Sir John Templeton used to quip that “People are always asking me where the outlook is good, but that’s the wrong question… The right question is: Where is the outlook the most miserable? Invest at the point of maximum pessimism.”

If you want deep value and a wide margin of safety then you have to be willing to venture where others won’t. Maximum pessimism is what creates the asymmetric bets where the risk then becomes time and not price, as Richard Chandler puts it.

Looking across global markets today there is perhaps only one industry that fits this bill. Where the outlook is beyond miserable and the stocks within it have either been dismissed by investors or just outright forgotten all-together.

I’m of course talking about marijuana stocks…

Just kidding. No. I’m talking about the shipping sector.

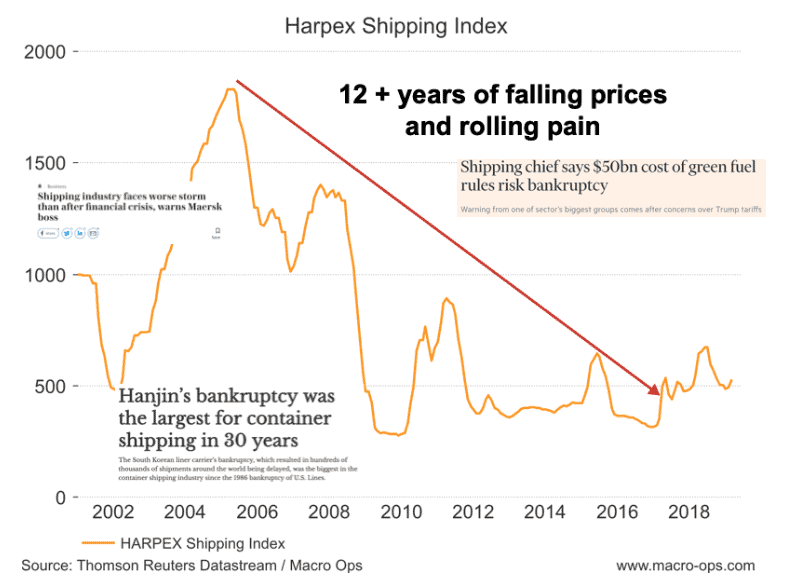

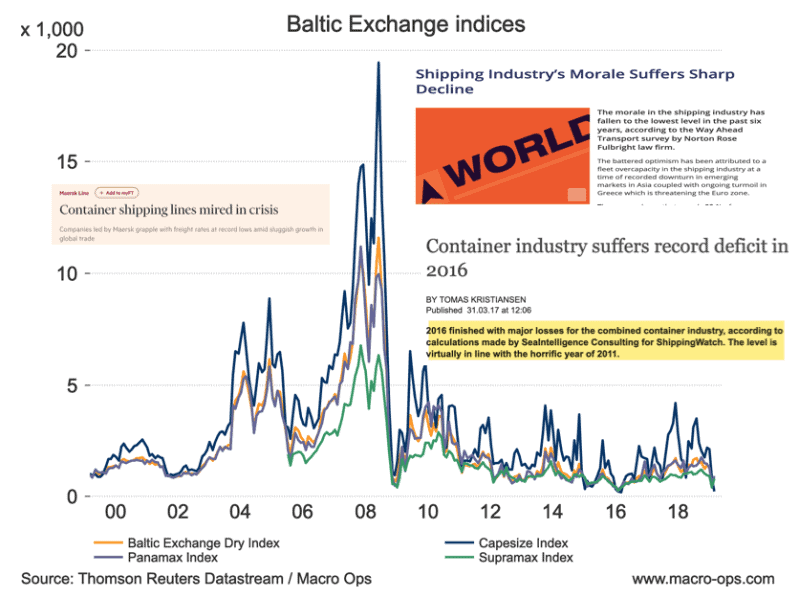

Take a look at the following charts showing the prolonged grinding drop in shipping rates.

