“The price extreme is the definition of the extreme of despair, which is in turn, by definition the moment when hope comes to prevail; hope feeds and is fed by rising prices until the peak of price and euphoria leave prices with only one way to go, which is down. This circular process underlies every price fluctuation in free markets from the smallest one measured in seconds or minutes to the largest measured in years or decades.” ~ The Way of the Dollar

In this week’s Dirty Dozen, we look at very bullish fund managers holding very little cash, cover forecasters boosting their SPX forecasts at record rates, talk about the little concern from the market about last week’s vol, then we get into bonds, pitch a long silver and EURUSD setup, plus more…

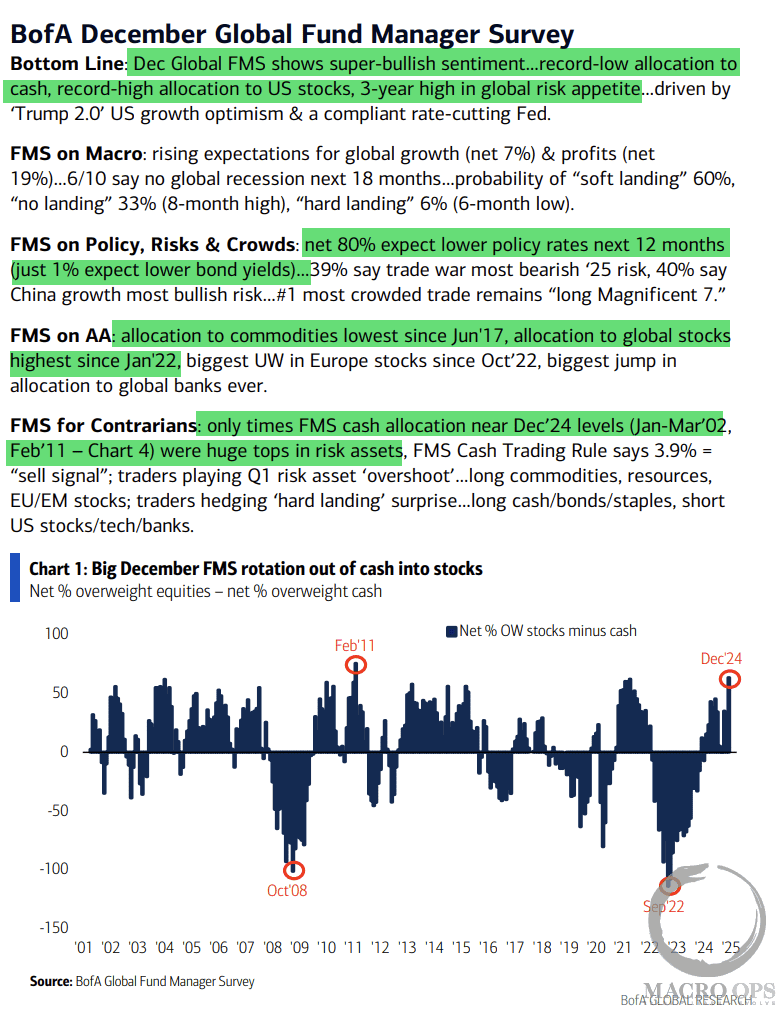

1. BofA’s Dec Global FMS was en fuego… here are the summary highlights.

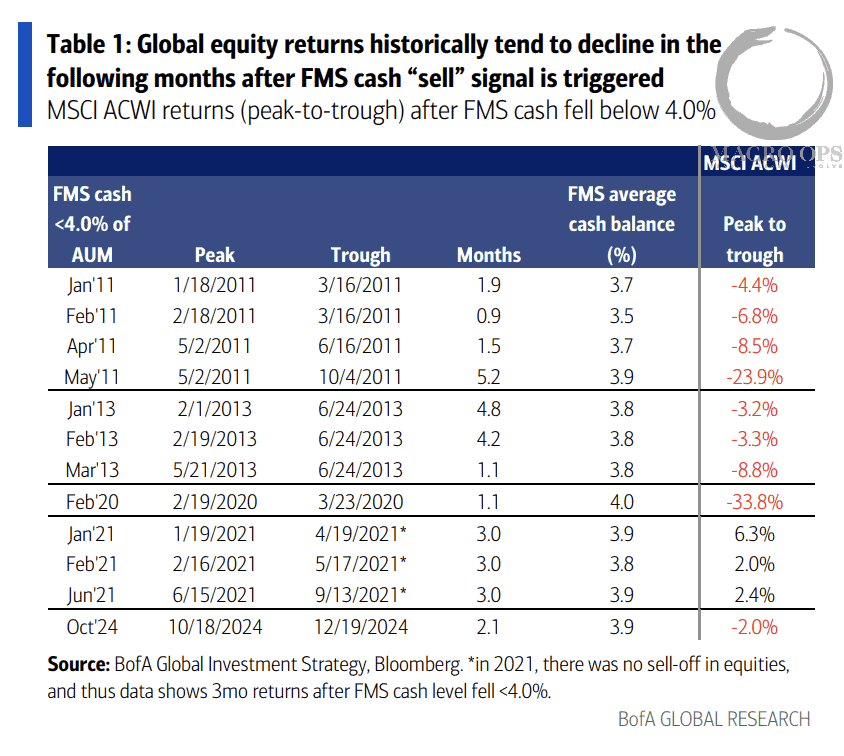

2. And here’s global equity returns following a cash “sell” signal, which historically shows a poor performance for stocks.

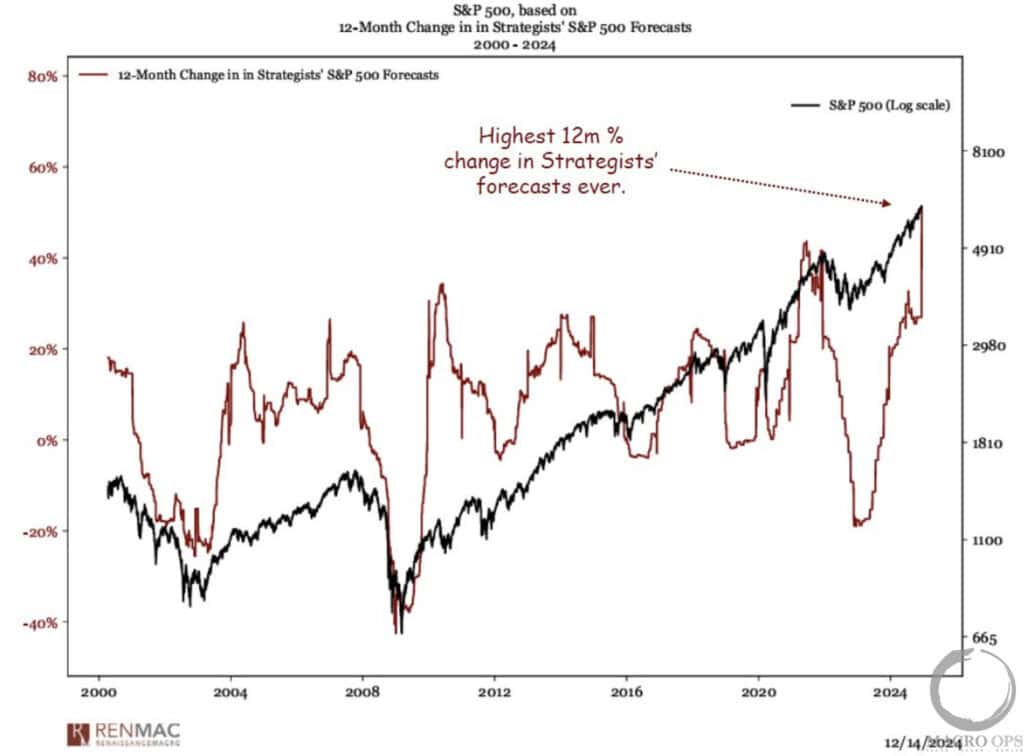

3. Chart and comment via @RenMacLLC: “The embodiment of the ‘wall-of-worry’ is being breached on SPX. Strategists have never chased the market higher – harder with targets than today. If we were country music lyricists, we’d call this song “It might be lonely at the top, but it’s crowded AT mkt tops.”

