“Seek facts diligently, advice never.” ~ Philip Carret

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at mean reversion and record hedging driving the indices higher, we pair this bullishness with some concerning cyclical action and a downright bearish indicator, before then taking a look at global defense spend, a defense contractor, and big whales getting out of big tech, plus more…

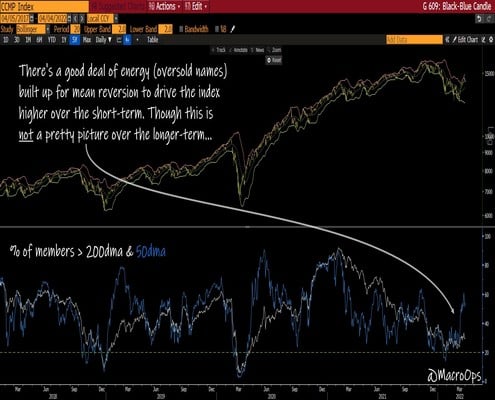

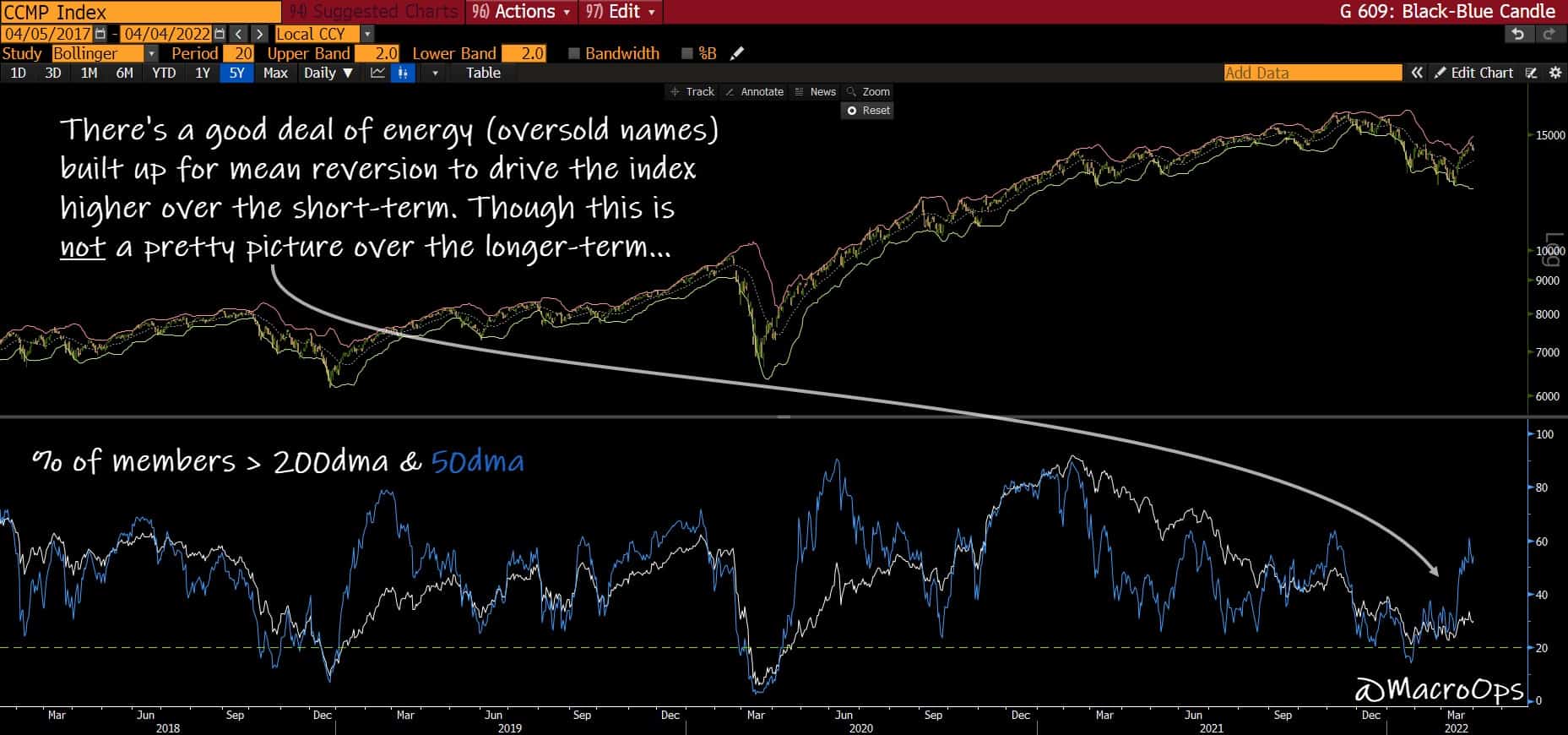

- Sometimes breadth gets so bad it’s good. This is due to the power of mean reversion. One of the three driving factors