Tyler here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at tyler@macro-ops.com and I’ll share it with the group.

Our June Macro Intelligence Report (MIR) is coming out next week! Alex and I believe that this stock market is about to enter into a blow-off top phase. Big tech stocks could scream another 50%, which means we can take advantage of our DOTM option strategy to place extremely asymmetric bets into year-end. These DOTM plays have the potential to 10x. Sign up now to secure your copy. We have a 60-day money-back guarantee, so there’s literally no risk for you to check out our favorite stocks. Click here and scroll to the bottom of the page to sign up for the MIR.

Recent Articles/Videos —

Misconceptions, Mispricings, And Models, A Look At Today’s Markets – Alex breaks down the current market within the context of his 7 favorite mental models.

Ray Dalio On Meditation — AK uses an interview with Dalio to discuss how meditation can help your trading.

Insane Valuations — What’s the right way to look at the standard valuation metrics used by most investors? AK explains in this video.

The Morality Of Trading — AK dives into this topic with the help of Billions.

Articles I’m reading —

May 31st was a “QT day”. That means the Fed let a bunch of their bonds expire and roll off of their balance sheet. This article from the Macro Tourist explains why there might be an edge in going short stocks on these days.

Back during QE, the market had a tendency to rise on any day that the Fed was buying bonds. Now there’s solid evidence that the opposite happens when these bonds expire. I’m seriously considering adding this trade into my playbook for the year.

I’m also looking at an article Cliff Asness wrote about hedge fund returns. (Link here) The popular narrative these days is that hedge funds have done horribly since the GFC and have destroyed value for their clients. Cliff proposes a different stance which takes into account risk-adjusted returns in order to make a better apples to apples comparison to index funds. I’ve copied the intro below:

Once again, I will review why hedge fund returns shouldn’t be compared to 100% long equities and how to do a more proper comparison. Analysts and authors often compare hedge fund returns to 100% equities (most often, the S&P 500). Then, almost always based on the last nine years since the global financial crisis (GFC) lows, they declare hedge funds an epic disaster. That’s just flat-out wrong. Comparing hedge funds to 100% equities would be a bad comparison at any time. To make things worse, this comparison is done over a cherry-picked time period. So this one has it all! An always fallacious comparison conducted over a particularly extreme period for that always fallacious comparison.

Podcast I’m listening to —

The Pitch is a new podcast I’ve stumbled across lately after a friend recommended it to me. Each episode is like an audio only version of Shark Tank minus the sob stories. If you want to beef up your business chops I think this show will help. You’ll get exposure to many interesting business plans. And you’ll also learn more about what makes investors tick — a key skill for anyone on the fundraising grind.

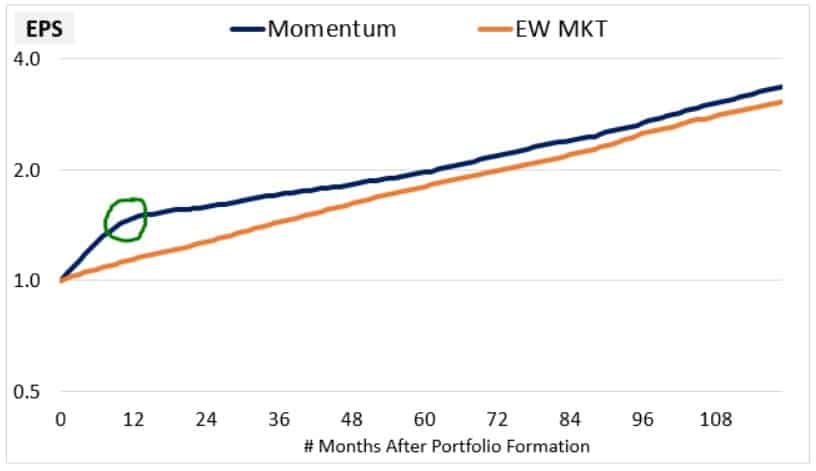

Chart I’m looking at —

Patrick OShaughnessy’s firm recently released on exhaustive analysis on how value and momentum premiums play out over time. I found the chart below especially interesting because it gives us insight into how long we can expect high-flyers to outperform the index.

The graph also shows us that after 12-months, investors start to re-rate these high flyers downward as lofty expectations inevitably get disappointed.

