Whatever one’s thesis about the inevitability of the Black Death, it cannot be denied that it found awaiting it in Europe a population singularly ill-equipped to resist. Distracted by wars, weakened by malnutrition, exhausted by his struggle to win a living from his inadequate portion of ever less fertile land, the medieval peasantry was ready to succumb even before the blow had fallen. ~ Historian Philip Ziegler

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at Qs on tech support, a massive oversold reading, a turning credit cycle meeting a cracking wall of FOMO, the internet versus semis, and some good names that have landed on bad times, plus more…

- The 14k support level held in the Nasdaq last week with the market putting in a double-bottom. There are a number of things putting odds in favor of a relief rally this week. But, there are numerous reasons to suggest this will be a rally to sell, not buy… Either way, it’s a Trader’s market… Huzzah!

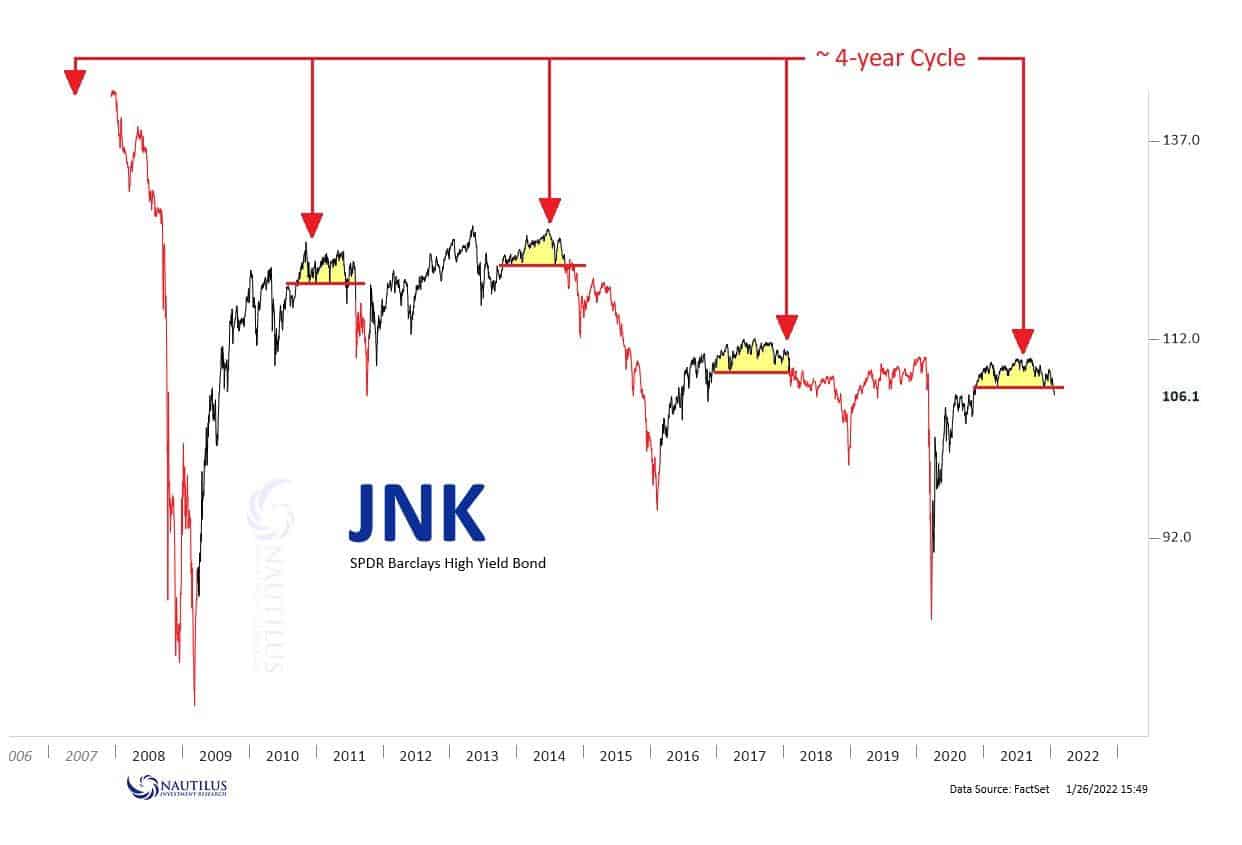

- Not a huge temporal cycle guy myself but a food-for-thought chart from @NautilusCap.

