Ah… Valentine’s Day. A day to cherish your significant other. Take them out to dinner. Sip some bubbly. Or wine if you prefer. Whatever you do, you just have to show your love. That is… if you actually remembered what day it was today. (You’re welcome for the reminder.)

Our team at Foundation almost never forgets this made-up holiday. We are gentlemen and scholars. And also very smooth, much like Teddy Pendergrass. But hey, it wasn’t always like this. We remember the days back when V-day used to make us sweat.

We’re a bit nutty over here, so we see everything in terms of markets. V-day used to always be a giant inflection point for us. Sort of like a company’s earnings release. Do you want to hold through earnings, or do you want to cut your position and run? Same with V-day. Do you really like this person? Because if you successfully perform the whole Valentine’s gig, you may be stuck with him/her for a while. So if you don’t like that person too much, you should probably cut and run before the big day.

It’s a tough choice. And it happens to remind of us of the recent events in the cloud space.

Tech investors’ love affair with cloud-based companies these past few years has been comical. Did half of them know what the “cloud” even was? Or what its benefits were? Who knows. But if a company mentioned the cloud, they bought its shares.

As investors scrambled to get a piece of these tech companies, they ironically got their head stuck up in the clouds with Cupid. Due diligence went out the window when it came to objectively evaluating these businesses. But the warning signs were all there. And the smart investors frequently pointed them out. Negative earnings. Increasing costs. Growth dependent on easy money policies. It wasn’t tough to figure out that most of these cloud companies’ business models were unstainable.

Yet no one cared. The “cloud” was hot and investors were getting all hot and bothered at just the mention of it. And that’s why we got the massive runup in various cloud names.

But this year, as Valentine’s Day loomed around the corner, investors came to their senses. And judging from the carnage, it seems they decided against making cloud stocks their Valentine….

The final straw that broke the camel’s back was Tableau’s (DATA) recent earnings report. As a maker of data analysis and charting software, Tableau was considered one of the high-flying cloud names. But after reporting a failure to harvest tax benefits from some assets investors kneecapped the stock on their rush out the door. The stock fell 50% the following day.

This disaster shook the entire cloud space. Big names like Salesforce (CRM) and SAP (SAP) dropped right alongside Tableau. And one cloud company in particular, Workday (WDAY), the human capital management software vendor, dove over 18% on the news.

