This is part 1 of our 4-part series on the global deleveraging which is now beginning and is expected to last over the next 2 to 4 years. We anticipate a lot of pain for the global economy in the form of crashing security markets and depression-like economic conditions. This series will cover how we believe this crisis is likely to play out. We will not only help you understand what’s going on, but we will show you how to protect yourself from the coming economic turmoil. We’ll even show you how you can profit from it. Enjoy part 1 below: China’s Renminbi Devaluation.

“Declaring war on China’s currency? Ha ha.” That’s the interesting title of a recent article published by the People’s Daily (official newspaper of China’s Communist Party). It serves as a warning to legendary fund manager, George Soros, against shorting the Chinese renminbi. (Side note: China’s currency has two names, the Yuan and Renminbi, they are interchangeable.)

The piece comes in response to comments Soros made on his bet against “asian currencies”. While speaking at the World Economic Forum in Davos, he discussed his expectations of a “hard landing” in China.

The People’s Daily article went as far as declaring that “Soros’ war on the renminbi and the Hong Kong dollar cannot possibly succeed – about this there can be no doubt.” Some pretty strong words from the Chinese ruling party.

So why the harsh reaction? Why would the largest country by GDP care about the passing remarks of a retired fund manager?

Either state media is petty and has a lot of time on its hands, or it’s a reflection of just how scared the Chinese government is of losing control of its currency… a la 97’ asian crisis style where multiple currency values were cut by 60%.

The evidence suggests it’s the latter. And as we’ve been saying for a while, a renminbi devaluation is not only likely… it’s inevitable. This is the single most important macro risk to markets around the world. Our team at Macro Ops considers it the first of four horsemen in the coming global deleveraging apocalypse. Let’s talk about why and how you can profit from it.

Why Renminbi Strength Is A Big Problem

China’s growth story over the last 20 years has been astonishing. It has lifted millions out of poverty, shifted the centers of global trade and power eastward, and built mega-cities and infrastructure at a scale and speed almost unimaginable. (Fun Fact: From 2011-2014, China used more concrete than the US used in the entire 20th century.)

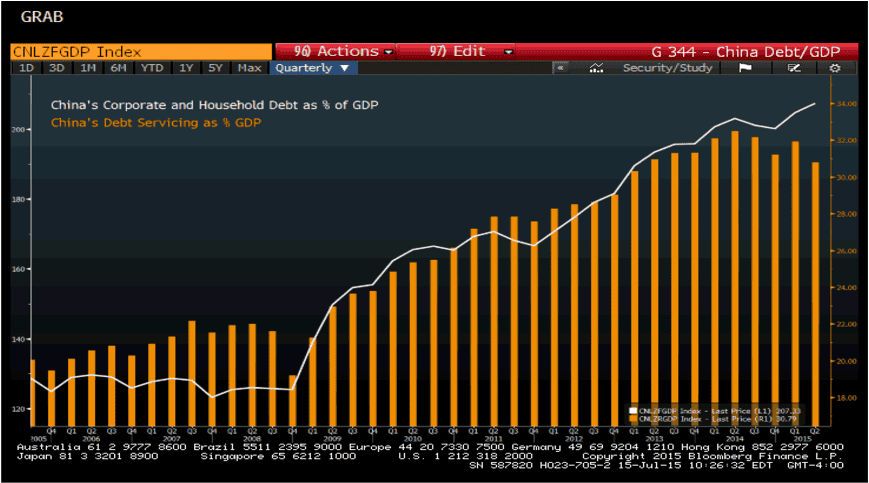

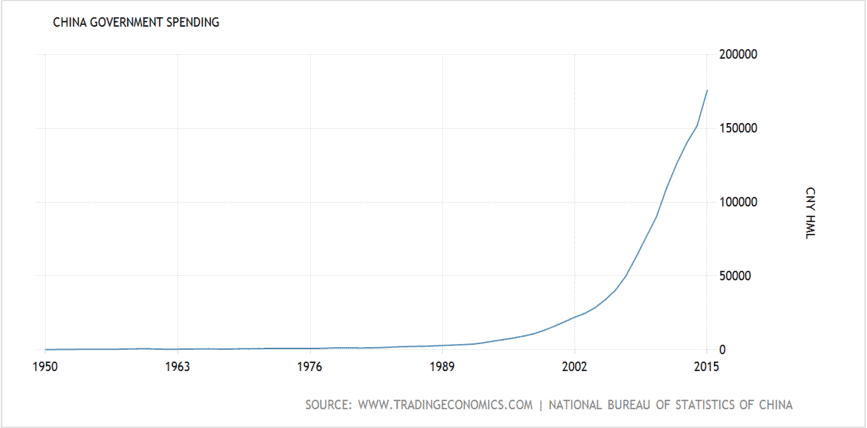

And all of this was done on the back of perhaps the largest credit-induced bubble and most egregious example of capital misallocation….ever.

