“In the long run, painful losses may prove much more valuable than wins — those who are armed with a healthy attitude and are able to draw wisdom from every experience, ‘good’ or ‘bad’, are the ones who make it down the road. They are also the ones who are happier along the way. Of course the real challenge is to stay in range of this long-term perspective when you are under fire and hurting in the middle of the war. This, maybe our biggest hurdle, is at the core of the art of learning..” ~ Josh Waitzkin, “The Art of Learning”

In this week’s Dirty Dozen [CHART PACK] we look at short-term divergences, positioning updates, consensus inflation calls, positive seasonality in crude, and a potential bottom call on a major Ag name, plus more…

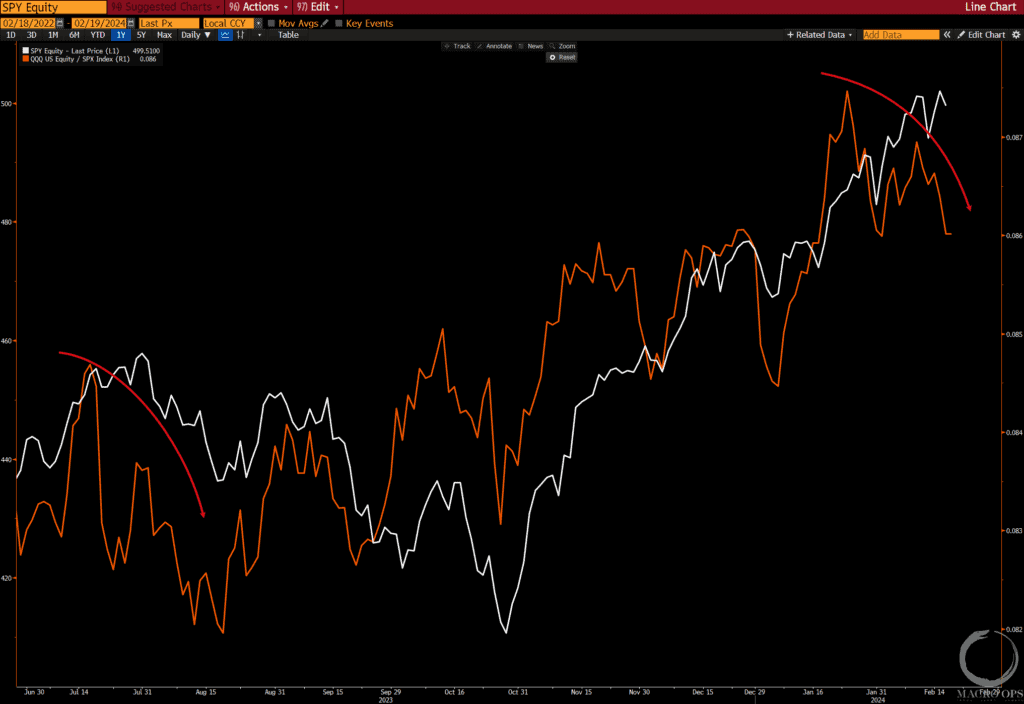

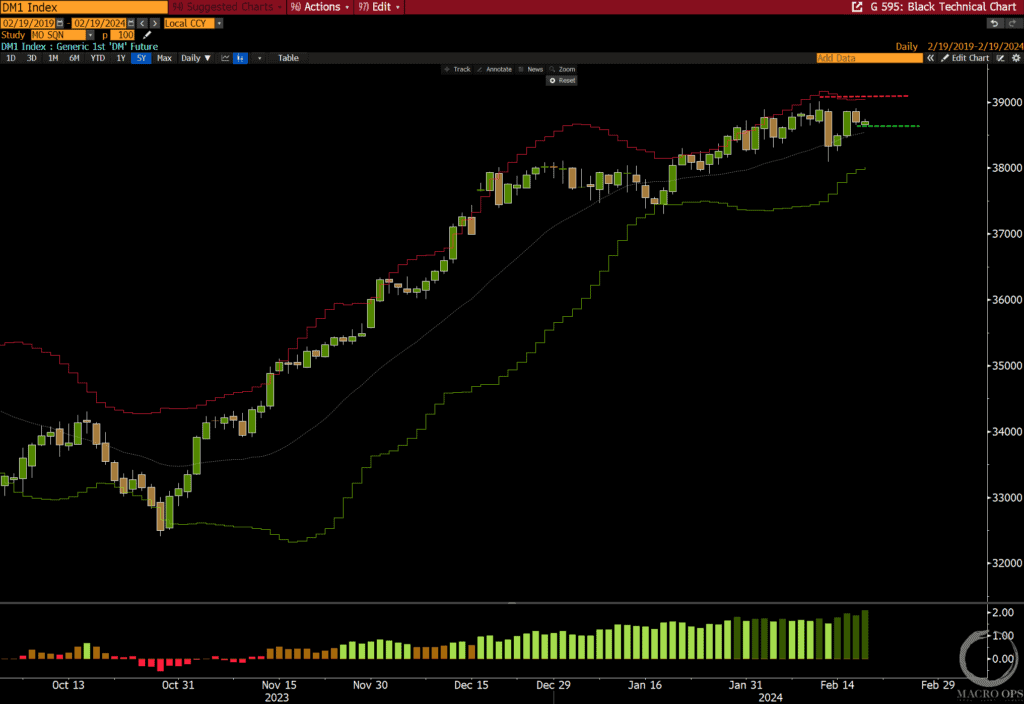

1. Qs vs SPY (orange line) are underperforming and this is worth keeping an eye on as continued divergence will likely point to a period of consolidation/downside retracement.

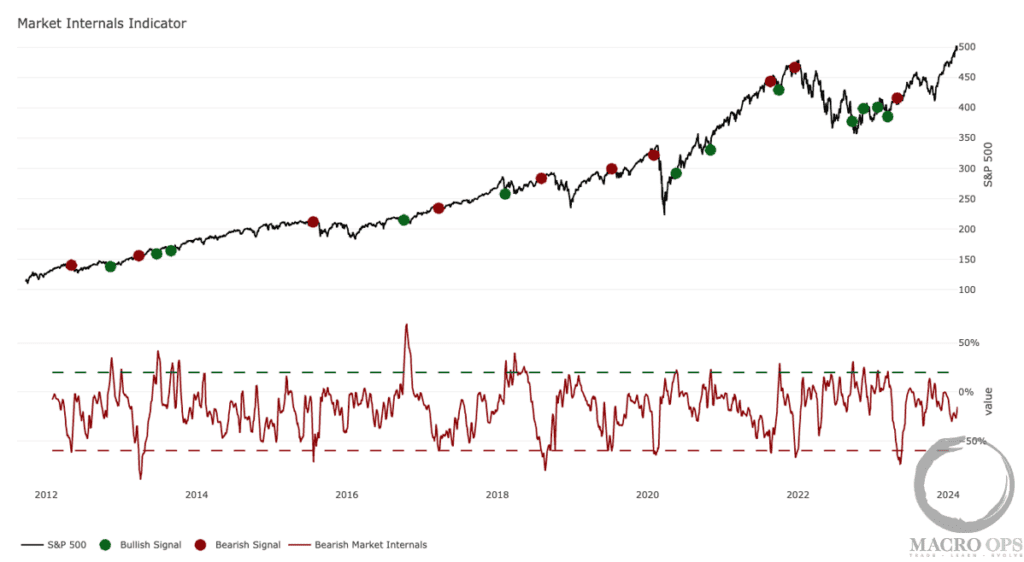

2. But as we’ve been writing for the past couple of months, we’re in a primary bull trend. So any pullback or consolidation should not be met with an overly bearish reaction. Our aggregate market internals indicator shows that overall this trend remains in good health.