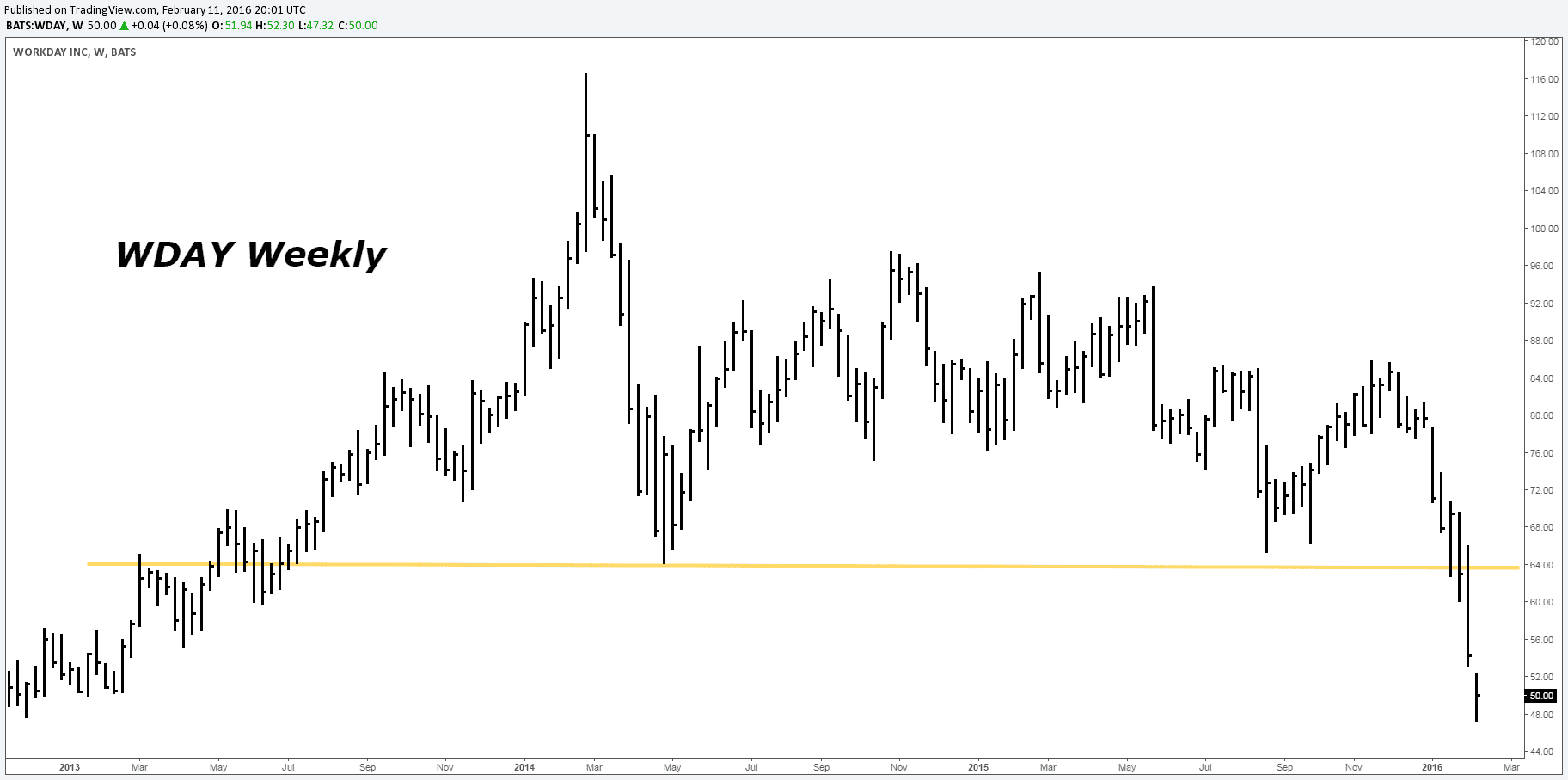

The Foundation team had a nice chuckle that night over the usual round of single malts. We got short Workday a few days before, on 1/28. We saw the huge multi-year topping pattern finally completing and we knew we had to hop our asses in there.

So far the trade has worked out pretty well for us. We’re now waiting for a good setup to pyramid our initial short position. Workday has a lot further to fall. Let’s go over why.

Easy Money, Dumb Business Model

The first thing we need to address is the rampant stupidity plaguing the tech space.

Actually, maybe it’s not stupidity. If someone offers you a bunch of free money, you would take it too, right?

That’s exactly what we’ve seen in the tech industry these past few years. Easy money policies implemented by the Fed after the 08’ crash pumped a lot of liquidity into the system. Investors suddenly had tons of cash and were being forced further out on the risk curve in search of return. And as is always the case in a free money environment, the dollars poured into the newest, shiniest, unproven business model with the hope that this lottery ticket would be the winner. This time around, that lottery ticket was tech… and cloud companies were the Powerball.

And boy did the tech companies love it. They took full advantage. With so much money flowing in, it became easy to get around the normal restrictions that keep a company financially disciplined. These companies bent the rules and built business models that relied on large, consistent streams of easy money. And by doing so, their businesses became unsustainable.

Here’s the thing, you can’t just build an entire business on the assumption that you’ll have easy money forever. If you do, you’ll be screwed when the cycle turns. And that’s exactly why a company like Workday is hurting so badly right now.

