Luxury design online marketplace 1stDibs (DIBS) is now trading at “stupid cheap” levels. At the same time, its business continues to execute and grow its (already leading) competitive advantages.

The company currently offers investors a chance to 5x their money in ~3-5 years with considerably less downside risk at the current price.

In this note, I explain the few key reasons I love the stock. I then dissect the company’s latest earnings report.

Finally, I troubleshoot the bear thesis by highlighting its three key arguments and where I think the bears have missed the mark.

DIBS really has it all.

It has a dominant business expanding its moat daily and a stock price that reflects none of those things. This gives us a chance to buy at trough expectation levels.

Let’s get after it.

1stDibs (DIBS) Is Approaching “Stupid Cheap” Levels Here

1stDibs (DIBS) is the world’s leading online marketplace for luxury design items. The company released Q4 earnings and further cemented its position as the front-runner in the $2,000+ online transaction race.

DIBS possesses the most potent brand awareness, employs the most selective seller vetting process, and has a ~20-year head start on the competition.

There are a few key reasons I’m so bullish on the company.

First, the market opportunity is enormous ($200B+) with little existing competition at DIBS’s Average Order Value (AOV). ETSY and FTCH, two common comparables, boast AOVs of ~$30 and $568, respectively.

Nobody comes close to DIBS’s $2K+ price point dominance.

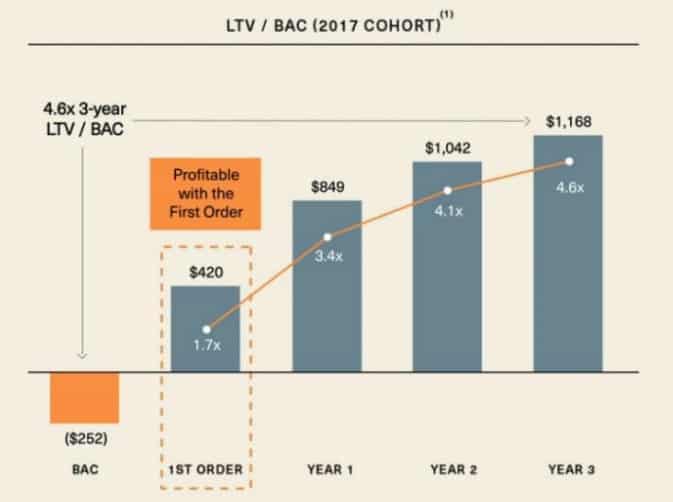

Second, DIBS has wildly attractive LTV/CAC economics. Customers are profitable from the first order and generate ~4.6x their CAC after three years.

Third, the company has multiple low-hanging growth levers to pull to juice revenue and gross profit growth over the next few years. They’ve already accomplished some of them, like

- Adding an Auctions platform (which they did in 90 days)

- Creating an NFT marketplace

- Adding local language capabilities on international websites

These factors, combined with a collapsing share price, create an opportunity to make 5-10x our money over the next 5+ years with a potential buy-out kicker to boot.

Let’s dive into the company’s latest earnings report.

DIBS Q4 2021 Earnings Breakdown

Here are the highlights of DIBS’s Q4 earnings call:

- Revenue increased by 25% YoY to $102.7M

- Gross profit grew by 26% YoY to $70.6M (68.7% margin)

- Active Buyers increased by 25% to 72,500

- Seller Accounts grew by 20% to 4,700

- Registered User Base increased by 20% to 4.3M

Trust is the most crucial factor when shopping online for luxury design items. That’s why it’s encouraging to see that GMV from listings priced between $2,000-$20,000 outpaced overall GMV growth.

DIBS buyers are becoming increasingly trusting of the platform and are buying more higher-priced items.

Auctions are also a hit with buyers and sellers. 15% of sellers have listed a product on Auctions since its launch and GMV hit $1M in <10 weeks.

CEO David Rosenblatt reiterated my thoughts on Auctions as it relates to consumer behavior during the earnings call (emphasis mine):

“But more specifically, it has to do with pricing, and that either consumers believe that the pricing is too high or that they don’t have the ability to interpret that pricing. Auctions, of course, are the best vehicle for price discovery and address that head on. So our expectations for auctions are high because, again, they address the primary reason why items don’t sell on the marketplace.”

Additionally, the company will launch its first local language sites in France and Germany during 1H 2022, DIBS’s two largest non-US markets. This is a big deal as 30%+ of DIBS’s users reside outside the US.

It’s important to note that these are low-dollar investments that will have exponential benefits to DIBS’s demand-side liquidity.

