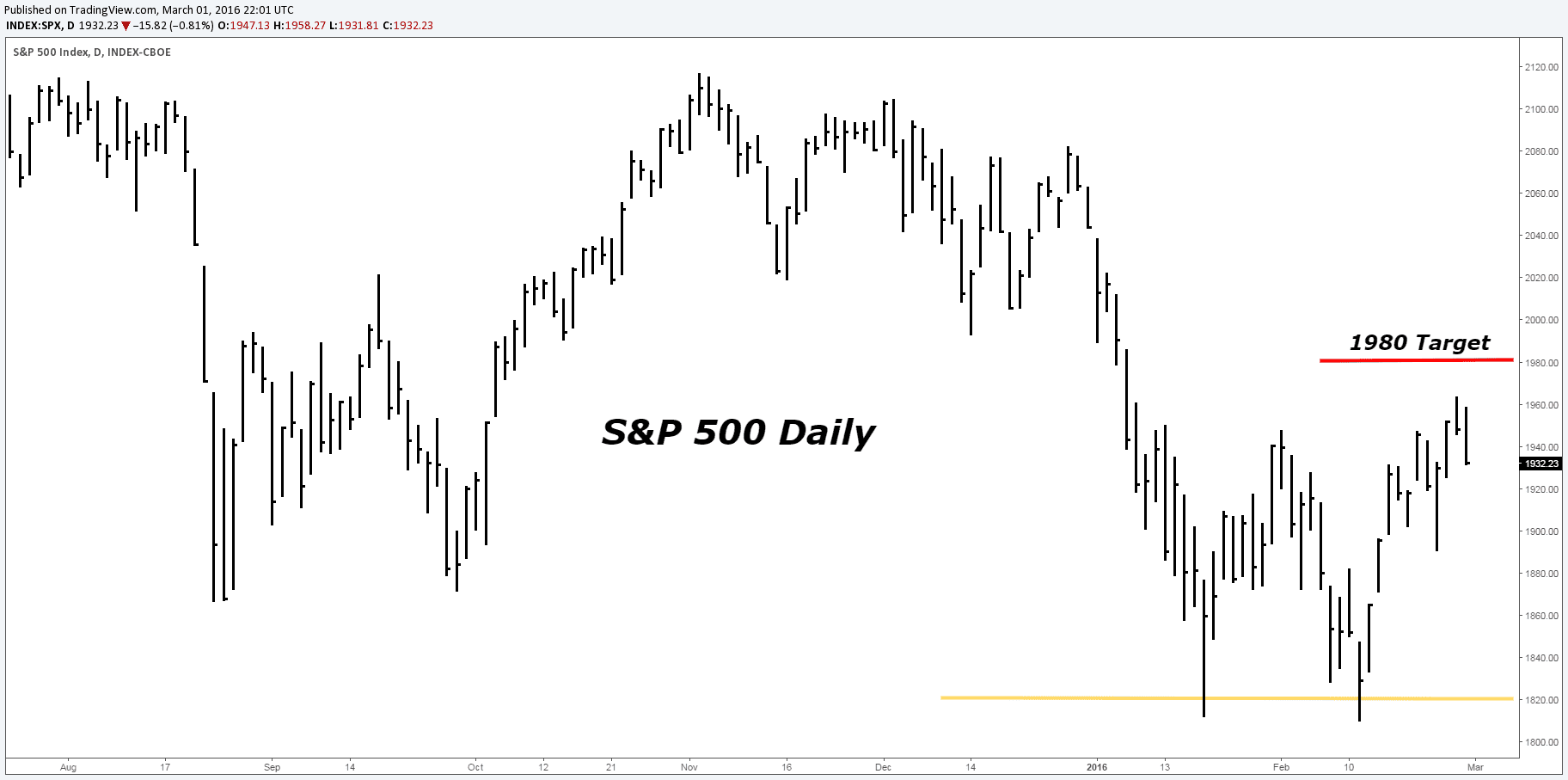

The S&P will likely retrace to the 1980-2020 area. For those looking to get short, this is where to put on a trade. After it hits this range, the index will likely fall back to test the support at 1820. Once it breaks that, there is a good chance it will fall to 1600.