of market technicals, the other two being trend, and momentum. This is the case for the Qs right now where the percent of members trading above their 50 and 200 day moving averages fell to the 20% level two weeks ago. The market bottomed soon after. Short-term this is bullish. Longer-term these weak breadth trends are bearish…

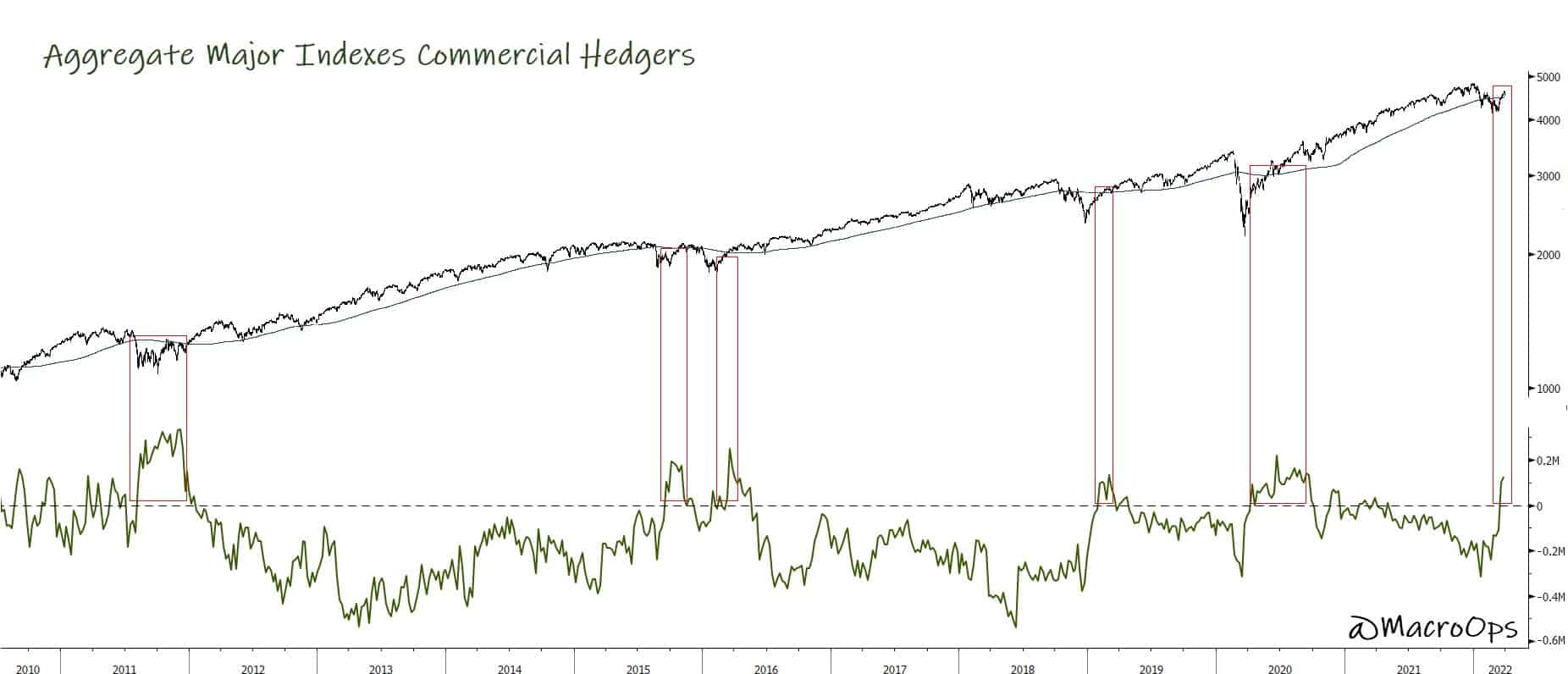

- Sentiment and positioning have also been a tailwind to the bulls as of late. Here’s a chart of the aggregate commercial hedger positioning amongst the major indices, showing near record longs (implying very short specs).

