“It is wise to take admissions of uncertainty seriously,” Daniel Kahneman noted, “but declarations of high confidence mainly tell you that an individual has constructed a coherent story in his mind, not necessarily that the story is true.” ~ via the book Superforecasting

Summary: Hey gang. Apologies for the absence of myself and the Dozen. I was dying from malaria for a bit, but now I’m firmly in recovery and looking forward to getting back at it. Expect more writing and communication from me over the coming weeks as I continue to get my strength back. Alright, quick summary… breadth good/neutral, internals good/neutral, liquidity good = market consolidating or setting up for a small shakeout at worst. Treat this as a buying opp (unless some insane AND meaningful policy/geopol stuff happens). No recession this year, just a muddle through, which should be good for risk. USD bear narrative and positioning have gotten crowded. We’re looking for a fade.

Alright, let’s get to it.

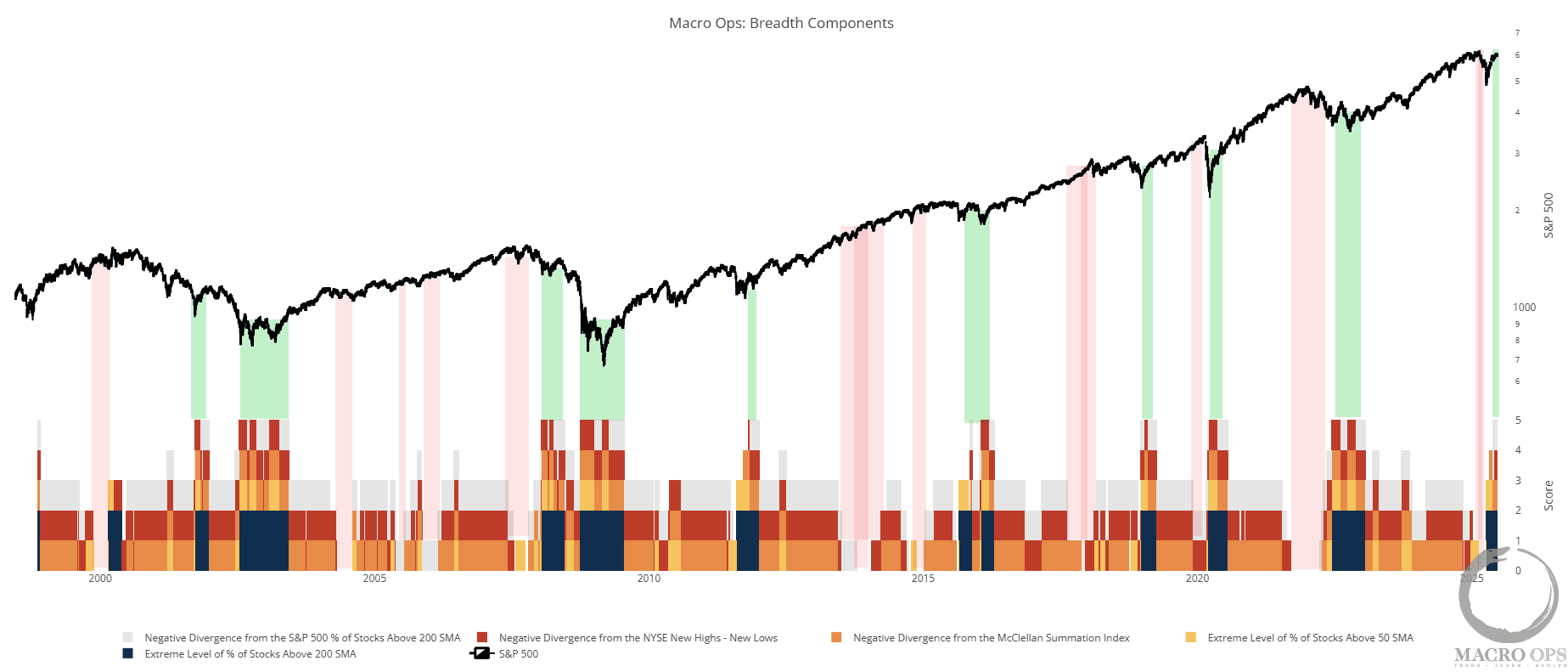

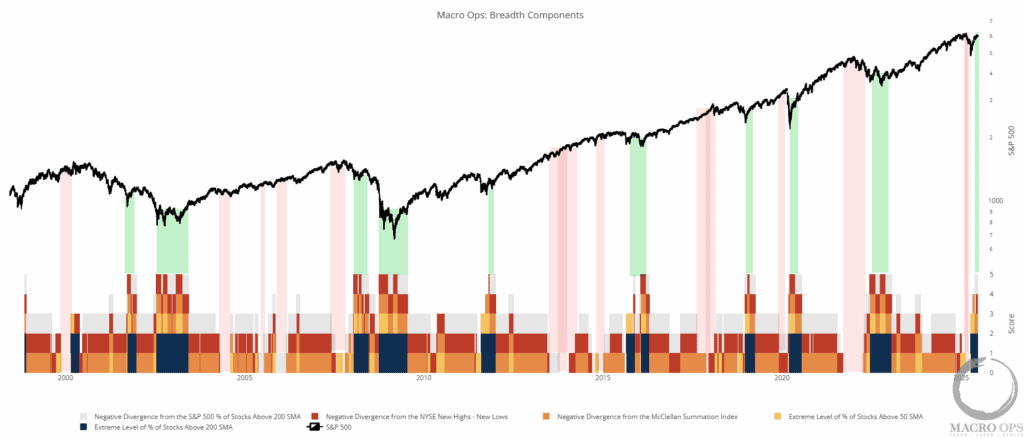

1. Our aggregate breadth indicator, which measures the direction and intensity of various breadth measures, is giving a reading of 5 (other instances highlighted in green). This is a positive sign often seen at the start of larger trends (though, of course, not always, see false signal during the bear market of 01’ and 08’). But we’re not in a bear market, we’re in an uptrend, which gives more weight to the measure. The red highlighted areas mark readings of 1 or lower.

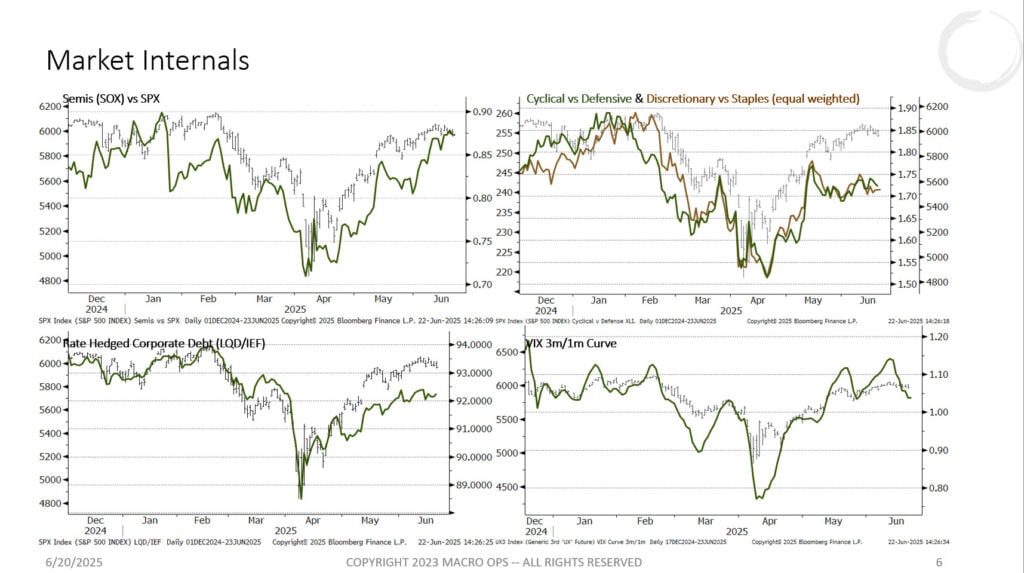

2. Our market internals are either positive confirming, or neutral. The sideways action we’re seeing in Cyc v Def and Disc v Stap often precedes a consolidation period or a brief shakout, which would be normal and healthy after the run we’ve seen over the past 3m+. But this is not what you see prior to a larger selloff or turn in the market.