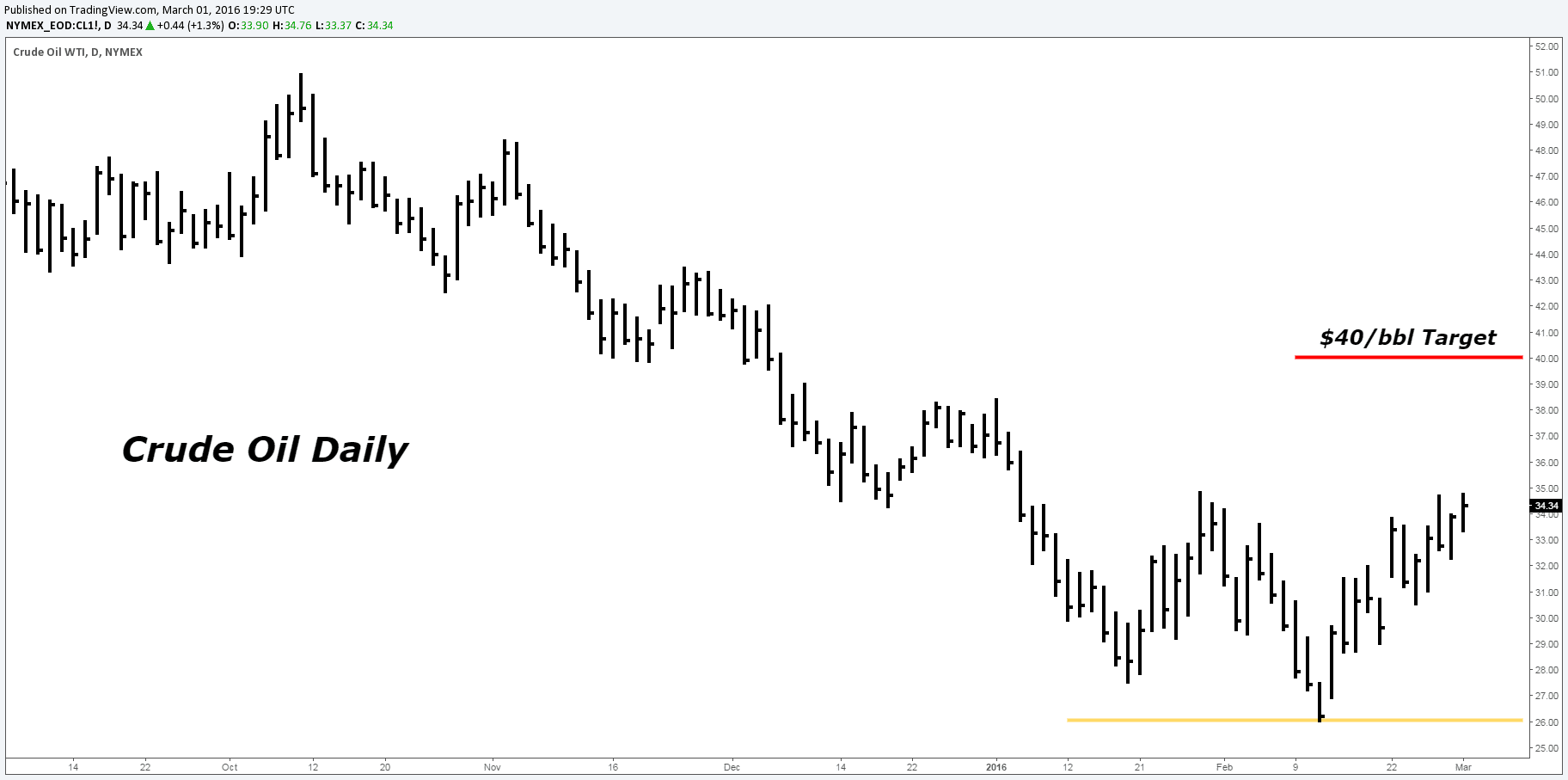

Like the S&P, oil will have a similar retrace to the $36-40/bbl area. From there we see it turning around and continuing its march lower. Our target for oil is still in the teens. The bottom won’t be in place until there’s blood in the streets of the oil exploration and production (E&P) industry.