The Harpex Shipping Index has been in a steep rolling bear market for nearly a decade and a half.

The Baltic Dry Index is down to 645. It’s only been lower three other times in the past 35-years for which we have data. Once in 1985, then in 2015 and again in 2016.

Price action drives sentiment which in turn drives price action in a perpetual feedback loop. A decade plus of falling prices and negative investment returns has created a pretty fatalistic consensus towards the industry — which has, in turn, led to some pretty amazing prices…

Many shipping stocks now trade for less than half their liquidation value. And that’s using sale prices in the fairly active second hand purchase market.

This means that companies could liquidate their fleets and after paying off debt there’d be enough leftover cash that equity holders would more than double their money.

So to sum things up, we have (1) maximum pessimism which has driven (2) bargain prices which creates (3) a large margin of safety.

That’s pretty good, but now we need a catalyst.

The shipping industry is a notoriously cyclical industry which follows the classic Capital Cycle. Martin Stopford’s excellent book, “Maritime Economics”, notes that there’s been 23 shipping cycles going all the way back to 1743. Timing here is key. We don’t want to sit in a dead money trade for another 5-years when our capital could be going towards something that’s actually working for us.

Luckily, there’s a number of potential catalysts lining up that could make 2019 the year that the trend finally changes. These are:

- A one-two regulatory punch

- New banking regs leading to tighter financing and thus lower supply

- Capital Cycle: supply and demand in deficit

- China/India starting to buckle down on fighting pollution which means they need to import cleaner industrial fuel imports (ie, more shipping demand)

Let’s start with the one-two regulatory punch.

Last year shipping companies were forced to begin installing costly ballast-water treatment systems, thus raising the operating costs on an already struggling industry. And by next year, shippers will have to adhere to IMO 2020.

IMO 2020 is a new global regulation aimed at reducing airborne sulfur pollution by requiring shippers to reduce the sulphur limits in their fuel from 3.5% to 0.5%. There’s a number of ways for companies to reduce their sulphur output and all of them are bullish for the shipping industries’ supply and demand dynamics.

For instance, shipping companies can install scrubbers that will reduce the sulphur from burning bunker fuel. But, these scrubbers are expensive, which means less capital to deploy towards ordering new ships and paying down debt. Also, installation will require significant dock time which means there’ll be less ships on the water, which means a tighter supply market.

Another option, and this is likely to be the more popular one, at least initially, is for shippers to switch to low-sulfur marine gasoil.

But the issue here is that even with no change to the current pricing conditions, switching to marine gasoil will represent a substantial increase in fuel costs and fuel costs already make up the largest portion of a shipper’s operating costs.

According to Wood Mackenzie, shipping industry fuel costs could increase by $60bn next year. This would represent a jump in fuel expenses of around 50%.

In order to economize on fuel costs, ship charterers are likely to begin slow-steaming ships. Here’s the following on what this will mean from S&P Global Platts (emphasis by me):

The simplest way to curtail costs would be to reduce consumption via reducing speed.

“Reducing speed from 12 knots to 10 knots would effectively remove 17% of dry bulk shipping supply overnight,” it said.

Ships older than 15 years of age, comprising about 142 million dwt or 17% of the existing fleet would come under maximum pressure and would become ideal candidates for scrapping, as their older engines are not able to burn LSFO.

“In 2020, you are going to have a supply shock either through slow steaming of the entire fleet or a combination of scrapping of some of the older ships and the balance of the existing fleet slow steaming,” it said.

Then we have new banking regs.

Basel IV bank regulations mean that the traditional sources of financing for the shipping industry (ie, the credit they use to order more ships) are no longer available.

Under Basel IV, bank’s have to account for the volatility of the asset being loaned against. And, well, shipping is pretty volatile. This means that shipping loans are becoming more capital intensive. Gone are the days of 90%+ loan-to-value construction finance which led to the glut of yore. Now, many new vessel orders require over 30% in equity financing.

