There’s four major holidays we like to celebrate at Value Hive. Q1, Q2, Q3 and Q4 Investor Letters. This month we get our Q3 batch of letters. The next three Value Hive editions will be chock full of these letters. We’ll cover new positions, recently exited positions and market outlooks from our favorite value managers.

Here’s what we got this week. Elliott Management’s back with their latest idea. Beware of Canadian bank stocks. Andrew Rangeley’s killer blog post and much more.

Make sure to subscribe to this newsletter so you receive it every week, completely free.

Let’s get to it!

—

October 09, 2019

The Month From Hell: If investors were smart, we wouldn’t look at markets for the entire month of October. Yet year after year we defy our past miseries and step up to the plate. For those getting their feet wet in the investing world, let me tell you a bit about October. October’s known for three market crashes: 1987, 2002 and 2008.

If you want to scare your neighborhood investors, dress up as the eight month of the year.

_____________________________________________________________________________________________

Investor Spotlight: It’s a Marathon, Not a Sprint

GIFs by tenor

GIFs by tenor

After recent success with AT&T, Elliott Management is back in the news. This time with their newest idea, Marathon Petroleum (MPC).

According to their site, MPC’s engaged in refining, marketing, retail and transportation businesses. The company operates through three segments:

-

- Refining & Marketing: refines crude oil

- Speedway: sells transportation fuels and convenience products

- Midstream: gathers, processes and transports natural gas, crude oil and refined products

The company’s cheap by conventional metrics. They trade around 13x earnings and 7.2x EBITDA. MPC generated $5.36/share in earnings in 2018 and $2.39B in FCF. That’s good enough for a 6% FCF yield.

What Elliott Sees

Elliott’s reason for activism is simple. According to Elliott, “Marathon Petroleum has failed to realize the potential of its three world-class businesses.”

How do they unlock that value?

A separation of each business would unlock $22-$40B of shareholder value (61% upside). Here’s what each segment would look like if Marathon separated them out:

-

- Refining Business: By itself, the refining business would be worth $29B in EV. You’d also get the best refining asset base in the United States.

-

- Midstream Business: Separating the midstream business would result in an EV of $50B. The spin-off would also free-up the midstream business to pursue growth opportunities.

-

- Retail Business: Retail business would become the largest US-listed retail operator on first day of spin-off.

Elliott and Marathon Have History

This isn’t the first time Elliott’s fired shots across the bow at Marathon. The investment firm voiced its concerns with trapped asset value in 2016. Those concerns fell on deaf ears. At that time, Elliott called for Marathon to spin-off its Speedway and MPLX businesses.

Marathon obliged and simplified their MPLX business. Yet according to Elliott, half-assed their review of the Speedway business. This didn’t look good. In Elliotts words, the actions, “eroded investor confidence that the Company would unlock the value embedded in its assets.”

The Integrated Model Isn’t Working

In 2018, Gary Heminger stated, “Our integrated business model allows for differentiated results.” The MPC CEO was true in that the results were different. He forgot to let shareholders know they’d be different in a very bad way.

Take a look at the total shareholder return of MPC vs. its peers:

MPC’s underperformance relative to its peers grew over time. The retail assets in particular are the most shocking. MPC’s lost 245% in shareholder return versus its peers. Ouch.

The underperformance hasn’t simply restricted shareholder value. It’s reduced asset values to the point of absurdity. Let’s take a look at what Elliott means by that.

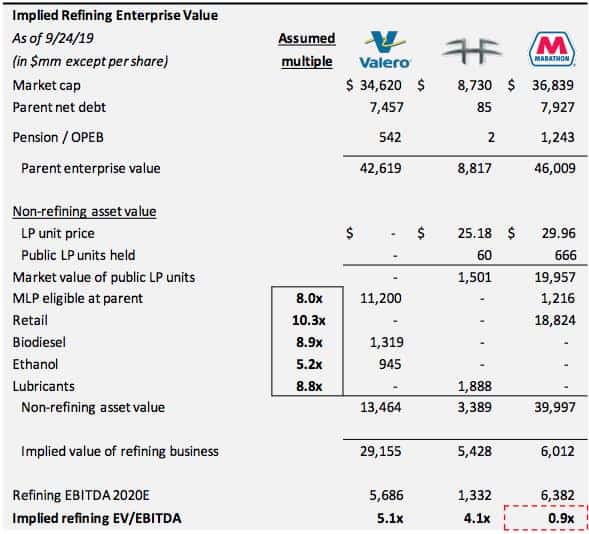

Buying Great Assets for <1x 2020 EBITDA

One crux of Elliott’s activist case is that MPC’s current share price implies a low EBITDA valuation for its refining business. For example, at current share prices, you can buy MPC’s refining business for less than 1x 2020 EBITDA.