- Not all is rosy though and one thing you should be tracking is Cyclical vs. Defensives, which led the market weakness at the turn of the year.

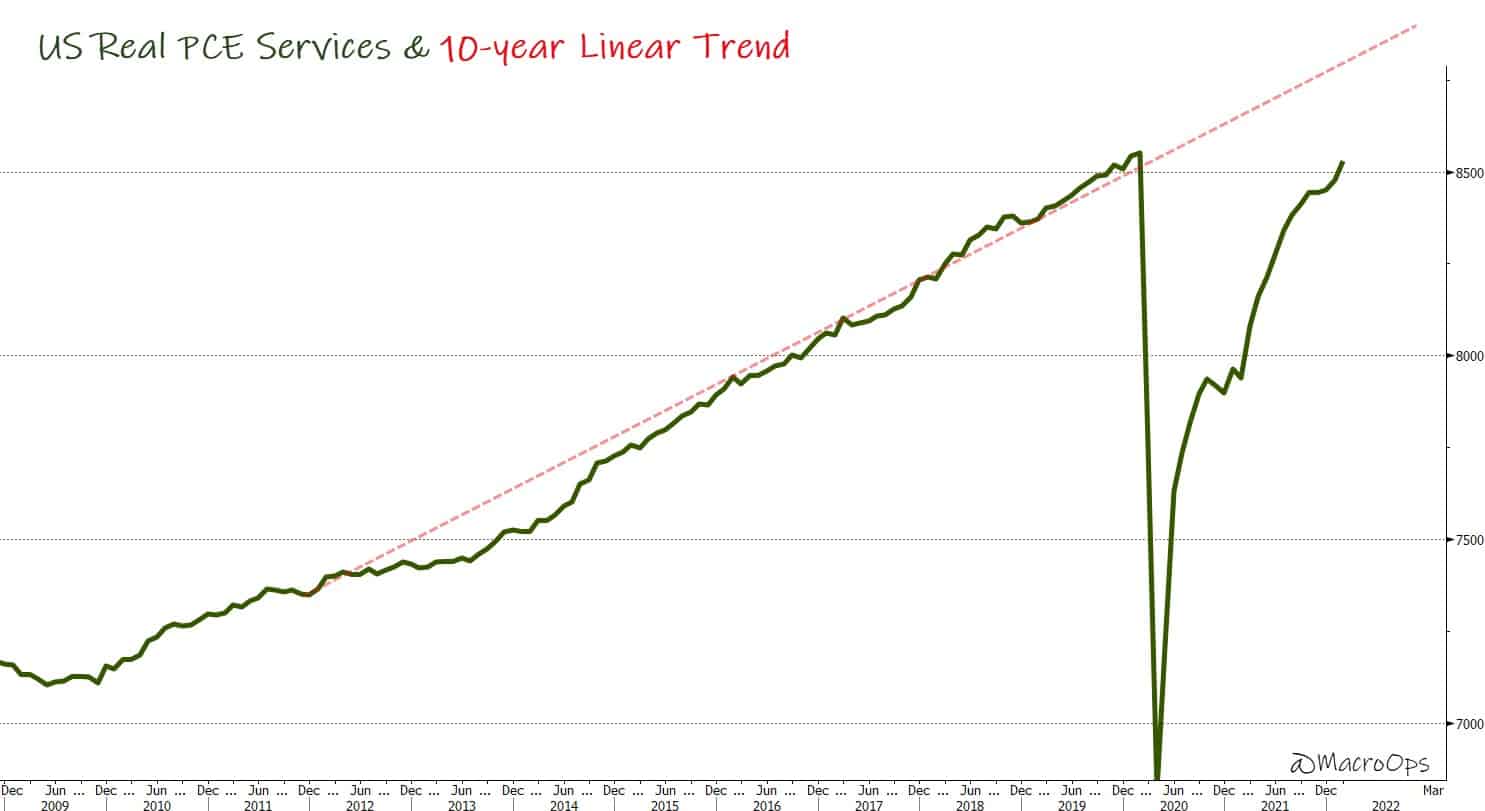

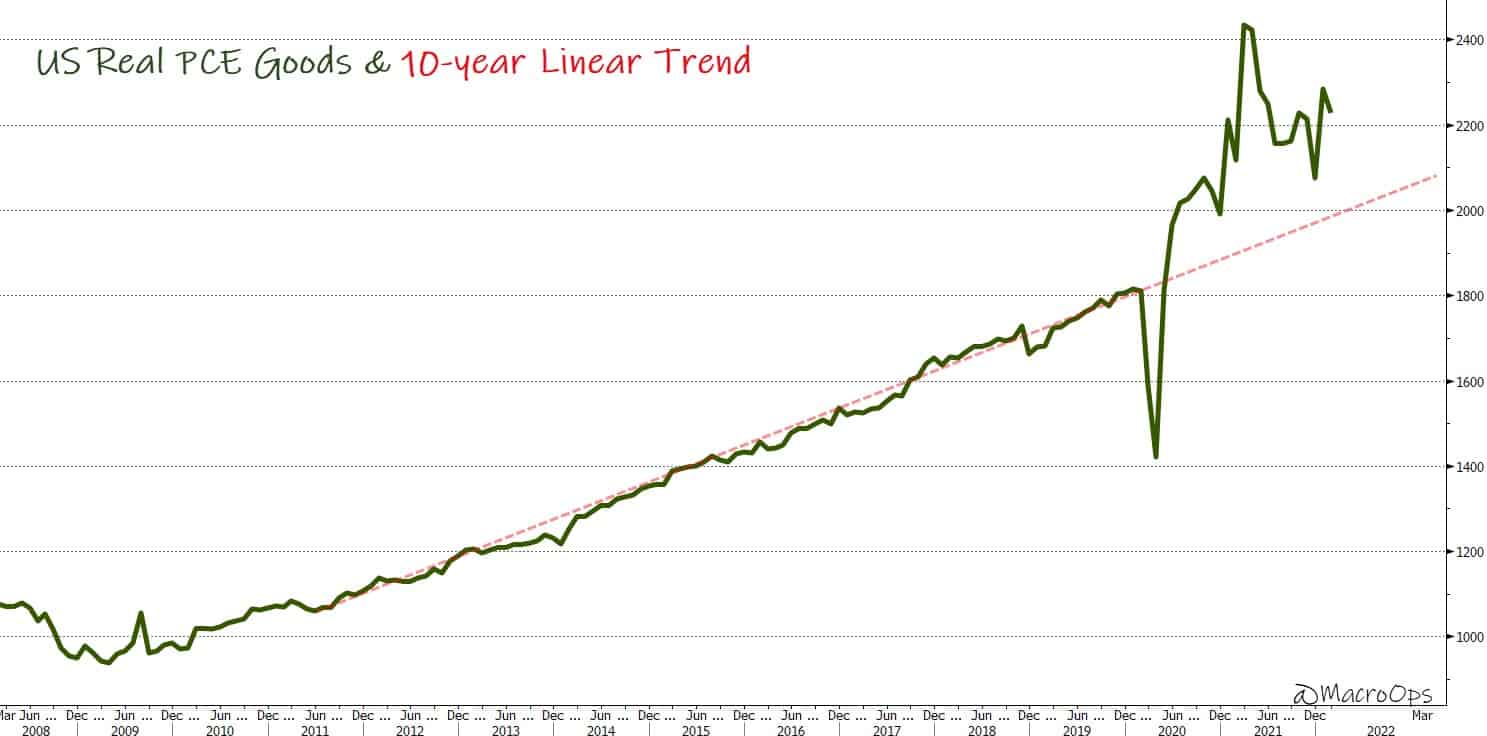

- We are witnessing the great convergence between services and durable goods. Expect a continued pickup in consumer demand for services and experiences…

- And a slowdown in goods which should ease up pressure on supply chains as well as inflation.

