It’s that time of the year when we review our Q2 2025 performance: the good, bad, and ugly.

Here are the raw Q2 performance data:

- April: -4.82%

- May: 1.46%

- June: 13.27%

- Q2 2025: 9.91%

- YTD: 32.60%

The S&P 500 returned +10.15% during the same period. On a full-year basis (as of June 30, 2025), the MO portfolio is up 23.78%.

Before we dive into the review, a quick note: We’re opening up our Macro Ops Collective enrollment until the end of the year.

The Collective is our premier service, offering discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders and investors dedicated to mastery.

We’re having a decent year (up ~30% as of today), catching a few significant themes, discovering a few stocks nobody had heard of, and avoiding any major mistakes.

If you’re interested in our Trifecta Lens Framework and trading philosophy or want to eliminate the guesswork of position sizing, risk management, and market noise, check us out.

Click below and sign up.

Join The Collective

Alright, onto the piece.

I’m sensing a theme in the MO book where nothing happens, nothing happens, then everything happens. We experienced this last quarter, with 2.42%, -1.23%, and then 12.68%.

My job is to generate absolute returns from equities. And while we had a few successes this quarter in the equity book, the bulk of our returns came from futures trading, specifically Chris Dover’s (@ChrisDMacro in Slack) mean-reversion and curvy systems trades, as well as Alex’s currency trades (I’ll say it again for new Collective members … Alex is the best currency trader I’ve met. And when currency markets start trending, look out, he can quickly rack up the PnL).

For example, in April, we generated closed trade profits of 808 basis points from long positions in gold, the British pound, the euro, and 10-year note futures. We followed that up in June with closed profits of 868 basis points as we rolled successful trades in the Mexican Peso, Swiss Franc, Euro, Nasdaq 100, and S&P 500, as well as crude oil futures.

This is why I love the Macro Ops approach to markets. We go anywhere and trade any market as long as we have an edge, completely unconstrained by any given style box that most investors call home. Like Druckenmiller says, when one market isn’t working, we can switch to another.

However, let’s discuss the equity book in more detail to see what went right, what went wrong, and what we learned from our mistakes.

The Good: It’s Okay To Sell Your Darlings To Protect Capital

April showers brought a surge in profit-taking in the equity book. Here’s what I wrote on April 4th in the trade channel (emphasis mine):

“Operators, we are de-risking our equity book substantially this morning.

Internals continue to deteriorate and we’re entering a period of high uncertainty and volatility.

I want to emphasize that these trades are in no way a reflection of deteriorating fundamentals within each business. We are very much LT bulls on each of these names. But we must respect risk.”

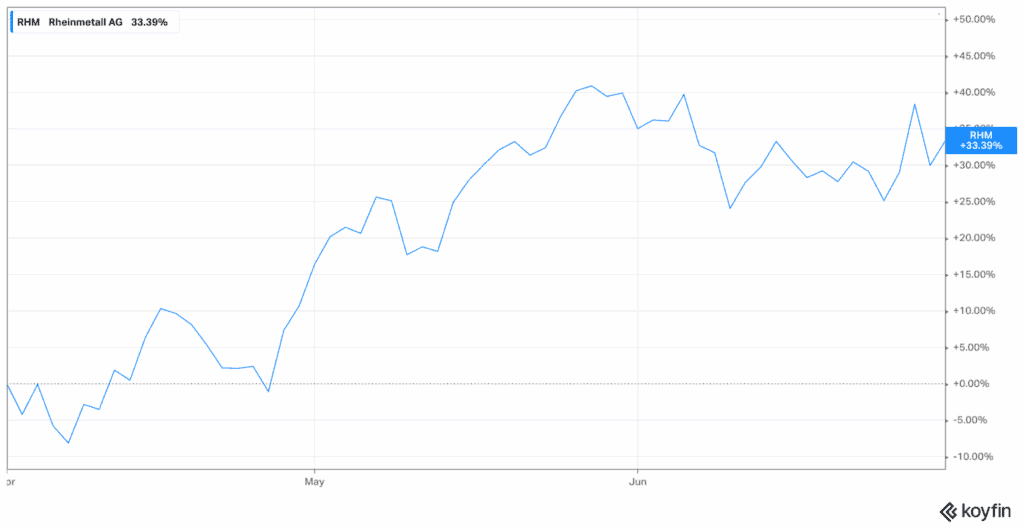

We exited full positions in Valuera Energy (VLE.T), Intrepid Potash (IPI), and Andean Precious Metals (APM). We also took half profits on Magna Mining (NICU) and Rheinmetall (RHM).