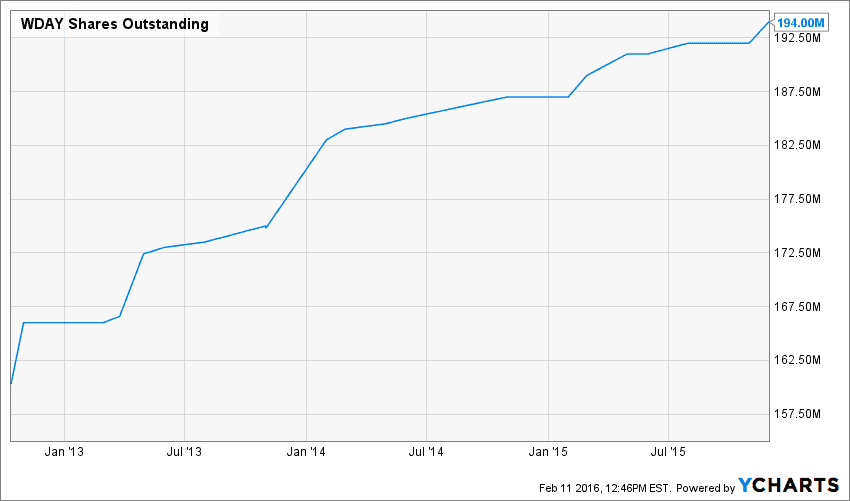

But when the times were good, they were real good. Workday is a prime example of a tech company that made sure to milk those good times. Their go-to-move was to issue new shares every time they needed to pay for something. You can see the upward trend in their outstanding shares below.

Investors loved the cloud. And they loved Workday. So they kept buying and sending the stock price higher. And in return, Workday kept issuing shares and collecting investors’ money. It was a real nice system they had going.

Everybody “won”. Investors got more cloud shares and WDAY got more money to help fuel their growth. Or really, to help buy their growth.

High sales growth is obviously essential for a growth stock like WDAY. And it’s true the company has had strong revenue gains since it ipo’d in 2012. But it’s never enough to just look at revenue growth alone. The key is to see how it came about. And in Workday’s case, they’ve been selling a dollar for 95 cents.

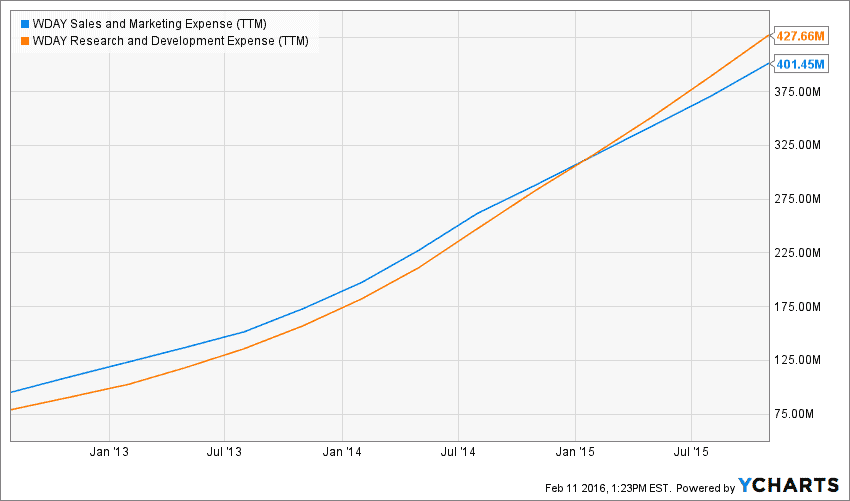

Check out the steep upward trend in their sales & marketing and R&D costs.

Their sales and marketing expense equals almost 37% of total revenue. And R&D costs equal nearly 41%. Combine them, and they take up nearly 80% of revenue… it’s ridiculous! And these costs will only keep increasing because this is how they buy their revenues. To help put it in perspective, competitor Oracle’s (ORCL) cost of sales and development is half of Workday’s as a percentage of revenue.