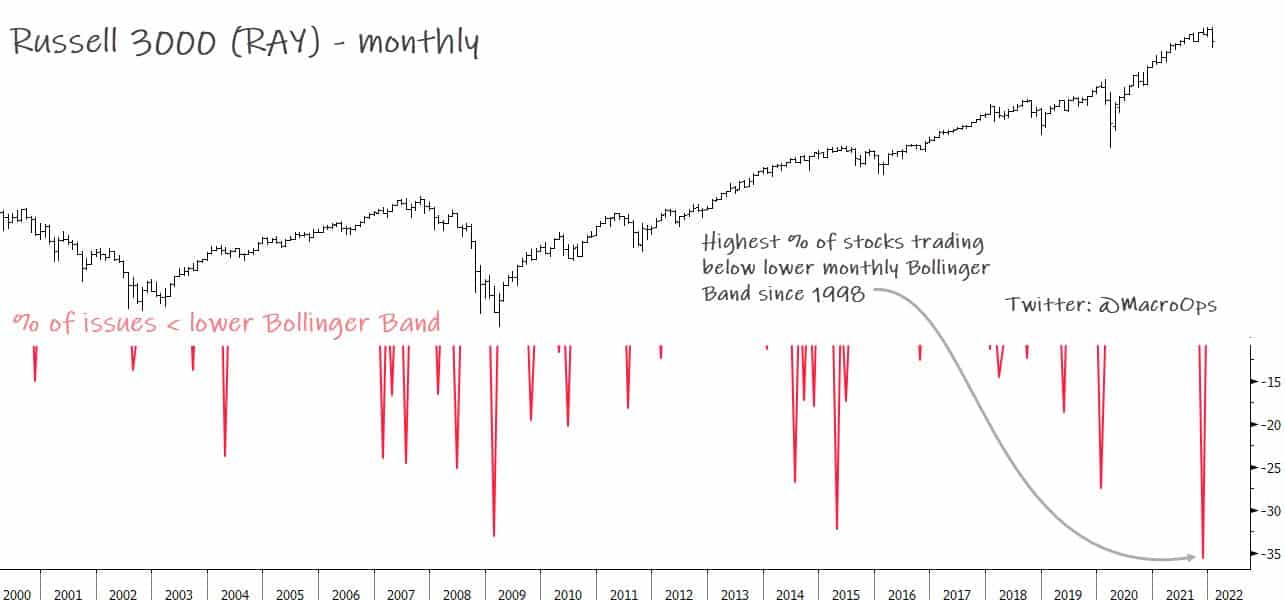

- Thought this was interesting… R3K’s percent of issues trading below their monthly Bollinger Bands hit their highest reading since 1998. That’s a LOT of stocks that are either deeply oversold on a monthly basis or undergoing a major regime change. Probably a bit of both, tbh…

