We’ve got an early Christmas gift for our swarm of Hive readers this week. Wait for it …

We have a podcast! The Value Hive Podcast!

Click here to listen to the podcast. It’s also available on Spotify and Apple Podcasts.

Stoked doesn’t begin to describe how we feel! We’ve got a killer lineup and a (growing) backlog of terrific content.

We’re talking with value managers, entrepreneurs, psychologists, doctors, you name it. If we think it can help you become a better investor, we’ll release it.

Make sure you click on the link above to listen to our first episode with Richard Howe of StockSpinoffinvesting.com.

With that out of the way, here’s what we got in store this week:

-

- Andrew Walker’s Media Guide Part 3

- Ideal Team Sizes for Research Firms

- The Value Premium is (*gulp*) …. Over?

- Chris Mayer’s Ideas for 2020

Let’s get to it!

—

December 18, 2019

(White) Elephant In The Room: Wondering what to get for your White Elephant office party? Well look no further. White Elephant Rules’ website offers tons of ideas. And for us value investors, each one is under $20! Not bad! You can find all the ideas here.

Here’s my favorites from the list:

-

- Toilet Bowl Mug

- Social Shower Curtain

- Beard Hat (I might buy this)

___________________________________________________________________________

Investor Spotlight: Everything Sports Rights

GIFs by tenor

GIFs by tenor

We’re in Part 3 of this (so far) three-part series on Media Investments. Andrew’s done a tremendous job with this project, and we couldn’t thank him enough. Part 3 covers all things sports rights. Oh, and here’s a tickler … we’re releasing our podcast with Andrew on this exact topic next week.

Stay tuned!

Sports Rights & Where To Play The Game

Sports faces a problem. They deliver more value to the TV bundle than they receive in compensation. But as Andrew explains, they’re never going to realize that value arbitrage as long as they’re tied to the bundle. Here’s the issue. If sports gets their way and realizes larger profits, every other content producer will do the same.

Andrew lays out four takeaways from the above logic:

-

- Sports delivers a lot more value than the price they get

- Sports channels are incentivized to increase their price

- Increasing price will eventually cause the collapse of the bundle

- There’s no way for sports to monetize better than its current form

How To Bet on Sports Rights Future

There’s bullish tailwinds for the sports rights industry. So what are some ways to play that theme? Andrew offers four flavors:

-

- Buy a publicly traded team

- Buy a publicly traded sport

- Buy an RSN

- Buy the networks

What’s Andrew’s take? He’s bullish sports rights and bearish sports rights holders. Here’s his thesis:

__________

“Sports is going to do gangbusters as they get more and more consumer data. My guess is that the sports leagues all eventually take their sports rights back and launch direct to consumer apps that they can monetize through hyper targeted advertising and merchandise sales.”

__________

The Dangers of Blackouts

Blackouts are bad. But I didn’t realize how bad until reading Andrew’s article. Check out this section (emphasis mine):

__________

“A long term blackout is really, really bad for an RSN. An RSN’s leverage is pretty simple: if you drop us, all of our passionate fans are going to leave you for someone who carries us. That’s a really powerful stick; however, once the RSN has been dropped, the stick isn’t there any more: after a few weeks, all of the people who cared enough about the team to switch providers have largely done so.”

__________

Here’s the rub. If a sports rights company prices themselves too high, they’re at risk of blackout. And good luck getting back in once you’re out. Fans would have nowhere to turn to for their local team.

Blackouts also affect the individual sports teams. Andrew notes that these teams rely on viewership for:

-

- Driving fan engagement

- Merchandise sales

- Popularity

- Season ticket sales

And more.

As always, the entire piece is a great read.

___________________________________________________________________________

Movers and Shakers: Optimal Teams & Value Premiums

GIFs by tenor

GIFs by tenor

Ever wondered what the optimal size for an investment team? Concerned that the long-standing value premium is dead? This is your section. First we’ll dive into Michael Mauboussin’s research on the ideal size of an investment team. Then, we’ll check out some charts to show the value premium is, in fact, dead.

Mauboussin’s Findings

The suspense is killing you.

According to the CNBC article, Mauboussin’s research reveals the optimal number. Three.