I ended the trade alert saying, “we will gladly (and hopefully) get back into these positions at lower prices on great technical setups. But we want to reduce risk, preserve cash, and survive.”

And that’s what we did. We rebought NICU, IDR, and APM all at decent notional sizes later in the quarter. This is a significant evolution in my process, and I don’t want to overlook it.

One of the hardest things for me is buying back a previously owned stock, regardless of price. It feels like having two kids under three. However, it’s often the best decision you can make. I know myself. And I know that I can’t be “objective” about a company or situation if I own their stock. I’ve read all the Buffett books, listened to all the Cliff Sosin podcasts … I just know myself.

I’m proud that we sold our darlings in April – which still had excellent long-term fundamentals – to protect our capital and buy them back later in the quarter. It’s a sign of personal growth.

Some Equity Winners

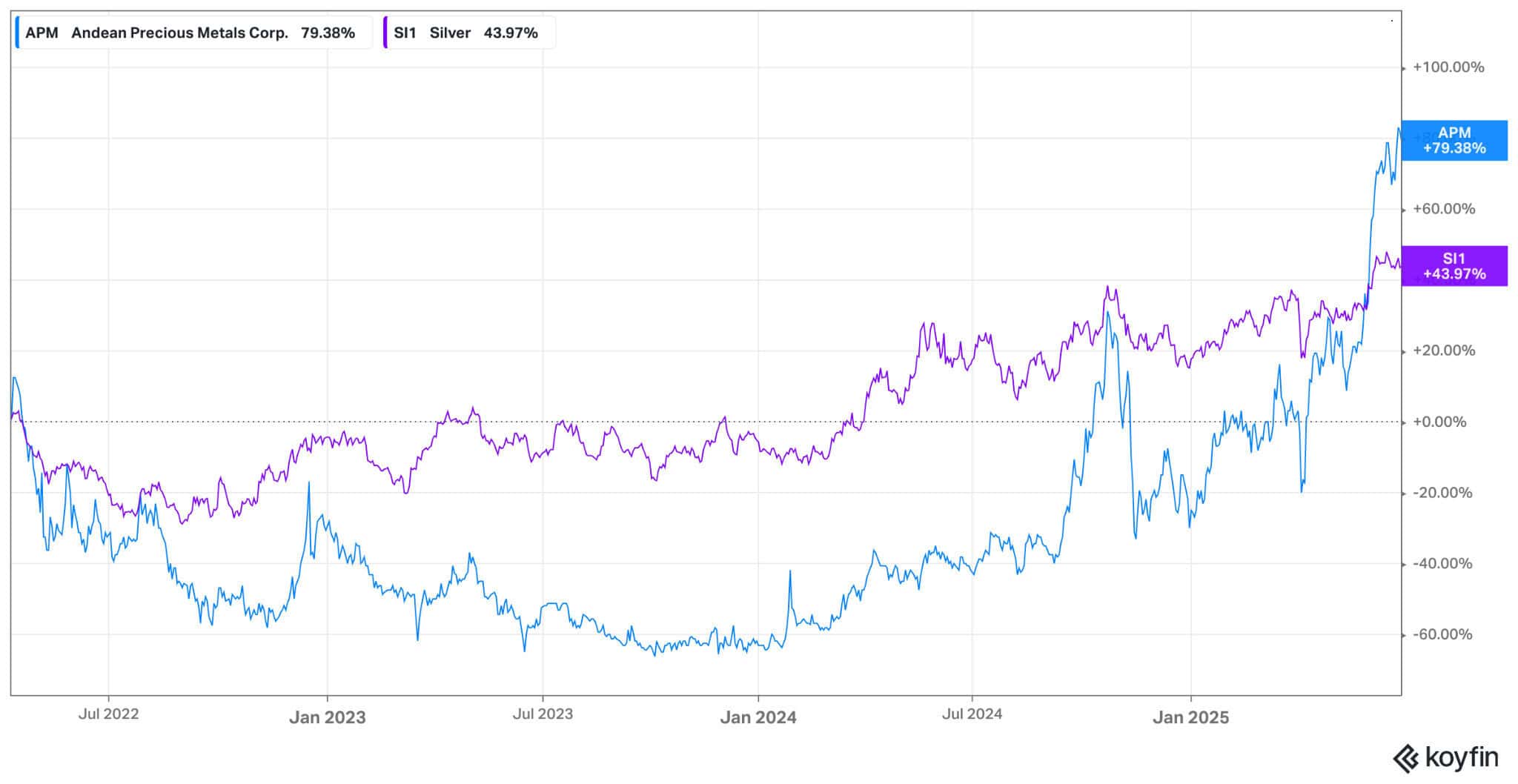

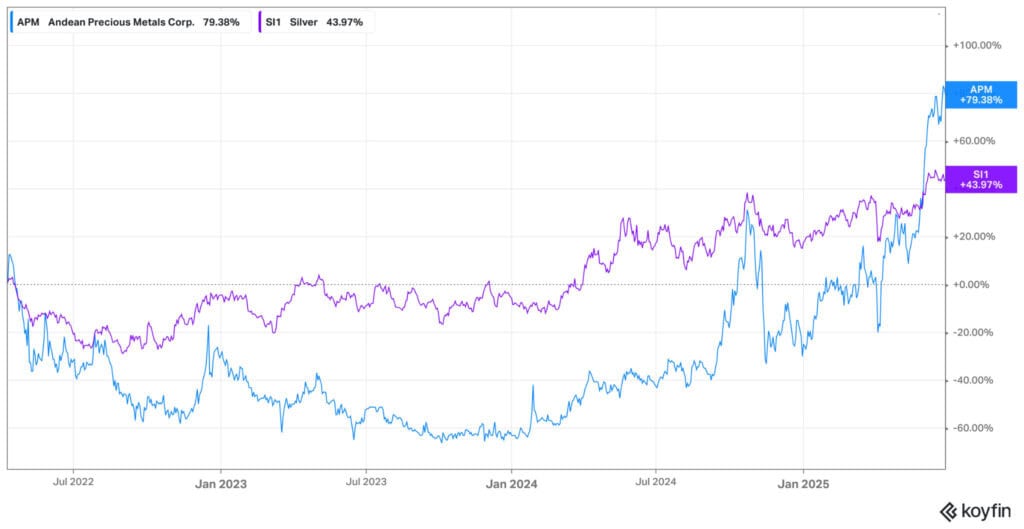

Andean Precious Metals (APM) was one of those rebought stocks. We purchased it on April 11 for approximately CAD 1.75. The stock ran ~80% from our entry during Q2 and is now a 6% notional position (see below).

Rheinmetall (RHM) was another big winner for us during the quarter (yet again). Despite taking half profits in April, RHM remained a notional position of ~7-8%. The stock rose 33% during the quarter as our European Defense Thesis continues to play out, with what feels like more confirmation each week.

The Bad: Poor Risk Management on Amentum (AMTM)

Most investors believe there are only two types of mistakes: mistakes of omission and mistakes of commission.

But they’re wrong. There’s also a third type of mistake: the mistake of being too cute with stop-losses that cost you principal and lost potential profits.