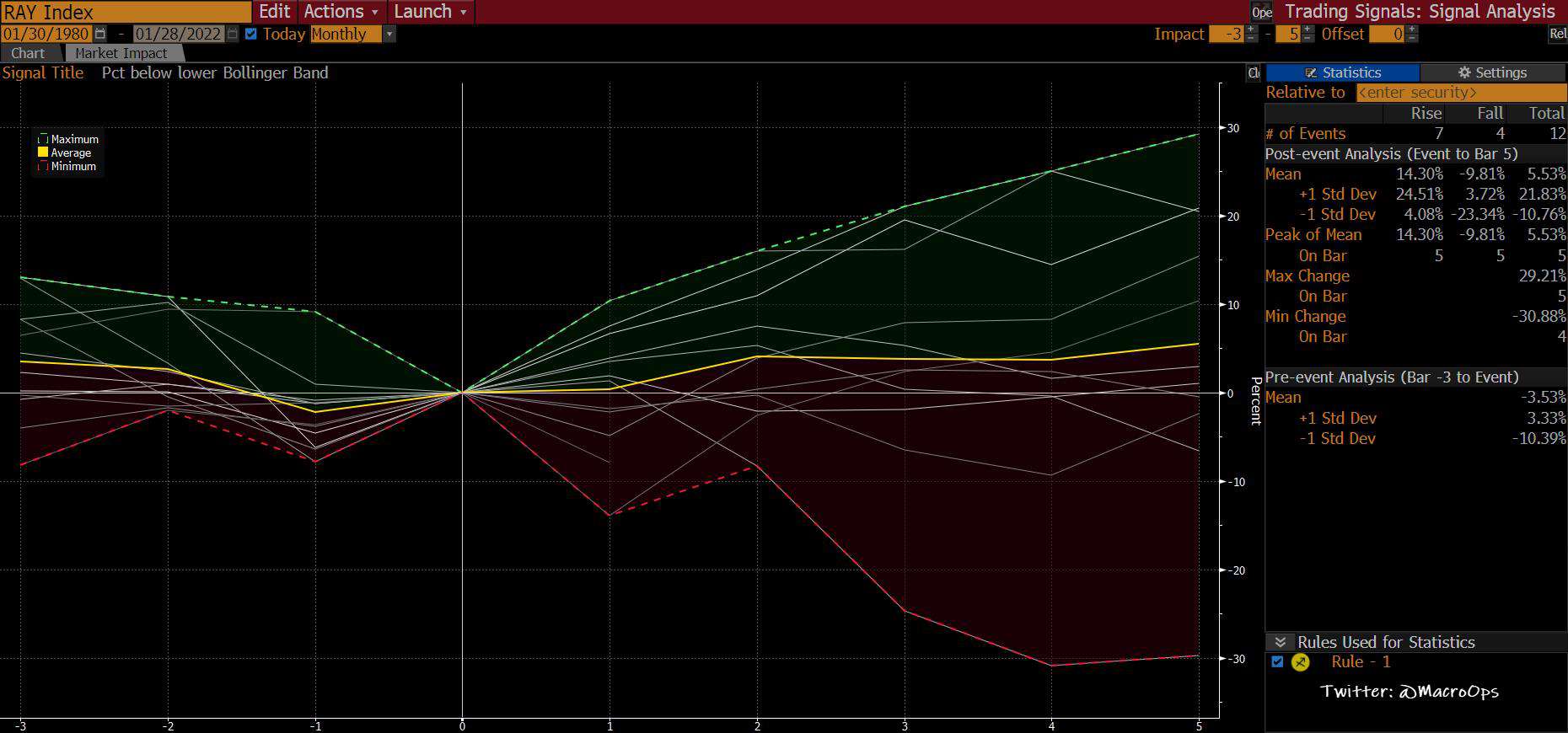

- I relaxed the parameters some to include more cases, but here are the historical instances where the reading has been over 25% of issues (over 35% recently). There have been 11 other occurrences over the last 25-years. Eight ended up positive 3-months later and 3 were down. The winners were up on average 9.3% and the losers down -11%.

What does this tell us?

Not much other than what’s going on in the market is unusual and indicative of a major inflection point — which could be either positive or negative over the next couple of months. So stay on your toes, manage your risk, and listen to the tape!

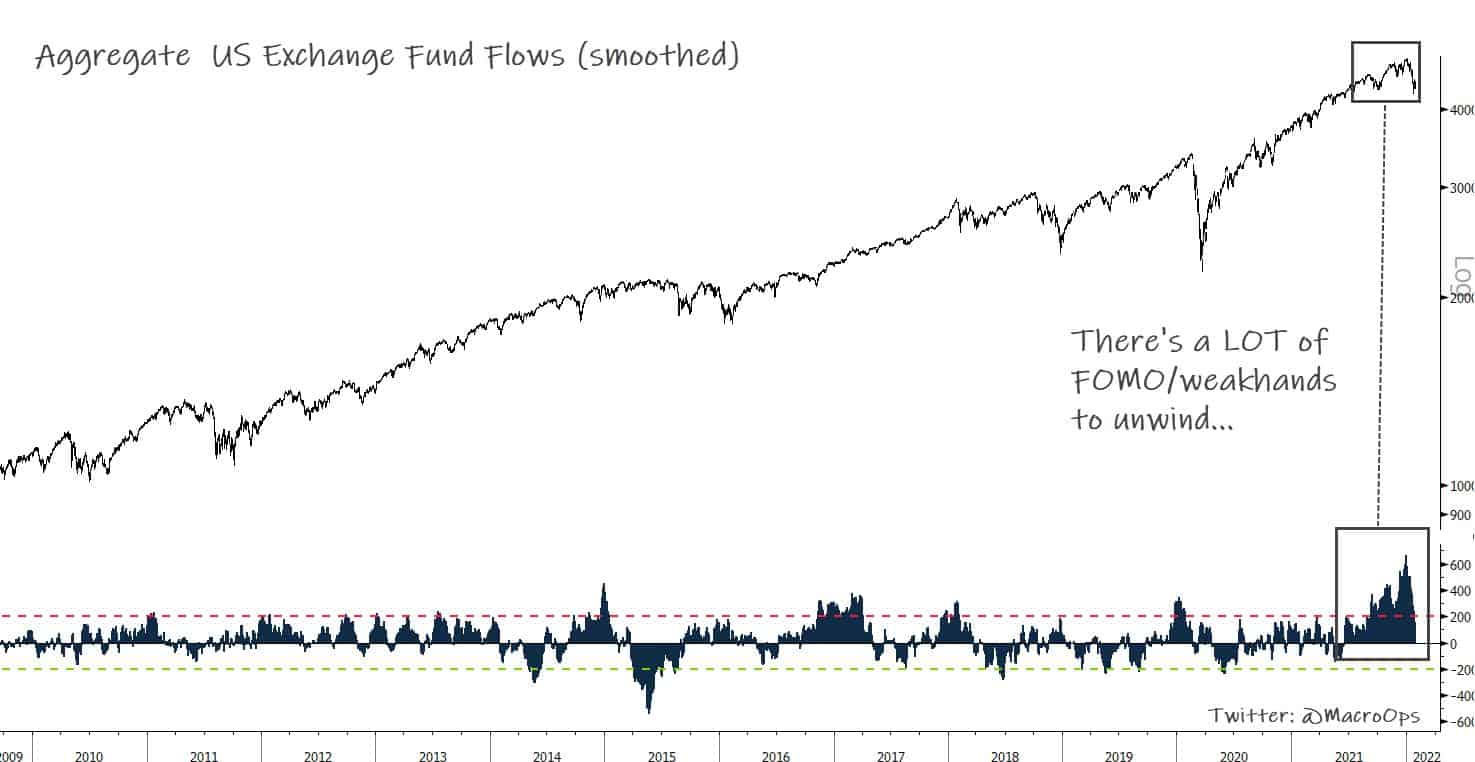

- There are plenty of signs that short-term bearish sentiment is overdone. That’s probably good for a bit of a bounce in the near term. But… I keep coming back to this chart of aggregate US fund flows.

