October’s well underway, but yesterday marked my official first day of Fall. My girlfriend convinced me to visit a pumpkin patch. We took “artsy” photos with pumpkins and tractors.

Safe to say I’m buying puts on her IG page if she posts those.

Here’s what we got in store for you this week. PG&E hides under the covers and shuts off power. Greece throws their hat into the negative-yielding debt parade. The short seller that screams loudest doesn’t always win, and more!

Make sure to subscribe to this newsletter so you receive it every week, completely free.

Onwards!

—

October 16, 2019

Back To The Trivia: We took a hiatus from financial trivia for a couple of weeks. Time to break that streak. This week’s trivia challenge is a good one. Are you ready?

How many times does the phrase “United States of America” appear on the $100 bill? House rules, no Google! If you know it, email me the answer and I’ll personally Venmo you $1. Oh and did I mention next week’s Value Hive will feature the winner’s name? Don’t everyone scream at once.

________

Investor Spotlight: You’re Wrong, Harry

GIFs by tenor

GIFs by tenor

Harry Markopolos. The man became a household name after exposing Eron for what it was. A giant fraud. After scoring big with his claim, Markopolos sought another target. General Electric (GE).

You can find his original bearish pitch deck here. But I’m warning you. It’s 175 pages long. That’s a lot of trips to the bathroom to finish a piece of that length.

While the sheer size of the piece is impressive, it turns out Markopolos might be wrong. There’s still a ton of red flags to go around surrounding GE’s future. But a high profile win in this corporate battle would go a long way.

What Did Markopolos Claim?

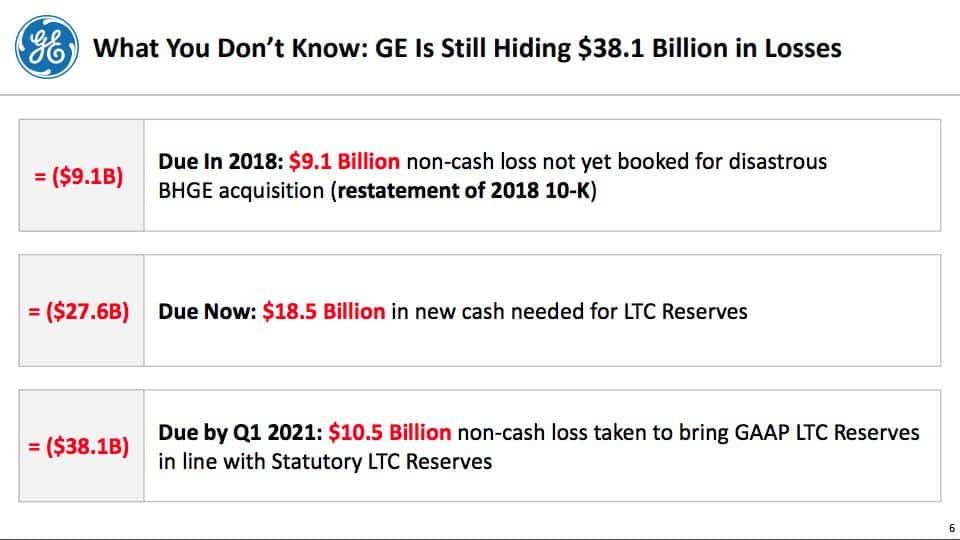

In short, Markopolos thinks GE’s hiding close to $40B in losses. Here’s his breakdown:

Markopolos goes on to assert that GE’s hiding another $29B in long-term care insurance liabilities. According to Markpolos, GE’s actions are worse than Enron and WorldCom.

That’s quite a claim.

Like I mentioned, GE has a lot of problems. Yet most of them stem from Jack Welch’s brain-child, GE Capital. Not current management.

Rumors then surfaced regarding the investigator’s motivation for such a release. After all, why now? Why not when Welch was at the helm? What unfolds next is something out of Billions.

