Thanksgiving’s right around the corner. Can you believe it? Turkey, mashed potatoes, gravy, and TSLAQ arguments. What else am I missing?

Anyways, there’s a ton of content for y’all this week. We’ve got a few more Q3 letters to share. A new spin-off from a major outdoor brand. valueDACH’s two-part interview with Guy Spier, and more!

Before we jump in, make sure to subscribe to this newsletter. You’ll receive Value Hive every week, completely free. Straight to your inbox.

Let’s feast!

—

November 20, 2019

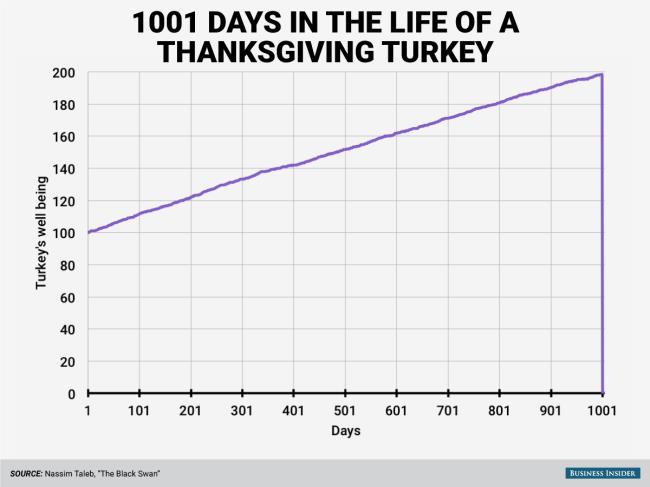

Taleb’s Turkey: For the most part, turkeys live good lives. That is until that day comes. After reading Nassem Taleb’s book Black Swan, I can’t help but think of this chart while feasting on Thanksgiving dinner:

A turkey’s life isn’t robust. Just like LTCM’s historic collapse, some things look like sure bets (like a turkey living past Thanksgiving) until they aren’t.

_____________________________________________________________________________________________

Investor Spotlight: GreenWood Investors & Hayden Capital

GIFs by tenor

GIFs by tenor

This week we’ve got two killer letters from Greenwood Investors and Hayden Capital. Each letter offers investment ideas, psychology lessons and even a book recommendation.

Let’s dive in!

GreenWood Investors: Pent-up Alpha

GreenWood Investors, managed by Steven Wood & Chris Torino, is up 2.30% YTD (as of 10-31). In their Q3 letter, Torino discusses long-term thinking, a couple European stocks and Boeing. After recent underperformance, GreenWood remains optimistic.

Torino believes GreenWood, “holds the future in their hands.” And the future looks bright.

The Corner of Dead Money & Unpredictability

Dead-money. The term often used to describe an investment which goes nowhere over long periods of time. The investment is ‘dead’ because it’s not earning anything in capital appreciation. Plus, that money could be invested elsewhere in a more, non-dead, investment.

Torino expresses the idea of dead-money through GreenWood’s Exor (EXOR) investment. He says Exor is, “a prime candidate of a company that can at times go for long stretches where it may seem like nothing is happening from a fundamental perspective;”

So how do you combat dead-money? Invest in exceptional allocators. Builders (emphasis mine)…

“However, it is a refreshing reminder that putting capital in the hands of managers whom we trust, and have significant skin in the game, will compound the underlying value of the businesses when the market is least expecting it.”

Exor still trades at a 28% discount to NAV.

The Pub vs. Tourist Approach

We’re huge fans of Rory Sutherland at Macro Ops. Sutherland’s book, Alchemy, didn’t have cash flow equations. It didn’t mention LTV/CAC ratios. Yet it was one of the best investing books I read in 2019.

How so? Via the pub vs. tourist example.

Torino discusses this framework of customer acquisition and retention in the letter. It’s a great mental model for thinking of the business/customer relationship.

The Pub Approach: “The business makes less money from people on each visit but likely generates significant trust and more profits in the long-term.”

The Tourist Approach: “The company attempts to gouge the customer on a single visit or short-term contract, and is thus less trustworthy.”

Torino notes of a simple, yet powerful investment strategy. Long the pubs, short the tourists.

Long Leonardo, Short Boeing

Torino gives readers an example of the long/short pub vs. tourist strategy in the letter. GreenWood is long Leonardo and short Boeing. Let’s find out why.

Short the Tourist: Boeing (BA)

GreenWood went short BA in late September when, “it became clear Boeing would not meet its early Q4 target for FAA approval of the 737 MAX and refused to admit the MAX had a hardware problem, not just a software problem.”

Boeing failed to think about the long-term prospects of their business. They chased short-term earnings beats. Their time-frame resulted in wonky airplanes, shoddy software, and untrained pilots.