That was a LOT of chasing into the tail-end of an epic 18-month rally. My best guess is that there is a good deal of weak hands to still work through before this market can find a more defensible bottom.

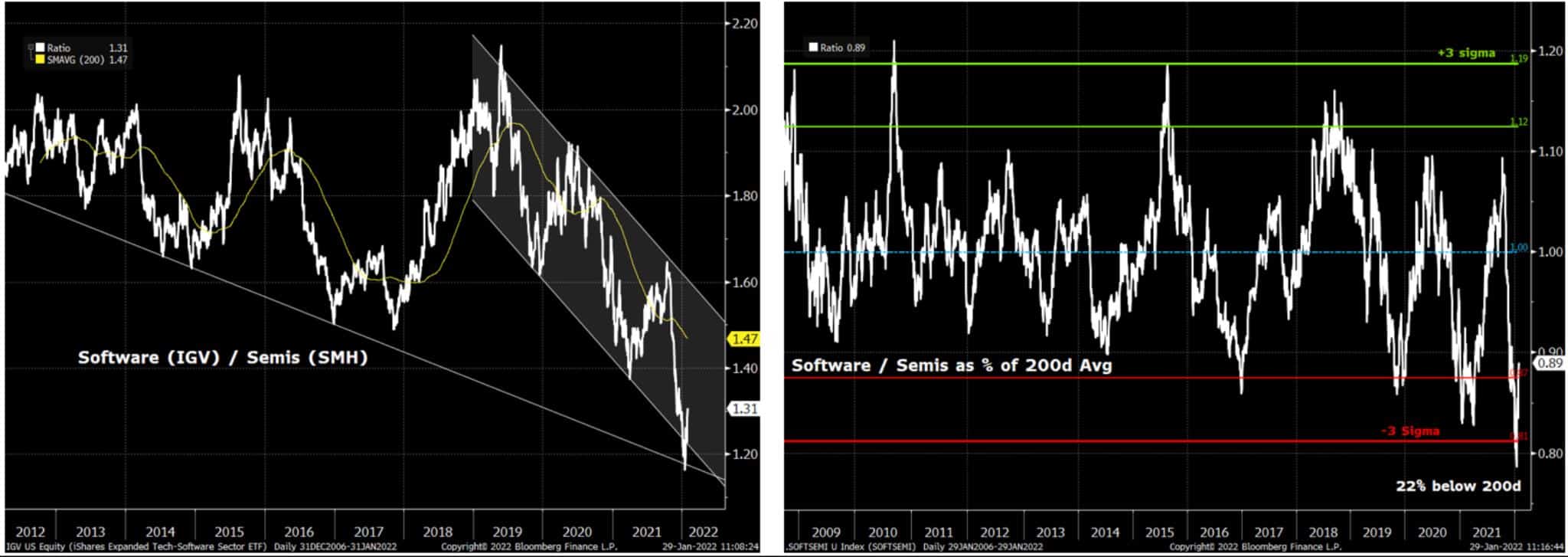

- @MrBlonde_macro has been putting out some great work recently. I highly recommend you give him a follow. In his latest (link here) he shares a number of excellent charts but one that really caught my eye (because it very much confirms my current bias), is the one below of Software vs Semis.

Gavin Baker also referenced this unusual relative-performance disparity in his latest chat with Patrick O’Shaughnessy. It’s a killer listen and I highly recommend you give it a go (link here).