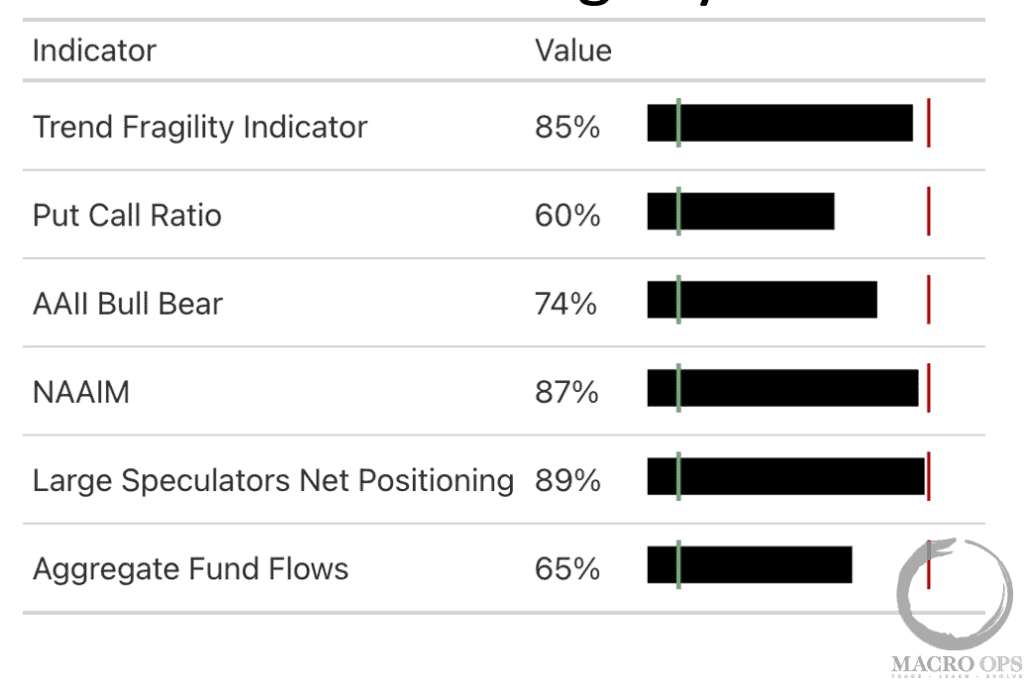

3. It’ll be telling to watch to see how much positioning and sentiment react to an eventual correction. That should give us a good feel for how much juice is left in this larger uptrend.