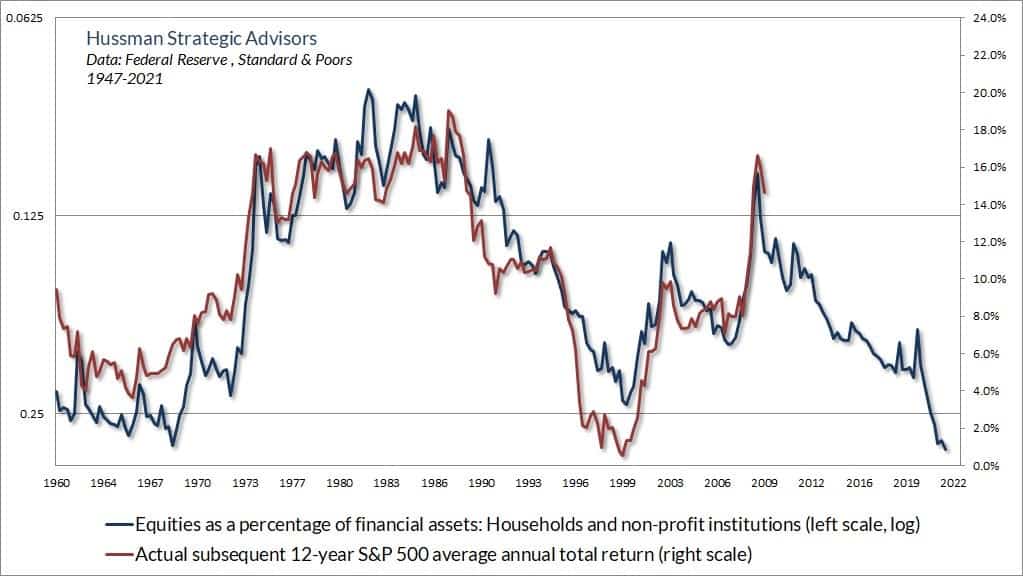

- US equities are a bit rich… @hussmanjp tweeted the following last week:

So this is fun. The share of household financial assets invested in stocks ended 2021 at the highest extreme in history (and our most reliable measures are even worse). The last two times we got close, the S&P 500 lagged T-bills for the next 13-18 years.

This is the perfect long-term backdrop for precious metals though (link here)…

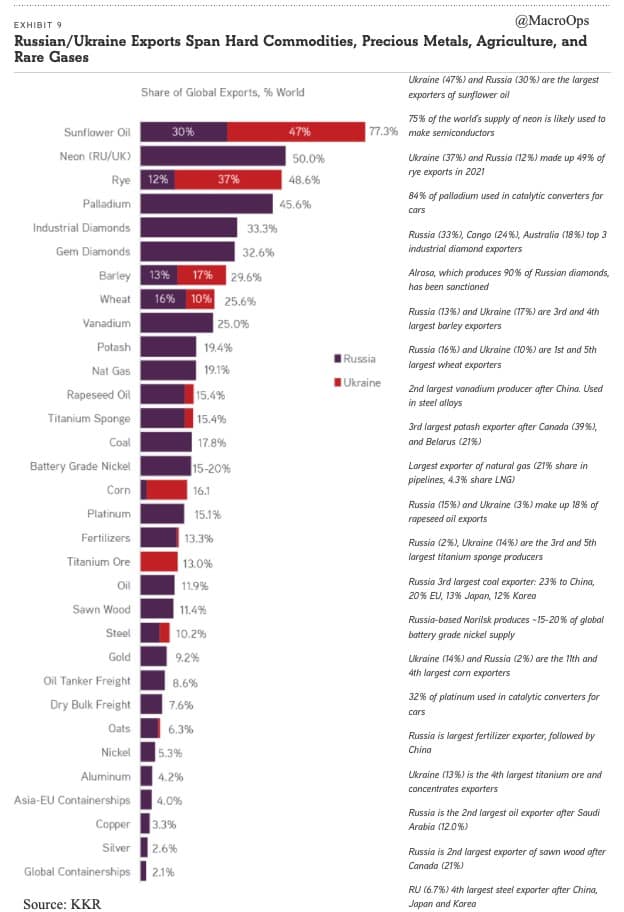

- Russia/Ukraine Commodity exports as a % of world total via KKR.