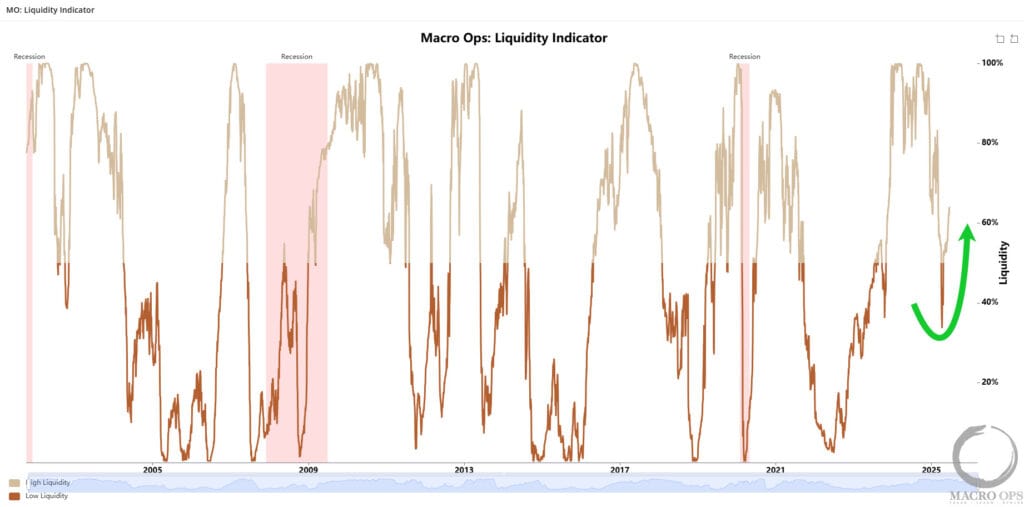

3. Backing up the above, the MO liquidity indicator is in positive territory and rising with a reading currently at 64%. This tends to provide a positive backdrop for risk assets.

