Saudi Telecom is the largest telco provider in Saudi Arabia. The company offers mobile, landline, Internet, and TV on-demand services, as well as international telecommunication, broadband, and other related services. A former government-sanctioned monopoly, it commands 75% market share and sports industry-leading margins.

They privatized in 1998 and spun-out as a public company in 2004. The company returned double-digit ROC for the last ten years while paying a 4% annual dividend. This slow-grower has a strong balance sheet with 33x FFO Interest Coverage and 18% total debt to equity.

In 2020 Saudi Telecom generated $3.4B in EBIT on $15.7B in revenue. In other words, for ~18x current EBIT you can buy Saudi Arabia’s largest, monopoly-like telecom company while getting a 4% dividend yield backed by a strong balance sheet. The company is first in revenue, net income, and EPS for GCC (Gulf Coast Council) telecom providers.

The True Cable/Telco Leader in KSA

Saudi Telecom (STC) is the clear telecom leader in the KSA (Kingdom of Saudi Arabia). Here are a few data points to convince you:

- #1 in Mobile & Fixed Broadband Subscribers

- #1 in Fixed Telephony Subscribers

- #1 in Postpaid & Prepaid subscribers

The company also laid 217K KM of fiber optic cables.

If that wasn’t enough, in 2020 Saudi Telecom won the best mobile coverage award and fastest 5G and mobile network award by Speedtest.

Along with their fiber optic cable density, the company owns 3,000 of KSA’s 7,000 5G cell towers.

Saudi Telecom’s Competitive Advantages

Cable/telco businesses are capital intensive and boast high regulatory barriers to entry. It costs a lot of money to lay cable and build/buy cell towers. Saudi Telecom has three main competitive advantages against its peers:

- Financial

- Geographic/Infrastructure

- Government

Let’s break these down.

Financial

STC commands 74% market share by revenue in Saudi Arabia. The company generates ~20% EBIT margins on those revenues, giving it the largest operating income in the country. This allows STC to invest in growth opportunities like new cell towers, 5G technology, or more fiber optic cable.

An example of growth projects includes STC’s AFrica1 cable initiative. Africa1 will connect numerous African countries with 36TB per second speeds across 12 countries in the MENA.

Geographic / Infrastructure

Telecom providers benefit from NIMBYism (Not In My Backyard). This means if you build one cell tower at location X, there’s no need to build another one at location X.

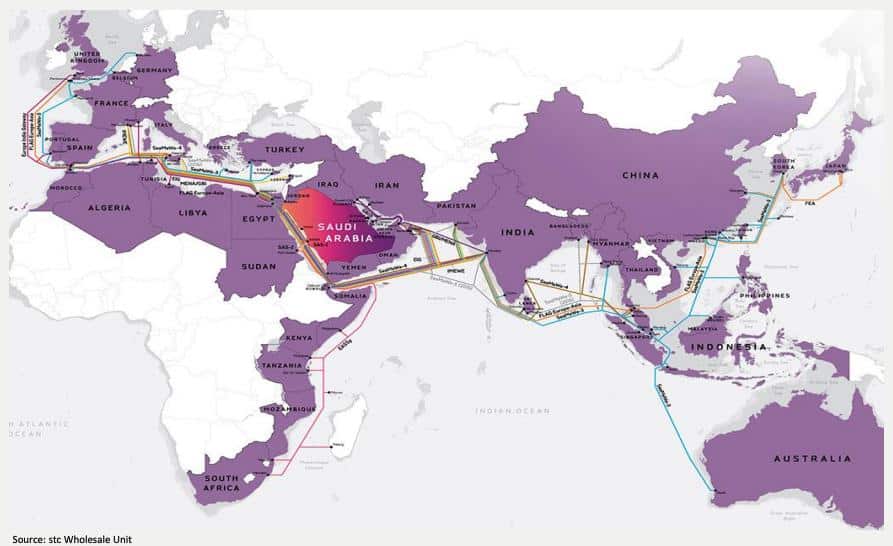

Knowing this, we can better understand the tremendous geographic advantage STC has over its competition. It owns the largest fixed-line (read: NIMBY) network in Saudi Arabia. It also sports a comprehensive cross-border network serving all MENA (the Middle East & North Africa) operators. We also can’t forget the 3,000 5G cell towers throughout the country.

STC has a 25-year history as the leading/largest cable network throughout the MENA region. Check out the photo below to understand the size of STC’s cable assets:

Another way to view STC’s cable dominance is via internet traffic volume. For example, the company runs >90% of Saudi Arabia’s internet traffic volume and data.

Government

This competitive advantage is (mostly) unique to Saudi Arabia. The Saudi government owns ~70% of the company’s shares. On one hand, this is a risk. Should the Saudi government need quick cash, what’s stopping them from dumping their shares?

On the other hand, this is a strategic advantage. Saudi Telecom is a national “flagship” company for the country. It’s a significant contributor to non-oil GDP and employment.

There’s a clear incentive for the Saudi government to not only keep their shares but do everything they can to maintain and grow the business. Doing this keeps STC’s status as a flagship business and the Saudi government continues to diversify its earnings away from pure-play O&G.

Back-out the Saudi government stake and there’s ~30% float available to investors. Of that 30%, foreign investors own a paltry 5.45%

Competitive advantages like the ones discussed above are “obvious” in the sense that you can see them with your eyes. You can see the government ownership, the physical cell towers, and cables. You see the revenue and market cap data against STC’s competitors. But one of the most interesting aspects of STC lies in what you can’t see: culture

Changing The Culture To Change The Company

Dr. Khaled Biyari joined the company in 2013 as Chief Technology Officer and assumed the CEO role in 2015. Biyari had a clear vision for STC’s future when he became CEO: Shift from a less-than-efficient government agency to a thriving, forward-looking private enterprise.