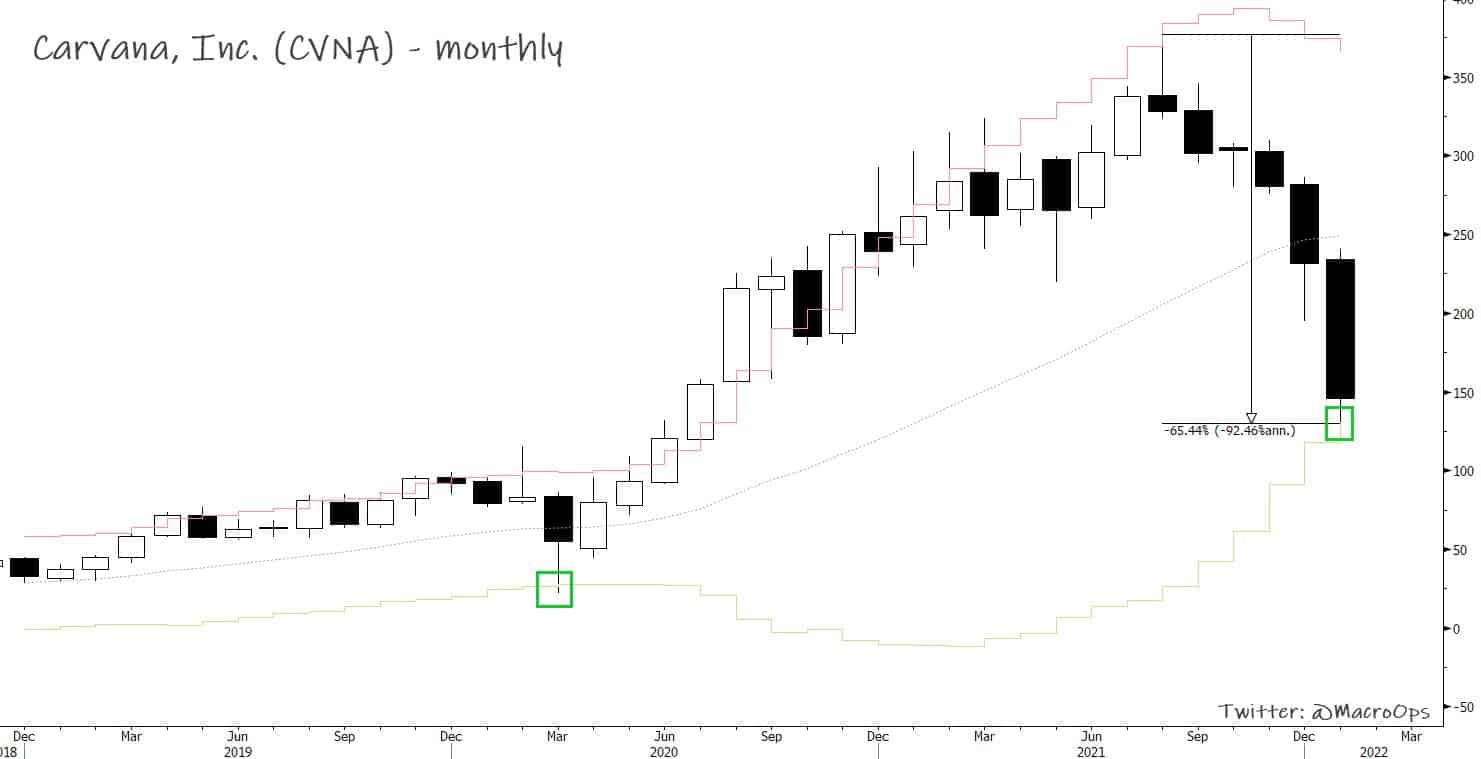

- Not a Software company but an e-commerce biz that has been flattened with the lot of them. CVNA, the digital seller of used cars is down over 65% from its recent all-time highs. The stock now trades at 85’ Grand Am values, going for 0.8x next year’s sales.

My partner Brandon spoke with @The10thman1 a while back about the bull thesis (link here) and RV Capital wrote ‘em up in their latest investor letter (link here). The stock is also at its lower monthly BB.