Markopolos’ Dirty Laundry

Here’s where things get interesting. It doesn’t matter if Markopolos ends up correct or wrong. He gets paid either way!

How so? Markopolos gave his short thesis to an unnamed hedge fund ahead of its release. Coincidentally, the unnamed hedge fund planned to short GE before the report became public.

In exchange for the short report ahead of public release, the hedge fund agreed to share its profits from the short with Markopolos.

If this sounds a little bit like market manipulation, it’s because it is.

Like clock-work, GE’s stock fell over 10% after the report hit mainstream outlets. We don’t know the size of the hedge fund’s short position, nor Markopolos’ winnings.

What Markopolos Got Wrong

According to the article, Markopolos failed to account for the differences between STAT and GAAP accounting. To simplify, STAT is GAAP’s more conservative brother. The article notes, “Both STAT and GAAP mandate that companies hold adequate reserves, but their methods of calculating those reserves are different — with STAT requiring greater caution.”

What does this mean for GE? In short, their STAT reserve requirements are much higher than what’s reported on their GAAP statements. Markopolos’ claim is that over time, the GAAP requirements must match the STAT reserve requirements.

Insurance Accounting expert Neal Stern thinks otherwise. According to Stern, “Nothing in that FASB rule requires that STAT and GAAP be the same.” Uh oh. Could it be Markopolos misinterpreted an accounting rule? And he used that misinterpretation as the crux of his thesis?

That’s likely an oversimplification, but there’s a lesson to learn here.

People Respond to Incentives

Markopolos is a smart man. Maybe he knew the report wasn’t 100% accurate. Yet I can understand why he released it anyways. Markopolos would’ve profited regardless of if it were true or not. This type of incentive — one which rewards deception and manipulation — is cancerous. It can destroy shareholder value at the expense of fat paychecks for a few individuals.

That’s enough soap-box preaching for one week.

________

Movers and Shakers: PG&E Goes Lights-out, Greece Issues Fresh Debt

GIFs by tenor

GIFs by tenor

PG&E (ticker: PCG) made another splash in the news this past week. Instead of causing wildfires, the California utility company took preventative measures ahead of such natural disasters.

The company’s shut off power to most of Northern California to prevent another wildfire. Why are they doing this? According to the Washington Post, NorCal’s experienced bouts of heavy rain followed by long periods of dry weather. This combination (known as ‘Diablos’) is a breeding ground for wildfires.

You Can’t See Me!

Remember the Paradise wildfire last year? The one that killed 85 people and left 14,000 homes in ashes? You can thank PG&E for that.

PG&E declared bankruptcy shortly after the Paradise wildfire, citing billions in losses. The market shortly (and justly) took PG&E out behind the woodshed:

The most recent drama knocked PCG’s stock another 27% this week (as of 10/10).

I bet you wish you bought puts a couple weeks ago.

Between a Rock and a Hard Place

PG&E’s damned if they do, damned if they don’t. Had they chosen not to shut-off power and a wildfire ensued, their stock would probably go to zero. In hindsight, if there isn’t a wildfire, PG&E shut off power for (effectively) no good reason. Causing millions to live like communist Venezuela.

What’s to learn here? Life as a utility company in Northern California is hard.

Greece Joins The Negative-Yielding Debt Parade

GIFs by tenor

GIFs by tenor

Early last week, Greece joined their European friends in the negative-yielding debt parade. This is yet another sign in the (never-ending) cycle of countries chasing returns — no matter the cost.

According to Avantika Chilkoti and Emese Bartha of the Wall Street Journal, Greece issued €487.5M ($535.31M) of three-month debt yielding -0.02%. In other words, you owe money if you invest in Grecian debt. This negative issuance comes off the heels of an eight-year economic downturn.

Greece is Still in Trouble

Although there’s buyers for their debt, Greece isn’t out of the woods. The country’s only four years removed from -2% GDP growth. Plus Europe’s economy is slowing.

(Note: I’m reaching the edge of my circle of competence with the macro stuff. If you want to dive deeper into the macro, read Alex’s work. He’s one of the best.)

