“The Big Debt Cycle is just one of several interrelated forces that together make up what I call the Overall Big Cycle or just Big Cycle. For example, Big Debt Cycles influence and are affected by largely coinciding big cycles of political and social harmony and conflict within countries…” ~ Dalio, How Countries Go Broke: The Big Cycle

Summary: This continues to be one of the most hated rallies in recent memory. This type of (dis)belief is precisely what fuels an enduring bull market (read my thread on how this works here). Breadth, sentiment/positioning, and technicals all remain supportive of the continuation of the trend. On the slightly negative side of the ledger, we have short-term trend overextension and weak seasonality over the next two weeks. So we could see a minor correction here, especially if the Fed’s messaging disappoints. But any correction should be viewed as an opportunity to add risk. Additionally, the short USD position continues to set up. ARK ETFs are breaking out, and more…

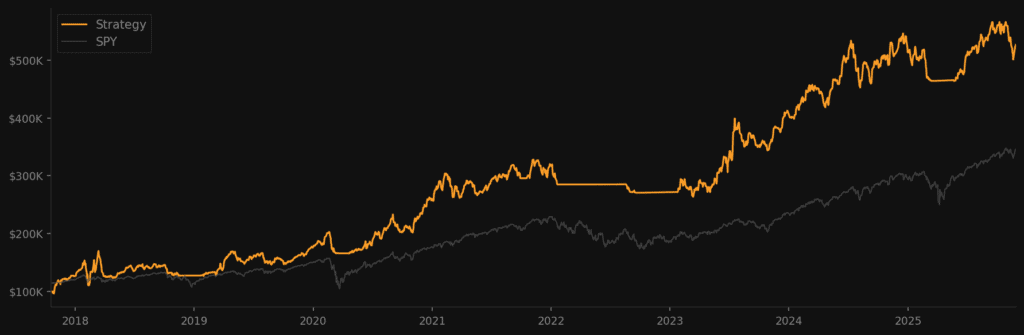

***The MO port is up +35.1% ytd, and we’re not seeing a shortage of great opportunities in this market. If you’d like to join me, the MO team, and our Collective of sharp, supportive investors and traders as we navigate these markets, then click the link below. I look forward to seeing you in the group.***

Join The Collective

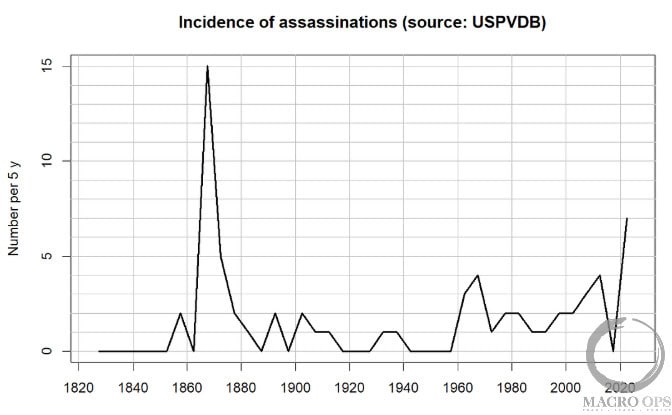

1. In Peter Turchin’s recent Substack post (link here), he highlights that “According to my US Political Violence Database (USPVDB), the five years from 2020 to 2024 saw seven assassinations. This is higher than the previous peak during the 1960s, although only half as large as that of the late 1860s”

As a longtime follower of Turchin’s work and his structural-demographic theory (SDT) — which explains long-term cycles driven by elite overproduction — I’m eager to dive into his latest book, End Times. The surge in political violence today reflects the convergence of multiple long-term cycles—including the debt cycle, SDT, Gurri’s theory on technology-enabled decentralization, and Kondratiev waves—coalescing into one major overarching cycle, as Ray Dalio describes it. This is why I fully, though regrettably, expect the upward trend in political violence, social unrest, and geopolitical tensions to persist throughout the coming decade.