4. Following a volatile week, I like to check the financial media sites, particularly those popular with the retail crowd, for a sentiment check. MarketWatch is one of my go-tos. Tellingly, we’re not seeing any bearishness on the front page or the most read articles — quite the opposite, actually.

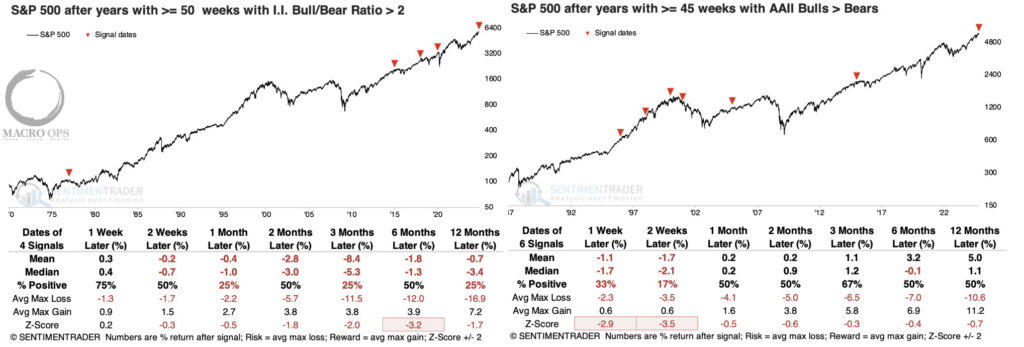

5. This aligns with these two recent studies from SentimenTrader on the consistently bullish readings we’ve seen this year in both the AAII & II surveys. ST writes:

After any year with at least 45 weeks of net bullish sentiment in the AAII survey, the S&P 500 tended to suffer weakness during the first couple of weeks of the new year. The one year that didn’t show weakness ended up giving all its gains back, and then some – it was the peak of the internet bubble.

And

The table below shows every year with at least 50 weeks with twice as many bulls as bears [in the II]. All of them showed losses in the S&P 500 either six or twelve months later. There are a few more precedents if we relax the parameters to 45 weeks of extreme bullishness during a calendar year. Even so, only two (2013 and 2018) enjoyed more reward than risk over the following year.

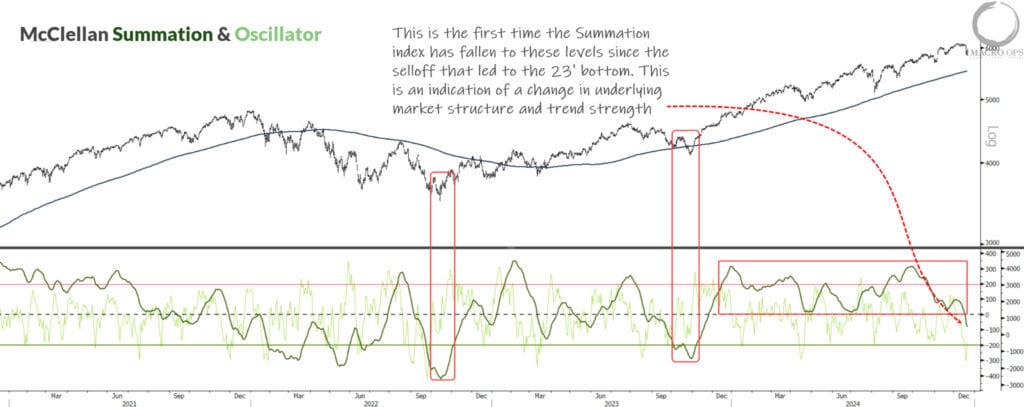

6. Our favorite indicator of breadth, the McClellan indicators, show that the oscillator is oversold, giving a short-term buy signal, while the summation index (dark green line) has broken to a new low for the year. This tells us the underlying market structure and trend strength have changed, and we’ve entered a new regime.