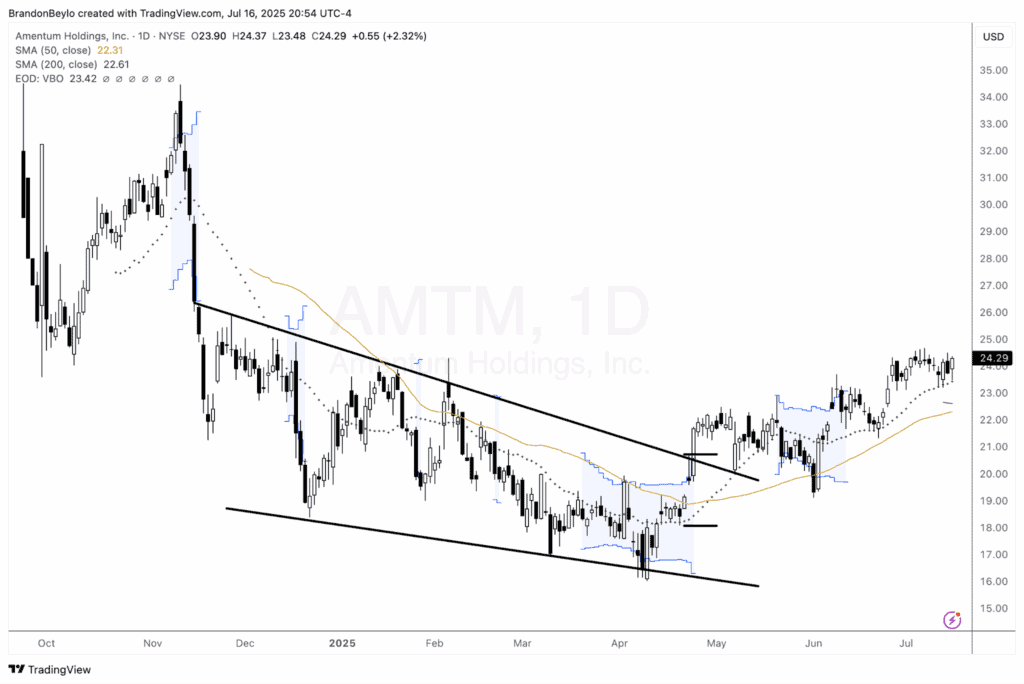

That’s what happened with Amentum Holdings (AMTM). AMTM is a core position in our National Defense thematic. My friend Adam Rossi pitched me the stock at ~$17-18/share. I liked the idea, but it didn’t fit our Trifecta Lens framework … just needed the technicals to confirm our entry.

We received technical confirmation of the April 24 breakout and purchased our first leg at $20.75 with a stop-loss at $18.05. The stock immediately moved in our favor and never really flirted with our initial stop loss.

That is a good exit point given our entry. It leaves enough room for the stock to breathe, but provides us with enough notional size to matter if the trade works. Here’s what I wrote in the trade alert (emphasis added):

“We’re buying a starter position in AMTM this morning. AMTM fits our Trifecta Lens criteria:

Fundamentals: One of the cheapest government/military contractors with one of the longest histories of operations (the original company worked on the Manhattan Project!)

Technicals: AMTM is breaking out of its downward channel/bottom with relative strength and increased buying volume

Sentiment: Broad sell-off in government contractors due to DOGE has created opportunities to buy companies like AMTM for cheap (these guys aren’t going anywhere — they work on too important stuff)

We’re risking 50bps with a stop below the midline. This is a wide stop so it allows us to cut well before a -1R loss if we choose. We’ll look to add to the position as it moves in our favor.”

Who’s that guy? He sounds smart!

Well, that guy got greedy. I added a second leg on May 20, with what looked like another VBO, only to have the stock close near its lows back inside the trading range. This is where compounding errors hurt. To compensate for the added risk of that second leg, I adjusted my initial stop-loss from $18.05 to $19.60.

As you can see from the chart above, I quickly stopped out, incurring a 101bps loss. We re-entered the trade on June 25, and yes, with a wide stop at $19.00.

Here’s the 101bps lesson: Do not get cute with Trifecta Lens Trades. Give them room to move. Size up initially if necessary. Have conviction in the Fundamental, Technical, and Sentiment alignment.

So of course I didn’t repeat the error during the quarter, right? Welllllllll about that.

The Ugly: Fumbling MP Materials (MP)

I’ll just say it … this one hurts. Not as bad as missing Droneshield (thanks for sending daily screenshots of that chart each morning, Chris M, means a lot). But it’s getting there.