Torino offers a great example at BA’s tourist thought process (emphasis mine) :

“At the end of the day, BA’s core-competency should be to build safe and reliable aircraft. It has failed to do so in the case of the MAX and it continues to insist of a reckless approval pathway that ignores the need to retrain pilots in a simulator, because it would impact operating earnings ~5%.”

Long the Pub: Leonardo (LDO)

GreenWood’s thesis is simple. LDO’s recent heavy investment should grow its backlog and improve their cash conversion profile. Second, the company won “very demanding” contracts with US DoD. Third, Leonardo is nearing certification for “the first civil tiltrotor in history”.

In GreenWood’s eyes, the company’s “taking substantial market share and is moving into a period of harvesting its major investments made a few years ago.”

All this coming “when investors are not paying attention.”

If you haven’t already, give Steven a follow on Twitter.

Hayden Capital: Insight Arbitrage

Fred Liu runs Hayden Capital. The fund returned -6.02% for the quarter. YTD the fund is up 20.75%. Liu spent most of the letter discussing social commerce, how companies use it, and the US’s slow adoption.

Let’s dive in.

The Dollar Auction: Investing in Money-Losers

The Dollar Auction is an economics game in which people bid on a $1 bill. The winner is the highest bidder. Yet there’s a catch. In this game, the second-highest bidder loses the amount that they bid.

Now one would think … “If they’re bidding on a $1 bill, wouldn’t the winner just bid $1?”

Not so fast. Liu explains that, “almost always, the end result is that the winning bid will surpass $1.”

But why?

According to Liu, it happens “as the bids rise and the bidders’ incentives shift from trying to make a profit to minimizing their losses by not being in second place.”

Liu argues that this game is going on in the private capital markets. “Private markets”, Liu asserts, “have been willing to fund these companies [questionable models, winner-take-all], providing the capital to make these even-higher bids.”

What will happen when the tide goes out and investors are caught plowing capital into money-losing enterprises?

The game might be up for those investors. The ones chasing unicorns without a care in the world of eventual profitability.

Social Commerce: Capturing Monetization

People like shopping. But people love shopping with their friends.

Companies such as Poshmark are taking advantage of this social commerce phenomenon.

Liu notes that companies (and apps) like Poshmark are in the business of user engagement. They want your eyes glued on their app all-day. Poshmark’s average engagement per-user is 23-27 minutes/day. That rivals Facebook and Snapchat’s 27 minutes.

Yet user engagement is meaningless without user retention (i.e., stickiness).

Liu makes this point, saying, “By keeping users engaged, it improves the user retention rates, and more importantly drives monetization.”

Gamifying Discounts

Liu’s commentary on the gamification of company apps was my favorite section of the letter. Gamifying apps increase user engagement and retention. And according to Liu, many companies use this as a cheap customer acquisition tactic.

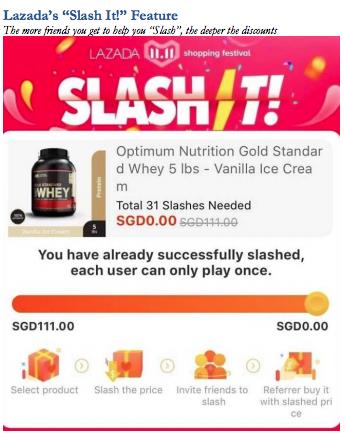

The letter provides examples from companies such as Pinduoduo, Taobao, Lazada and Shopee. Check out the Lazada example:

Users literally swipe their screen to ‘slash’ the product. If they get enough of their friends to slash the same product, the price could drop to zero. It’s an ingenious way to grow your brand’s audience. What’s one free protein powder compared to 31 new slashes (users on the app)?

Stocks Mentioned

Hayden sold out of their Credit Acceptance Corp (CACC) position in Q3. The stock generated a 26% annualized return since initial purchase. Not bad!

Why are they selling? Here’s Liu’s own words:

“The remaining pool of potential customers are going to be a tougher sell (there’s a reason they haven’t already joined the program), implying at most 60% upside in its dealer relationships. Volumes per dealer may increase … but this is likely to be short-lived and will return to structural norms afterwards.”

Finally, Hayden Capital is looking for two interns for the Spring semester. If you or someone you know would be a great candidate, shoot Fred an email. While you’re at it, give Liu a follow on Twitter.

_____________________________________________________________________________________________

Movers and Shakers: Icahn’s Plan & Sam Zell’s Purchases

GIFs by tenor

GIFs by tenor

Carl Icahn and Sam Zell are two investing legends. Both investors are in the spotlight this week. Icahn’s trying to negotiate a mega-deal between two well-known companies. Zell’s buying dirt-cheap oil assets for pennies on the dollar.