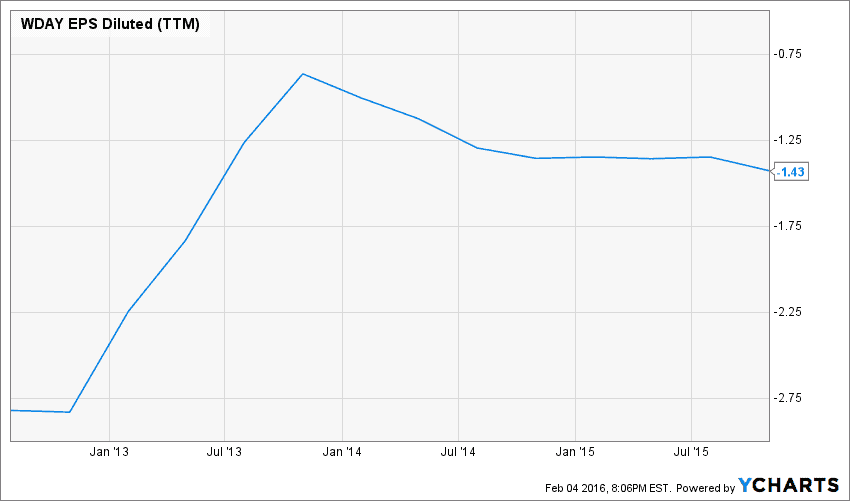

With growth coming at such an expensive price, it’s no wonder Workday has never made a dime. Take a look at their earnings per share since they’ve been public.

Not only have they consistently lost money, but in the past few years it’s been getting worse. EPS is actually downtrending as the company loses more and more.

But hey, it didn’t matter to investors.

“Losing money? No problem! Here’s some more! As long as you’re “growing”…”

Workday had no incentive to reign in its expenses because investors weren’t focused on the bottom line. Nothing was stopping them from throwing endless amounts of money into sales and development. Investors rewarded them for it and their stock price appreciated. So Workday continued to do the same thing over and over again.

There are bulls out there who claim Workday could trim these two expenses and become profitable. But there’s a problem with that logic. If they cut those expenses, where would their revenue increases come from? Their growth is completely dependent on heavy spending in those two areas.

Easy money is like heroin to a drug addict. Once you start using it… good luck kicking the habit.

And that’s why we call it buying growth. Without an increasing flow of money into sales and development, revenue growth stops.

But the easy money didn’t just go to sales and development. It also went to pay employees.

That’s the huge benefit of having a stock price that’s rocketing higher. Employees are happy to take stock options over cash. The mentality becomes “why get a lump sum now when you can get some sweet optionality with company shares?” I mean shit, the stock’s going to the moon isn’t it? Why cap your gains?

That’s how employees thought. Everybody bought into the popular delusion. And Workday took full advantage by issuing options instead of cash. The money they saved went right back into buying growth. As of November 2015, Workday had over 12 million shares in exercisable options. That comes out to an equivalent of almost 10% of the company’s current market cap. That’s a lot of shares….

So all this seems like a pretty great racket right? Just use easy money to pay for everything. The company wins, the investors win, and everybody’s happy.

But here’s the problem. This strategy only works when the stock price is rising. As soon as it decides to go the other way, shit hits the fan. And it hits hard. The whole business model falls apart. And that’s why we say it’s completely unsustainable.

Think about the new Workday employees coming through the door. Wide-eyed college kids planning to change the world through their fancy HR software. They see the stock price rising and they believe in their mission. They also swear their HR system is revolutionary. So of course they think the company’s stock is probably undervalued. Forget about the hardcore business side of it and the sustainability aspect of the model. Who cares about that. Let’s just go with the dream here. So yes, they gladly accept stock options in lieu of real cash payments. It’s clearly the better choice.

But sadly, these kids’ hopes and dreams of fixing the world really just hinge on the stock price rising. Why? Because they aren’t THAT stupid. Their badass degrees from their badass ivy league schools won’t let them be. So yea, even though they likely believe that building Workday’s HR system is as important as solving world hunger, a falling stock price still means less money in their pockets. They start to realize that they can’t go to the bar and buy rounds with options that become more worthless by the day. It’s just too hard to impress the opposite sex like that. It won’t work. So at that point, they say screw you, pay me real cash.