4. If we were going to short a US index here it’d be the Dow where positioning and sentiment are crowded bullish.

5. And recent highs give one a tight inflection point to place a stop and get some size on for a cheap hedge.

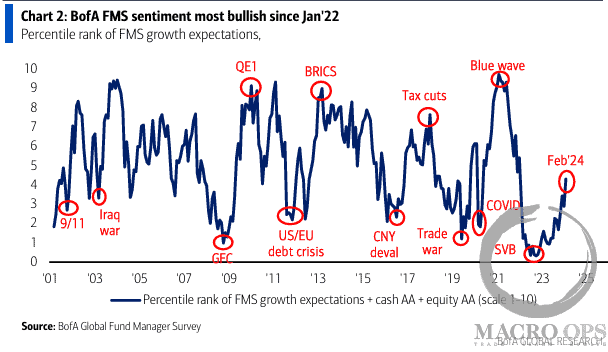

6. The latest percentile rank of global fund manager sentiment shows longer term sentiment and positioning is neutral.

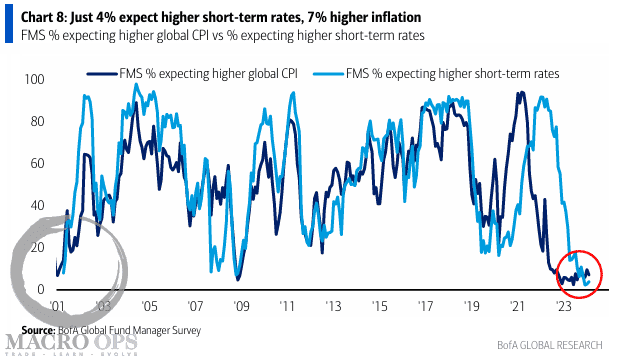

7. Also from that report is this chart showing that only 4% of fund managers expect higher short-term rates, and 7% higher inflation. I don’t currently have strong views on the short-term path of inflation but the confidence in this view seems questionable considering the strong trend US growth and a rebounding RoW.

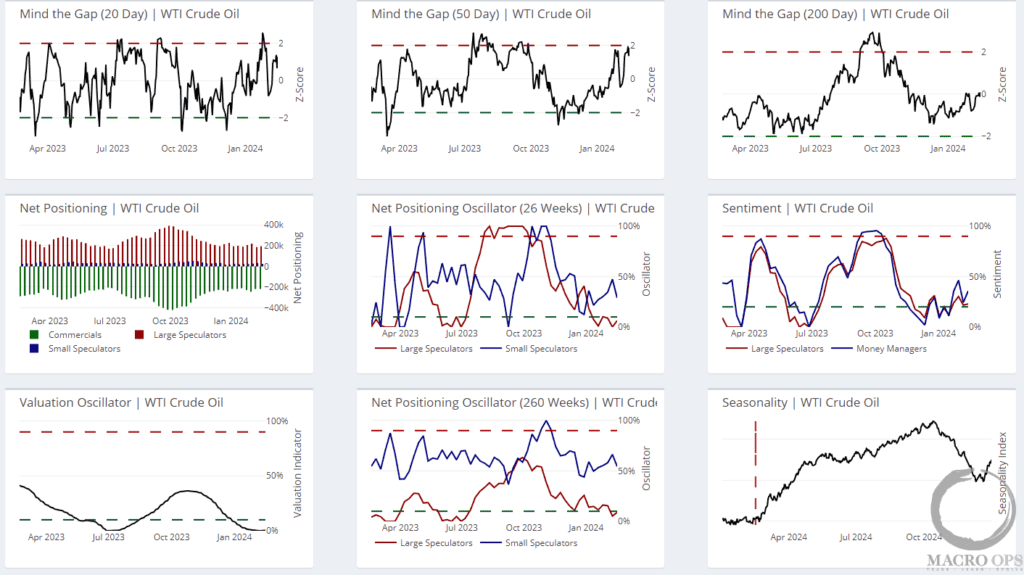

8. Crude kicks off its strongest period of seasonality this week with the additional backdrop of crowded bearish positioning and sentiment.