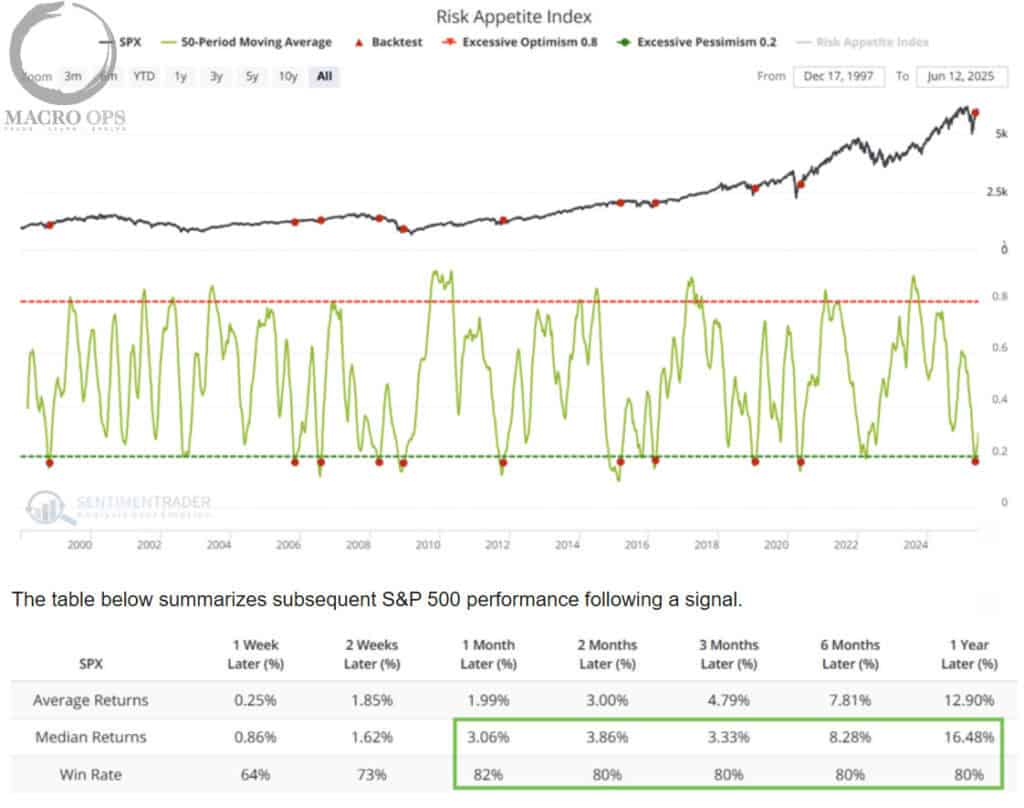

4. SentimenTrader’s Risk Appetite Index recently triggered a positive signal as well. Win rates and median returns on the table below.

5. But what about the Trade War and the incoming recession? Let’s talk about that… Our base case at MO is that the US is aiming for strategic decoupling from China. However, Trump also doesn’t want to rock the boat too quickly, which is why there’s so much talk of TACO right now. Now there’s the foreign war he’s gotten himself involved in. That costs political capital, and it takes up time. This all means that the US-China talks are likely to take some time, and neither party seems eager to escalate things right now.

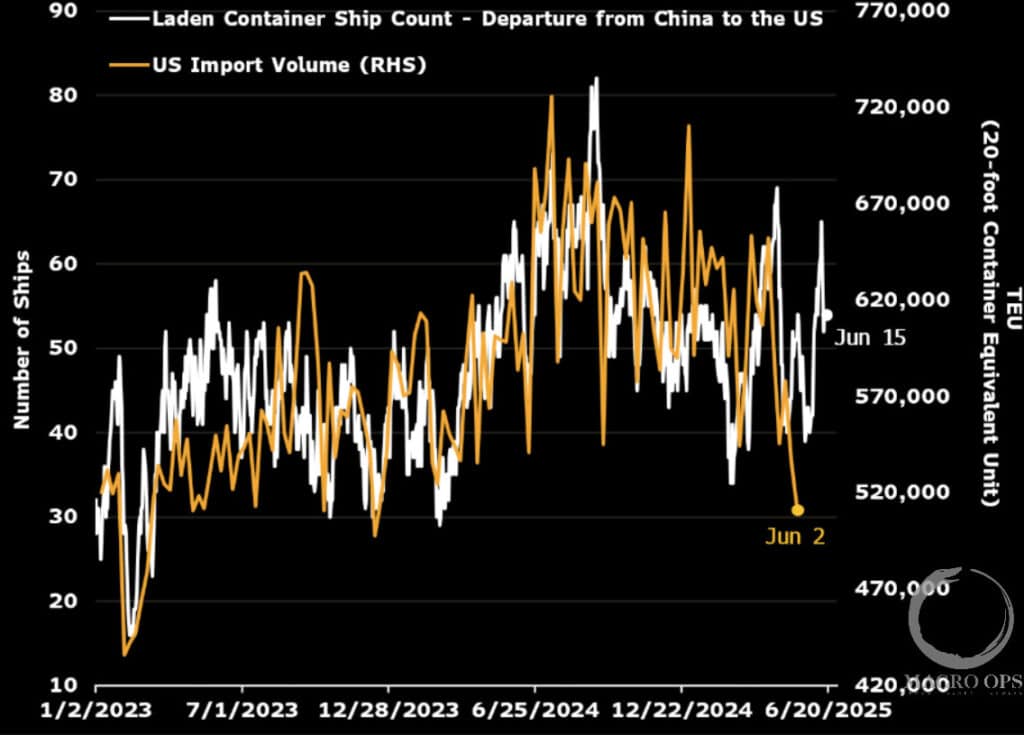

This from BBG shows that US-China trade is already starting to rebound significantly. BBG notes “Ships are sailing from China and US shelves are filling… container traffic from China is back on the move, with year-to-date import volumes on pace to exceed normal levels at least through summer.”

So much for the “empty shelves” scare narrative. This is also positive for inflation as overstocking is now a risk, meaning there’s a good chance we’ll see price reductions as we progress further into the second half of the year.