The two charts below give an idea of the amount of debt spending.

It’s easy to have explosive growth when your non-government debt doubles as a percentage of GDP in just 10 years. Not to mention government spending going parabolic too.

But as it always happens, debt spending reaches a maximum saturation point. The time of reckoning eventually comes. And that time has come for China in the form of a deflationary deleveraging, which is why they’re worried.

A quick aside on deleveragings: A deleveraging is the opposite of a leveraging. A leveraging is just the increasing of debt, which increases demand by pulling future consumption forward. A deleveraging is the reverse. It’s the reduction of debt which results in falling demand. The falling demand causes prices to drop, which is deflationary. Large deflationary deleveragings are painful because they generally occur when a maximum debt limit has been reached. The falling demand and lower prices lead to less income for people to service their built up debt. At the same time, the real value of that debt grows relative to the price of other things. This makes deflationary deleveragings the most painful of economic environments.

The Chinese government’s number one focus is social stability. Maintaining the peace and appeasing the public keeps the Party in power. They’ve accomplished this so far through rapid growth and rising living standards. But a large deleveraging threatens to upend this arrangement and puts the party at risk — a fact the government is very aware of.

Which brings us back to the renminbi.

Since the mid 90’s, the renminbi has been on a steady path of appreciation. It has been set on a crawling peg against the dollar that’s been tightly managed by the People’s Bank of China (PBoC).

This dependable appreciation, coupled with the government’s loose fiscal policy and habit of perpetually rolling over bad loans for state enterprises (SEOs), has created a generation of businessmen, analysts, and policymakers who don’t understand credit and currency risk. They essentially fail to grasp the other side of capitalism.

On top of that, there’s two decades worth of financial products and business models built on the belief that the renminbi always rises over time. This idea has been instrumental in guiding capital structures and lending terms for Chinese corporates.

These realities are just additional tinder for the soon to be currency fire.

The pyre on which it sits is China’s unavoidable debt deleveraging and the US dollars hulk-like strength.

The US dollar has appreciated 25% over the last 18 months. And the renminbi, which was pegged to the dollar, appreciated right alongside it.

But now this currency strength has become a problem for China because of its reliance on exports.

China’s competitors; Japan, Europe, Korea, and Thailand, have been actively devaluing their currencies for over a year. Many of these currencies are down 20 – 30% against the dollar, all while the renminbi has appreciated with the greenback. This has put China at a huge competitive disadvantage in terms of exports. With a stronger currency, their exports become more expensive, and therefore less attractive in relation to their neighbors.

China was able to shoulder a stronger currency in the past because of their strong growth. But now that they’ve started deleveraging, this currency drag has become too costly.

China Will “Choose” An Uncontrolled Devaluation

China’s official GDP growth rate last year was 6.9%. However, those familiar with China know these “official” numbers are about as reliable as a politician’s promises. Xu Dianqing, an economics professor in Beijing, was recently cited in a WSJ article saying that the GDP is likely “between 4.3% and 5.2%”. Other experts suggest it’s even lower. This is clearly a big decline from the heady days of double-digit growth.

A stronger currency has come at the worst time imaginable. China is now stuck between a rock and a hard place. They only have two choices. And both of them are bad.

The first choice is to try and continue defending their currency, keeping it artificially strong. This would involve selling their FX reserves (USD) to buy renminbi, creating demand for the native currency and raising its value. If this route is taken, the already crippling deflationary deleveraging will be exacerbated. Real debt levels will stay elevated and exports will continue to flounder. This will cause the economy to slowly grind to a halt.

The other option to is drastically weaken the currency. Or in other words, allow a large devaluation that risks hyperinflation. China can weaken its currency to not only increase exports, but also make debt less expensive to pay off. But this comes at the cost of destroying both the value of renminbi and the world’s confidence in the Chinese economy.

China claims they won’t choose to devalue. But here’s the key. Throughout history, governments choose inflation over deflation… every… single… time.

The reason being that inflation is simply more appealing politically. Deflationary deleveragings are extremely destabilizing. They make existing debt far more expensive and suck liquidity out of the system. It’s not something you want when you’re leveraged up to your eyeballs.