So maybe we see a rip over short term before a larger corrective phase?

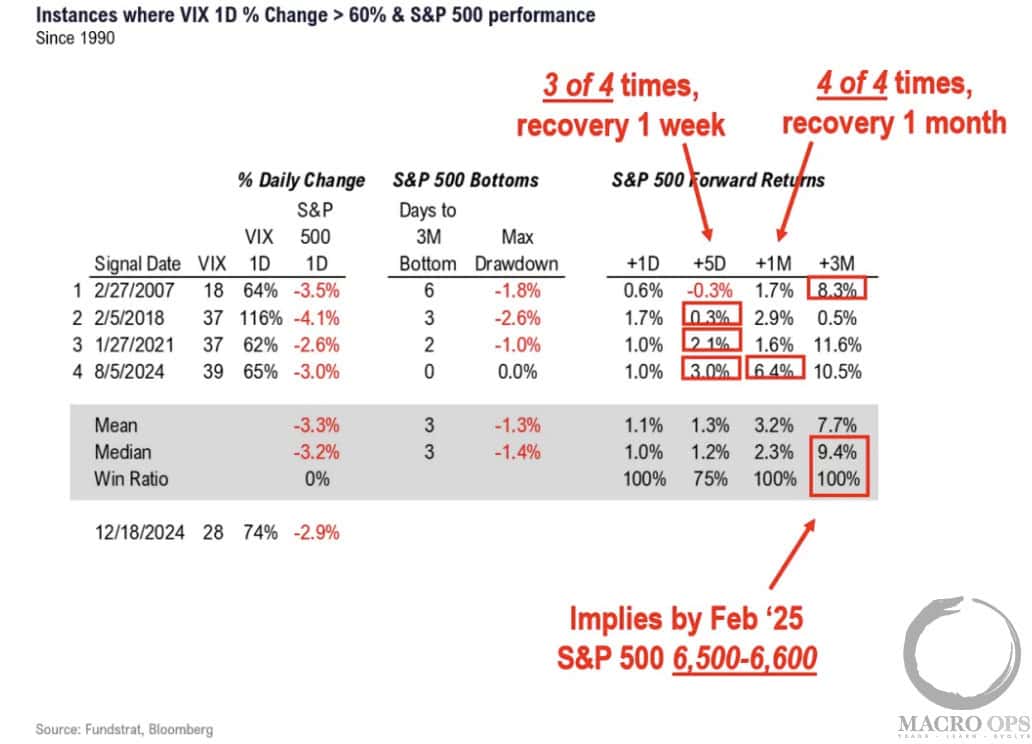

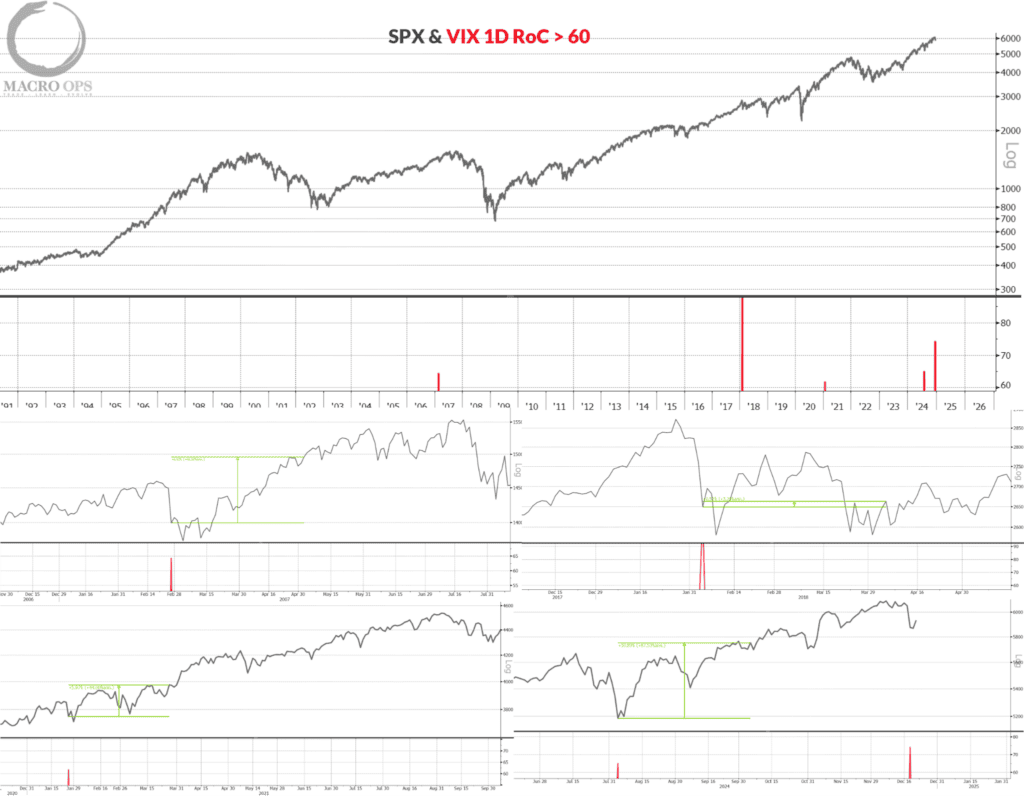

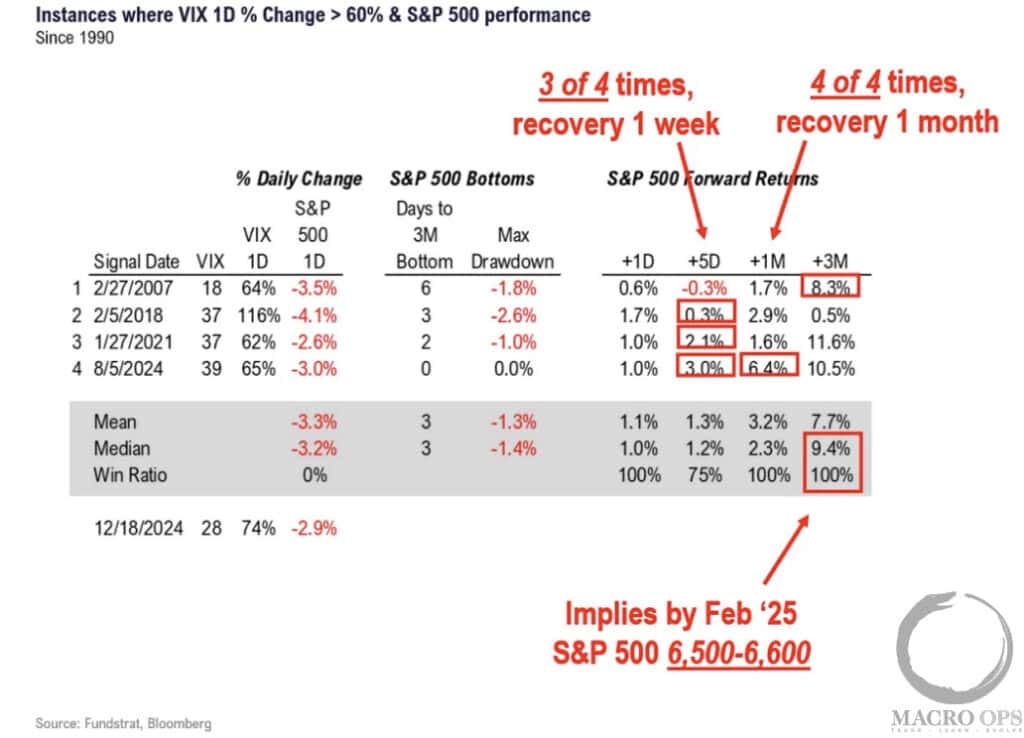

7. The above paints an increasingly bearish picture for the intermediate outlook. That said, we saw a substantial VIX spike last week, which tends to be a reliable indication of short-term capitulation. Red lines on the charts below mark the other four instances where the VIX’s 1D RoC spiked above 60.

