Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Special Event —

Special Event Trailer — Tyler will be hosting a special event next Wednesday, December 27th at 8PM EST. He’ll be talking about how we used a multi-strategy mindset to earn 40% returns with only a 4% drawdown. He’s also going to show you how to deal with the 2 most common trading frustrations.

Make sure to watch the trailer above and register for the event! You won’t want to miss it.

Recent Articles/Videos —

2017 Performance Review — Detailed results of how our portfolio performed this year. You won’t see many trading websites do this. Check it out!

Reflexivity — AK made a great video explaining George Soros’ theory of reflexivity through the examples of Jeff Bezos and Dwayne “The Rock” Johnson. You can check it out below:

We also recently created a Fallible Facebook page. Be sure to go like it here. We’ll be posting and discussing various topics on that page.

Articles I’m reading —

The WSJ did a comprehensive write-up on how the recently passed tax reform will impact each industry group. Here’s the link, it’s worth scrolling through.

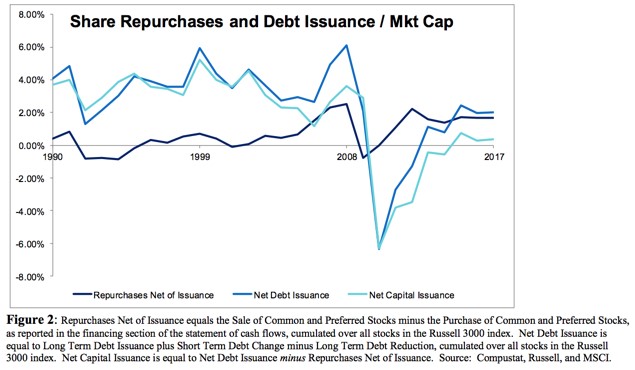

Cliff Asness and team over at AQR put out an interesting paper looking into the validity behind the popular criticisms of corporate America’s so-called “buyback binge”. Not surprisingly, they find there’s not much, if any, evidence to support this pessimistic take. The paper’s worth a read (link here). Here’s a summary of its concluding remarks.

The popular press is replete with commentary seeking to damn the behavior of corporate managers in handing free cash flow back into the hands of shareholders. Investment professionals have even been heard to comment on the profligate use of free cash flow when it is used to buy back common shares. These criticisms are often, even regularly, without merit (at least merit that can be demonstrated), sometimes glaringly so. Whilst there is always the possibility for agency issues to create incentives for corporate managers to engage in sub-optimal share repurchase decisions, we feel that in aggregate share repurchase activity is far less nefarious than the popular press would lead you to believe. In fact there is at least as much “agency theory” arguing that paying back free cash flow is a positive as there is that it’s a negative. Aggregate share repurchase activity has not been at historical highs when measured properly, and when netted against debt issuance is almost a non-event, does not mechanically create earnings (EPS) growth, does not stifle aggregate investment activity, and has not been the primary cause for recent stock market strength. These myths should be discarded.

And for those of you who are of a real wonkish bent, NBER put out a beast of a paper titled The Rate of Return On Everything, 1870-2015. It gives a great breakdown of the total returns for all the major asset classes covering 16 advanced economies over a 135 year period. One of the more interesting takeaways is that housing has shown similar long run returns to equities but with less volatility on a national level. Here’s the link.

Urban Carmel, writing at his blog The Fat Pitch, put out a must-read piece last Friday detailing his thoughts on what’s to come in 2018. I’m a big fan of Urban and his data driven BS fluff free take on market action. He sums up the article saying.

US stocks will likely rise in 2018. Earnings growth, investor sentiment and valuation suggest that mid-single digit appreciation is a reasonable expectation, but the truth is wild cards, especially investor psychology, could push returns much higher (or lower). A bear market is possible, but unlikely. An intra-year drawdown of 10% (even a 14%) is odds-on; it will feel like the end of the bull market when it happens.

I concur. Here’s the link.

The whole blockchain/crypto orgy has officially gone full retard. Penny stock companies are adding blockchain to their names and rising 1,500% overnight, totally validating Fama’s theory of efficient markets.

This Bloomberg article covers these new ‘innovators’ of the blockchain-gig-social-mobile economy. Companies from reverse bra makers to juicers and furniture makers are pivoting to the blockchain and getting in on the ground floor of this amazing technological revolution!

