“The only thing I do know is that from chaos comes opportunity.” – Daniel S. Loeb

POWW’s largest shareholder Steve Urvan went full-on activist this week. The former GunBroker founder launched a website called TheUrvanGroup.com, where shareholders and interested parties can read his activist letter.

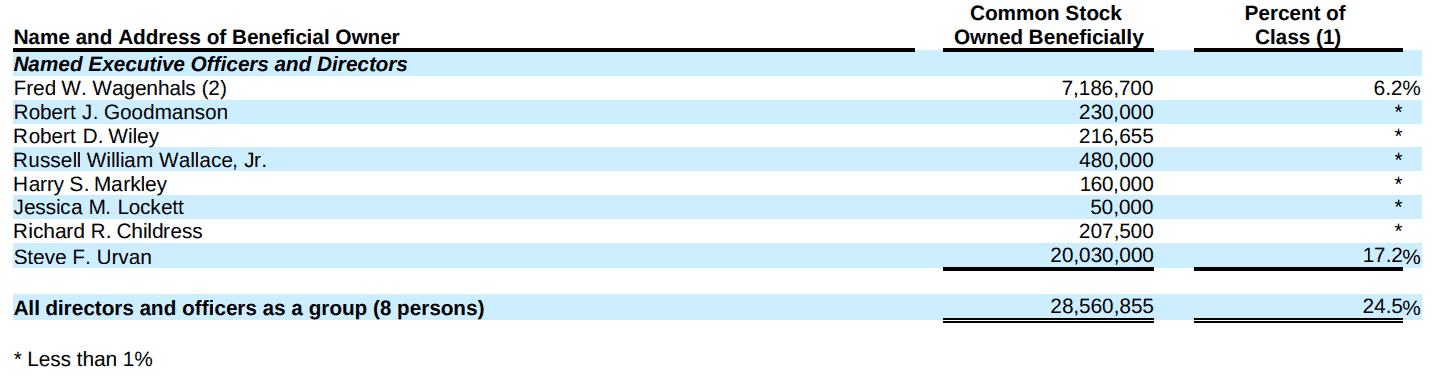

Urvan founded GunBroker.com 22 years ago with his capital and turned it into the world’s leading online marketplace for firearms. Currently, Urvan owns 17% of POWW, which he gained from the sale of GunBroker.com last year.

We’ll dissect the details of Urvan’s letter and explain why we agree with nearly every proposed initiative.

The bottom line is that this is excellent news for existing POWW shareholders. POWW’s most significant issue is (and always has been) its management team and capital allocation decisions.

If successful, we believe that Urvan can resolve these issues and create an attractive company and a compelling investment opportunity.

The Urvan Group’s Shareholder Letter

Urvan outlined his main issues with POWW and the management team, which include:

- Five consecutive years of rising costs, compressed margins, and an explosion of SG&A expenses

- $40M in total losses since going public

- The little-to-no positive impact from rising ammunition sales growth

- Egregious related party transactions

- Misaligned Board of Directors w/ No Relevant Experience

I agree with every issue above and wrote extensively about them in my post Why I’ve Changed My Mind on POWW.

Let’s flesh out Urvan’s concerns.

Growing Operating Losses w/ Worsening Unit Economics

Five consecutive years of operating losses aren’t concerning if you’re a fast-growing young company. Investors can even accommodate losses if they see improving underlying economics. So far, POWW hasn’t demonstrated positive trending economics from its “core” manufacturing business.