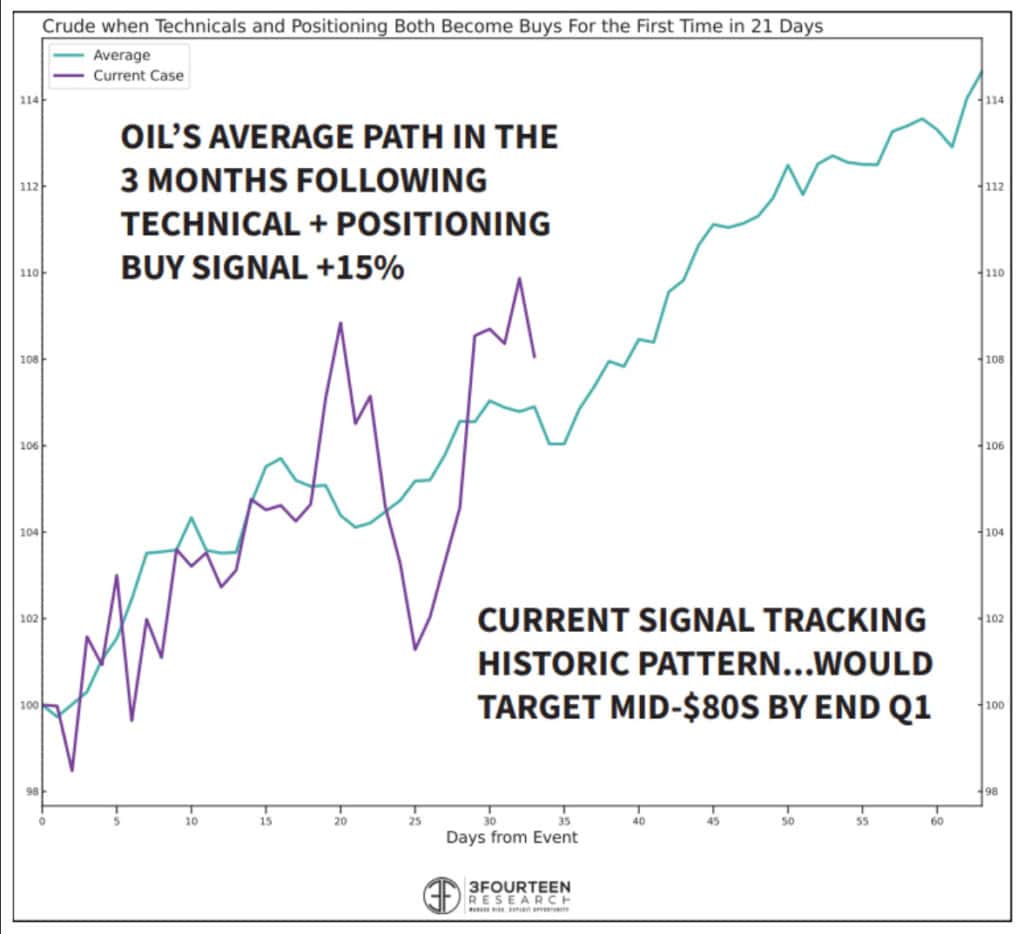

9. This chart from Warren Pies shows that crude is tracking its average path following the recent technical and positioning buy signal. His model gives crude an end-of-quarter price target in the mid $80s.

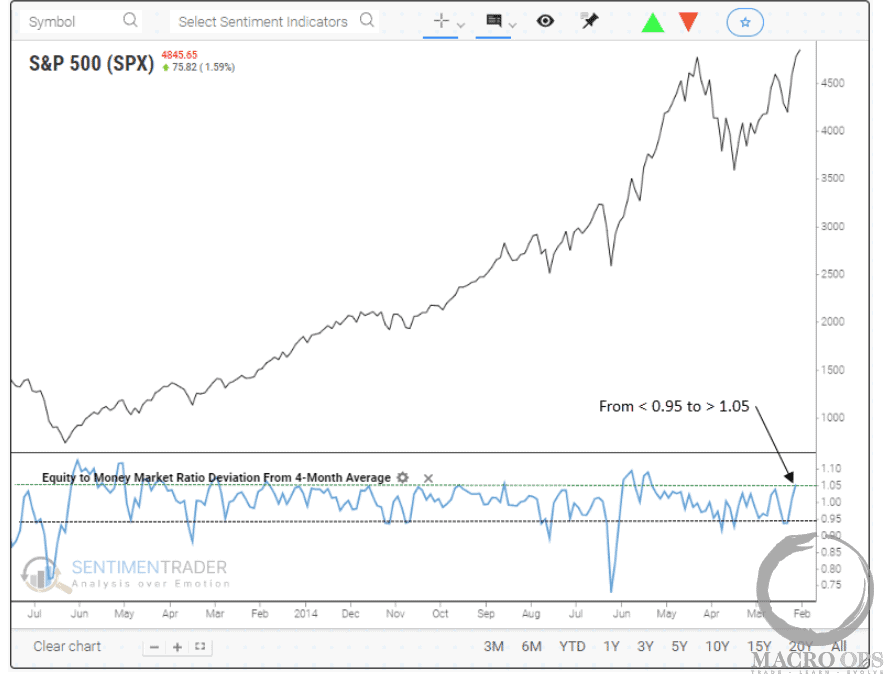

10. We started the year with investors holding a pile of cash in money market funds (roughly $6trn). This chart from SentimenTrader shows how that cash has been making its way back into equities and what that means for the market. They write:

“With the most recent update from the ICI, the equity-to-money market ratio deviation from its 4-month average increased to the highest level since December 2020, triggering a buy signal for a model that measures a shift from below 0.95 to above 1.05.

“Shifts in the equity-to-money market ratio deviation from its 4-month average, like now, tended to occur after corrections and bear markets. In most cases, the Federal Reserve was lowering interest rates, resulting in a less enticing cash option, which is not the case now.

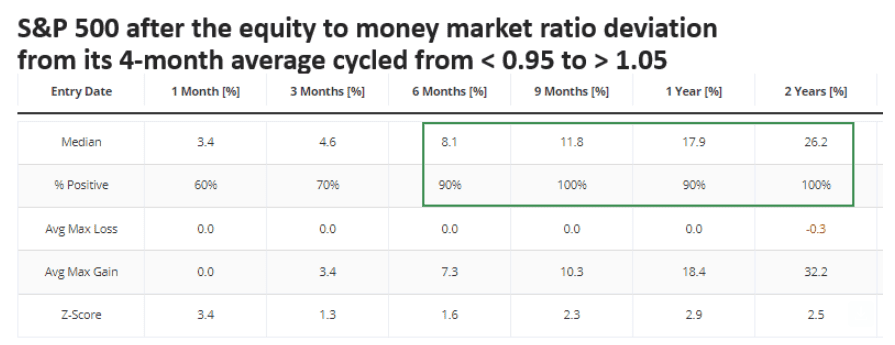

“When the equity to money market ratio deviation from its 4-month moving average cycled from less than 0.95 to greater than 1.05, the S&P 500 was higher 100% of the time over the subsequent nine months.”

11. From Brandon Beylo (Macro Ops Value):

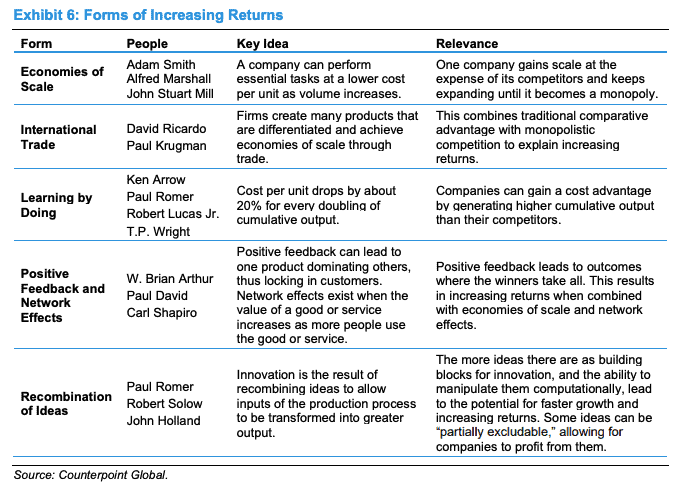

I’m a simple man. Whenever I see a new Michael Mauboussin piece, I stop what I’m doing and read it. Mauboussin’s latest focused on Increasing Returns. The main idea is that there are five “forms” of increasing returns: Economies of Scale, International Trade, Learning by Doing, Positive Feedback/Network Effects, and Recombination of Ideas.

I highly recommend you read the entire paper here.