Video I’m watching —

Value investor David Einhorn did a Q&A as part of the Oxford Unions speaker series. He talks about how he got started in the game and built up his fund, Greenlight Capital. As well as what it takes to be a great investor and where he thinks the market and economy are today. He’s a smart and thoughtful guy and the video is worth a watch (link here).

Book I’m reading —

This week I read Long-term Front-running by Michael Fritzell. You can find Michael on twitter under the handle @Fritz844. He’s a good follow and also writes a great markets/trading blog called Fritz Capital.

I really enjoyed this book. It’s a quick read (only 88 pages) and it covers the nuts and bolts of Michael’s trading framework as well as touch on some market theory.

Here’s an excerpt from the chapter How to understand what is priced in:

Next-year consensus estimates for sell-side tend to be too bullish in the order of 5-10%. So in order to gauge true investor expectations you may want to scale down consensus numbers somewhat.

Well-publicized facts about the company are almost always priced in. If the average investor and analyst know about the fact, then it is probably priced in. If you think people’s first instinct is to go long (or short) a particular stock, the investor community is probably biased on the upside (downside).

A trick to get a sense of the overall level of bullishness is to ask who the burden of proof is on. If you pitch an idea, do other investors take your side immediately, or do they require evidence that your view is correct? If the answer is the latter, you idea is probably off-consensus.

What sell-side analysts typically do is to assume that current growth rates continue for a few years and then converge to long-term GDP growth. Analysts rarely expect earnings to go to zero, or for growth to continue for multiple decades. That’s why it often makes sense to bet on growth companies and bet against companies in decline.

A word of caution: Just because a PE ratio is low, does not necessarily mean that earnings expectations are too low. And just because people are expressing negative views about a company, doesn’t necessarily mean that estimates are too low. You will have to dig deeper into estimates.

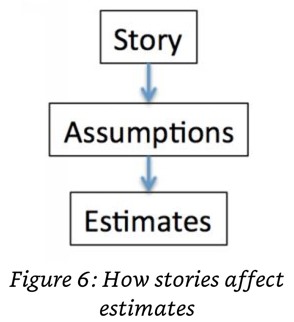

A story about a new exciting product for example, will be reflected in a set of assumptions that go into analyst models. By putting them into a DCF model they in turn affect earnings estimates. Does the story about the success of a product make sense, do the assumptions make sense and does their impact on earnings estimates make sense?

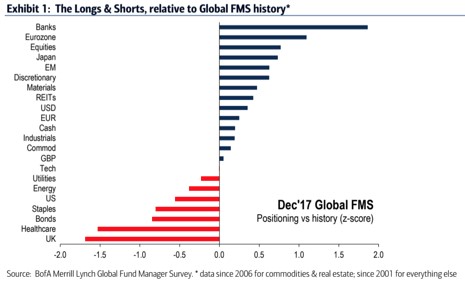

Chart(s) I’m looking at —

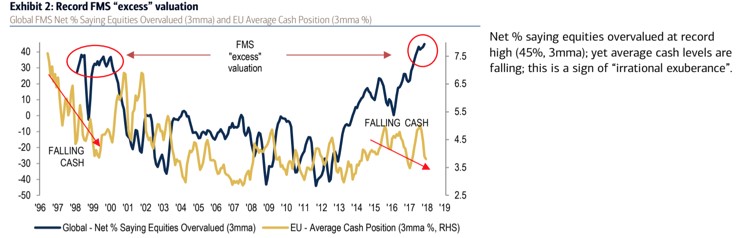

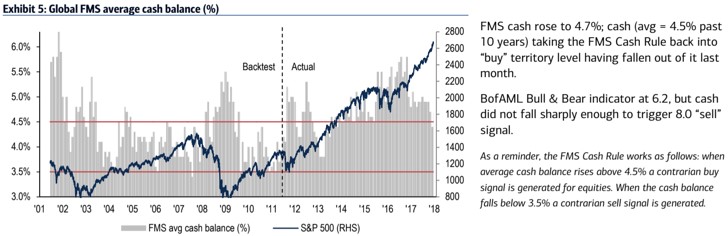

BofA’s latest fund manager survey is out. Here’s a few charts of note.