Doing All The Right Things … So What’s Up With The Stock?

DIBS is doing all the right things. They’re growing active buyers and registered users (read: future buyers) while increasing the number of sellers and products offered.

The company ended 2021 with $14B+ in GMV, up from $10B in 2020. $14B is merely scratching the surface on what’s available to DIBS if they execute.

As of this writing, you can buy DIBS for ~$300M market cap. Half of the company’s market cap is in net cash, so you’re really paying ~$140M for the operating business.

So what’s up with the stock price? What are investors missing?

A few things …

First, yes, DIBS benefited from a COVID pull-forward in demand. This makes next year’s revenue growth rates optically low (~11%). And sure, maybe it does come in at 11%.

But again, you’re not paying for growth at the current prices.

Moreover, next year’s growth does not matter for the long-term bull thesis.

The most important question to ask regarding this worry is: “will more people buy luxury goods online in ten years than they do today?”

As long as that answer remains “yes,” it doesn’t matter whether DIBS grows revenues 11% or 30% this year.

What matters is that they continue to steward the world’s leading luxury online purchasing infrastructure. Infrastructure that allows buyers to access goods they otherwise would never see, and connect sellers with buyers they would otherwise never sell to.

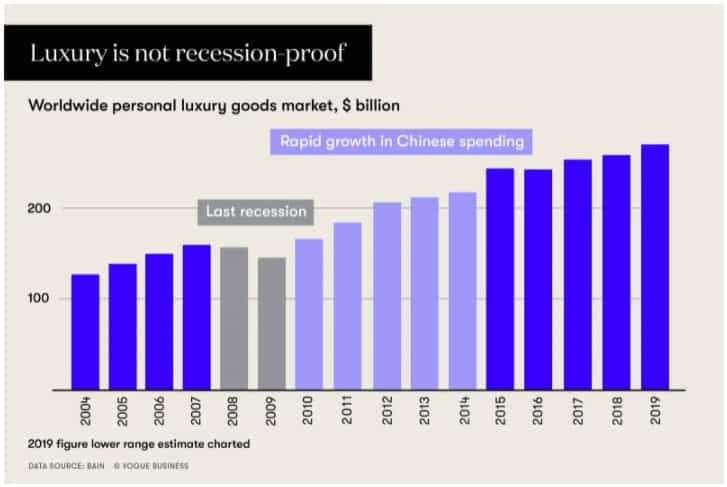

Second, investors are worried about a real recession and how it might impact luxury goods spending. Yes, luxury goods do suffer during recessions, but not as badly as you’d think.

For example, luxury goods lost ~9% of its market value during the Great Recession. Not good, but better than nearly every other industry. On the other hand, luxury goods recovered faster than other industries exiting the recession.

Things get interesting when you peel back the layers of the luxury goods onion.

Take heritage brands like LVMH, for example. LVMH’s top-line was ~flat during the recession. Richemont, another luxury brand, actually grew revenues ~2.4% per year during that time.

Compare that to high-end department stores, which suffered ~25% revenue declines in 2009 as they hemmorgahed beneath a bloated fixed cost structure.

The above two data points give us a probability of DIBS’s future during the next recession.

And that probability looks very different than what the market is pricing in.

Here’s why.

DIBS operates a high-margin, asset-light online marketplace. They don’t have massive fixed costs like leases, etc.

DIBS operates a high-margin, asset-light online marketplace. They don’t have massive fixed costs like leases, etc.

This means DIBS can rapidly adjust its spending and margins in an economic recession.

Remember, the company is profitable if you back out growth spending. Oh, and there’s the whole $170M in cash on the balance sheet without a cent of long-term debt.

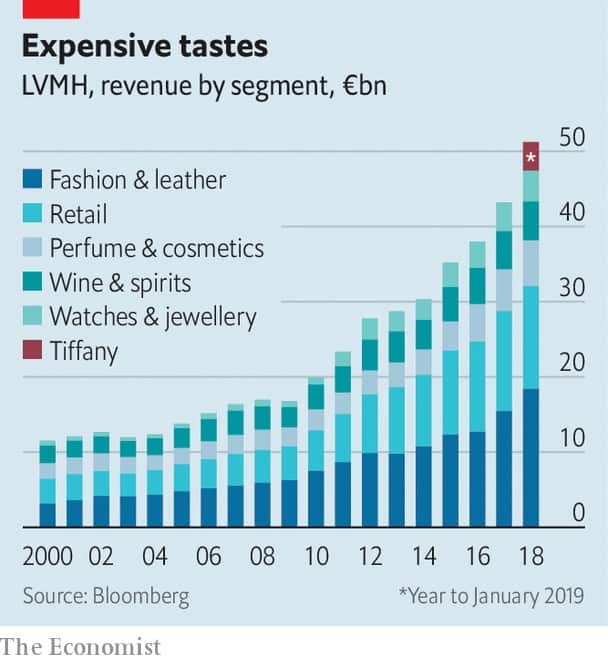

DIBS’s GMV also consists of the highest quality luxury goods, like the LVMH’s and Richemont’s of the world.