12. From Brandon Beylo (Macro Ops Value):

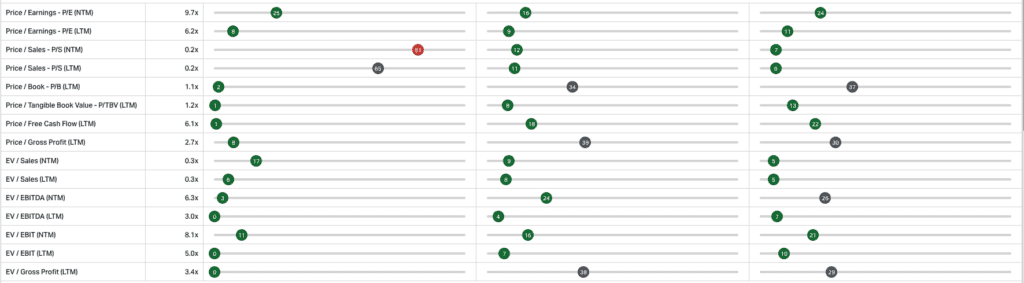

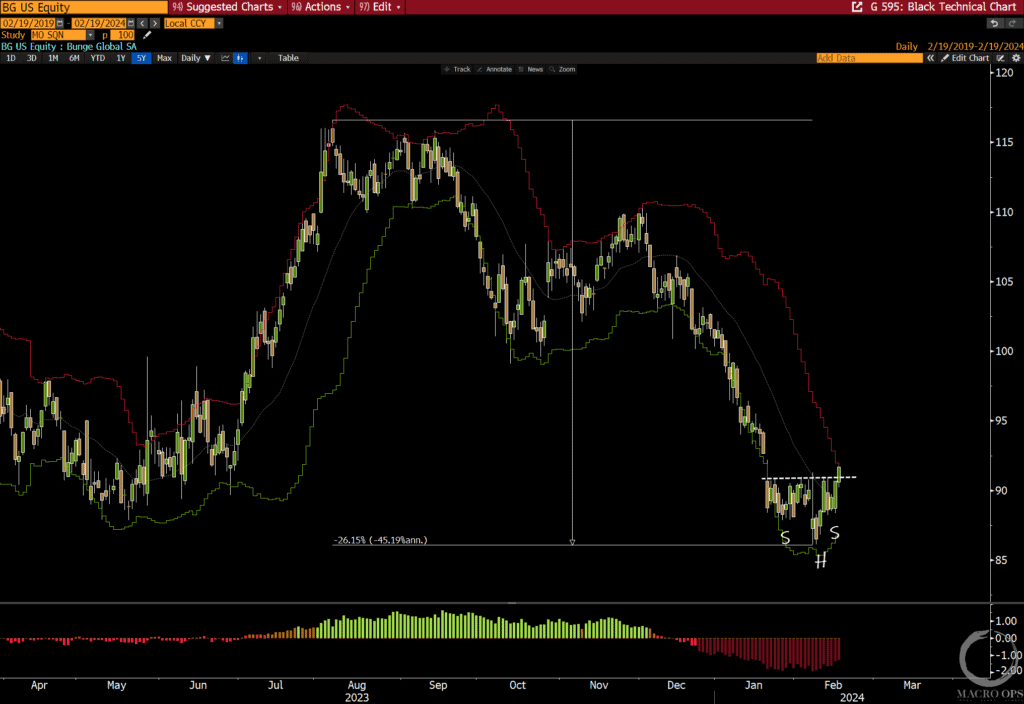

Bunge (BG) is a global agriculture conglomerate. The best way to describe it is that they’re the nervous system of the entire agricultural value chain. Anyways, we’re getting increasingly bullish on agriculture as many of the softs (corn, wheat, soybeans) trade at their lows with massive Large-spec short positions. BG has a global network of irreplaceable agriculture assets yet trades at historically low valuations (see below via Koyfin).

I like the weekly chart as a way to play the bullish agriculture theme. The stock is down ~20% from its recent highs and failed to break below the 200MA on the weekly chart. You can get great size with little actual risk exposure here.

Thanks for reading.