8. This chart from Fundstrat shows the follow-on equity returns after similar instances. Returns skew strongly positive over the following one- and three-month periods. A few things, though: This is a small sample size, so take with a grain of salt.

And look, the picture I’m trying to paint here is that the cone of probabilities has widened for the immediate future. I can argue for a Santa rally bottom here that sees the market go parabolic over the next month, just as easily as I can argue for continued chop and vol as increasing yield volatility compresses equity valuations.

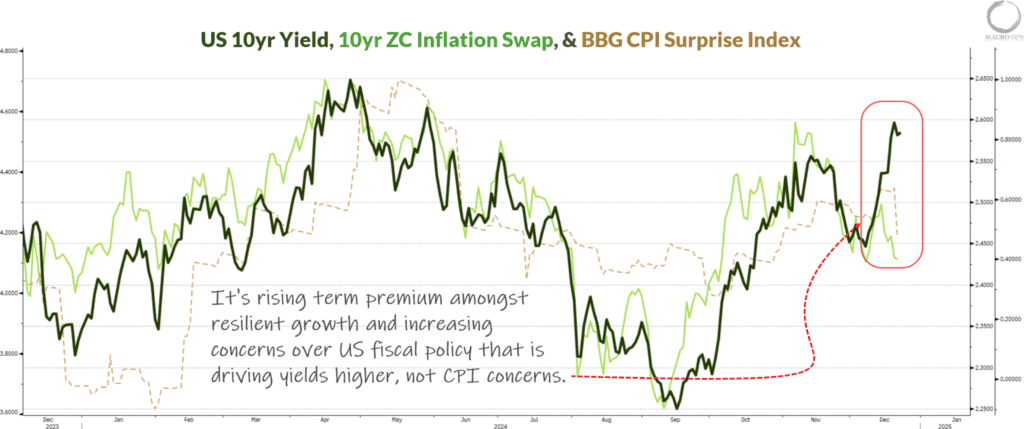

9. Speaking of yields, the recent spike isn’t being driven by inflation concerns, which I see a number of people pointing to. Instead, it’s due to resilient GDP growth and growing concerns over the US’s fiscal position. Both of these factors are driving a widening in the term premium.

Here’s the thing, though… I’m seeing increasing weakness in the economic data. This drives me to overweight the probability we see much lower growth and inflation in the first half of 25.