6. Our base case is that the US economy muddles through this year. Inflation is coming down, the Fed should start cutting this summer. Consumers are still spending, and we’re seeing an acceleration in bank lending, which will show up in growth with a lag.

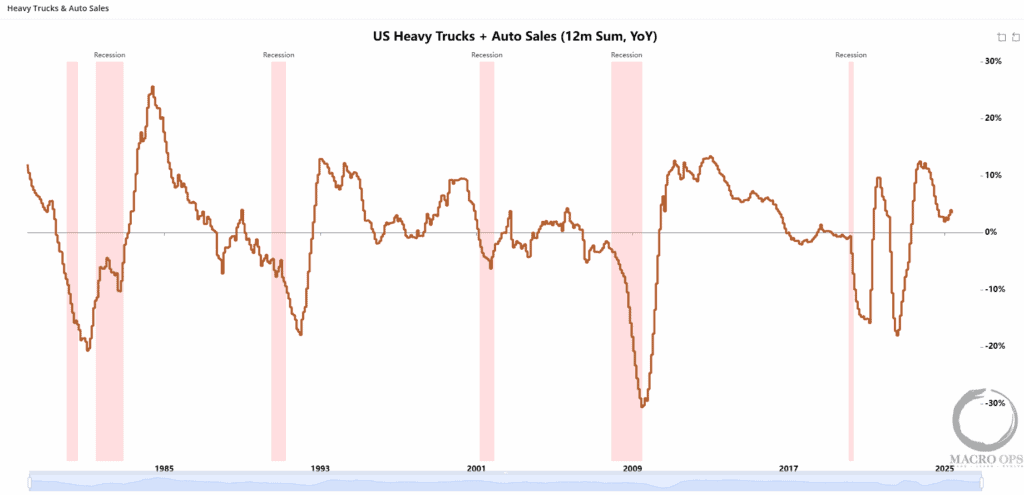

So recession this year? One of our favorite recession indicators, which is US heavy trucks and auto sales year-over-year, says no.

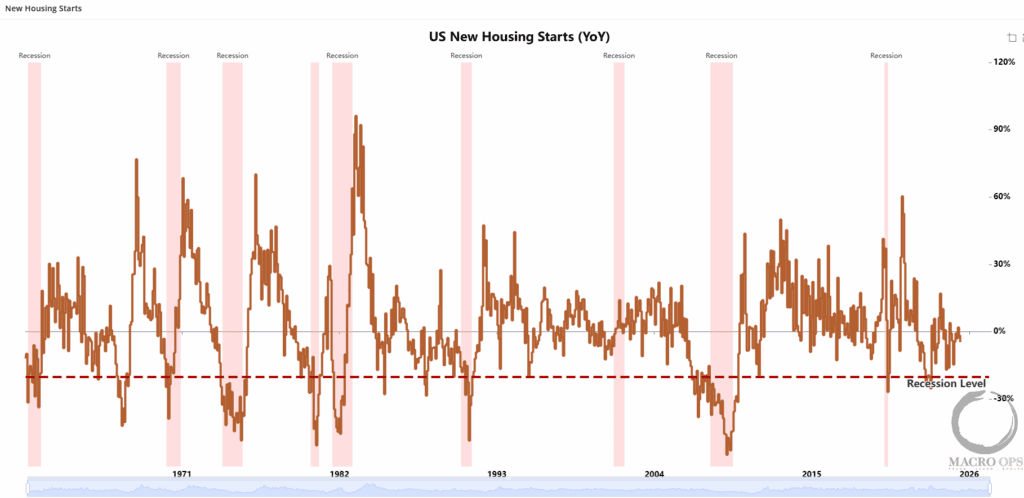

7. And while housing continues to slow, it’s still far from levels that signal recession.

8. The labor market is indeed slowing, but it’s also definitely not cracking… Here’s one of our favorite labor market indicators. It shows monthly hiring in the most cyclical sectors of the economy. It’s rebounded from last year’s low and is trending sideways. This is not a sign of an imminent recession.

