Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

China VS Russia & Japan — Is China headed for the same disaster both Russia and Japan experienced? Make sure you subscribe to Fallible to follow our latest series on China’s downfall!

Why Emerging Markets Are A Dead Money Trade — Find out why Alex thinks it’s too early to buy the EM dip.

Articles I’m reading —

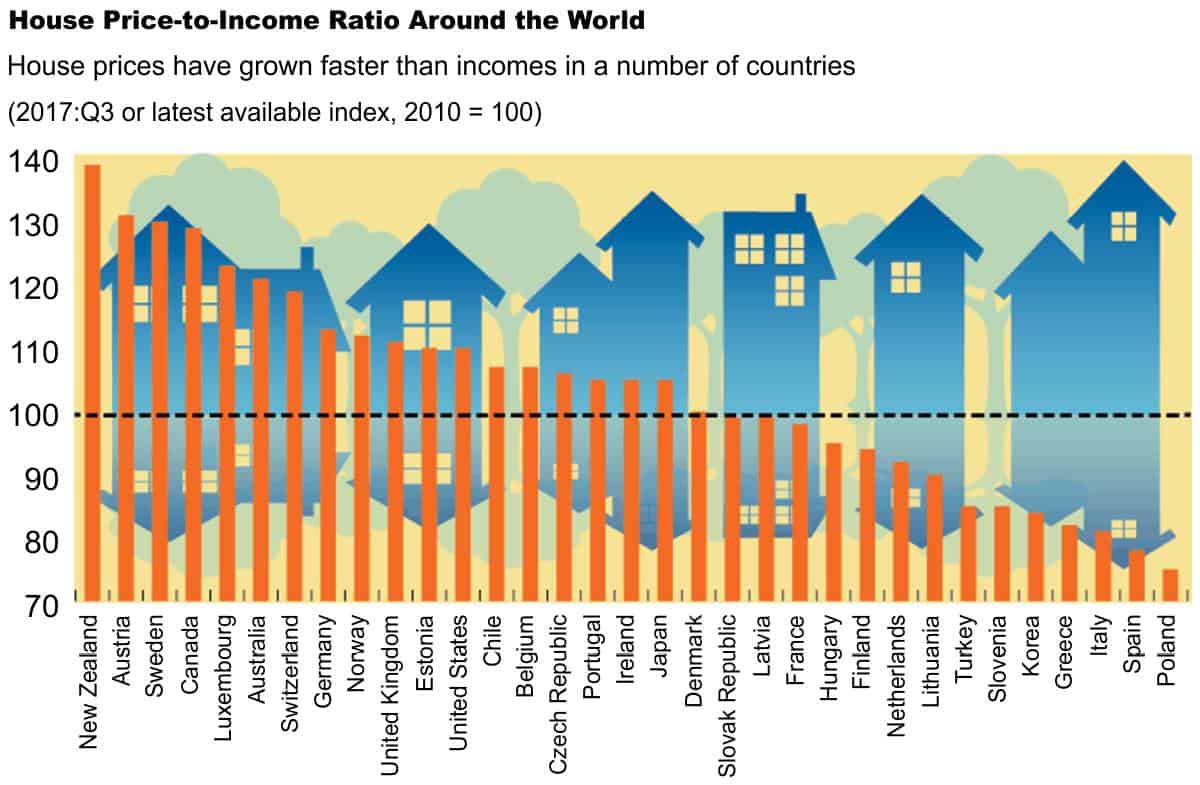

I’ve been digging into global housing markets lately. It’s a sub-thematic of the two most important macro drivers of the current market, which are (1) the market’s continual underpricing of the Fed’s rate path and (2) the slow and quiet Chinese deleveraging.

13-D Research recently shared some of their work on the subject where they discuss how whacky things have become in select metros around the world. Here’s a snippet (emphasis by me).

In Vancouver, home and condominium prices are up roughly 60% in just the past three years. In Sydney, house prices jumped over 80% between the end of 2009 and the peak last September. And in Toronto, Stockholm, Munich, London, and Hong Kong, housing rose by 50% on average since 2011. As the IMF writes: “In recent years, the simultaneous growth in house prices in many countries and cities located in advanced and emerging market economies parallels the coordinated run-up seen before the crisis.”