Yet here we are, value investors. Shouldn’t we be greedy when others are fearful? There’s plenty of fear to go around in Greece.

Some Grecian Stock Ideas

Greece stocks usually mean shipping stocks. We’re very bullish on the shipping industry at Macro Ops (disclosure: I own shares in STNG & CPLP). Is there a way to combine our bullish industry sentiment with a fear-laden macro backdrop?

For those that want to do more research, here’s a list of all publicly traded Grecian ADRs.

We’re seeing a lot of bottoming patterns with Greece stocks. Check out some of our favorites:

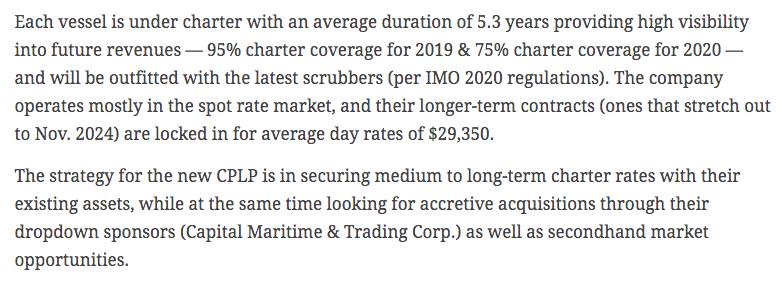

1. Capital Product Partners, L.P. (CPLP)

I wrote about CPLP in my March post, Anchors Away. Here’s the quick-and-dirty thesis:

Current share prices offer a 70% discount to book value (most of which are tankers). Along with a margin of safety, you can buy their existing operations — which are profitable — for less than 4x this years EBITDA.

I am long CPLP as of 10/11/2019.

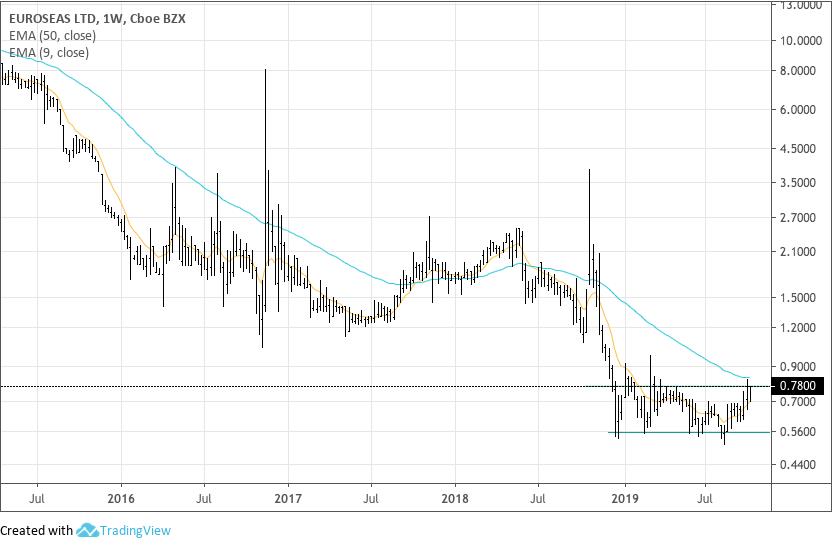

2. Euroseas, Ltd. (ESEAS)

ESEAS is a micro-cap ($12M market cap) shipping company. You can buy shares for 10x EBITDA while getting 70% discount on book value and sales. They also generated $4M in FCF last year. That’s good enough for a 44% FCF yield.