How do we get to that figure? Check out Elliott’s back of the envelope valuation:

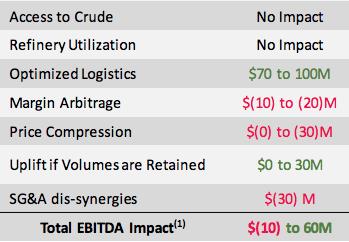

How Much Will The Separation Cost?

One excuse Marathon used to avoid the spin-offs in 2016 was the cost of spinning off each business. Elliott isn’t buying it.

Further down in the slide deck, Elliott lays out the total EBITDA impact from the separations. Spoiler alert: it’s jokingly small.

In a best-case scenario, the spin-offs would accrete $60M in total EBITDA. How MPC management doesn’t acknowledge the risk/reward benefit blows my mind.

Call To Action

Even though Elliott’s benefited from their activist stake in AT&T, the MPC idea looks to be the better bet. In order for this idea to get off the ground, MPC management must first acknowledge that the integrated model is a failed model.

Secondly, management needs to spin-off each business. I don’t want to get too excited about the idea until I see some Form 10-12s.

_____________________________________________________________________________________________

Movers and Shakers: Canadian Bank Stocks & YAVB

GIFs by tenor

GIFs by tenor

Canadian bank stocks are on the rise. Canadian Financials ETF (XFN) is up over 14% in 2019.

After the run-up, many investors wonder if now’s the time to get into the banks up North.

Not according to this guy: Nigel D’Souza.

A financial analyst from Veritas Investment Research, D’Souza mentions a few reasons to not be so bullish on Canadian banks. His main argument revolves around credit risk. He mentions three aspects of Canada’s 2019 credit risk:

-

- It’s higher than the 2015 and 2016 credit risk cycle

- It’s affecting not just oil and gas, but many sectors

- Banks expect elevated credit losses in near-term

So When Do We Buy?

I know. You want me to skip the details and get right to the meat and potatoes. D’Souza thinks investors should look North by late 2020 or early 2021.

D’Souza explains, saying (emphasis mine):

“Keep in mind management teams at the banks themselves have said they expect credit losses to continue to normalize. So if you think credit losses will continue to go up, you want to buy bank stocks in the future, not right now.”

Roger that, Nigel.

For a reminder, say, “Alexa, remind me to look at Canadian bank stocks on January 1, 2021.”

Andrew Walker and His Really Good Blog Post

GIFs by tenor

GIFs by tenor

Andrew Walker releases (arguably) the best blog post every month. How does it do it with such consistency? Every month, Walker posts the titled: Some things and ideas for the specific month.

Each post oozes with, well, things and ideas! Andrew discusses stock ideas, books he’s read and podcasts he’s listened to during the month.

Needless to say, it’s a must read.

Let’s touch on some things I thought were most intriguing.

The Gold-Star Challenge

This is (by far) my favorite feature from Andrew’s posts. The Gold Star Challenge first appeared in his August edition.

What is the Gold Star Challenge? Read at least one new 10-K a day. That’s it. It sounds simple. Yet think of the compounding nature of reading a new 10-K each day. For example, Andrew read 31 10-K’s last month.

How many did you read? How many did I read? Not that many!

The Value Hive needs to hop on Andrew’s Gold-Star Challenge train!

Jealousy in Investing

Charlie Munger often says (paraphrasing), jealousy is the only sin without some personal pleasure.

Andrew highlights a few key aspects of jealousy in the investing space. If left unattended, jealousy produces counterproductive habits and thoughts. Check them out:

Jealousy is a lot like Medusa (stay with me). There’s one key driver — jealousy — but expressed in various ways (or snakes). Along with arrogance and excessive risk taking there’s revenge trading/investing.

Revenge investing is the feeling that the market stole something from you. And it’s your job to get it back. What does this look like? In the value investing space this can be doubling-down on your biggest loser if your thesis failed. It can also mean placing larger-than-normal bets to “make up” for previous losses.