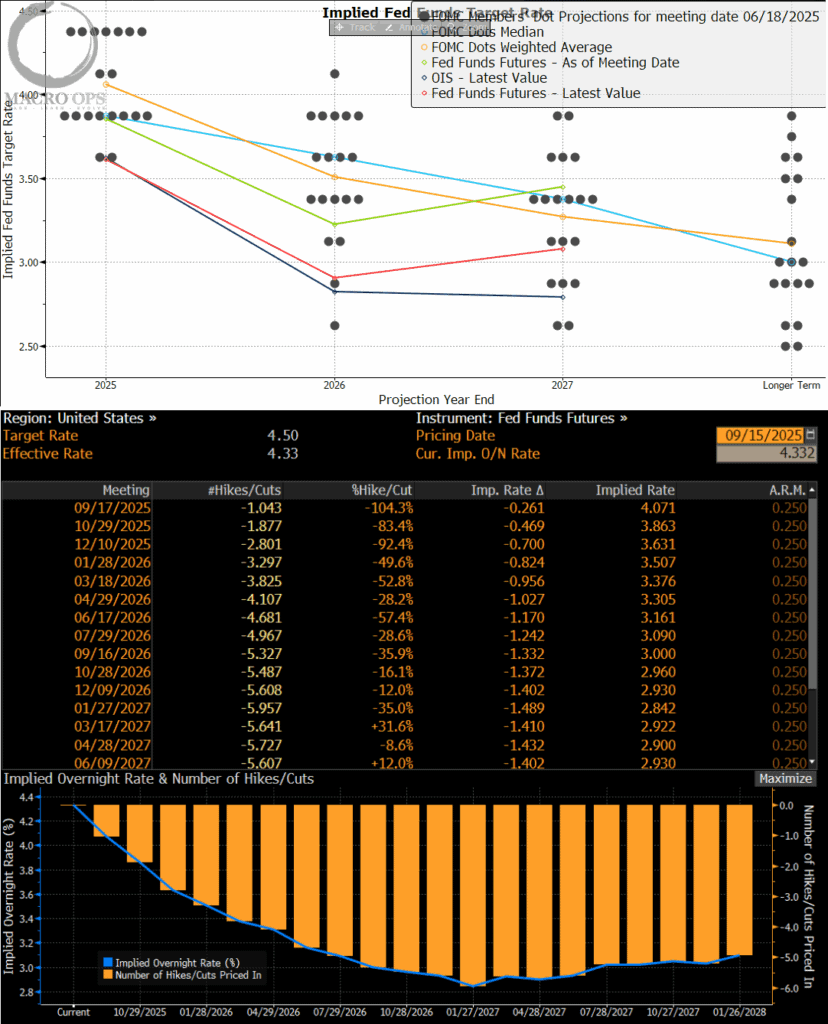

2. The FOMC is the big event this week… the market is currently pricing in 70bps in cuts by year’s end. I’m not sure we’ll get there. I’m increasingly in the “reflation” camp, as I’ve been seeing improving growth impulses in both the US and RoW, as well as rising inflationary pressures.

