Business Description: RDVT’s platform (CORE™) stores 1+ trillion data records on nearly every individual in the US. Their data sources include MVA, property, criminal, court, and employee records. The proprietary, cloud-based platform funnels all the records into one, easy-to-query database. RDVT uses this technology in two products: idiCORE (risk management, debt recovery, fraud detection) and FOREWARN (individual background checks catered to realty professionals, see our homebuilding thesis here).

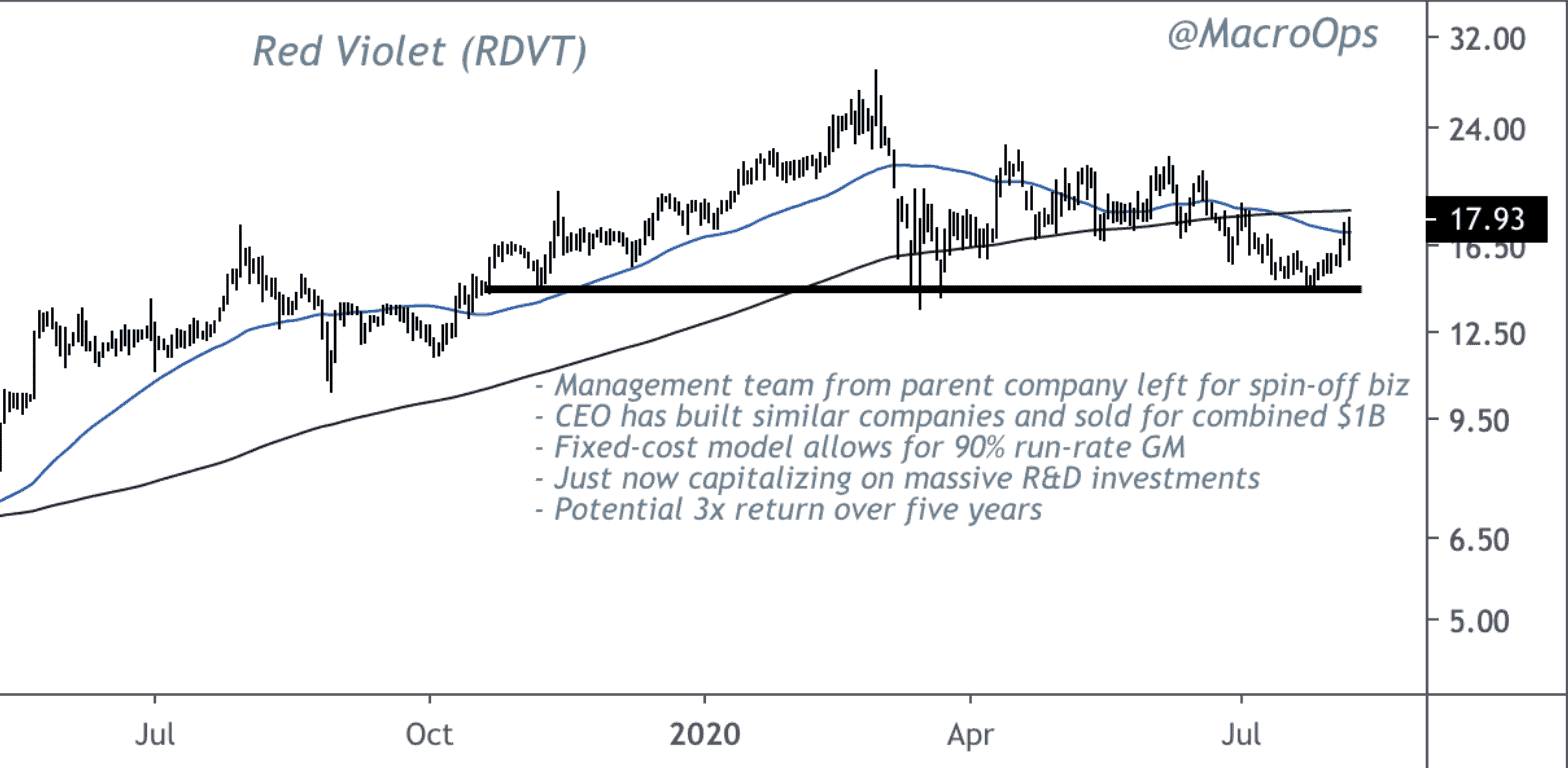

Thesis: RDVT is a fast-growing, highly scalable data fusion company delivering 1+ trillion points of data to its customers at lightning speed. Their platform allows customers to assess risk and achieve a full-scale picture of any individual and business before meeting/conducting a deal. The company sports a fixed-cost model with 90% incremental gross margins. Management has a history of building similar companies, with two sales totaling $1B in the same industry. We believe the company can reach $190M in 2024 revenue with 40% EBITDA margins, giving us nearly 300% upside from current prices.

History & Spin-off: The current RDVT team began developing the CORE platform in 2014 under the name “The Best One” (TBO). TBO received an investment from Phil Frost, changed its name to Cogint and listed it as a public company (under ticker CGNT). In 2018, the company merged with Fluent under the ticker FLNT. That same year FLNT decided to spin-out the CORE platform company (TBO/CGNT). Here’s what’s interesting: every single executive left TBO/CGNT to work at the newly spun-off company, Red Violet (RDVT).

Fixed-Cost Model: The most attractive aspect of the RDVT thesis is their fixed-cost business model. In short, they pay a fixed, long-term contract on their data feed. It doesn’t matter if they generate $10M in revenue or $100M. Their cost remains fixed. This allows the company to reach 90% steady-state gross margins and near 100% incremental GM. As the business scales, they won’t have to spend as much on SG&A. This ramps up EBIT margins (in some estimates, reaches 40%).

History of Value Creation: Dan Dubner and his executives were the early founders of the data fusion industry. They’ve built two companies like RDVT that sold for a combined $1B. RDVT is a spin-off of all the things that weren’t great in prior iterations of such data fusion technologies. We have a strong belief that management knows how to build, how to price and how to create value for shareholders. They own 20% of the company so incentives are aligned.

Valuation: We’re assuming 45% annual top-line growth over the next five years — starting with $50M in 2020 revenue. At scale the company generates 90% GM and 40% EBITDA margins (based on their two previously sold companies). Given our assumptions, we end 2024 with $190M in revenues, $76M in EBITDA and $55M in FCF. Add back our $9M in net cash and we get a market cap of $578M ($50/share). If we assume a 17x exit EBITDA multiple (in line with historical sales), we get $700M in market cap ($62/share). That’s near 3x upside.

Risks: Data supplier concentration (receives 43% of its data from one provider), competing away margins, litigation risk from competitors (CEO is lawyer by trade), Data price increase leads to reduced margins.

***Disclosure: We currently have a position in RDVT at the time of this release***