European banks, which have long been the primary lenders to the industry for the last 100-years or so, are either drastically reducing their loan books or exiting shipping finance all together.

Bear markets are always the authors of bulls. And it’s for reasons like the above as to why tight financing effectively means tight future supply and tight future supply means higher prices.

And this brings us to our next catalyst: The Capital Cycle.

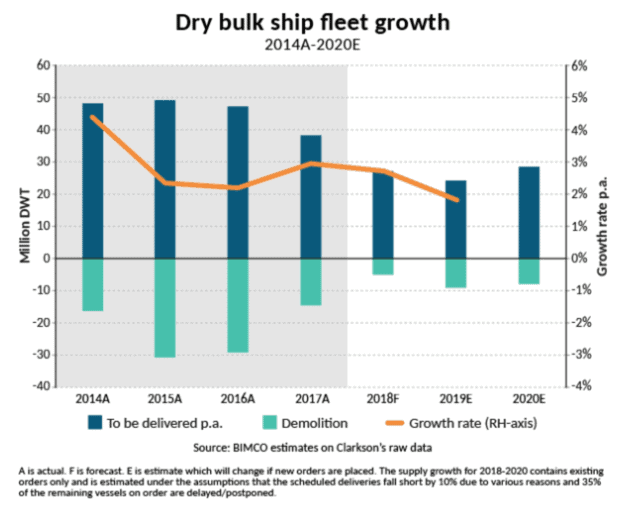

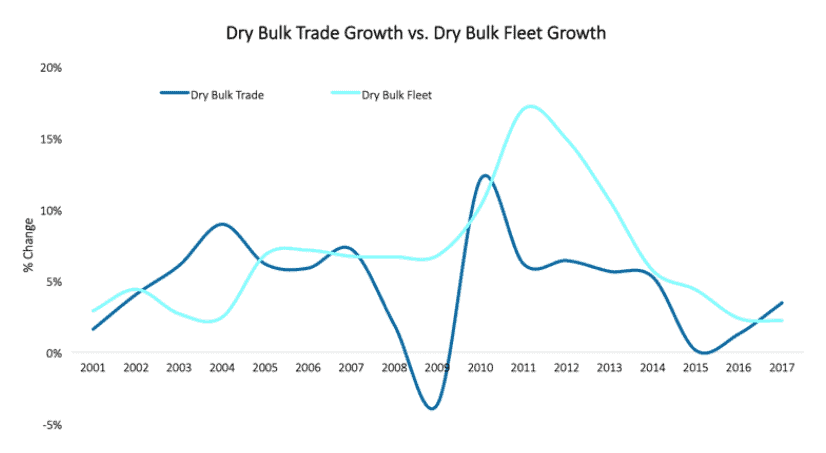

Dry bulk shipping is an extremely capital-intensive business. With over 10,000 ships, each with an average 25-year lifespan, somewhere between 300-500 new vessels need to be built each year just to counteract natural attrition. That’s not even accounting for growth in demand.

According to Clarksons Research, the global bulk fleet is expected to grow by just 2.2% this year.

This will make 2019 the third consecutive year in which demand growth outpaced the growth in supply, putting the market in deficit.