And this is where the model starts to fall apart. Workday needs the best talent coming in. And without a strong stock price, they have to pay up a lot more for that to happen. The cash that starts going to employees gets taken away from the growth “buying” strategy. So sales and development spending go down. This in turn causes revenues to take a hit. Lack of revenues piss off investors because they see less growth. And as always, the investors’ solution is to take their frustrations out on the stock price, which gets hammered. And now with the stock price even lower, all of Workday’s problems become worse. It makes it even MORE expensive to hire good people. Plus it’s tough to issue new shares to get cash because the demand is gone. Investor’s are turned off. And even if Workday can issues shares, they’re getting less cash for each offering because of the lower price. This leads to less spending on sales and development once again. Which leads to less growth and more disenfranchised investors. And that leads to…. yada yada yada.

You see the downward spiral forming. It turns into a giant negative feedback loop that tanks the company.

As every good drug dealer knows, you don’t get high on your own supply. But that’s exactly what Workday did with the model they built around paying for everything with their own appreciating shares. I mean, didn’t they learn from what happened to Pacino in Scarface? We wouldn’t be surprised to eventually see Workday washed up in some alleyway, turning tricks for ticks in its stock price. Metaphorically of course. If you choose to build this type of business model, these are the consequences you’ll eventually have to face.

And just remember how easy it was to start this chain reaction. All Tableau had to do was report some tax issues and the whole industry went to shit. Talk about walking on thin ice….

The Tableau earnings release was the inflection point that signaled the beginning of the end. It caused the initial large price drop that triggered the negative feedback loop, which we’re now benefiting from by being short WDAY stock.

What’s funny is that there are many companies that followed Workday’s lead and jumped into this space with the same business model. So now, not only are all their businesses in trouble, but the vicious competition between them is cannibalizing whatever revenues they’ve been able to gain thus far.

Bloody Red Ocean

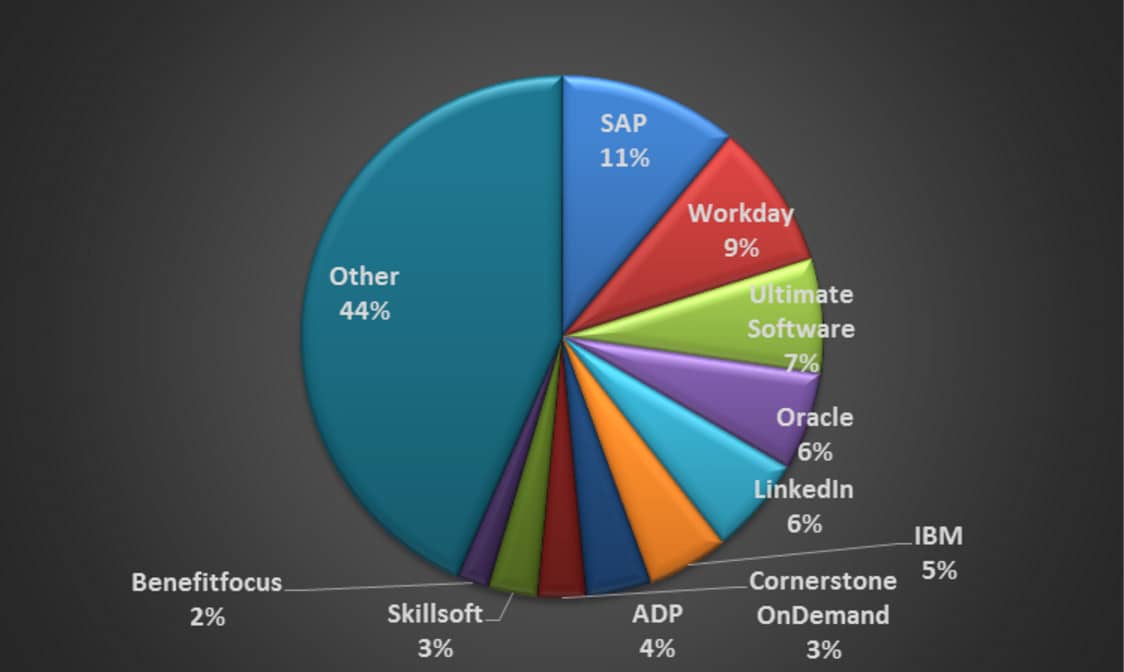

Workday operates in the Human Capital Management (HCM) solutions market. And as you can tell from the graphic below (courtesy of Apps Runs The World), the space is very fragmented.