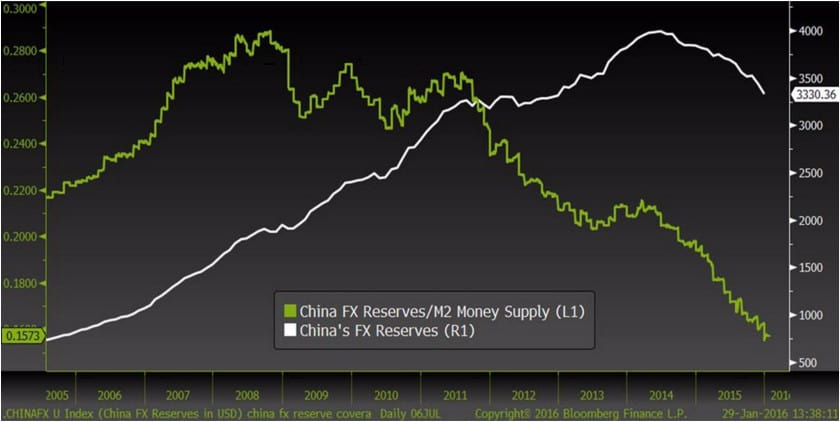

Many have argued that China is capable of doing a “managed” devaluation of the renminbi. They cite the country’s large FX reserves which stand at $3.3 trillion (the largest in the world). Supporters believe China can use this war chest to depreciate the currency gradually over time to a level they want.

But there’s a few problems with this argument. One, it gives too much credit to China’s leadership. Remember, these are the same people who got China into this debtor’s prison in the first place. And two, it makes the mistake of being “wowed” by the large number of FX reserves (in absolute terms). It fails to view the amount on a relative basis — which is what matters.

Yes $3.3 trillion is a lot of money, but China is also a very large country. And when you compare China’s FX reserves to its M2 money supply, you find it’s only worth about 15% of the total amount of cash in the economy — which is a mere pittance.

The M2 money supply can be thought of as an economy’s sum total of cash and highly liquid assets that can be quickly converted to cash. With Chinese foreign reserves only being equivalent to 15% of that total money supply, there’s clearly a much bigger pool of renminbi that can be converted into other currencies than there is foreign reserves to be used to buy up and “defend” the currency. Simple supply and demand dynamics are not in the Chinese government’s favor.

To put the FX/M2 amount into perspective, during the 97’ asian financial crisis, most of the asian tigers had ratios of 20-25%. This was higher than China’s, yet still wasn’t enough to protect their currencies. China is not nearly as capable of fighting off a run on its currency as is generally thought.

Another important point is the makeup of China’s FX holdings. The truth is that China can only readily deploy about a third of its FX reserves, or $1 trillion. The large majority of its holdings are in illiquid assets that would be difficult to convert to dollars quickly enough to fight runaway capital flight.

Finally, many mention China’s ability to lock down its financial borders to prevent currency from leaving the country. Again, this is giving too much credit to the omnipotence of the ruling party. It fails to hold up to the evidence.

It’s still all too easy for capital to find ways out of China. Corporates can simply buy USD assets or commodities or even record fictitious exchanges in order to convert their renminbi. And the public can buy bitcoins and do web transfers or many other things to move money out. The PBoC spent over $1 trillion last year fighting this capital flight, and $100 billion just this last month alone. And all this spending is before the real party even gets started…

Just wait until the public realizes that the government can’t and won’t attempt to defend the currency anymore. Then we’ll see real capital flight.

Chinese savers have been significantly over-invested in China. Especially in comparison to savers in other emerging markets. They’ve kept the majority of their savings in their homeland because for the last 20 years, it has been the safest place to be.

Well, that is all about to change, and this crude awakening to Chinese savers will cause a stampede for the exits.

A similar scenario, though brief, happened in 2008 at the height of the financial crisis. There was record capital flight out of China and there was little the government could do to stop it.

These reasons make it clear that China won’t be able to control the devaluation of their currency. Either they will try and fail, or realize the futility of trying and give up. Inevitably, there will be a quick and massive move in the value of the renminbi as market forces find a new equilibrium.

China’s Posturing Is Just Political Cover

Last December, China announced it would start tracking the value of the renminbi against a basket of currencies, instead of just against the dollar. They didn’t release the makeup of this currency basket, but we can assure you it will be heavily weighted to their trading competitors.

This move, along with the government’s posturing on their intentions to avoid an active devaluation, serve as political cover more than anything else.

China knows they can’t prevent a devaluation. But they also know that a devaluation will be met with international political backlash and accusations of currency manipulation. So all the “aggressive” talk from the Chinese party against renminbi “short-sellers” and the changing of the currency basket is really just political cover for the coming devaluation.

Governments around the world have accused China of manipulating its currency. Multiple times they’ve called for China to liberalize exchange rates to let the market decide. This of course was said with the belief that markets would strengthen the renminbi. So it’s ironic that now when China is likely to finally let it go, it will have the exact opposite effect.

