Happy October! This month means Pumpkin Spice Lattes, apple orchards and pumpkin carvings. Speaking of October, we’ve got some spooky news for a few companies in this week’s Value Hive! Forever 21 files for bankruptcy. WeWork halts their IPO. Brokerage companies race to zero commissions, and more!

Make sure to subscribe to this newsletter so you receive it every week, completely free.

Let’s Pumpkin-spice things up!

—

October 02, 2019

Where Did It All Begin? — October. The month we celebrate skeletons, dead people and grabbing candy from strangers’ homes. Is there really an age limit to Trick-or-Treating? Anyways, can you guess where Halloween officially began? House rules apply: No Google! Answer at the bottom.

Investor Spotlight: No Mas IPO for WeWork, Bye Bye Forever 21

GIFs by tenor

GIFs by tenor

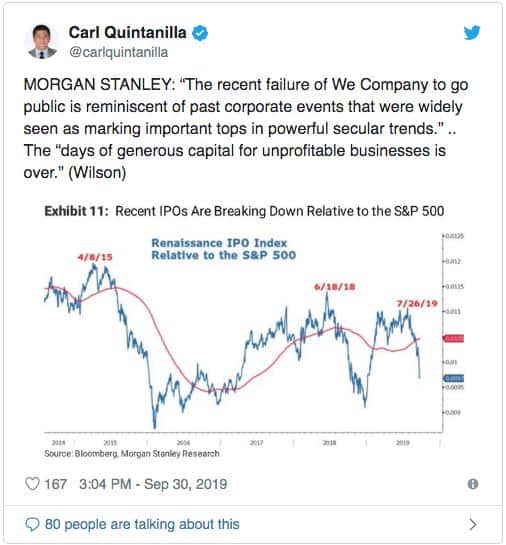

Value Hive was born the first week of September. Over the last four weeks we’ve covered WeWork in some shape or form. Yet it appears this week will be our last dance with the glorified rental property company.

The NY Times reported Monday that parent company We halted its IPO plans. The article explains the sentiment around WeWork perfectly, saying:

“The move is the clearest sign yet that investors are increasingly wary of ambitious young companies that have run up huge losses and might not be profitable for years.”

We couldn’t agree more.

The fun doesn’t end for WeWork with the IPO halt. They have cash problems to worry about. The company sported around $2.5B in cash at the end of June. That cash will likely evaporate by the end of the year.

Living on a Prayer

WeWork is the epitome of a train wreck at this point. The company’s fired their CEO, halted the IPO and struggles to secure lines of credit to keep the business afloat.

We’s bonds went from 102 cents on the dollar to 85 cents. Yields skyrocketed to 11%. In other words, every sign is pointing to the same conclusion: WeWork isn’t a good business.

Yet despite the obvious warning signs, WeWork’s negotiating deals with JPMorgan Chase. This last ditch effort appears to be in restructuring their $6B loan that was originally offered.

CNBC correspondent Carl Quintanilla had this to say about the whole WeWork ordeal:

Forever 21 Files for Bankruptcy

Forever 21 is yet another example of the shift in how consumers prefer to shop, as well as the dying culture of shopping malls.

The company filed Chapter 11 bankruptcy. What is Chapter 11 bankruptcy you ask? Good question.

According to USCourts.gov, Chapter 11 bankruptcy is used to restructure the business while keeping the personal assets of the business owner safe (if the business is a corporation). In other words, Forever 21 isn’t shutting down all stores and halting production.

The company said it will close a lot of stores over the coming months. 350 closures when it’s all said and done.They want to get “back to basics” according to senior executive Linda Chang.

What’s The Plan Stan

Forever 21 got a kickstart on capital preservation in September. How? They didn’t pay their leases (don’t give Tesla any ideas!). The company’s renegotiating some of their larger leases. Along with this, the teenage-targeted merchandiser cut over 1,000 jobs.

The company is private and family owned/operated. The Changs plan to pass the business on to their two daughters — if it’s still alive by then.

Movers and Shakers: Brokerage Houses Race To Zero

GIFs by tenor

GIFs by tenor

Early last week, Interactive Brokers (IBKR) announced IBKR Lite. IBKR Lite offers unlimited commission-free trades on US equities and ETFs. Oh, and zero account minimums.

And just like that, the race to zero was on!

This isn’t necessarily a surprise to investors given the rise (and popularity) of trading app, Robinhood. Yet it wasn’t until Charles Schwab came to the party where things got interesting.

Early Monday, Schwab (SCHW) announced that its ending commissions on all U.S. stocks, ETFs and options. It takes Schwab’s commissions from $4.95 to nothing. Zip. Nada.

CEO Walt Bettinger backs up the claim, stating, “This is our price. Not a promotion. No catches. Period.”