SAP holds the top spot in the HCM market with an 11% share. Workday is fortunate enough to come in second with 9% of the market. But this percentage isn’t much of the total pie. You can see above that there are way too many companies fighting for the same customers. Not only that, but there are more companies entering the market everyday. The competition has transformed the space into a bloody red ocean where the economics have become terrible.

For example, take the competition between Workday and their archenemy Oracle. The founders of these companies have a rocky history, so they especially love screwing with each other. Oracle recently decided to offer heavy discounts to their HCM customers in an obvious attempt to steal market share from Workday. So Workday had to respond. They chose to switch up their billing model to make it more lenient on their customers. And according to analysts, this move was basically the equivalent of telling their customers “just pay us whenever you feel like it”.

Various analysts lowered their ratings of Workday after seeing the effects this billing change had on their latest earnings report. Steve Koenig of Wedbush Securities cut his price target citing disappointing revenue growth due to the new, more flexible payment schedules. Barclays and Nomura Securities also downgraded the company for similar reasons, while also commenting on the heightened competition in the HCM industry.

As the analysts mentioned, this destructive competition is widespread in the industry. It isn’t just limited to the cat fight between Oracle and Workday. SAP is another example of a company hurting from the the scrapping. They’re on record complaining about competition from various companies including Workday. But they’re not backing down. They’re willing to go to the mats too. As Chief Executive Bill McDermott explained:

So, should SAP decide to focus on a margin rate and not compete in those markets and let them have the marketplace? The answer is: Hell no! You will have to compete, in some cases, on a lower profile margin rate.

So not only are these companies losing tons of money, but the situation is only getting worse. Their negative margins are going to become even more negative. It’s a race to the bottom for market share. Investors would be stupid to expect profits anytime soon.

And all these losses are coming at a time when a lot of big companies are actually reconsidering the use of HCM software. There has recently been a lot of backlash against ranking employees with the types of systems HCM companies provide. You probably remember the scathing article in the New York Times about Amazon’s internal practices and culture. Part of the criticism included the use of HCM tools that evaluated employees. These tools were supposedly abused by management and cutthroat employees to create a toxic work environment.

Companies are thinking about moving away from these tools because they’re finding them to be ineffective. All they do is piss off employees. It’s bad enough being stuck in a cubicle. But now the company is going to do things like monitor your computer and then rank you based off that information? Really? Can you imagine that during March Madness? You definitely need as many games playing as you have monitors available. We imagine the response is likely the same among employees whose companies try to overly-penalize them for their love of college basketball:

Go Blue.

Breaking Up With The Cloud

So what we have here is a business model dependent on easy money, terrible industry economics with losses everywhere, and a possible trend away from the industry’s main product. Clearly these companies are in huge trouble.