The best thing for China to do, and what we think they will do, is to completely stop defending the currency and let market forces quickly devalue it. This is the least worst option. It allows them to devalue from a position of strength, where they can maintain a sizable FX reserves buffer. The buffer will allow them to provide a liquidity boost to markets in the form of increased export attractiveness and debt reduction. This will help temper an otherwise violent devaluation.

The longer they attempt to defend the inevitable depreciation of the renminbi, the more FX reserves they blow through and the further they weaken their position. Doing so also maintains the economically destructive strong currency anchor on their nominal growth.

What Does This Mean For Markets?

The average devaluation amongst the Asian Tigers during the currency crisis in 97’ was 60%. And we believe that a similar devaluation for the renminbi is certainly possible, with a 40-50% depreciation against the dollar most likely.

This is very important to US investors. When a country the size of China devalues its currency by half, it essentially exports its deflation to the rest of the world. By making its products cheaper and more competitive through devaluation, other countries will be forced to follow suit, greatly exacerbating the budding currency war in the global race to the bottom.

The deflationary pressures drive prices lower, which lead to lower incomes and therefore less demand. This again causes further devaluation to try and spur demand to fix the problem. You eventually end up with a deflationary feedback loop that has many other ugly second and third order effects. This happens until the level of devaluation, which is inflationary, is enough to counter the deflationary pressures of the debt. It essentially works by monetizing away existing debt.

The US dollar is going to go through the roof. As bad as things are in the US, we’re still the world’s cleanest dirty shirt. And investors around the world, fleeing their evaporating home currencies, will pile into US dollars and USD equivalents.

Commodities, which have already suffered massively over the last year… will get destroyed by the stronger dollar. And as a result, commodity producing countries who are already in a world of hurt, will reach new lows.

In a world awash in debt, with central bank monetary ammunition completely spent, the coming deflationary storm will be devastating.

US markets, which are historically overvalued and appear to be entering a cyclical bear due to a turning business cycle, are going to be crushed. And so will markets around the rest of the developed world.

As you can see, this reasoning is why Macro Ops believes that China’s renminbi devaluation is the first of “Four Horsemen” signaling the deleveraging apocalypse.

But enough doom and gloom. We’re not fear peddlers. We’re simply interpreters of information whom make probability weighted assumptions. And right now, this is the most likely scenario as we see it.

The world economy has been here before and will be here again. And though we expect a lot of short term pain over the next 2-4 years, things will eventually rebound and the world will continue to spin.

Besides, the volatility caused by an event like this provides the savvy investor with an amazing opportunity to make a killing.

Here’s How To Profit From This

The biggest trades over the next year will be long safety and short risk.

Investors who are long equities should make sure to stay tactical and closely manage their risk. It would be wise to hedge their downside with index options.

We like long dated US treasuries. Long bonds are going to considerably outperform the market over the next twelve months. This is something we’ve written about extensively. As much as people love to hate it, US debt is still the safest and most liquid asset in the world. And long bonds do well in deflationary environments as well as in times of volatility — both of which we will have very soon.

Another kicker to the long bonds trade is the China situation. China is the second largest holder of US debt. And once they stop defending their currency, a lot of selling pressure on USTs will disappear. This will happen at the exact same time that investors around the world flood into these bonds looking for safety. We are very bullish on US treasuries.

We’re also short commodities. We don’t believe the downtrend is anywhere near finished. The biggest driver here is dollar strength. Oil won’t bottom until there’s absolute destruction in the exploration and production (E&P) space and a complete capitulation in price. Our target range for a bottom in oil is around $16/bbl. Copper is also on our radar to the short side.

In general, it’ll be smart to keep a lot of dry powder in the coming months. In bear markets and times of extreme fear, it helps to hold a lot of cash. This is especially true when cash (USD) will be one of the best performing currencies and assets in the months to come. Having reserves will be key once this China situation resolves itself. There will be some unbelievable buying opportunities to be had.

The best opportunities will come in the hardest hit sectors; commodities and some emerging markets. We’re closely watching and licking our chops, knowing that once this theme plays out, these opportunities will have full retirement making potential.

Lastly, investors should stay nimble with an eye on the bigger picture. Bear markets are extremely volatile and full of many sharp retracements. But letting these entice you to the long side is a suckers bet. The largest short-term bull moves happen in declining bear markets. The system is extremely biased to the long side (as it should be) and so you should expect many volatile swings.

It will pay to be cautious going forward. We are entering the largest global deflationary deleveraging ever. And never has the world been more connected than it is now. There are a lot unknowns investors will soon be facing, but we can always do our best to prepare ourselves. Keep your eyes open and your risk management tight.

We hope you enjoyed part 1 of our 4-part series on the coming global deflationary deleveraging. Part 2 has just been released.