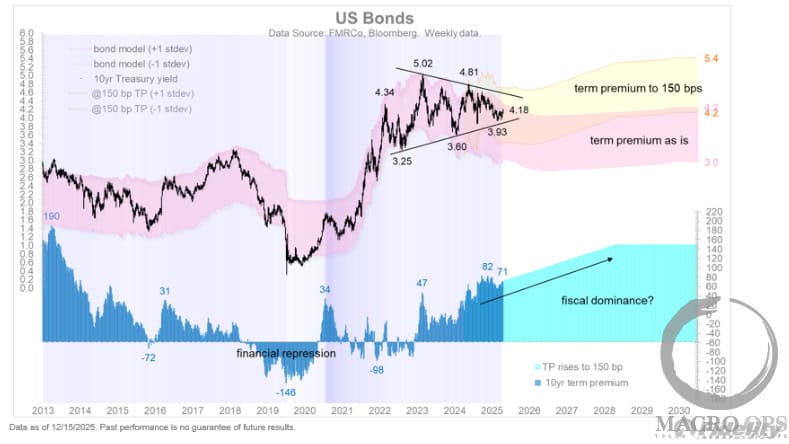

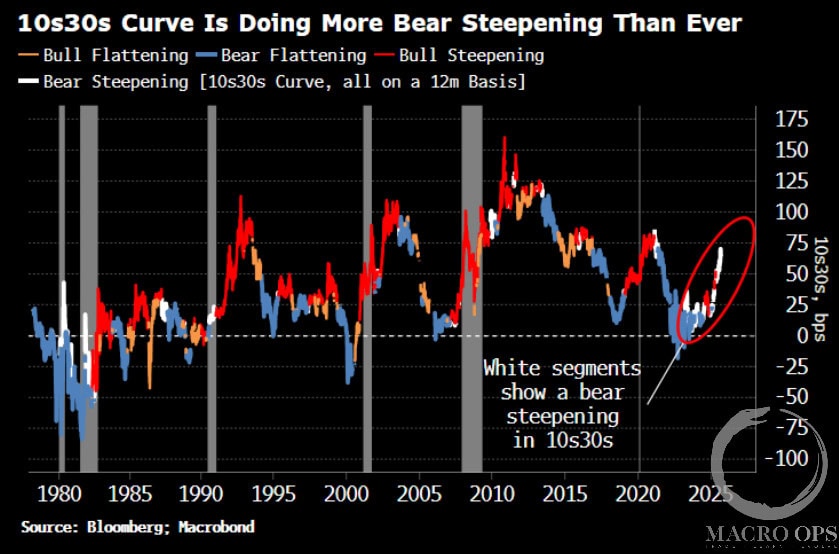

3. BBG’s Simon White recently shared the following: “fiscal concerns are in abeyance for now as the Federal Reserve looks likely to bow to its sovereign master and loosen policy. But the yield curve has not forgotten them.” The 10s30s curve is “behaving in an unprecedented way. It is bear steepening — yields are rising and longer-maturity yields are rising more than shorter ones — and it has done so for more days over the last two years than ever before in the almost 50 years there has been a 300-year Treasury bond.”

We’re long the front end but remain suspicious of the recent bid in the long end.

4.This 👇

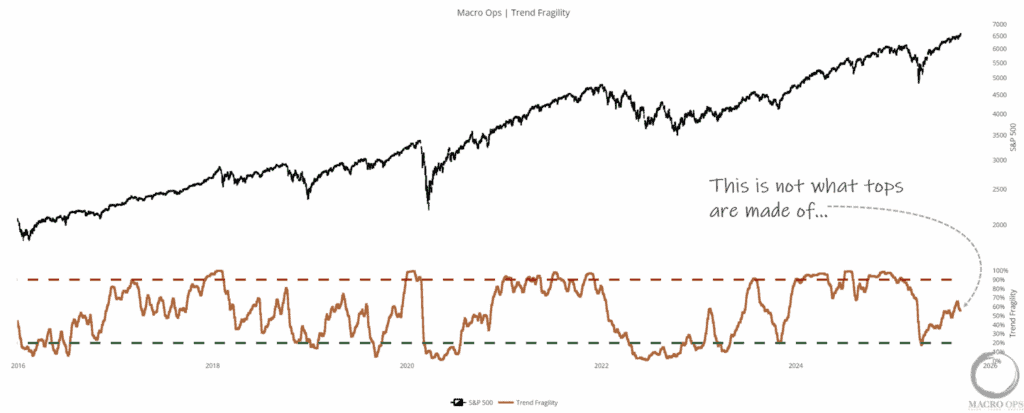

5. This remains one of the most hated bull rallies in recent memory. Despite the SPX making new all-time highs last week, our Trend Fragility indicator (a composite of sentiment and positioning data) edged lower, from an already subdued level. For those of us who’ve been long and buying, this is precisely the type of disbelief we want to see. Love it…