Mr. Market’s Response

Mr. Market doesn’t seem as thrilled as Schwab clients about zero commissions. Schwab opened Monday down 8% and never fully recovered.

What is the market anticipating? The move reduces Schwab’s top-line revenue. But by how much?

The company anticipates a hit of 3-4% of total revenues. That’s not that bad. And if Schwab is right on its bet, it’ll make up that 3-4% in AUM fees.

The CNBC article notes that the last time Schwab lowered its commission fee, it grew assets from $2.92T to $3.72T. I’m assuming the same reaction will happen this time.

TD Ameritrade Isn’t a Fan

Although the race to the bottom looked inevitable, some brokerages did better than others at adapting. TD Ameritrade wasn’t one of the lucky adapters.

While Schwab and IBKR were busy adjusting their business models to survive in a $0 commission world, TD Ameritrade seemed oblivious.

TD Ameritrade’s stock AMTD took a nosedive, over 25%. Check out the gruesome chart below:

I don’t know if the race to zero is good or bad for Robinhood’s planned IPO. On one hand Robinhood got the major brokers to play on their field with their rules. On the other hand, the major brokers have the resources and market share to take down Robinhood.

Either way, the real winner here are the investors using the brokerages. We win.

Idea of The Week: Nekkar, Inc. (NKR), Focused Compounding

GIFs by tenor

GIFs by tenor

This week’s idea comes from our friends over at Focused Compounding. In their latest quarterly letter, Andrew and Geoff discuss their newest investment, Nekkar Inc (NKR).

Going Abroad for Value

NKR is a Norwegian micro-cap company that’s a combination of Syncrolift and a couple of new ventures. According to Geoff, Syncrolift is a, “ship moving technology used at shipyards as an alternative to a drydock.” The new venture includes cages for land based salmon farming.

The combined ventures will result in “the new Nekkar”. The stock trades on the Norwegian Exchange and reports in Norwegian Kroner. Adjusting for USD the company sports a $30M market cap.

What Geoff & Andrew Like About NKR

There’s a few things Geoff and Andrew like about NKR:

- The company has 3-4 years of backlog. Some of which is paid up-front

- The company is trading for less than net cash (with no further needs for capital)

- The business needs no additional capital as it grows

The last part seems to be the crux of Geoff’s thesis. The business needs no additional capital as it grows.

To explain this phenomenon, Geoff gives a hypothetical scenario for NKR (emphasis mine):

“This means that if Syncrolift were to grow revenue, earnings, free cash flow, etc. by about 6% a year — which is about what it probably has done over the last 25 years — it would be able to pay shareholders a dividend of literally everything it reported in earnings and that dividend would also increase 6% a year.”

How Cheap Is NKR?

Given the net cash, Geoff and Andrew paid a negative EV/EBITDA for the company. Yet on a forward looking basis, Geoff believes the price paid “isn’t going to be that low.”

Geoff estimates that when it’s all said and done, they would’ve paid around 15-20 earnings for NKR.

What’s Not To Like

Nekkar is a very cyclical business. When it looks expensive that’s when it’s probably cheap. And when it looks cheap that’s probably when it’s actually expensive. There’s also currency risk involved between the Norwegian Kroner and the USD.

Focused Compounding’s Newest Fund

I can’t talk about Focused Compounding without bringing up the HUGE news. Focused Compounding, in partnership with Willow Oak Asset Management, will launch a private investment fund vehicle.

I’ve known Andrew via Twitter for quite a while now. There’s not two people more deserving in this business than Anrew and Geoff. I wish both of them the greatest of successes in their newest venture.

Hey, it gives small guys like us motivation to keep going!

Resource of The Week: Jim Chanos Slide Deck

GIFs by tenor

GIFs by tenor

When Jim Chanos speaks, I listen. He’s one of the best (if not the best) short seller of this generation. Late last week Chanos released a slide deck on GAAP Accounting fraud.

It’s loaded with gems. I found myself reading the deck on my iPhone while at a bar in Charleston at 1:00am. I don’t know if that says more about my dedication to investing, or my complete lack of social skills. I’ll let you decide.

One of the biggest takeaways from the deck was the rise of “Pro-Forma” and “Adjusted” results. Companies that direct investors’ attention away from audited financials and towards adjusted metrics should be taken with a grain of salt.

According to Chanos, earnings press releases are the “Wild West” of Wall Street. They’re lightly regulated and prepared by management, not auditors.

Who Won Twitter? — MastersInvest.com

Bonus Round

It was the Celtics from Ireland that started the tradition of Halloween. How many of you thought it was a Hispanic country?

That was my first guess (curse you, Dia De Los Muertos!).

The Celts believed that on October 31st, dead relatives would visit their families.

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!