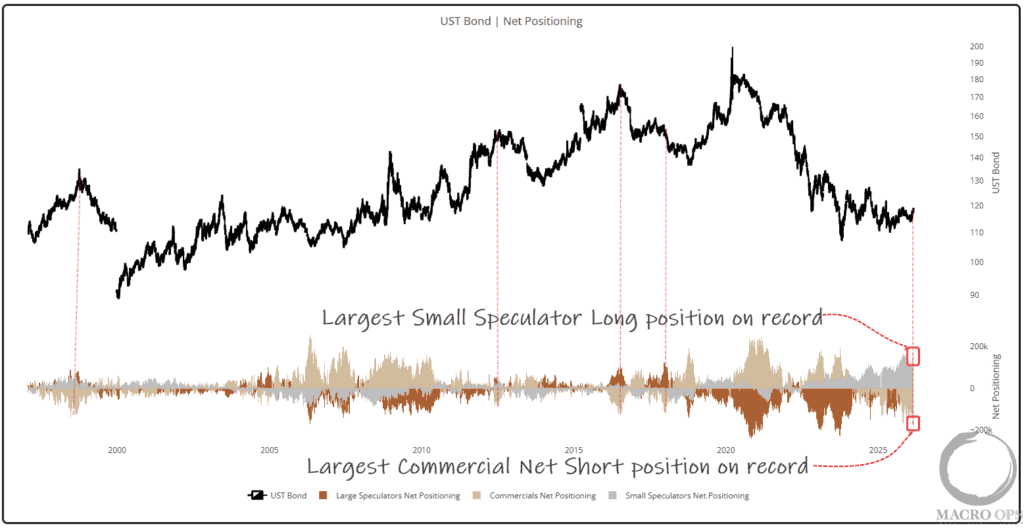

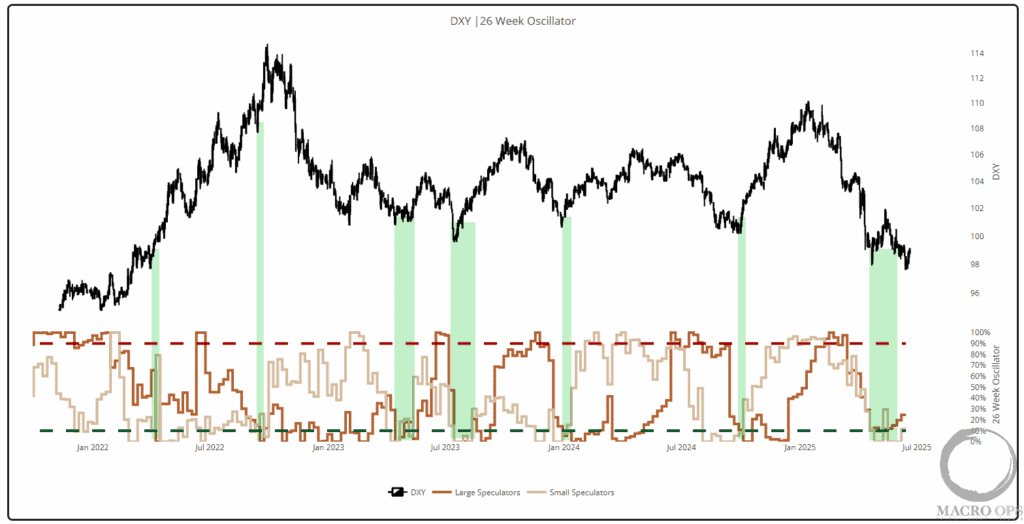

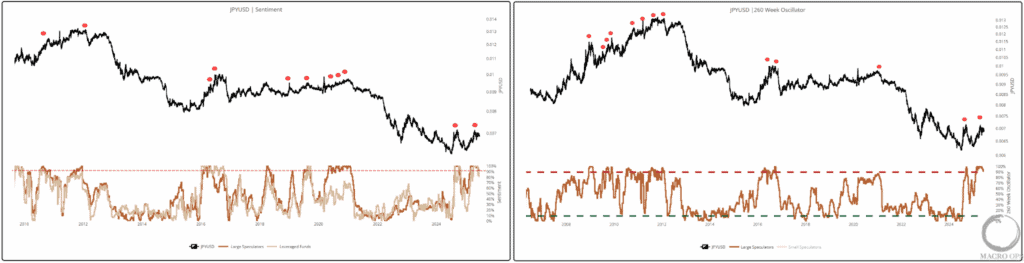

9. Alright, here’s some trades I’m looking at… So we’ve been short USD against several pairs for the past couple months. But we’re going to start taking some profits on those names as I’m looking for a potential reversal here. Large and small spec positioning is very bearish on a 26-week oscillator basis.