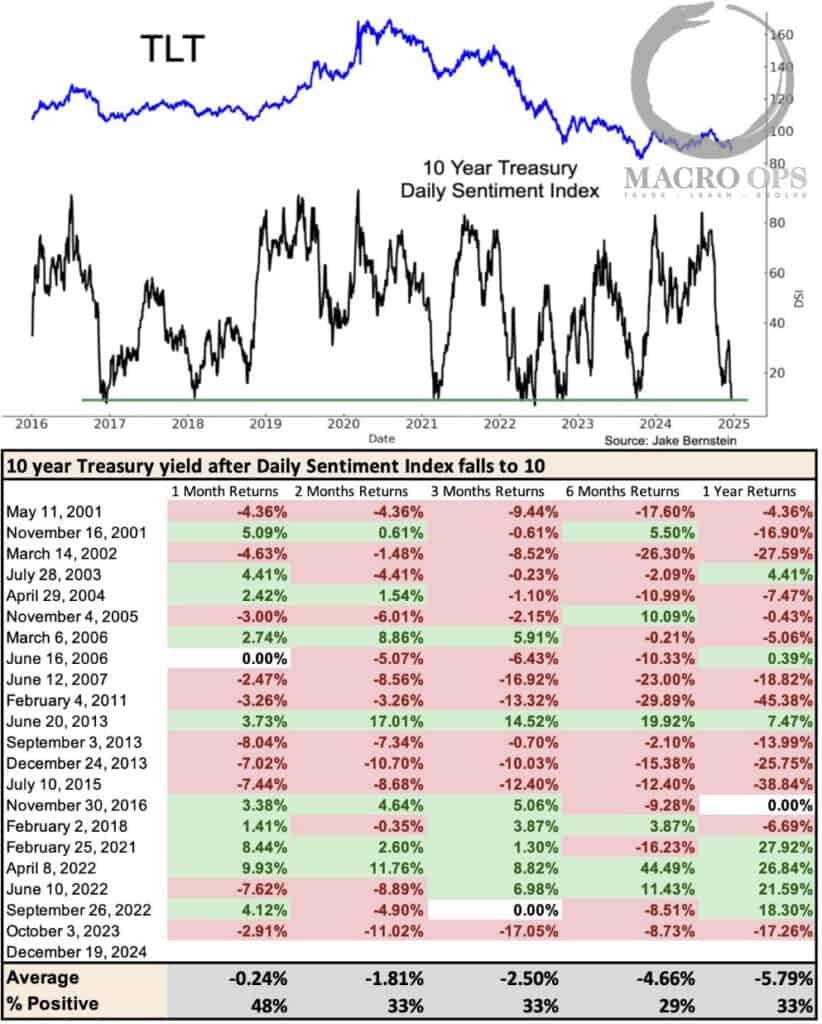

10. Bernstein’s Daily Sentiment Index (DSI) for iShares 20+ Year T-Bond ETF (TLT) has fallen to an extreme bearish reading of 10. As you can probably eyeball, these levels tend to coincide or precede significant bottoms in bonds.

The table shows the returns for yields (not bonds) after similar readings. As we can see, yields tend to fall (bonds up) after such bearish readings.

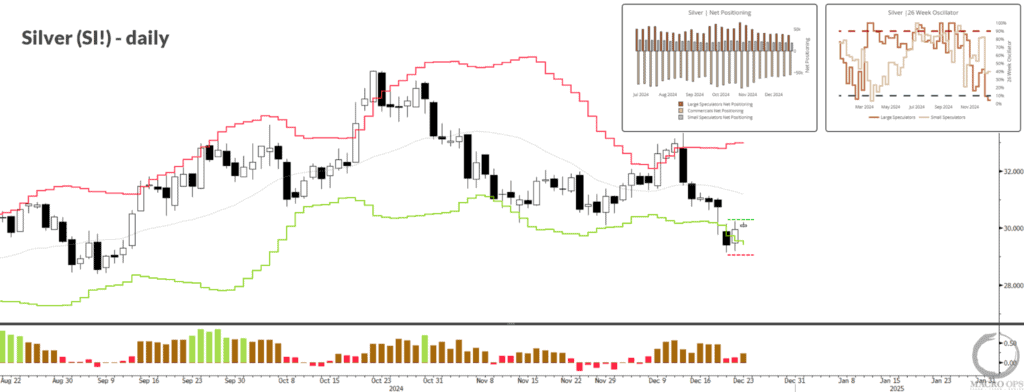

11. Well, when bonds get a bid, precious metals tend to get one as the lower yield makes USD assets less attractive on a relative basis. We’ve been very bullish PMs for the past year and a half. And while we’ve traded around the trend (adding on bottoms and taking partial profits on upside extensions), we continue to view PMs as a Big Bet looking out over the next 3+ years. In fact, according to our framework of fundamental drivers for PMs, the real bull market hasn’t even started yet…

So, in that light, take a look at silver. Our CoT oscillator is giving a contra-buy signal while silver is reversing off its lower band with a neutral SQN regime. This is a good spot to either buy for a quick reversal or take a cheap shot at rebuilding one’s long position.