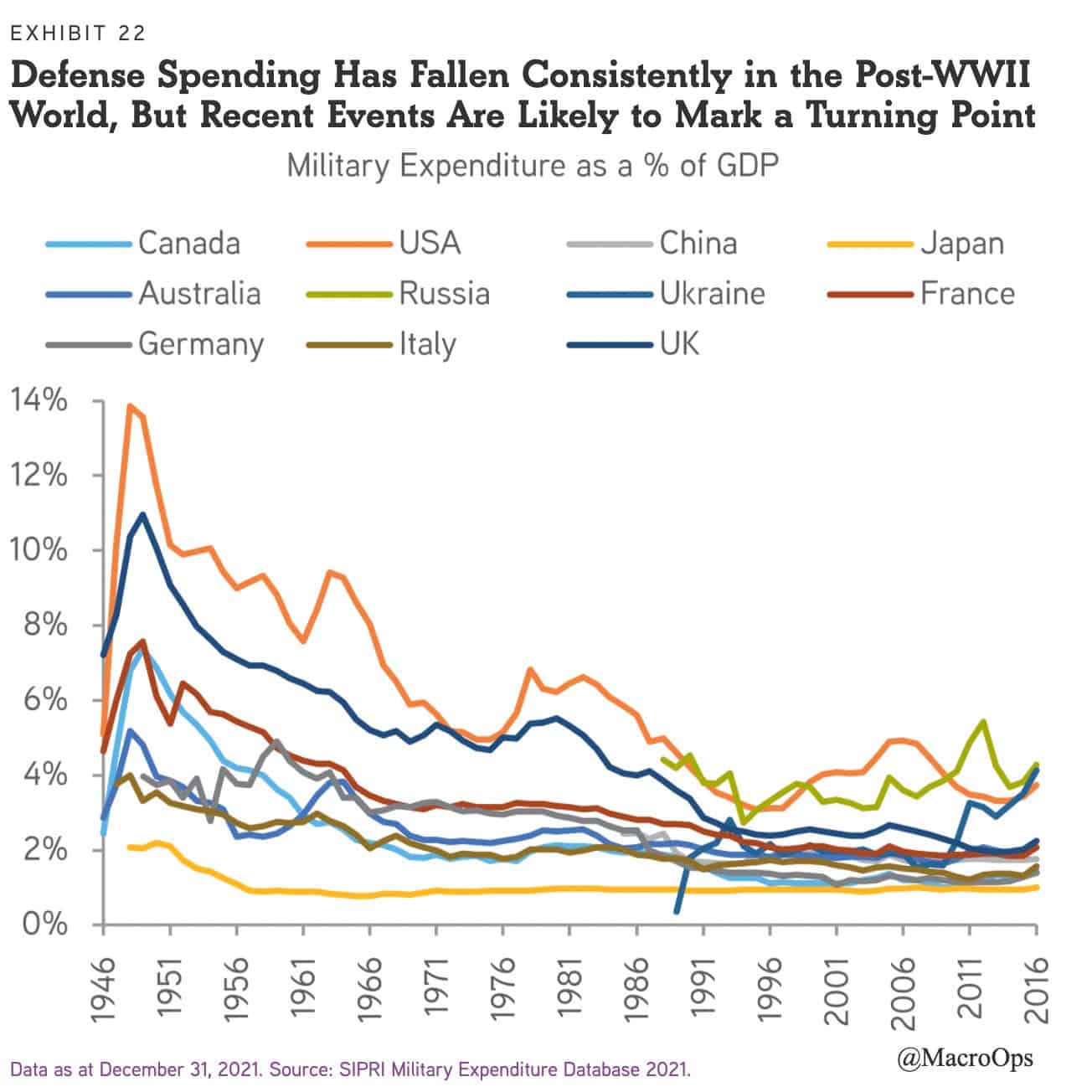

- Sadly, it’s probably a pretty good bet that we’re starting a new secular bull in defense spending (chart via KKR).

- Leonardo (LDO:MIL), an Italian-based defense contractor, will be a big beneficiary of this trend. LDO sells into markets across the EU, UK, and the United States. The stock is cheap, has broken out from a major triangle bottom, and has a few fundamental catalysts coming down the pipe to drive improved growth and margins. We’ll be putting out a report to Collective members on the company soon.

- Net-block order flows don’t paint a pretty picture for FB. Note that this gave a solid lead on the selloff.