…In its annual housing report released last September, UBS concluded: “The risk of a real estate bubble in top global cities has increased significantly in the past five years.” The role foreign and institutional money has played in escalating home prices beyond the spending power of the local population was at the heart of the Swiss bank’s concern.

In Hong Kong, it now requires 19.4 times the average salary of a resident to buy a home, up from 4.6 times in 2002. In London, the equivalent price-to-income multiple today is at 16 times. Paris, Singapore, New York, and Tokyo all have multiples greater than 10. The IMF has charted the escalating divergence of real estate and income appreciation globally since 2010.

I’ve tried to not focus on real estate this cycle because it feels too much like ‘fighting the last war’. But nonetheless, I think there may finally be actionable trades to be made off this theme as global liquidity continues to tighten. Here’s the link to the 13-D piece.

Ray Dalio (warning: there’s lot’s of Dalio in this week’s Musings) shared a short writeup on Linkedin this week, where he updates his views on where we are in the current cycle. Ray makes an important point about how longer bull markets tend to follow deeper contractions, like the one we just experienced in the GFC. He thinks we have a “couple more years left” in the current one, which I agree with. Here’s an excerpt and the link.

To reiterate where we stand now, a) the short-term debt cycles (also called business cycles) of most developed countries are in the 6th or 7th innings so they are not near their contraction phases. These expansions typically go on about 7-8 years (plus or minus a few years) with the longer ones coming when there is a lot of slack due to the last contraction being a deep one and when growth has been slow. Since the last one was deep, growth has been relatively slow, and debt growth is not high relative to income growth, and since capacity constraints that now exist are not leading to dangerously high inflation and fast tightening, it looks to me that we have a couple more years left in this cycle’s expansion.

And lastly, Institutional Investor did a great profile on famed short seller, Jim Chanos, that’s worth a read. Apparently, his Kynikos Capital Partners fund, which runs a 190% long and 90% short strategy, has returned a net annualized gain of 28.6% since inception in 1985. Those are Soros/Druck type numbers. Here’s the link.

Chart I’m looking at —

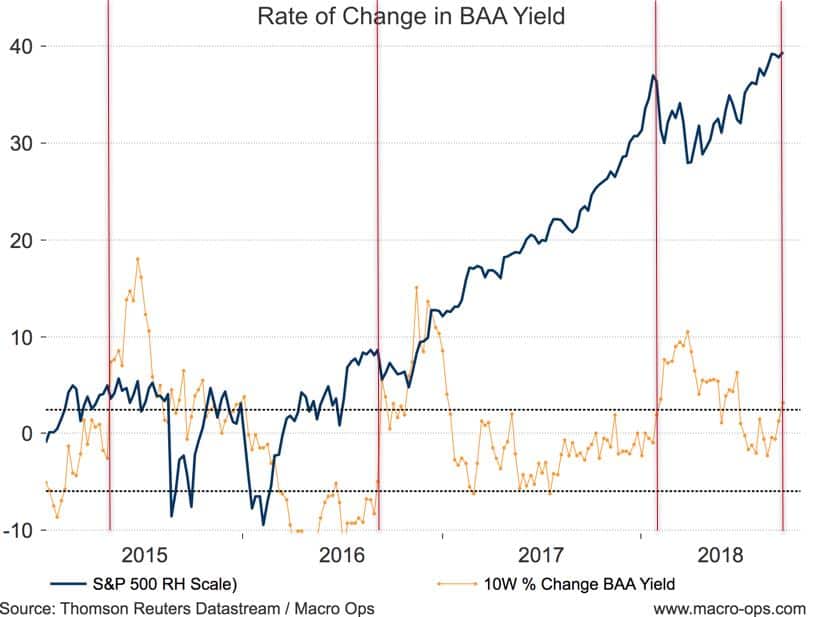

I remain bullish on US stocks but the high positive rate of change in yields recently, makes me cautious over the short-term (next 1-4 weeks). Stocks and bonds compete for capital flows and fast rising bond yields pull demand from stocks and back into bonds. My BAA yield ROC chart below shows that yields have picked up quickly enough to warrant caution.

The S&P 500 is also now technically overextended. The weekly chart below shows it’s bumping up against the upper part of its bollinger band. I’m looking for a pullback down to the midrange of the band (red line) which also happens to be right at its trend line. This pullback should be viewed as a buying opportunity.

