Legendary hedge fund manager Stanley Druckenmiller had a lot to say at the recent New York Times Dealbook conference.

When The Druck speaks, you should listen.

One of his more interesting segments involved him proclaiming his love for Amazon. But these aren’t just words, Druck tends to put his money where his mouth is. According to Business Insider, Druckenmiller’s family office Duquesne Capital bought a large amount of Amazon shares during the third quarter. Druckenmiller is bullish on Amazon for 3 reasons – their focus on the long term, their profitable cloud-computing business AWS, and their ability to eventually flip a switch to drastically increase profits.

Focused on the Long Term

The last 19 quarters, Amazon has missed their quarterly earnings nine times. They don’t give a damn. – Druckenmiller

Druckenmiller loves the fact that Amazon doesn’t care about short term quarterly earnings. He understands that their focus on the long term is why their stock price is as high as it is and will continue to climb.

He highlights Amazon’s strategy by juxtaposing it against IBM. According to Druck, IBM is the poster child for bad corporate growth.

He describes how IBM’s sales continue to decline year after year. This occurs as they reduce their research and development spending as a percentage of those sales. These actions serve as a double whammy to their R&D department. IBM’s absolute percentage of spending decreases as does the total sales number the spending is based on.

Amazon has done the opposite. They’ve increased their R&D spending from 5 to 10% on increasing sales. There is clearly a large divergence between the two companies’ business strategies. And this difference is obvious in the two company’s stock prices.

Druckenmiller also compared Amazon to another company he admires – Netflix. As he explained in the interview:

I only heard 30 seconds of [Netflix CEO Reed Hastings] … but he said, ‘If you manage for quarterly earnings, you’re dead.’ Then somebody on CNBC says, ‘Well, it’s easy for him to say with a stock price like that.’ Well, why do you think he has a stock price like that? Because he thought about the long term and not cared about quarterly earnings and all this short-termism the whole time.

We agree with Druckenmiller’s assessment of Amazon. We have begun to see a “winner take all” mentality develop in the tech space. Investors are searching for the last few areas of growth in a fundamentally deteriorating market. Our views are echoed by Scott Kupor, managing partner at venture-capital firm Andreessen Horowitz. He believes “…there is a huge premium [given to] large-cap player[s] [that] can actually show growth. There’s just a scarcity of opportunities”.

These scarce opportunities are especially prevalent in companies leading the cloud computing revolution like Amazon. Amazon’s focus on the long term has allowed it to establish a wide moat in this space. They stand to profit for years to come as the cloud industry continues to grow. Investors are eager to pile their funds into the growth opportunity Amazon offers.

Amazon Web Services (AWS)

[Bezos has] come up with this AWS, which is absolutely exploding … If you’re starting a business today, you don’t need a tech department, you don’t need a back office, you can use AWS. By the way, it’s just ripping to shreds the 10 or 15 consultants from IBM … that you used to need, but you don’t need because now you go into cloud. – Druckenmiller

Druckenmiller is a big fan Amazon Web Services (AWS), Amazon’s profitable cloud computing business. He views it as the number one growth engine for the company.

And it’s not just Druckenmiller. Cloud computing looks to be the main tech driver that most investors view nowadays. Marc Benioff, chief executive of Salesforce.com Inc, believes that cloud computing “is the biggest revolution in computing that we’ve seen in decades”. He thinks “we’ve hit the psychological tipping point”. This seems likely as investors now frequently laser in on cloud computing metrics.

AWS has become a multi-billion dollar business with an annual growth rate of 78%. Investors go wild seeing growth metrics like this. They have no problem plowing their money into Amazon’s stock.

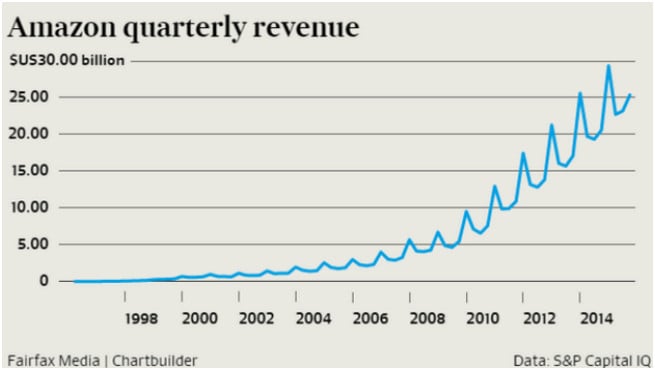

Amazon achieved this growth rate by spending billions in developing their cloud services. This investment enabled them to dominate the growing industry. The reason they could invest so much is because of the success of their other businesses. The cash-flows these businesses produced created the funds necessary to invest. They allowed Amazon to build a large advantage in the cloud area that became difficult to match. As seen in the revenue graph below, Amazon has had no shortage of firepower to plow back into their R&D.