- Same with AMZN… The whales are dumping their holdings of big tech, passing the shares to future bag holders.

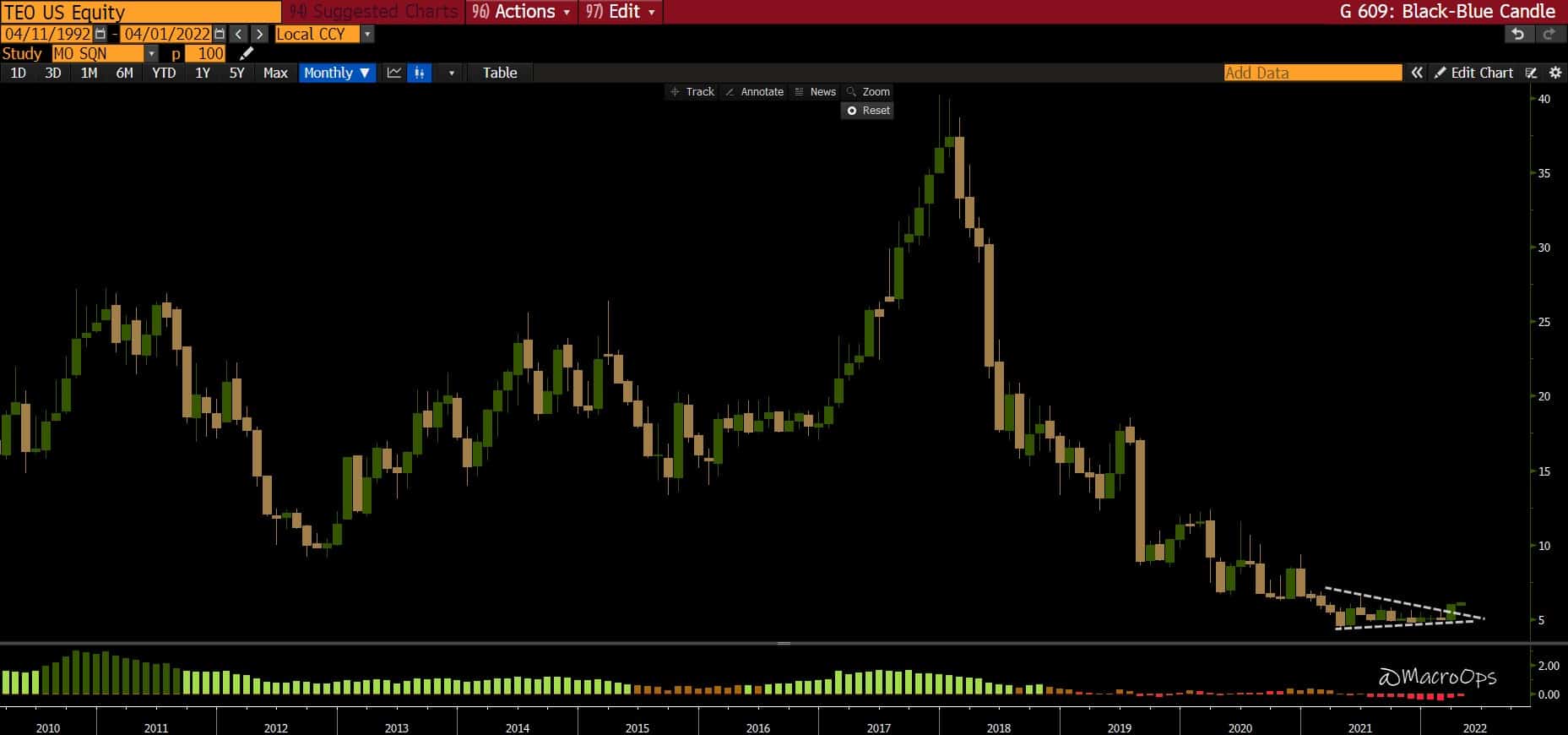

- Here’s another Argentinian stock (last week I shared TGS). This one is TEO, a TelCo play. The chart below is a monthly. I know nothing about the fundamentals. They’re probably garbage. And, again, this is an Argentinian stock so full caveats apply. But… there are some great long-term technical setups in that market and they’re a large exporter of Ags, so *shrugs*…

Thanks for reading.

Stay frosty and keep your head on a swivel.