Icahn’s Proposed Marriage

Icahn wants to combine HP and Xerox. To accomplish his mission, he’s bought 10% of Xerox and nearly 5% of HP (ticker: HPQ). If anyone can get the deal done, it’s Icahn.

Here’s what we know so far:

-

- Xerox offered $33B in a cash + stock offer for HP

- HP confirmed the bid, but did not disclose the offer price

HP is more than 3x the size of Xerox. But according to Icahn, the deal is a “no brainer” for Xerox.

What Icahn Sees

Icahn thinks a merger between HPQ & XRX is “in the best interests of both sets of shareholders.” He notes the merger would:

-

- Give the potential for cost savings

- Market a more balanced portfolio of printer offerings

The old-school corporate raider’s done a deal like this before. Last June, Icahn gained a seta on Caesars’ (CZR) board. He then initiated a $17.3B merger between CZR and smaller-sized peer, Eldorado Resorts.

First Glance at Both Companies

HPQ is a great company trading at an attractive price. You can buy the business for 7x earnings and 6x EBITDA. That’s not bad considering HPQ generates around $3B in FCF annually (10% FCF yield).

XRX isn’t as cheap as HPQ on paper. The printing company trades for 14x earnings and 8x EBITDA. They generate close to $1B in FCF (11% FCF yield).

Sam Zell: Fishing Where They Ain’t

GIFs by tenor

GIFs by tenor

Sam Zell is a magnate in the distressed investing space. A multi-billionaire, Zell made his fortunes buying assets when nobody else wanted them. This Forbes article outlines his investing strategy:

-

- Look for bargains: assets that are out of favor or in bankruptcy

- Ensure that those assets are of high intrinsic quality

- Structure the deal so that you pay as little in taxes as legally possible

So where’s he looking now? The US Oil sector.

In a recent Bloomberg interview, Zell revealed he’s buying assets in California, Colorado and Texas. His reasoning? Capital’s drying up and assets are cheap:

“The amount of capital available in the oil patch is disappearing.”

Zell’s providing capital to companies that are expecting problems. In other words, these are proactive capital infusions, not reactionary investments. Zell likens the current oil and gas downturn to the real estate market in the 1990s. Zell said, “you had empty buildings all over the place, nobody had cash.”

Distressed Ideas in O&G

There’s plenty of distressed companies to go around in the O&G market. Let’s dive through a few names and their valuations.

But I’ll warn you. O&G companies, especially in downturns, take on a biotech stock role. They burn through cash, leaving nothing for their shareholders.

1. Sandridge Mississippian Trust (SDT)

SDT trades at 1x earnings and 0.39x EBITDA. The company has no debt, nearly $3M in net cash and a whopping 70% dividend yield. It’s also trading at an 85% discount to book value.

2. Rosehill Resources (ROSE)

ROSE is a *gulp* former SPAC. It trades for 0.42x earnings and 3x EBITDA. They have $360M in net debt, 68% pre-tax margins and a 15% discount to book value.

3. TransGlobal Energy Corp. (TGA)

TGA trades for 2.5x earnings, 2x working capital, and around 1x EBITDA. They have $19M in net debt and generated $0.13/share in cash flow last quarter. Given their low debt-to-EBITDA ratio (0.19), the company intends to leverage strategically to acquire and grow their business.

Dumpster Diving

Zell made billions dumpster diving. But that’s what it is — a large dumpster. There’s loads of garbage to sort through. But if you’re prudent, you can find diamonds in the rough oil.

_____________________________________________________________________________________________

Resource of The Week: valueDACH & Guy Spier

GIFs by tenor

GIFs by tenor

valueDACH’s content gets better and better. This week they’re back with part deux of their interview with Guy Spier. Spier covers a variety of topics, including:

-

- Allocating time to think alone

- How many companies he researches per year

- Factors that make him dive deeper into a company

- Limits to number of holdings

- When and why he sells a company

This is an interview you’ll want to watch again. There’s that much wisdom in it.

_____________________________________________________________________________________________

Idea of The Week: An Explosive Spin-off

Last week, American Outdoor Brands (AOBC) announced its intentions to spin-off the ammunition manufacturer, Smith & Wesson. The spin-off leaves AOBC with their outdoor products and accessories business.

The majority of AOBC’s revenues come from their ammunition sales. In fact, AOBC’s original name was Smith & Wesson. Yet the recent surge in gun control laws (and overall sentiment around guns) prompted the company to change their name. And subsequently their business strategy.

As a standalone products and accessories business, AOBC should generate around $160M in annual revenue. This is in stark contrast to Smith & Wesson. AOBC’s expecting $600M in revenue and $90 – $105M in EBITDA within the first 12 months post-spin:

Important Dates for Spin-off

-

- Date of Form 10 Filing: 1H 2020

- Finalized Spin-off Date: 2H 2020

Here’s AOBC’s slide deck if you want more information.

_____________________________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!