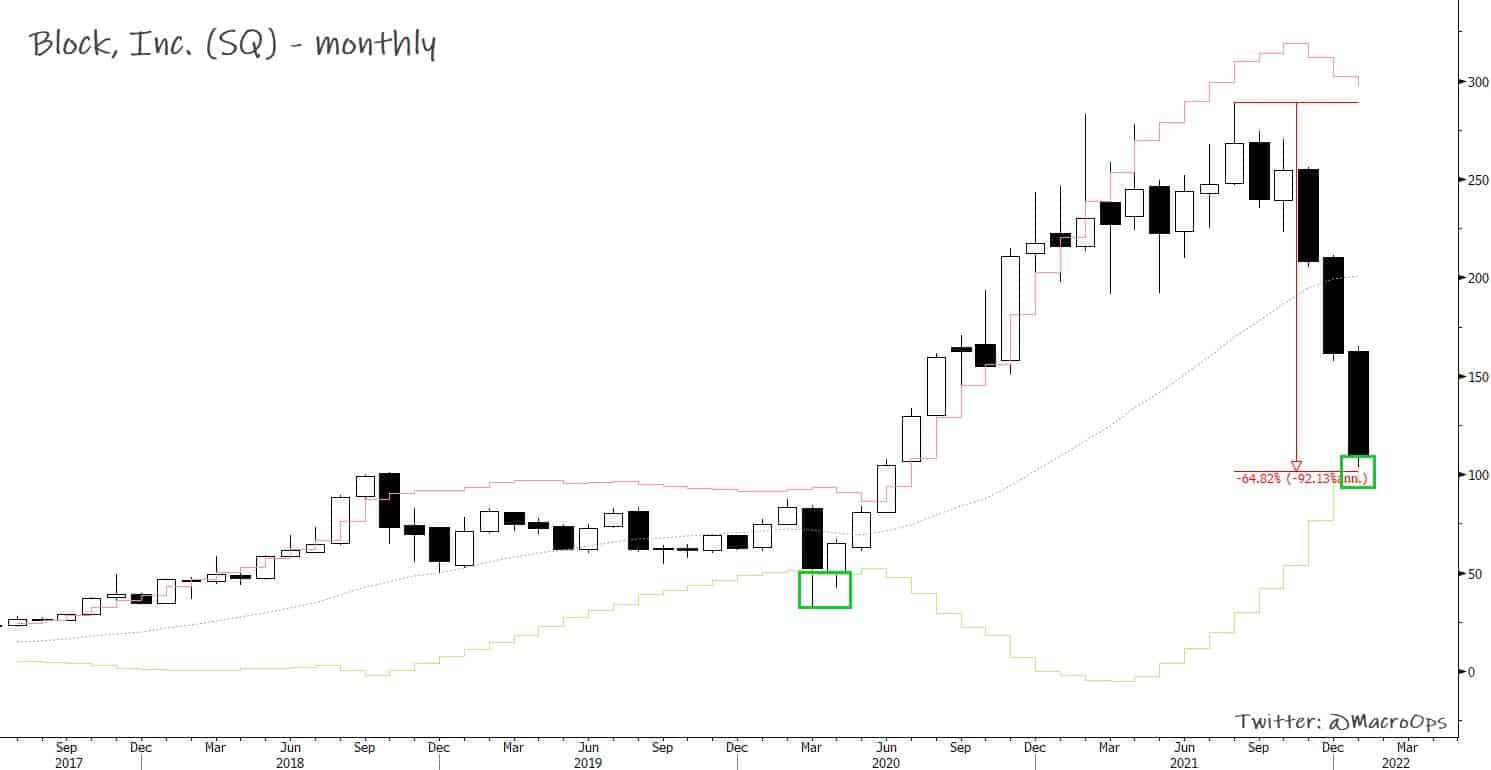

- I wrote up the bull thesis for Square-now-Block back in 2019 when it was trading for roughly $60 a share. The thesis was simple… The Street was being consistently too bearish on the company and Cash App’s growth was not being properly valued at all.

SQ is now down 64% from its recent all-time highs. The Street continues to underestimate Jack, his Block, and its growth potential. This shows up in consistently large revenue and earnings surprises. The stock is also up against its lower monthly BB.