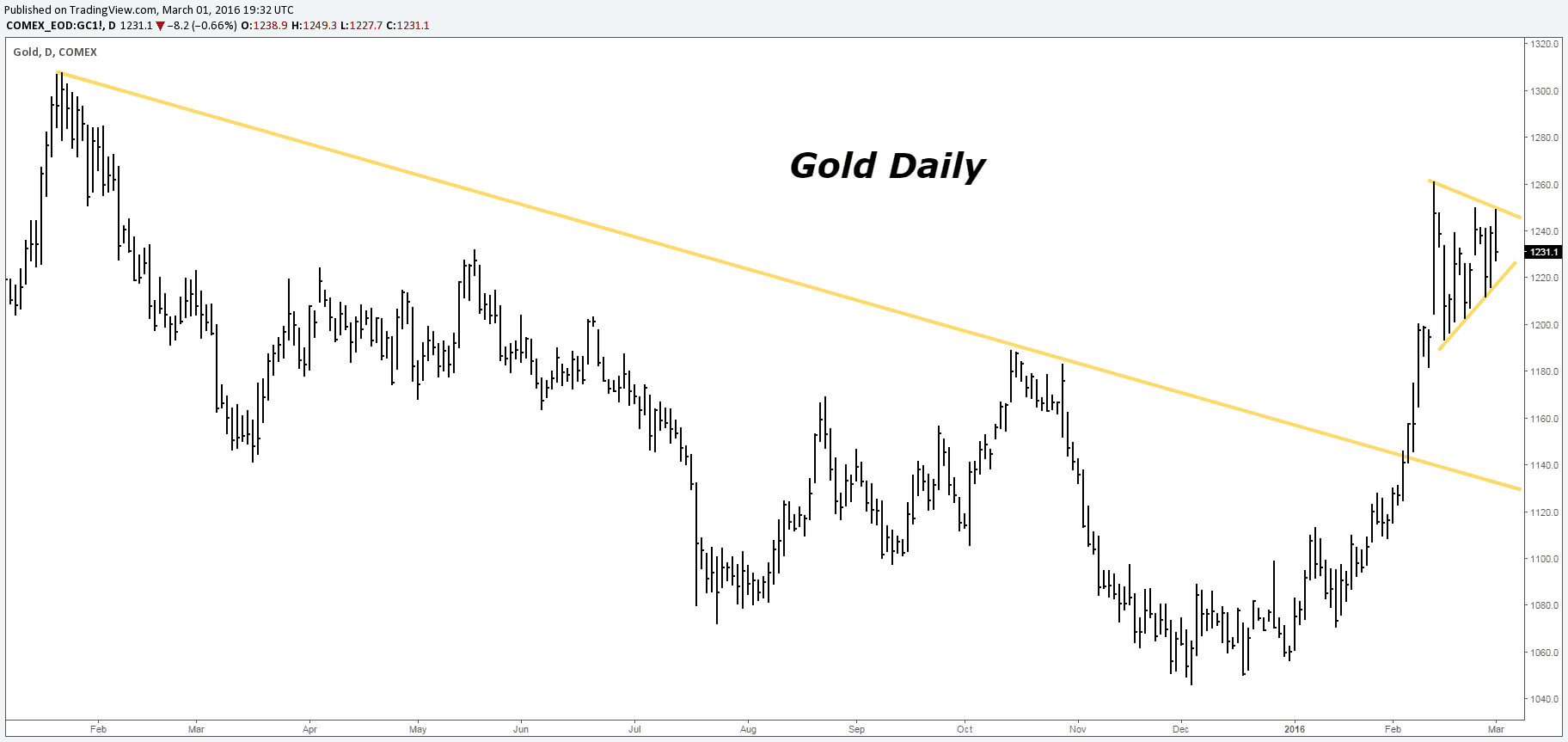

As we’ve explained in a previous article, the recent rally in gold is likely a bull trap. Just like oil, gold is a commodity. That means it’s priced in dollars. Dollar strength has a large impact on it. As the dollar gets back to trending higher, gold will fall and continue lower.

Gold is also an inflation hedge. If investors see the Fed as hawkish compared to the rest of the world, a lot of the demand for gold will subside.