10. I’m considering getting long USDJPY since JPY has the most crowded positioning and sentiment, according to our indicators. It’s also reversing off a 24m+ significant level. We likely see some mean reversion in this pair with a move back to its monthly BB midline or above.

11. Here’s its Sentiment and Positioning. Red dots mark extreme readings.

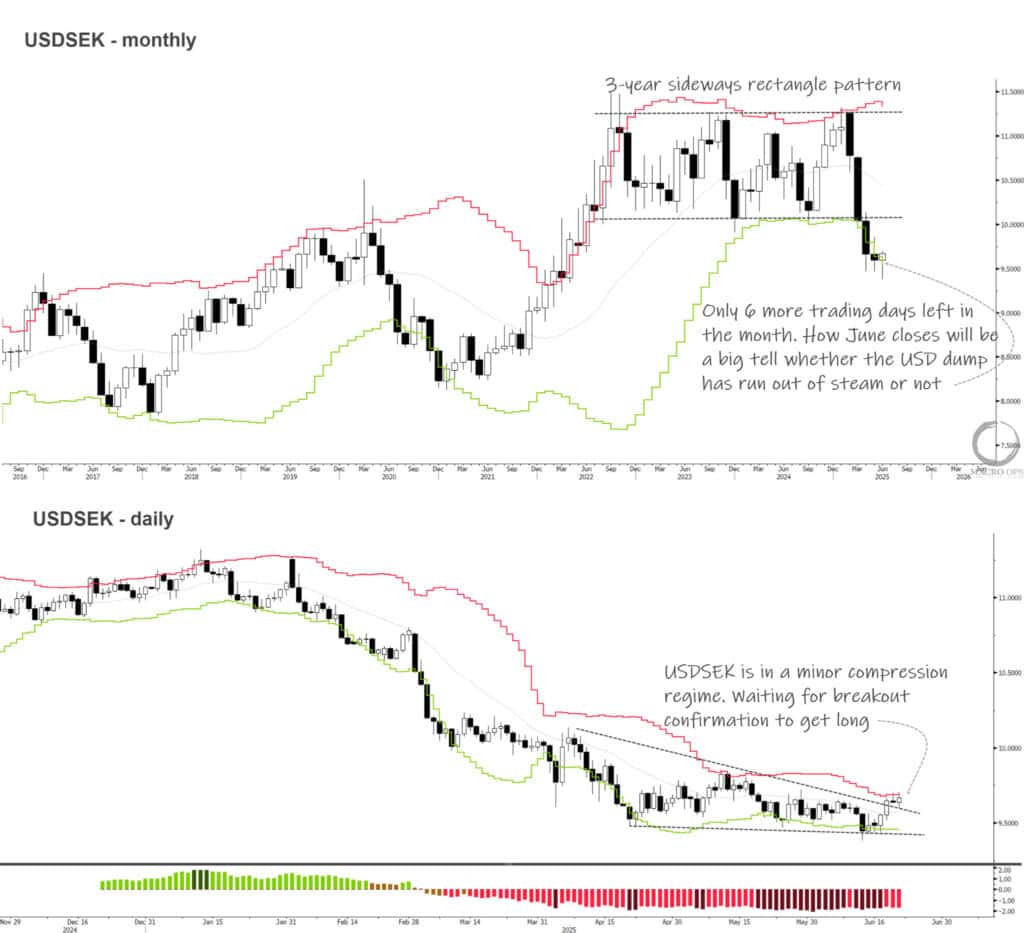

12. Long USDSEK is another pair I’m tracking. It’s in a minor compression regime and is six trading days away from putting in a bullish monthly reversal bar.

Join The Collective

Thanks for reading.