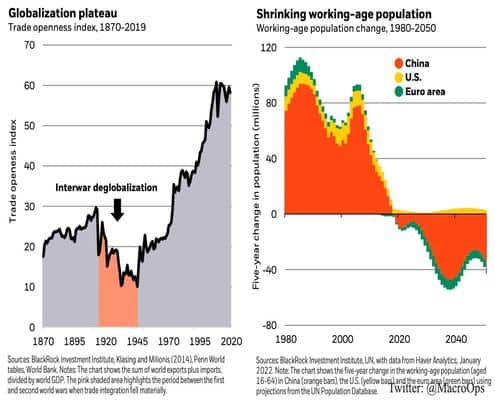

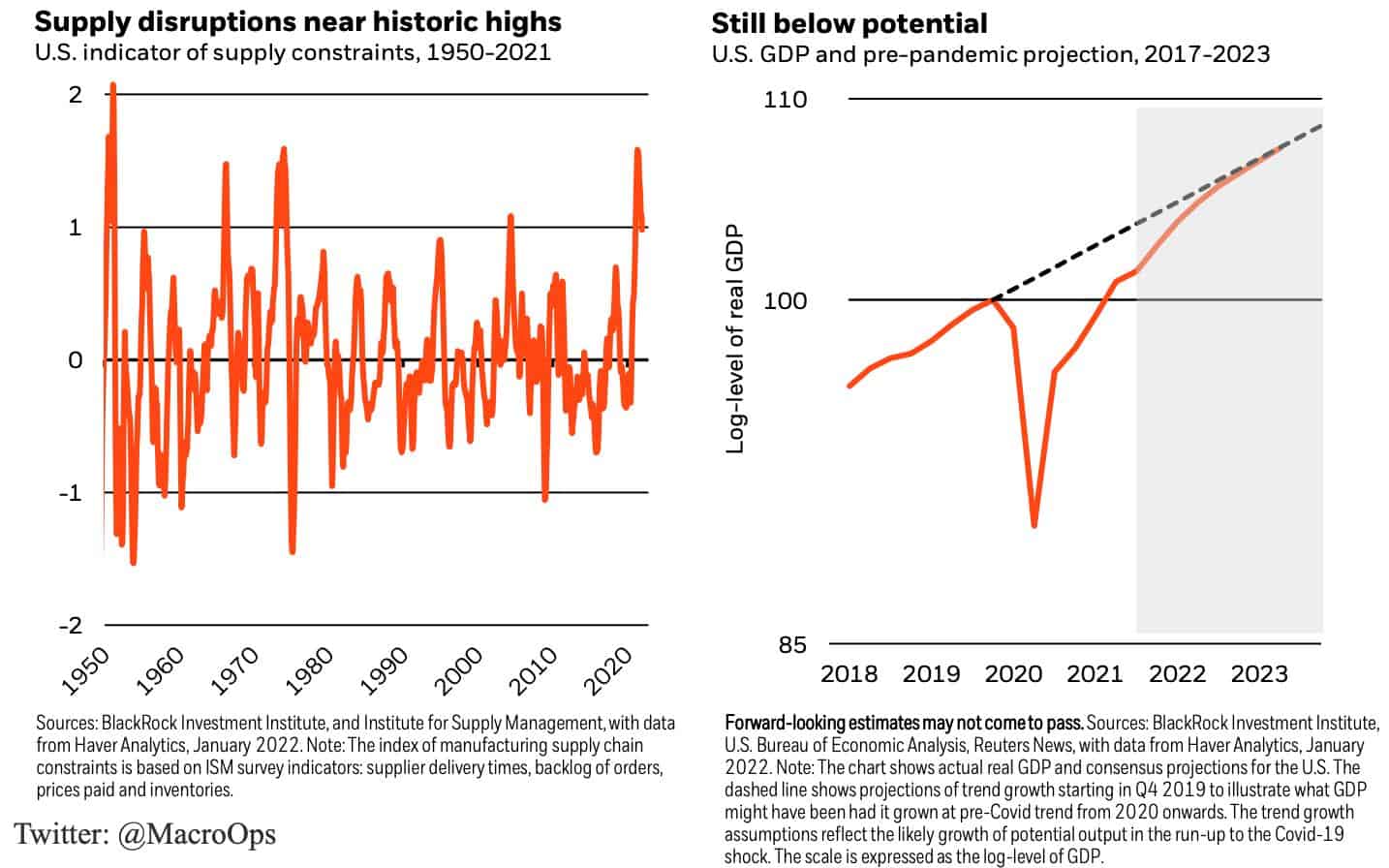

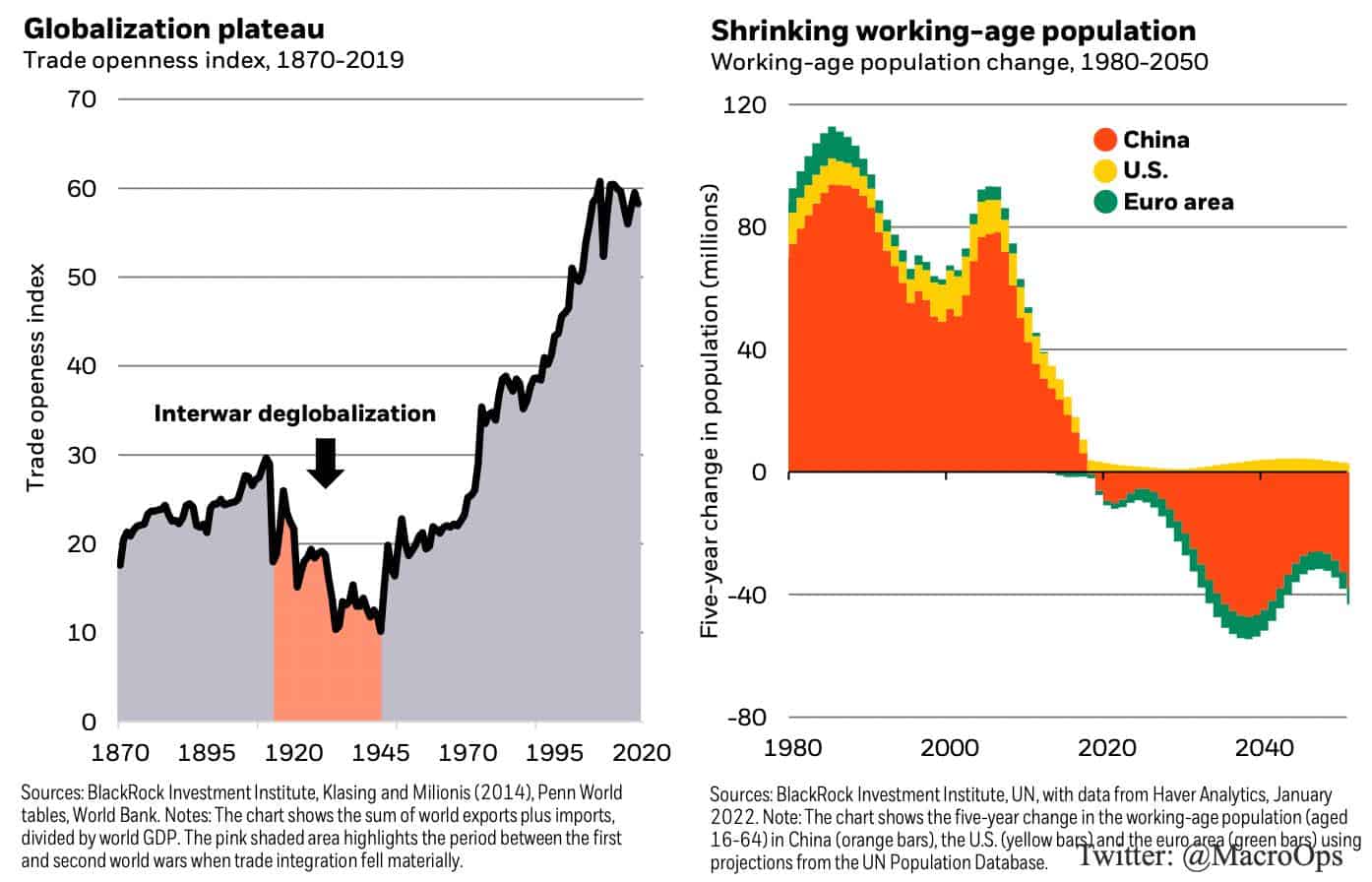

- BlackRock put out a great report (link here) the other week on what they think is really driving inflation along with where they think it’s headed. It’s a good short read and I’m in agreement with much of what they write. Below are two excerpts and charts worth noting (emphasis mine).