Video I’m watching —

Ray Dalio has been doing the rounds on the financial news networks the past few weeks promoting his new book (more on that next). Here’s a 15 minute clip of his interview with Bloomberg’s, Erik Schatzker, that’s worth a watch. In it, Ray discusses his debt cycle framework and applies it to emerging markets, and what’s going on in Turkey and Argentina, specifically. It’s worth a watch. Here’s the link.

Book I’m reading —

This week I’m reading Dalio’s new book, A Template for Understanding Big Debt Crises. I’m a little over half way through the it and I’m a little disappointed. That’s not to say the book isn’t good. It is. And at the price of FREE (for the PDF/ebook versions) it’s certainly worth picking up. But if, like myself, you’ve read his previous white paper on the subject — which I think has been taken down from BW’s site — and were hoping for some new major additions, then you’re in for a let down.

With that said, it’s an excellent primer on the subject and an easier read than the original paper. And maybe there’s some new stuff towards the end of the book, we’ll see. I’ll be sharing my book notes with the Collective next week. Here’s a cut on depressions from the book.

Some people mistakenly think that depressions are psychological: that investors move their money from riskier investments to safer ones (e.g., from stocks and high-yield lending to government bonds and cash) because they’re scared, and that the economy will be restored if they can only be coaxed into moving their money back into riskier investments. This is wrong for two reasons: First, contrary to popular belief, the deleveraging dynamic is not primarily psychological. It is mostly driven by the supply and demand of, and the relationships between, credit, money, and goods and services—though psychology of course also does have an effect, especially in regard to the various players’ liquidity positions. Still, if everyone went to sleep and woke up with no memory of what had happened, we would be in the same position, because debtors’ obligations to deliver money would be too large relative to the money they are taking in. The government would still be faced with the same choices that would have the same consequences, and so on.

Trade I’m considering —

I’m considering putting on a big position in Facebook (FB) soon; preferably after we see a broader market correction in the next few weeks which will help reset rates and sentiment a bit. FB stock is currently trading at major support in its 100-week moving average (green line below).

Sentiment has notably shifted on the stock since management reset growth expectations in their last earnings call. I view management’s moves as being smart and strategic, and which should ultimately be beneficial to patient shareholders.

One of my favorite value investors, Jake Rosser of Coho Capital, put out a great write up on FB in his latest Investor Letter. The entire letter is worth a read (he also discusses Disney (DIS), which happens to be our largest stock holding at the moment). Here’s the link and his concluding remarks on FB.

Strong Downside Support with Homerun Potential. The best money to be made on a stock is when there is a sizable gap between future cash flows and anticipation of those cash flows. In Facebook’s case, we think the gap is sizable enough to result in multiples of value creation over the next five years. If we net out Facebook’s $42 billion in cash, as well as its stake in WhatsApp, (since it is not yet profitable –we assume WhatsApp is only worth its acquisition price of $19 billion) then we are recreating core Facebook and Instagram for 18x forward earnings, in-line with the forward earnings multiple for the S&P 500. Not bad for a 30% grower with 35% operating margins (future margin guidance on Q2 earnings call that caused the stock to collapse – still 10% better than Google). This valuation is based upon current Wall Street estimates, which have given little credit to Facebook’s non-nameplate platforms.

You get the optionality of future monetization of Facebook’s messaging apps and home-run potential with Instagram for free. We like the set-up and believe our downside is well-protected. As a result, we have made Facebook our largest position. The steady rise in equity markets has made it more difficult to source stock bargains, but as concentrated investors we only need one or two opportunities a year to make a difference. As students of the world’s best companies we prepare our shopping list well in advance. When volatility strikes, we can act quickly having already spent years (in many cases) researching the companies we purchase. As French Micro-biologist Louis Pasteur once said, “chance favors the prepared mind.”

Quote I’m pondering —

As the story goes, God and the Devil were debating about the goodness of man as they walked down a seldom-used road. While they were arguing about man’s inner nature, they noticed the lonely figure of a man approaching them. Suddenly, the man bent over and picked up a grain of “truth.” “You see,” God exclaimed, “man just discovered ‘truth’ and that proves that he is good.” The Devil replied, “Ah, so he did. But you don’t understand the nature of man. Soon he’ll try to organize it, and then he’ll be mine!” ~ Bennett W. Goodspeed, from his book “The Tao Jones Averages”

I love this little story…

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.