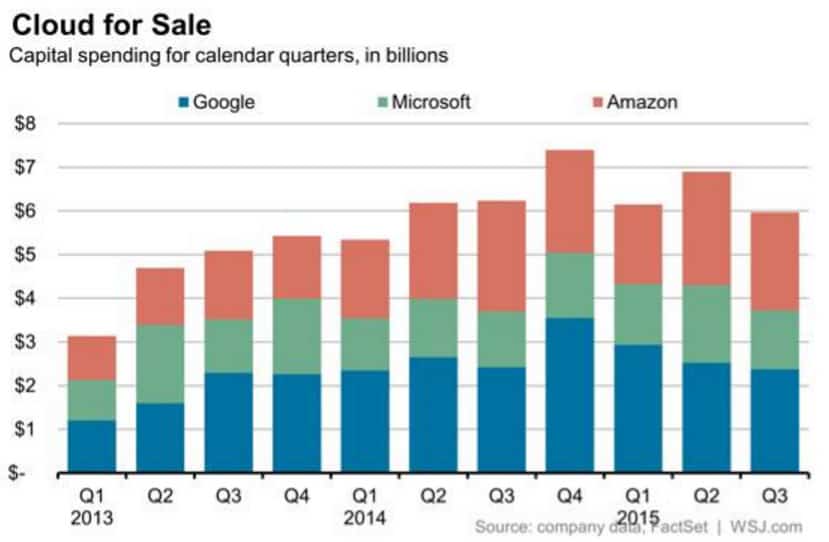

A large chunk of that revenue has gone specifically into developing their web services as seen in the chart below.

Amazon has continued to reinvest into AWS, while taking advantage of economies of scale. This has helped reduce prices for their customers and help spur growth.

Not only that, but Amazon is always collecting massive amounts of data from their customers. This data gets used to constantly customize and improve their services. The years of personal data Amazon has been able to gather have given them another huge advantage. Other companies once again cannot compete. Amazon’s moat in this industry will continue to grow. They are building a strong foundation to profit off the ongoing explosion in cloud computing.

Flipping the Switch

[Bezos is] just sitting there with narrow margins and when he has enough share of market… whenever he wants he can cut those margins up. – Druckenmiller

Druckenmiller subscribes to the common “switch” theory regarding Amazon. He, like other investors, believe that Amazon can just flip a switch to turn a profit. This “switch” is their margins. Once they increase them, investors believe Amazon will become extremely profitable.

The interviewer asked Druckenmiller if he believed Bezos would ever actually flip the switch. Druckenmiller was astonished at the fact this question was even asked.

Druckenmiller believes Bezos is a businessman before anything else. He thinks Bezos’ total dominance strategy is only in place to one day reap enormous profits. He replied:

…I see his strategy and I think it’s genius.

Druckenmiller explained how Amazon is 22% of US retail sales growth this year. That amount of growth from one company is quite amazing. The total dominance strategy seems to be working well.

We agree with Druckenmiller’s view here once again. As we have explained, Amazon is focused on the long term. They are building a giant moat and are looking for total dominance. This position they are putting themselves in will one day enable them to “flip the switch”.

Prominent venture capital Fred Wilson agrees with us. In a recent blog post, Wilson discusses his theory that “software is the new oil”.

He explains that during the industrial revolution, oil producers were able to just sit back and collect profits. These massive profits lead to their extreme wealth and power. Oil was the lifeblood of the industrial age. It powered the factories, railroads, and everything else. Oil producers greatly benefited from the “economic surplus” that resulted from the revolution. It provided the golden opportunity in the oil game.

In the same sense, Wilson believes that software is the “oil” of the current information revolution. Companies like Amazon that have invested billions into the infrastructure needed for the information revolution will be able to sit back and collect profits just like the oil barons of the the 20th century. This will again lead to great wealth and power.

This relates to Amazon’s infrastructural cloud computing moat. Nearly every business, old and new, will use the cloud in the future. Amazon is making itself the number one platform for this. They are solidifying their advantage against competitors and looking to profit immensely.

Wilson also discusses how the capex spending required to put this infrastructure in place has shielded a lot of cash-flows. He believes this may continue, but that we are growing closer a point where cash-flows will overtake capex. Investors will soon see massive profits.

Druckenmiller is clearly long Amazon for many good reasons. You should be too. We believe Amazon’s stock price has a lot more room to go. It’s a great long term investment.