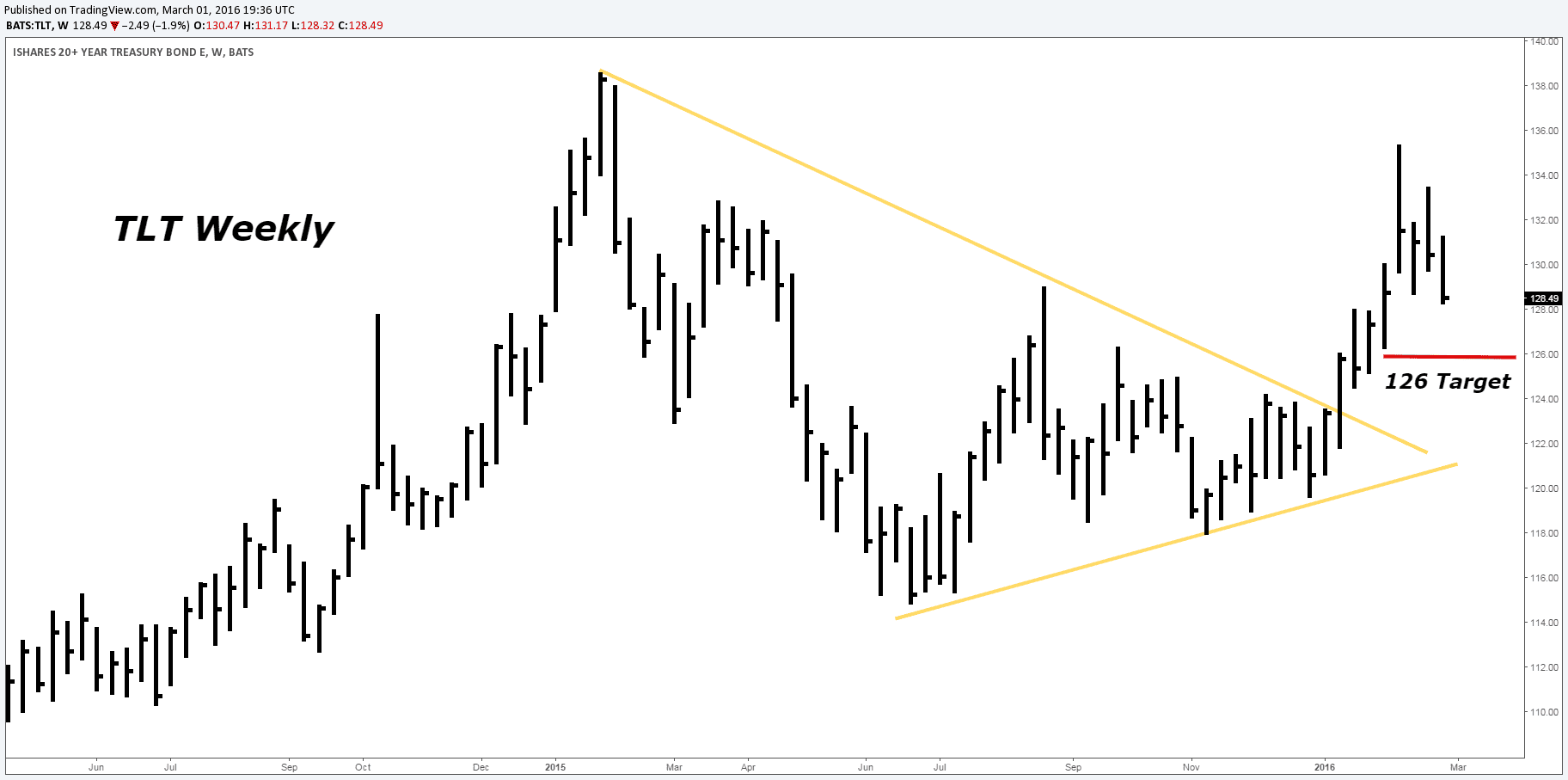

Our favorite play in this environment is long dated US treasuries. Capital will be flooding into the US due to the global slowdown. This is especially true when this is one of the few countries with positive interest rates. As global volatility picks up and the prospects for deflation become realized, investors will pile into long bonds as a safe haven.

We see long dated bonds (TLT) correcting to the 126-114 area before continuing to new highs.

Many markets have taken a break from their primary trends along with USD. But when the dollar resumes its trend, so will these other markets. Don’t be like other investors and the Fed. Don’t let the dollar deke you out!