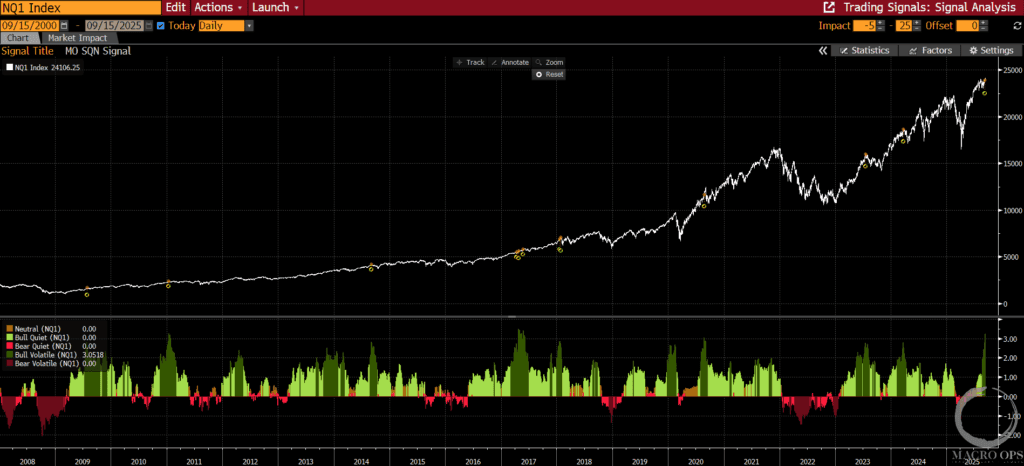

6. Will we see minor pullbacks along the way? Of course… though with readings like the above, expect them to be relatively small (think 4-7% range). However, there are growing signs of trend extension, such as our SQN indicator, which is in a Bull Volatile regime with a reading of 3+. Read this to learn more about our SQN Market Regime indicator here.

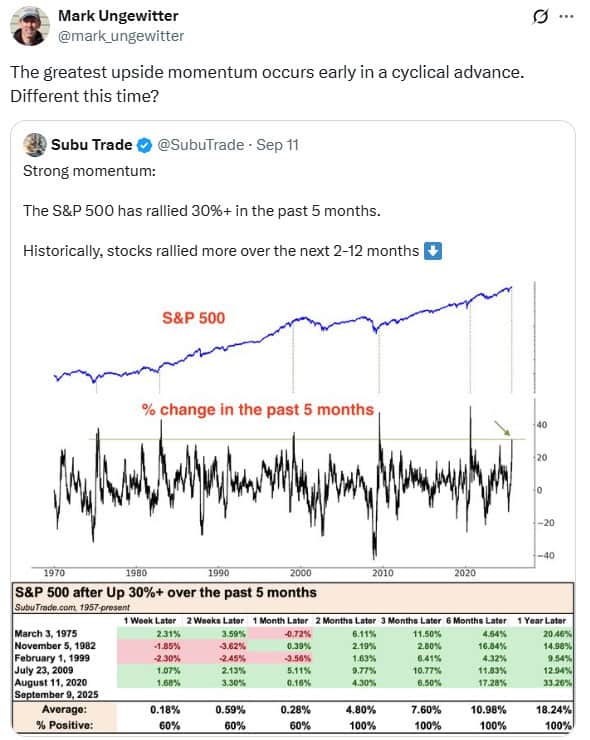

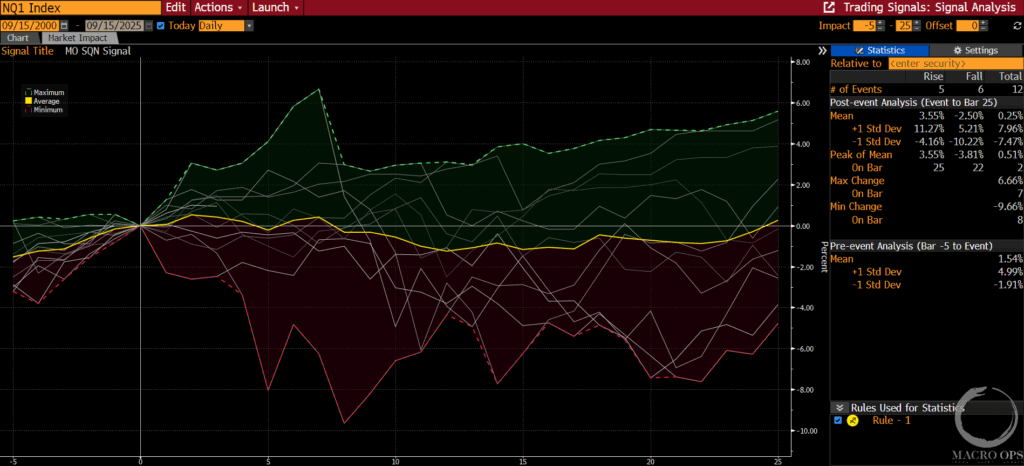

7. The following shows the forward 25 trading day returns following past instances. There are 12 events total, with five rising over the following month and six trading lower, with the average (yellow line) showing a gain after a brief dip.