Doing that would require a complete transformation of STC’s culture. So Biyari used McKinsey’s Organizational Health Index (OHI) to score (and track) the company’s progress.

Using 2013 results as its baseline, Biyrai realized the company was one of the worst-performing companies among the 1,000+ companies using the metric. They scored a 33 out of 100. Biyari attributes the poor ranking to the complexity of the telecom industry (emphasis mine):

“When I joined in 2013, the organization was very complex—telecom is complex. People were extremely demotivated because they were not clear on exactly what was going to happen. Some were scared. Many of the top management decided to leave or were let go. There was a bit of a management vacuum. The time between mid-2013 to the latter part of 2014 or early 2015 was a time of changing…a period of stabilization.”

Over the next five years, Biyari transformed the company’s culture, operating metrics, and margins. By 2018 the company scored a whopping 71/100 on the OHI and grew net margins 400bps and operating margins 200bps. ST’s market cap nearly doubled during this time. Part of the transformation meant finding ST’s core values. Biyari asked employees to think of the company’s core values, and a list of 37 emerged. Management filtered the list of 37 to five:

- Customer-first: “We serve our customers passionately—external and internal.”

- Innovation: “I capture the new and deliver it to our markets.”

- Lead with agility: “I am an agile leader who performs in a changing world.”

- Build trust: “I say what I think, do what I say, and do it well.”

- One STC: “We collaborate to deliver STC’s vision.”

In turn, Biyari reimagined ST’s work environment. Management added smaller, open offices, improved break areas, better food, and designated smoking areas.

The culture change worked. Here are a few data points to prove it:

- Market capitalization more than doubled while competitors’ market cap decreased by about 50%.

- Call center service levels increased from 30% to 90%.

- Customer complaints were reduced by 35%.

- Brand value grew from $2.8 billion to $6.2 billion.

Biyari eventually left the company in 2018 to take an Assistant Minister of Defense role for the KSA. Al Nasser, Chief Technology Officer at the time, assumed the role of CEO.

Al Nasser had big shoes to fill. But STC Board Chairman Prince Mohammed Al Faisal has all the confidence that Al Nasser’s ready for the job. Faisal recalled a meeting he had with Al Nasser (emphasis mine):

“In my first meeting with Al Nasser, I was saying to myself, this is a guy who is proactive. He might not have all the skill sets for the job yet, but he has the attitude to build what we need.”

There’s no question the company’s improved since 2013. But Al Nasser isn’t one to rest on his laurels. When asked about company performance benchmarks, Al Nasser didn’t choose other Saudi companies. His benchmarks? Amazon, Apple, and Google. Al Nasser has four main objectives:

- Digitize STC’s operational capabilities

- Accelerate the performance of core assets

- Reinvent the customer experience

- Expand scale and scope

Al Nasser will step down as CEO in March of 2021 for personal reasons.

How STC Makes Money

There are three ways the company makes money: stc, stc Channels, and Other Operating Segments. The stc segment, which provides general telecom services and mobile/broadband communication, generates ~75% of the company’s revenue.

The remaining 25% is stc Channels and Other Operating Segments. stc Channels works in wholesale and retail of smart card services, communications equipment, and computer services. They sell/resell all fixed and mobile telecom services and maintain commercial operations.

Think of ST’s Other Operating Segments like Google’s “Other Bets” segment. The company’s involved in myriad non-core segments that have asymmetric return potential. A few of those investments include:

- Tawal: owning, constructing, operating, leasing, and investing in cell towers

- stc Solutions: cloud computing, IoT, cybersecurity, big data analytics

- Aqalat: property manager for company properties

- stcPAY: digital secure wallet enabling customers to send, receive, spend and manage money simply on their phone. stc pay offers its services in more than 30,000 points of sale in the Kingdom and deals with over 525,000 approved Western Union agents worldwide.

- Saudi Technology Ventures (VC Fund): Independent VC fund with $500M anchored by stc with access to its assets

The company’s using the profits from its core business to fund these digital-first initiatives (stc Pay, stc Solutions, etc.)

What Do You Get For 18x Normalized Earnings?

STC trades for ~18x normalized earnings. Nearly all earnings are from their two segments (stc, and stc Channels). So what do you get for 18x earnings? A few things:

- The largest, monopoly-like telecom provider in Saudi Arabia with expansion into the broader MENA region

- Generating 57% GM, 23% EBIT margins and ~20% net income margins

- Ten years of 14-18% ROC

- A fortress balance sheet with ample interest coverage

This doesn’t include the company’s “Other” business segments, which we get for free at 18x earnings.

While 18x earnings don’t scream cheap, it’s important to note the shareholder returns ST investors have generated over the last five years:

- 1YR: 10.16%

- 2YR: 21.60%

- 3YR: 11.54%

- 4YR: 10.58%

- 5YR: 8.75%

Here are the 1, 3, and 5 year annualized returns if you include reinvested dividends:

- 1YR: 16.33%

- 3YR: 17.62%

- 5YR: 15.15%

Not bad.

Risks & Concluding Thoughts

There are lots of ways we can lose with this investment. First, the Saudi government could dump their shares. Worse, they could favor another telecom company and push for that competitor to gain market share. Second, STC could repeat their history of poor acquisition growth and burn capital which lowers ROC. Third, STC has quite the CEO carousel. The company’s changed CEO’s three times in the last eight years.

Despite these risks, STC is a dominant monopoly business trading below 20x earnings. The company boasts three massive competitive advantages (financial, geographic/infrastructure, and governmental) allowing it to generate industry-leading margins and profits.

Investors can buy this business without paying for its “Other Bets” whose value is greater than $0. Wrap that up in a 4% dividend yield and you’ve got the makings of a long-term portfolio stalwart.