He also notes a couple of interesting facts:

-

- Funds managed by three-person teams outperform solo-run funds by 58bps a year

- 75% of all actively managed funds are team managed, leaving only 25% run by one-man shops

Three makes logical sense. Not too big where bureaucratic practices take over and ideas can’t pass. Yet not small enough to fall victim to one person’s biases or intellectual errors. Further, Mauboussin explains that, “Smaller is better than bigger. Three would be preferable than seven.”

Mauboussin notes that diversity amongst an investment group is critical to its success. He’s not referring to social diversity (such as race, gender, etc.), but also cognitive diversity. Cognitive diversity includes differences in education, training, experience and personality.

The End of The Value Premium

I hate to get all gloom-and-doom on you. But this whitepaper from StarCapital Research is full of insights on the value premium decline.

The main thesis (emphasis mine): “Any consistently successful strategy would attract so much capital over time that it would rob itself of its own basis for success. Cycles are the price of outperformance. Nevertheless, after more than ten years of disappointment, the question arises whether we are experiencing a normal weakness or whether structural changes mark an end to the Value effect.”

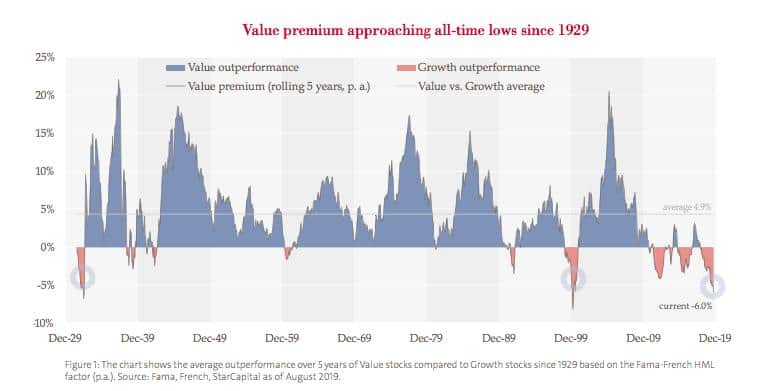

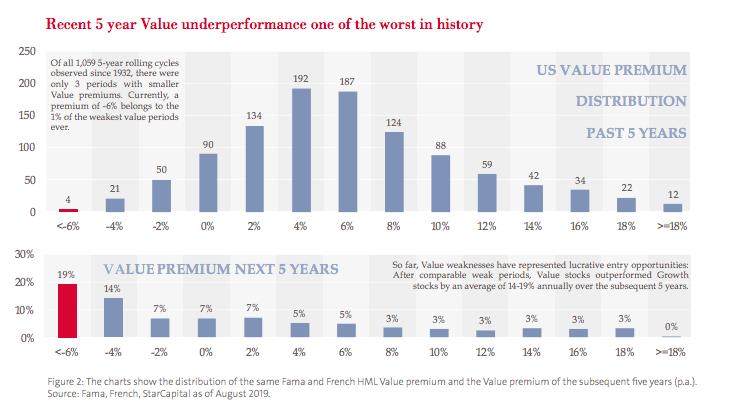

Some Nice Lookin’ Charts

Here’s a couple charts that highlight the scale of this value effect decline:

As you can see in the above chart, we haven’t experienced growth outperformance like this since the dot-com bubble and the Great Depression.

The most recent five-year value underperformance is in the top 1% of worst performances in statistical history. Ouch!

But why? StarCapital offers a few reasons:

-

- Increased use of smart beta products

- Growth stocks able to maintain above-average growth rates and profitability

- Convergence of technology, media and communications sectors

- Simultaneous integration of new technologies and lack of regulation on new business models