The quality of goods on the marketplace should act as an additional buffer during recessions as consumers see these items not as consumables but as investments.

Third, investors worry when they see slower purchase volume growth versus more robust registered user growth. Because on the surface, it looks like fewer people are purchasing items on the marketplace (i.e., more lurkers).

More lurkers and more items result in a smaller Average Order Per User ratio, at least in the short term.

I believe that this is a structurally good thing for DIBS’s business.

In essence, DIBS is amassing incredible potential buying power from its growing userbase. The coil just hasn’t sprung yet, but it will.

A $2,000 online transaction takes time. It requires monumental trust in the platform, which takes time. It needs consumers to scale Sears-Tower-level psychological barriers to entry.

Here’s why that matters. Once that trust is forged, a cascade of positive things happens.

Active buyers purchase more goods on the platform, raising average order values and average orders per buyer. More buyers buying more items lowers the height of the trust barrier, so to speak.

In turn, this makes it easier for registered users to convert to active buyers, bringing more transactions on the marketplace at a greater frequency.

In that reality, DIBS generates exponentially more revenue from its existing customer base without paying for customer acquisition.

This, of course, leads to structurally higher profit margins and a more substantial network effect for both buyers and sellers, as more buyers incentivize more sellers on the platform, etc.

To summarize …

Bears Say: Slowing growth is a sign of COVID pull-forward, and DIBS won’t regain 20%+ top-line growth.

- The Reality: This year’s growth rates don’t matter. More people will buy luxury design items online in ten years than they do now, and DIBS has that market cornered.

Bears Say: We’re about to enter a recession, and nobody will buy luxury items during a recession.

- The Reality: Luxury goods companies suffer during recessions, but not as bad as people think. Additionally, the quality of DIBS’s GMV, its strong balance sheet, and flexible business model insulate it well during a recession.

Bears Say: Lower purchase order growth compared to registered user growth means fewer people buy goods on DIBS

- The Reality: The $2,000 order takes trust and time. DIBS is fostering a massive base of potential buyers that should convert into high-paying, higher-frequency active buyers over time

What’s The Prize If We’re (Directionally) Right?

DIBS is radically undervalued at the current price and offers investors a 25% 10YR IRR.

Today, you can buy the operating business for ~$126M. That operating business will likely generate ~$70M in Gross Profit in 2022 or more than half its current Enterprise Value.

The company is barely scratching the surface of a $200B+ industry at the inflection point of online sales adoption.

Additionally, DIBS has one of the strongest balance sheets in consumer tech with a sharp CEO at the helm who knows a thing or two about digital businesses (having led DoubleClick to a Google buyout previously).

Q4 earnings reinforce DIBS’s competitive advantage in the $2,000+ online transaction space, and there are no signs of slowing down. And these advantages compound as the company grows, which they should at ~20% per year over the next five years.

In five years, DIBS could likely generate $110M+ in gross profit at 10-15% EBIT margins. Eventually, the company can reach 25-30% EBIT margins as it reduces growth capex and leverages SG&A.

If we assume a modest 7x multiple on gross profits, you get a price that’s 250%+ higher than today.

In other words, we can reasonably create a reality where DIBS earns a ~25% EBIT yield over the next ten years.

Think about that for a second.

How often do you find a 25% EBIT yielding business that also has …

- A leading position in a fast-growing, $200B+ market that’s rapidly shifting towards the way it does business

- Half its market cap in cash with no debt on the balance sheet

- Ridiculously high 4.6x LTV/CAC ratios and customer profitability from the first sale

- Low-hanging fruit to quickly expand customer base and increase sales

- World-class CEO that’s well connected with industry peers and has built a strong team around him

Not too often. Yet that’s precisely what we have with DIBS.

We’ll look to get a starter position in DIBS very soon. The chart is still broken, so we’ll treat it like a DOTM call option with no stop-loss and look to add over time.