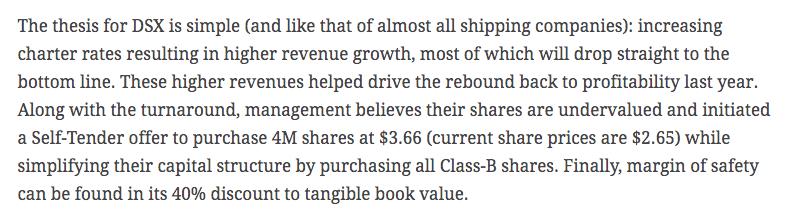

3. Diana Shipping, Inc. (DSX)

DSX was another company I wrote about in the Anchors Away piece. This was my take back in March (it hasn’t changed):

__________

Idea of The Week: PICO Holding, Inc. (PICO), East 72

GIFs by tenor

GIFs by tenor

This week’s IOTW comes from East 72’s Q3 letter. The entire letter is worth the read, especially for those that love asset plays.

Let’s break down Andrew and Marc’s PICO thesis.

It’s About The Water

According to the letter, PICO emerged from a 2016 shareholder revolt laser-focused on monetizing their water rights. The water rights come from two sources:

-

- 51% interest in Fish Springs Ranch (which serves NV)

- 100% interest in storage credits which service AZ market

Andrew and Marc break down the asset value in the letter, saying:

“At prevailing prices, the lesser assets appear to have a value around $70M; the interest in Fish Springs Ranch is worth some $233M ($185M preferred + $48M of equity).”

Remember PICO’s market cap is only $210M (debt-free). According to the letter, the stock trades at a discount to its lesser valued assets, alone.

But we’re not done.

50% Discount to Asset Value

Andrew and Marc then assess the value of the long-term storage credits (emphasis mine):

“The credits can be traded. Recent market prices for the credits are around $375/credit; PICO owns just over 290,000 [credits], worth an estimated $109M.”

Here’s the kicker (emphasis mine):

“Adding up these three assets alone gives a value around $412M before the value of any real estate; along with $10M of cash, the company has an equity value of some $422M before costs.”

A Stock That Doesn’t Screen Well

As of writing this (10/14 AM) the stock trades around $10.30/share. Or a market cap of $203M.

What I love about this idea is that PICO doesn’t screen well for traditional value metrics. The company sports a 200x P/E and 83x EV/EBITDA.

If you’re interested, I wrote about this topic in last month’sValue Ventures newsletter.

Greenblatt likes to say, “If you do good analysis work, the market will reward you. You just don’t know when.”

PICO trades at half of its water asset value. Over time the market should reflect that divergence. It just doesn’t happen on our time frame.

_______

Resource of The Week: Jeff Bezos Interview Compilation

GIFs by tenor

GIFs by tenor

I’m on a Jeff Bezos binge. Yes, it is better than an Office binge.

I found a compilation of interviews from Bezos on Investors Archive’s YouTube channel. The video is 47 minutes long but well worth it. I’m in my second iteration of listening and am learning new things each time.

Also, if you haven’t already, you need to read Bezos’ 1997 shareholder letter.

I tweeted my favorite sections from the letter this AM.

________

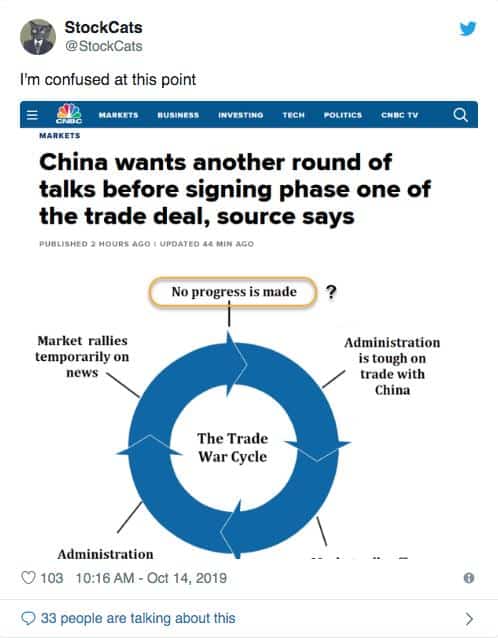

Who Won Twitter? — StockCats

This week’s winner goes to StockCats. Although I’m not a fan of cats (sorry, Alex!), the tweet is money.

__________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!