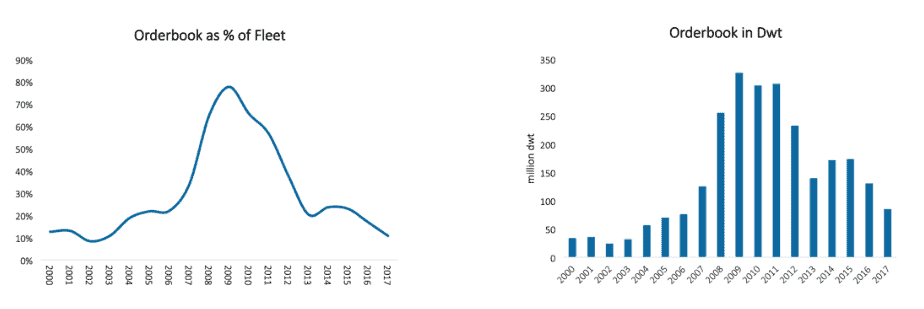

And by the looks of the current orderbook, this deficit looks set to continue. The current orderbook at just 11% of the fleet, is at its lowest levels since the early 2000s. It takes approximately 2-years from the time of order for a ship to be delivered. So this means that a supply constrained market is practically guaranteed going forward.

And lastly, we have the growing importance of combating pollution in emerging markets.

Following China’s recent “Two Sessions”, Li Ganjie, the Minister of Environment and Ecology, declared that “It is necessary to maintain the strength of ecological and environmental protection” and there must be “no wavering, no relaxing” according to Trivium China. Li went on to say that four sources account for over 90% of particulates, with industrial emissions and coal burning the two worst offenders.

The industrial emissions are largely attributed to China’s dirty steel mills. These mills use iron ore that has a high sulphur and ash content. Recent changes in policy will require mills to use less pollutive materials going forward. This means that China will have to import “cleaner” industrial fuel sources (ie, iron ore and coal) from far away places, such as Brazil and Australia.

This is important because iron ore and coal account for over half of the global dry bulk trade (29% and 24% respectively). According to shipbroker Banchero Costa, “China remains very much at the centre of the action, estimated to account for 70 percent of global iron ore imports and 41% of the dry-bulk market all-together”.

Just to show you the outsized impact China has on the shipping market, see the chart below showing Chinese iron ore imports (orange line) and the Baltic Dry Index (blue line).

So the requirement for cleaner industrial fuels is a positive. But this chart also reveals the shipping industries’ achilles heel. China.

Where Chinese iron ore imports go, so too will the shipping industry.

And that’s where the near future for shipping stocks becomes less certain.

I’ve been writing for the last year about how China is slowing down. This slower growth is clearly visible in the data.

And this is putting downward pressure on global trade; hence the recent collapse in the Baltic Dry Index.

But I’m also expecting China to begin pump-priming its economy for the 2021 centenary anniversary of the Communist Party in the second half of this year.

If that happens, then we should get a buoyed global market combined with a structurally tight shipping industry; one that appears to be rising from the trough of the capital cycle.

Throw in the secular rising demand from India crossing the Wealth S-curve and brighter days should be ahead for the industry.

If this ends up being the case then there’ll be oodles of money to be made. Not only do we have bargain bin prices currently but these companies also benefit from high operational gearing.

Shipping companies have extremely high fixed costs, so even a tiny uptick in charter rates flows directly through to their bottom lines. Plus, any upturn in the cycle will raise the value of the underlying fleets which are trading at depressed values. This kind of operational gearing combined with the currently low stock prices means that some of these shipping companies could earn their entire market cap in a single year once cash flows mean-revert.

This is why bull markets in shipping tend to be incredibly explosive.

Shakespeare once wrote that:

There is a tide in the affairs of men, Which taken at the flood, leads on to fortune. Omitted, all the voyage of their life is bound in shallows and in miseries. On such a full sea are we now afloat. And we must take the current when it serves, or lose our ventures.

Shippers undoubtedly have the most miserable outlook. Over a decade of falling charter rates has birthed maximum pessimism, which has led to depressed prices (read: amazing values). Now we have a tight supply market and a turning capital cycle, with a number of structural changes that will ensure it stays this way. China is the big unknown, but it always is. Buying positive FCF producing shippers for less than half of NAV gives us a reasonable margin of safety where our only risk is time, not price.

We’re going to put on a starter position in a basket of shippers. Look for a trade alert with further info soon.

Time to leave the shallows and take the current…

For more information on our market framework click here to access the Macro Ops handbook.