Growing signs of ‘exuberance’ but cash levels are still pretty high. And energy is still on manager’s sh*t list which is coincidentally one of my favorite sectors going into 18’.

Trade I’m looking at —

Long Criteo (CRTO). I came across this trade from Fritzell’s blog (you can read the post here) and have started digging into it and like what I see so far.

Here’s a summary of Fritzell’s long thesis.

Criteo is an ad-tech company that buys ad inventory from Google and Facebook and offers customers performance-based, targeted ads. The moat is possesses comes from network effects: it sits on a treasure trove of data, which helps explain why its click-through rates are 4x the industry average. Customer retention rates are 90% and ROI for customers is very high. The reason the stock is down is because of third-party cookie restriction in iOS 11 (potential impact of 7-10% of revenues). I consider this to be a one-off – with still-positive growth to be expected in 2018. I am comfortable with the risk of ad blockers, for the following reasons: 1) tough privacy restrictions in Safari is nothing new, in fact Criteo’s competitor AdRoll expects almost zero impact on its business thanks to work-arounds 2) publishers already adjust their impressions based on the percentage of users using ad blockers anyway 3) advertisers usually find ways around ad blockers and 4) ad blockers don’t work in apps, which is where time is increasingly being spent. Ad fraud may be common across the industry, but customer retention rates are high and ad performance is easily measurable through ComScore data. Much of the negative news should be priced in at this point with the stock down 42% from the peak and short-sellers doing victory laps. The stock is relatively inexpensive given the underlying overall 20-25% growth momentum in the digital advertising market in my view, and will continue to grow on a secular basis.

Fritzelll was early with his call and underestimated the impact to revenues from apple’s third-party cookie restrictions in iOS 11 (the company came out with guidance for a 22% not 7-10% hit to revs). The stock is down 30+% on the news. But from my digging so far this doesn’t appear to be game changing news for the company’s future. And now the market seems to be offering up a wide moated growth company, in a strong secular growth industry, for a discount (it’s trading at just 0.8x sales).

I don’t know. I’ve got to dig a bunch a more. I’ve lost a lot of fingers over the years catching knives (I can’t seem to help myself) so do your own diligence.

Quote I’m pondering —

Here’s two quotes/excerpts that I’ve been thinking about lately.

The only analytic tool that mattered was an intellectually advantage disparate view ~ Michael Steinhardt

According to Buddhism, the root of suffering is neither the feeling of pain nor of sadness nor even of meaninglessness. Rather, the real root of suffering is this never-ending and pointless pursuit of ephemeral feelings, which causes us to be in a constant state of tension, restlessness and dissatisfaction. Due to this pursuit, the mind is never satisfied. Even when experiencing pleasure, it is not content, because it fears this feeling might soon disappear, and craves that this feeling should stay and intensify. People are liberated from suffering not when they experience this or that fleeting pleasure, but rather when they understand the impermanent nature of all their feelings, and stop craving them. This is the aim of Buddhist meditation practices. In meditation, you are supposed to closely observe your mind and body, witness the ceaseless arising and passing of all your feelings, and realise how pointless it is to pursue them. When the pursuit stops, the mind becomes very relaxed, clear and satisfied. All kinds of feelings go on arising and passing – joy, anger, boredom, lust – but once you stop craving particular feelings, you can just accept them for what they are. You live in the present moment instead of fantasising about what might have been. The resulting serenity is so profound that those who spend their lives in the frenzied pursuit of pleasant feelings can hardly imagine it. It is like a man standing for decades on the seashore, embracing certain ‘good’ waves and trying to prevent them from disintegrating, while simultaneously pushing back ‘bad’ waves to prevent them from getting near him. Day in, day out, the man stands on the beach, driving himself crazy with this fruitless exercise. Eventually, he sits down on the sand and just allows the waves to come and go as they please. How peaceful! ~ Yuval Harari, Sapiens: A Brief History of Humankind

I hope you all have a fantastic holidays and get to spend it with the people you love, eating good food, drinking the good stuff, reflecting on the year that’s passed, and getting excited about the year ahead.

Thanks for being a reader, it’s a real pleasure getting to share our work with you.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I posts my mindless drivel there daily.

And if you’d like to discuss macro with the rest of the Operator community, check out our Global Macro Facebook group by clicking here.

Cheers!

Your Macro Operator,

Alex