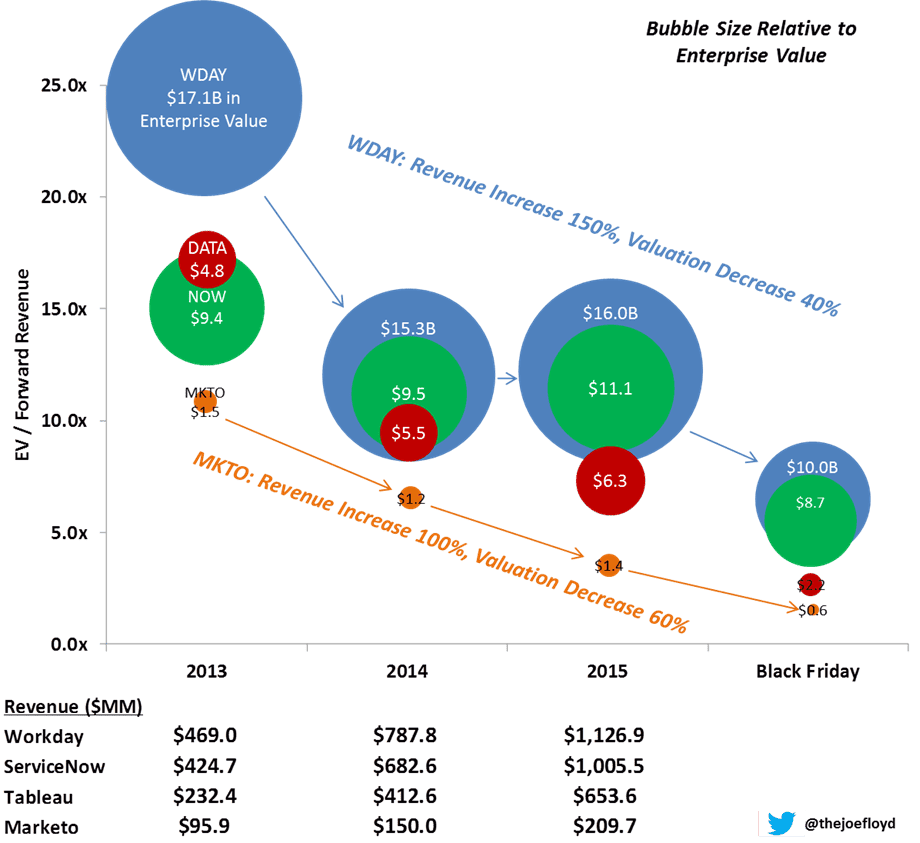

But bulls may still say that none of this matters as long as revenues are growing. They think that if there’s growth, the stock price will be fine. But this just isn’t true. This type of mentality doesn’t work in a bear market. It doesn’t matter how fast you grow your revenues when investor sentiment has changed. As VC Joe Floyd reveals in his diagram below, multiples can compress a lot faster than revenues can grow.

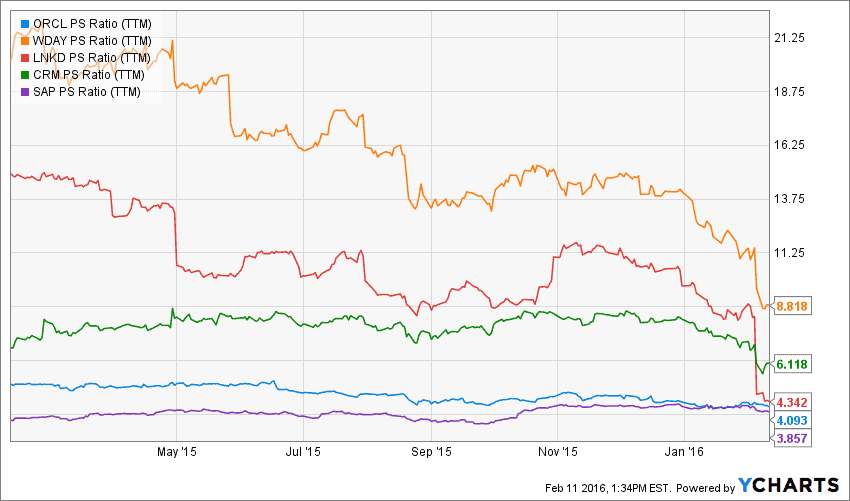

And from a valuation perspective, Workday is one of the most expensive stocks out there. Just take a look at Workday’s price-to-sales ratio compared to its competitors. It’s almost double everyone else’s.

Considering how overvalued it still is, Workday makes a great short, even after its recent fall. Our team at Foundation is currently waiting for an area to pyramid our short position. We believe the company has a lot further to drop.

Investors have finally broken up with the cloud. And Workday is the company that will be dumped the hardest.

Happy Valentine’s Day!