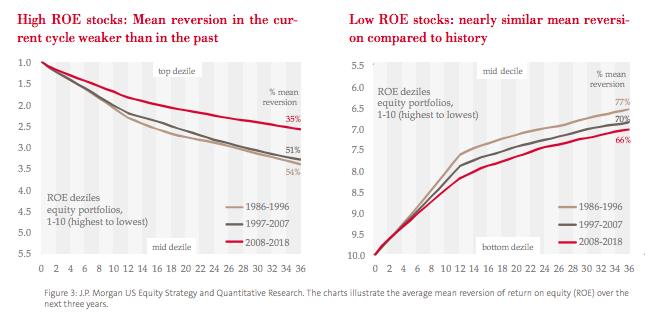

But the real problem here is lack of mean reversion …

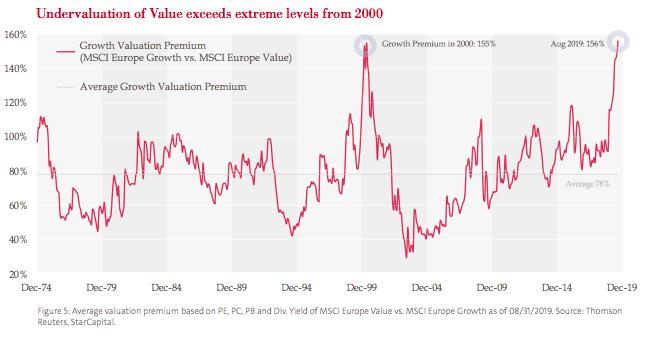

But not all hope is lost. Inverting the question, we realize value stocks are cheaper than they’ve ever been in history. Check out the chart below:

Since this is a value investing newsletter, we’re hoping the tide shifts. Remember, value investing works because it doesn’t work all the time.

___________________________________________________________________________

Resource of The Week: Adventur.es 2019 Annual Letter

GIFs by tenor

GIFs by tenor

New Fund, New Partners, Same Old Strategy

That’s the title of Brent Beshore’s 2019 Annual letter. The letter is full of gems so I encourage you to read the whole thing. Here are Brent’s cliff-notes from his Twitter post:

I’d say that’s being a bit productive! Brent and company buck the trend of traditional private equity. Don’t believe me? Check out this paragraph (emphasis mine):

__________

“We take no fees on the capital we raise and cover all our own costs, including travel, dead deal-related expenses, and all overhead. We buy with no intention of selling, typically use no debt, and like to keep leadership teams intact post-close. If you’re familiar with private equity, that makes no sense.”

__________

I love that. Not only is it a great framework for future private equity funds, but also for investment partnerships. It echoes Buffett’s early partnership days.

Career Risk Changes Everything (But The Culture of PE)

Brent nails it when he asks the question, “if the traditional PE model is broken, why don’t people change?” Here’s his response (emphasis mine):

__________

“The short answer is career risk. No one wants to break wind in the crowded elevator. To quote the great philosopher Austin Powers when asked how dare he, “I didn’t know it was your turn, baby.”

__________

I’ve chatted about career risk for investment managers in the past. But back to Brent’s letter. He listed a collection of quotes from his road-show to various LP candidates. Here’s a couple of personal favorites:

-

- “If I’m committing to 27 years, I need to see your entire medical history, including blood work and your doctor’s charts.”

- “There’s no way you’ll build a team in Columbia, MO. I mean, come on, who’d want to live there?”

I can smell the LP ignorance through the quotations.

If you haven’t already (and why haven’t you already), give Brent a follow on Twitter. He posts tremendous content that is worth every second.

___________________________________________________________________________

Idea of The Week: A Dark Stock from Dave Waters

GIFs by tenor

GIFs by tenor

Dave Waters released his latest idea on OTCAdventures.com. The stock of note? Monarch Cement (MCEM).

What does Dave like about it? Here’s a few hints (from the write-up):

-

- Cement is low-value, but heavy and bulky. This makes shipping it beyond certain distances from the plant uneconomical

- Element of NIMBYism (Not-In-My-Back-Yard). Cement production plants are loud and dusty. Securing one provides geographical moat

- Operated for 110 consecutive years. That’s saying something

The company trades around 4.4x EBITDA. Realizing that arbitrage between cheap and fair value will take time.

Dave reminds readers that shareholders of dark, illiquid stocks must remain patient. He says, “As with any company like Monarch, shareholders must be prepared to wait a long, long time for an eventual catalyst.”

Dave’s fund, Alluvial Capital, owns shares of MCEM.

___________________________________________________________________________

Tweet of The Week: Chris Mayer’s Ideas For 2020

Chris Mayer wrote a great piece on his ideas for 2020. I recommend reading the entire thing. But if you’re in a jiffy — here’s the cliff notes version:

-

- Buy something in energy

- Buy something in the UK

- Buy something in India

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!