MP was another Trifecta Lens trade within our Metals/Mining and National Defense thematics. We even had an event catalyst when China banned critical minerals, including REEs. We bought the stock on April 14 with me writing:

“China’s latest export ban on critical raw materials, and specifically REEs, looks like a potential catalyst for MP, one of the US’s largest REE developers.”

I did the REE work for Idaho Strategic (IDR), so MP was more of an “Invest then investigate” position. In fact, it was basically a flows play. I believed the news would cause investors to want to own REEs, and MP was the best way to do it, even if the company sent 80-90% of its REEs to China for processing.

Shout-out to @MichaelP in Slack for asking that question. Here was my response to him (emphasis mine):

“Specifically, MP currently has contracted processing agreements with China for ~80% of their ore. Which is obviously a lot and a potential conflict of interest as we move forward.

However, this is a trade. Maybe it becomes an investment, but we’re treating it as one trade in a potential basket REE approach. The algos and momentum-driven traders don’t know, nor do they care, about MP’s processing agreements with China.

The trade is basically: “REE will become very important –> I want to buy exposure to REE –> Oh look, MP is the largest and most liquid way to play that –> BUY.”

You could also imagine a world where the US decides to match China’s processing agreement or terminate the agreement and pay whatever fine back to MP for reneging the contract, etc. But that’s pure speculation.

Right now, this is a thematic trade as part of a potential basket of REE exposure that could possibly turn into a LT investment as we do more work.”

All of that sounds great (and smart, too?). But then I botched the stop-loss. I put it at $21, and I wanted to tell you that was because of some technical level or something. But it wasn’t. It was just a bad stop placement.

MP was a volatile stock when we bought it, routinely swinging 20-30% over the course of a few weekly bars. The correct stop placement would’ve been $15.40, below the right shoulder and pivot low of December 2024 (see below).

It goes back to what I said about AMTM … Do not get cute with Trifecta Lens Trades. Give them room to move. Size up initially if you have to. Have conviction in the Fundamental, Technical, and Sentiment alignment.

The REE / National Defense trade is a long-term secular thematic. Why am I positioning stop losses using the midline? I should match my stops with my trade time frame and use at least the 200D moving average on long-term weekly or monthly charts.

Conclusion: It’s All About The Trifecta Lens

I’m not using these bad and ugly examples as a way of saying, “I told you that this would happen! Look at how smart I am at predicting these events, why hasn’t Druckenmiller called to congratulate me yet.”

Instead, I highlight them because they reveal the power of focusing on the Trifceta Lens Process. It’s not just about nailing the fundamental view or sentiment analysis or technical setup. It’s about getting all three to align simultaneously, recognizing that, and then getting the hell out of the way and letting the trade work for you.

There’s an unwritten rule in baseball that you avoid talking to a pitcher who’s throwing a no-hitter between innings. After a few innings of no-hit ball everyone in the dugout gets the memo: don’t f**k this up, it could be sports history.

I feel the same way about Trifecta Lens trades. When all three criteria align and you place the trade and it starts working … don’t talk to the trade. Let it do it’s thing. Improper stop-loss placement interrupts the natural flow state of a trade that is likely to work.

So if there’s one lesson I want to carry into the second half of the year, it’s to let the trades do the work, keep to myself in the dugout, and hunt for that next Trifecta Lens pick.

Oh, and don’t forget to check out our MO Collective if you’re interested in learning more about our process, trading philosophy, and joining a raucous group of the internet’s smartest market participants!

Join The Collective

Equity Portfolio Stats (as of July 16, 2025)

Total Positions: 19

Top Five Positions (notional):

- iShares Bitcoin: 19%

- Rheinmetall: 7.93%

- Uber Technologies: 7.29%

- Andean Precious Metals: 6%

- Rocket Labs: 5.90%

Industry Exposure:

- Metals & Mining: 36%

- Aerospace & Defense: 23%

- Tech/Other: 21%

- Oil & Gas / Energy: 8%