“Past bouts of inflation have been driven by economy-wide demand running unusually hot. Economic policy can cool off inflation and keep the economy from overheating. But when supply constraints are responsible for higher inflation at a time when the economy is not yet back to full capacity, there is a difficult choice to be made: either live with higher inflation or destroy activity before reaching full capacity.”

- “…Meanwhile, aging populations mean that the global labor force is growing more slowly. In Europe and – notably – China, it is set to contract. Developments in the Chinese working-age population have, and will, dwarf those in other economies. According to UN data, after expanding by nearly 240 million between 1990 and 2020, the working-age population in China is now starting to decline. This decline, combined with the policy shift in China to a greater focus on quality over quantity of growth as it prioritizes worker safety and well-being, will raise labor costs. An aged population will also mean China consumes more of what it produces, reducing the supply of goods to the rest of the world.”

“Together, these trends mean developed markets will likely face higher costs and will need to source more locally. To do so, resources will need to be reallocated to meet demand. Supply constraints are likely to become more common.”

- I’ve been on the wrong side of the dollar trade the last two weeks, trying to get long. I’m back on the sidelines just watching and eating popcorn. But… EURUSD is back at its lower monthly Band, which has acted as a reversal point in the past (red circles) sans 2014.

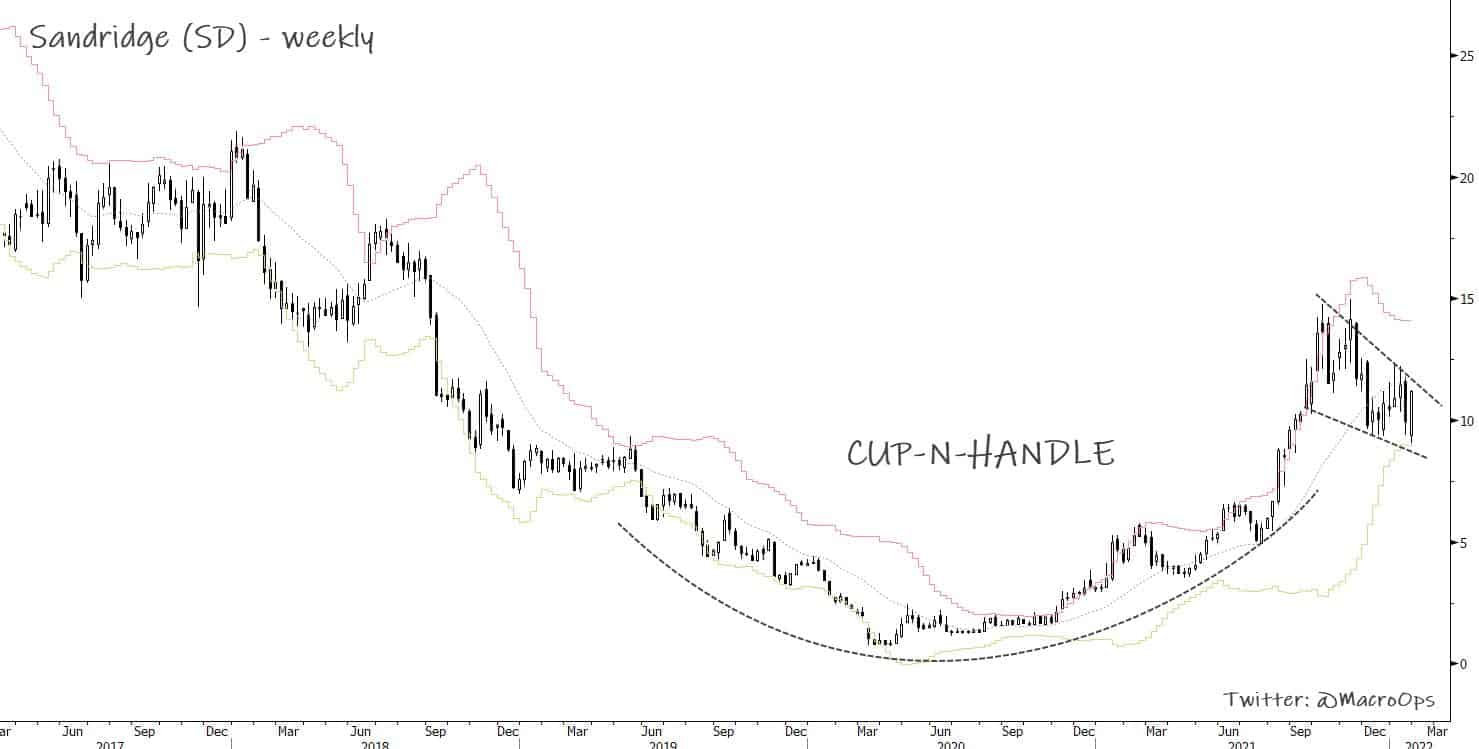

- NatGas continues to do its thing, putting in a strong bullish reversal bar for Jan. I pointed out last week how our Predictor tool projects natty as having the highest forward 10-week return according to historical SQN and price action mixes. The charts for producers are looking mighty fine, as well. Below is Sandridge (SD) with a large cup-n-handle on the weekly.

Thanks for reading.

Stay frosty and keep your head on a swivel.