Stick To The Process

How do you combat jealousy investing? Andrew makes it simple: stick to the process.

Do yourself a favor and follow Andrew’s blog. Oh, and start reading more 10-Ks!!!

_____________________________________________________________________________________________

Idea of The Week: Sberbank (SBER), Vlata Fund

GIFs by tenor

GIFs by tenor

I came across this idea a couple years back in a stock screen (based on low P/E). But seeing that it was a Russian company, I passed. My reasoning? Too many headaches and geopolitical issues to worry about.

Yet here we are two years later and I find myself interested in the Russian banking powerhouse.

What triggered my interest this time was Vlata Fund’s Q3 letter.

Daniel Gladis runs Vlata Fund and he’s one of the OG’s to invest in Sberbank. According to the letter, Gladis first invested in SBER in 1997. At the time he only managed his personal assets.

20 years later Gladis remains invested. Why?

SBER Generates A TON of Profit

SBER is one of the most profitable companies not just in Russia, but in the entire world. For example, Daniel notes that Sberbank’s annual profit is on the level of Deutsche Bank’s market cap.

That’s wild to think about.

How can they sustain such high levels of profitability? Through deep and wide moats.

The company owns at least 25% market share in every major Russian banking category:

All-World Finance Metrics

SBER’s not only a powerhouse within Russia. The company shines when compared with any global financial institution.

For example, SBER generates the highest return on equity (ROE) based on the top 100 banks by market cap (excluding China). 23.1%. The company’s second in the world in return on assets with 2.9%. And they lead all banks in financial leverage ratio with 11.3%.

Positive Dynamics in Play in Russia

SBER’s local growth remains positioned to accelerate. Russia is deleveraging, there’s wage growth of 12% and loans are more affordable than ever. The average consumer loan rate in 2014-2015 flirted with 35%. Imagine paying 35% interest on a loan. Yikes!

Four years later, the average consumer loan rate hovers around 15%. Still relatively high, but much better than 35%.

On top of that, consumers are paying off their loans faster than ever. SBER’s repayment ratio (which measures the repayment amount as a percentage of loan) is an impressive 65%.

In other words, the average monthly payment is 2.3x the minimum amount due. That’s a healthy loan environment.

SBER is Cheap

Despite leading almost every world bank in profitability and return percentages, SBER trades at a discount to its peers. Here’s a breakdown of the metrics:

-

- P/B: 1.1x

- P/E: 5x

- Dividend Yield: 10%

Most comparables trade (at least) twice the P/E ratio as Sberbank.

Check out their latest slide deck if you want to dive deeper.

Disclosure: I do not own shares or derivatives of SBER stock.

_____________________________________________________________________________________________

Resource of The Week: Michael Mauboussin on P/E Ratios

GIFs by tenor

GIFs by tenor

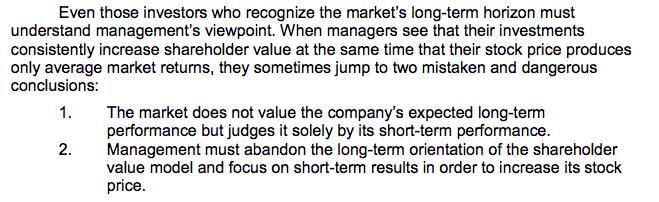

This week’s Resource of The Week is an oldie-but-a-goodie. In his 2001 whitepaper, Michael Mauboussin (along with Alfred Rappaport) breaks down the issues with earnings and P/E ratios.

Mauboussin argues that the stock market is long-term oriented in nature. Yet the tools we use to value stocks focus on short-term results. This disconnect trickles down into management’s inability to effectively allocate capital.

Mauboussin explains this further:

If earnings are the wrong tool for the job (i.e., valuing a company on a long-term basis), why do so many investors still use it?

Mauboussin’s answer is simple. Because it’s convenient. Yet this convenience comes with a price. What you gain in convenience (Mauboussin notes) you lose in accuracy and relevance.

The entire PDF (18 pages) is pure gold. Take the time to read it.

_____________________________________________________________________________________________

Who Won Twitter? — Ramp Capital

Earlier this week, Ramp Capital took the prize for Best Twitter Thread of 2019. I know. There’s still time left in the year. But trust me. It won’t be close.

For those that haven’t seen it, check it out here.

Here’s a teaser: It’s the story of WeWork rise and fall, told through The Office gifs. Michael Scott is Adam Neumann.

_____________________________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!