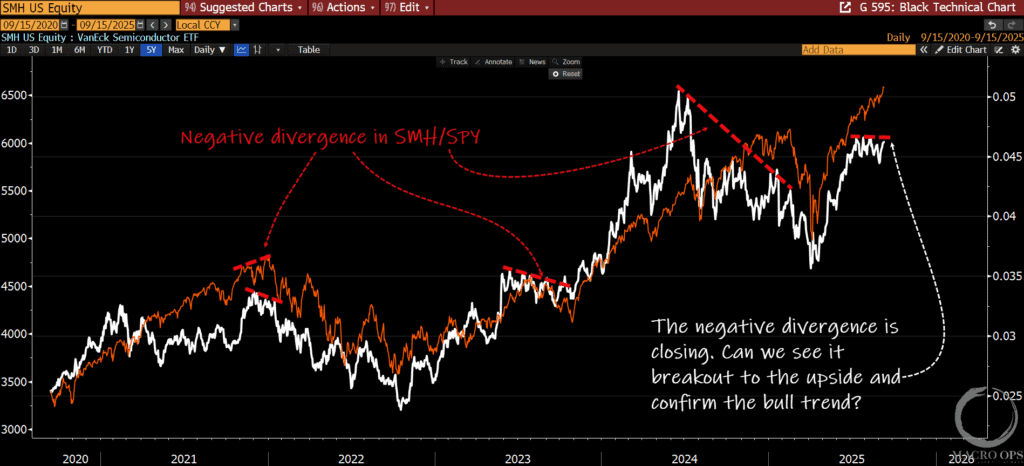

8. One thing I’m tracking is market internals. We’d seen weakness over the past month in QQQ/SPY, SMH/SPY, and LQD/IEF. The latter has resolved, but both Qs and semis have lagged, which is not ideal if you’re a bull. But… both have recently rebounded off their relative lows. The chart below shows SMH/SPY in white and the SPX in orange. A breakthrough to the upside to confirm this bull trend and would be a nail in the coffin for these stubborn bears.

9. And semi breadth suggests we’ll get there. The % of semi stocks trading above their 200dma is north of 80% and climbing. Semis are a sector that tends to lead. This is not bearish.

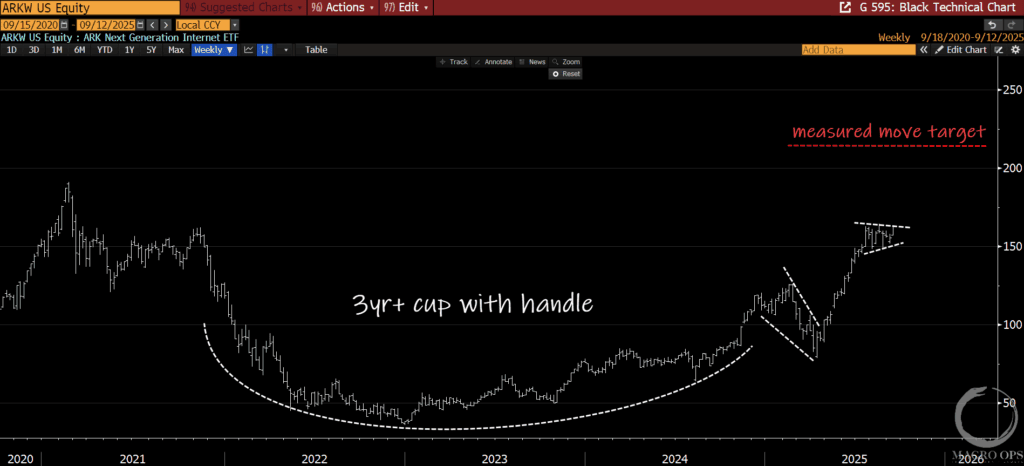

10. A number of ARK’s ETFs (ARKK and ARKW pictured below) look poised to break out of a recent compression regime. The chart below is a weekly.