Here’s their detailed conclusion on the findings:

Momentum’s EPS initially grows at a rapid pace, building up a sizeable lead over the market. But around the one year point, the growth rate turns and tapers off, eventually converging onto the market growth rate. Given that the slowing of the growth rate and the reversal of the previously achieved price gains begin to occur at around the same time, we can conclude that one effect is likely causing the other. That is, the growth deceleration is likely functioning as the catalyst that induces the market to re-rate the stocks downward, giving rise to the momentum reversal that we discussed earlier.

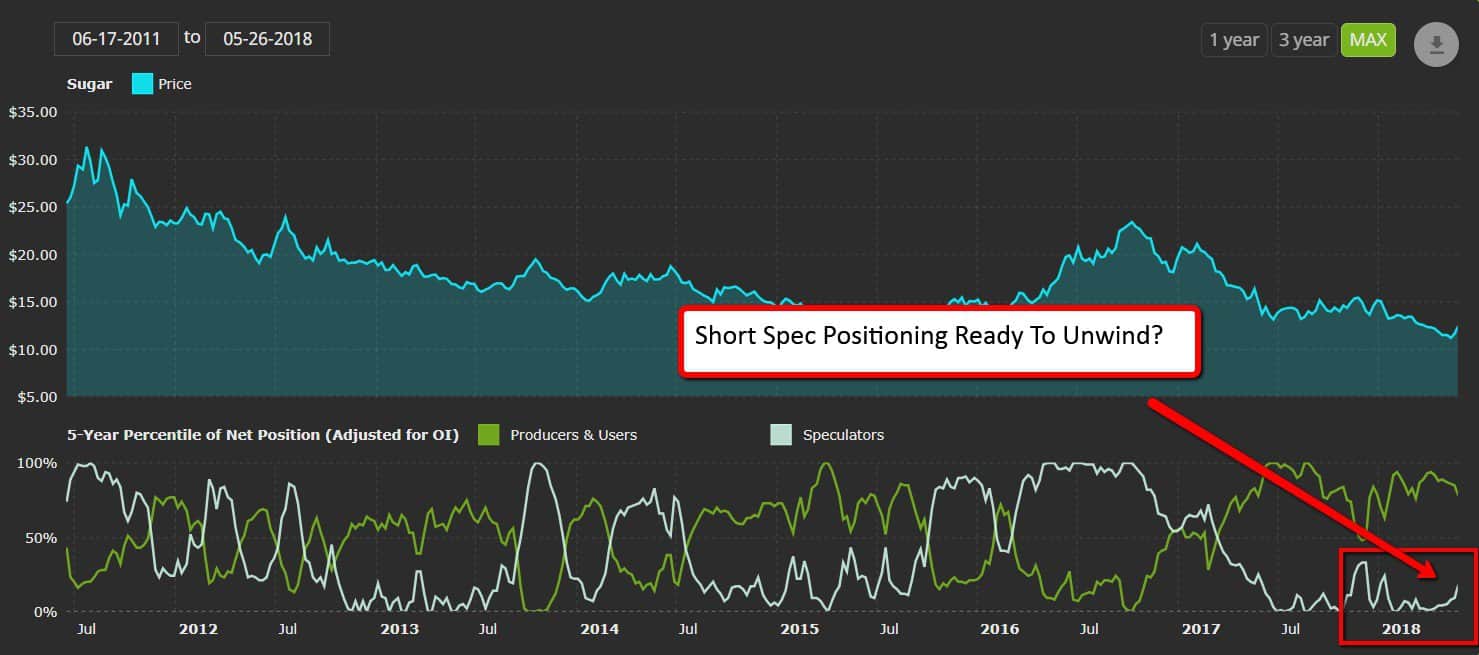

Trade I’m looking at —

Sugar has finally started to stage a rally from its late-April lows. This is a market we’ve been closely monitoring because of the large spec short position that has built up from summer of last year. The recent rally in sugar may finally trigger the unwind we’ve been waiting for.

Our preferred entry signal is a new 50-day high because that’s also what many trend following funds use as a signal to cover shorts. Price came close to breaching this important level but then fell back into the range.

If sugar can make a strong close above the 50-day high next week we’re looking to get long.

Quote I’m pondering —

There are times when it is important to invest cautiously, and there are times when it’s important to invest aggressively. A big part of the job is knowing where we are and choosing between those two. ~ Howard Marks

Opportunities in the market ebb and flow. To maximize returns we need to learn how to ebb and flow with it. Conserve your mental capital for when there’s a lot of asymmetry present. Don’t burn it all out on mediocre edges and setups.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. Alex posts his mindless drivel there daily.