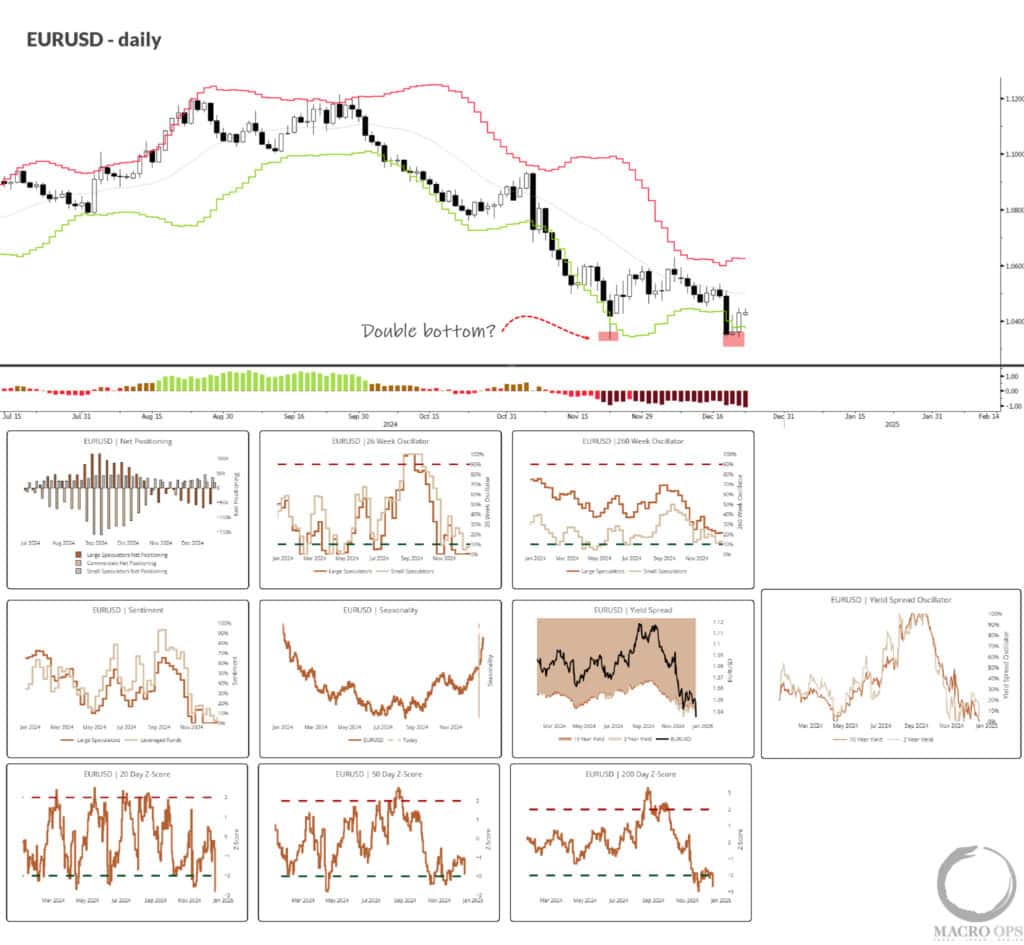

12. We’ve been USD bulls for the past few months, playing the up trend in USDCAD. And while we’re still long, we’re noticing a few USD pairs looking ripe for a reversal.

One of these is EURUSD, which is putting in a potential double bottom on the daily. We have CoT buy signals across both short and long-term indicators. Sentiment is in the trash and the tape is oversold. And if US bonds catch a bid soon (yields fall), then look for a sharp reversal here. Current technicals give us a good R/R low-risk entry point.

If you’d like to join the Collective, our premier service that offers discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders/investors dedicated to mastery, then click the below and sign up. We look forward to seeing you in our Slack!

Thanks for reading.