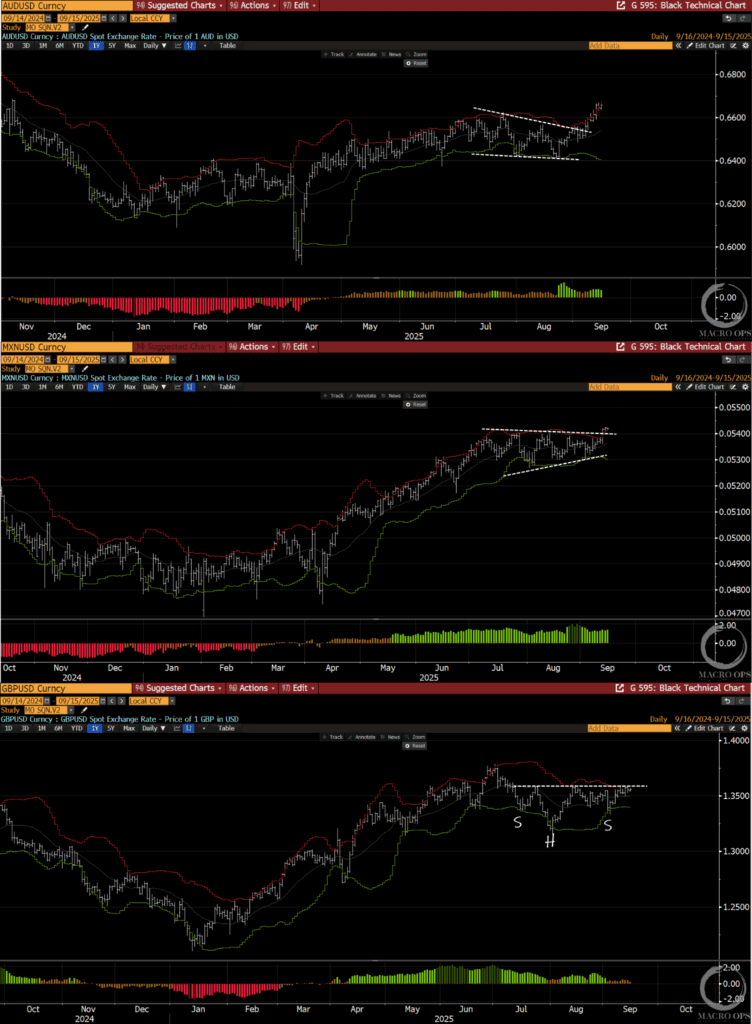

11. We’re short the USD and will continue to add to our position as long as we continue to see charts like those below (top to bottom: AUD, MXN, and GBP).

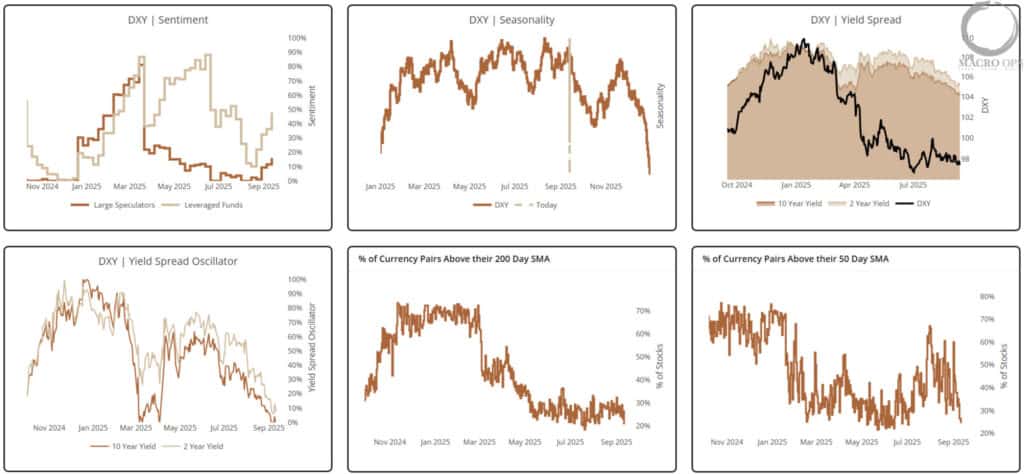

12. DXY breadth is awful, yield spreads and spread momentum are heading south, and seasonality is about to turn significantly down.

Join The Collective

Thanks for reading.