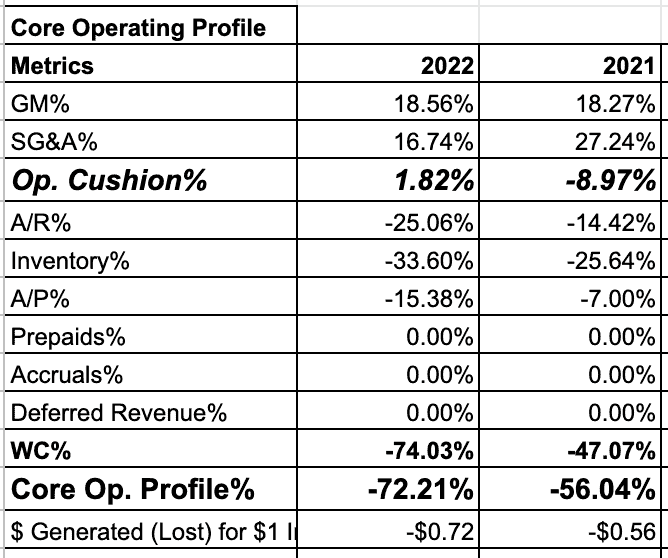

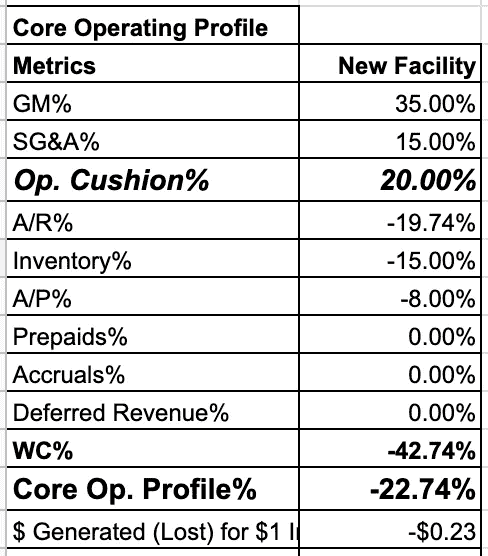

Check out the YoY decline in the manufacturing segment’s Core Operating Growth Profile.

POWW’s manufacturing business lost $0.72 for every $1 in incremental revenue growth. The opposite of improving economics.

Management blamed the new manufacturing facility for the worsening unit economics, but I don’t buy it. Assuming management’s high-end guidance of 35% gross margins and industry-average SG&A expenses still doesn’t get us to unit profitability (see below).

Even under this Blue Sky Scenario, POWW’s ammo business would still lose $0.23 for every $1 in incremental revenue growth.

Manufacturing Business Generated <5% of Operating Earnings

The ironic part is that the manufacturing business generates $1.8M of the company’s $36.5M operating income. Urvan explained his frustration at this fact by saying (emphasis mine):

“Further, it appears that the recent onset of meaningful revenue growth delivered by the legacy Ammunitions segment has had little impact on the bottom line.”

In other words, POWW spent hundreds of millions to make a couple of million.

Then there are the issues with the board and management’s related party transactions.

High-Interest Personal Loans & Lack of Board Ownership

Urvan outlined two critical issues with the current management team and board of directors. Let’s start with the board.

POWW’s Board of Directors – ex Wagenhals and Urvan – own a combined 1.11% of the company’s shares outstanding.

The board has no incentive to care about the company’s stock price. Additionally, the Board has zero experience leveraging its most prized asset, the online e-commerce marketplace. Check out the bios of each Board Member below (from POWW 10-K).

- Rusty Wallace, Jr.: Hall-of-Fame NASCAR driver and principal shareholder of the Rusty Wallace Automotive Group, a group of eight automotive dealerships in Eastern Tennessee.

- Harry Markley: Served with the Phoenix Police Department for more than 30 years, most recently as Assistant Chief of the Patrol Division from 2013 through 2017 and Commander of the Family Investigations Bureau from 2002 to 2013.

- Jessica Lockett: Corporate and securities law attorney focused on representing public and private companies at various stages of development.

- Richard Childress: Former NASCAR driver and owner of Richard Childress Racing since 1969 and Childress Vineyards since 2004.

Two NASCAR drivers, a police officer, and a securities lawyer walk into a bar …

Urvan wants to Drain The Swamp and institute a new seven-member (including himself) Board of Directors, which include:

- Gregg Alper: Founder of GWA Distribution Group, an online retailer focusing on replacing automotive, marine, and small engine parts (acquired in April 2021). Gregg was also the former Chief Operating Officer and Director of e-commerce of USP Motorsports, an online performance parts provider for German vehicles.

- Darren Farber: Founder and Managing Partner of Albion River LLC, a private investment firm focusing on aerospace, defense, and government-related businesses.

- William Fraim: Former Chief Executive Officer and Chairman of the board of directors of AcuSport Corporation, a nationwide distributor of outdoor and shooting sports products.

- Susan Lokey: Chief Financial Officer of IA Tech LLC, parent company of GunBroker.com, LLC, and former Manager of the Sales Audit and Sales Accounting department at The Home Depot, Inc. (NYSE: HD)

- Christos Tsentas: Partner of Albion River LLC, a private direct investment firm focused on aerospace, defense, and government-related opportunities, and former investment banker at KippsDeSanto & Co., an M&A advisory firm focused on the aerospace and defense markets.

- Wayne Walker: Founder and President of Walker Nell Partners, Inc., an international business consulting firm, and currently serves on the boards of directors of Wrap Technologies, Inc. (NASDAQ: WRAP), Petro Pharmaceuticals, Inc. (NASDAQ: PTPI), and AYRO, Inc. (NASDAQ: AYRO).

I don’t need to explain that Urvan’s nominees represent a step-function change in experience and capabilities.

Finally, there’s the related party transaction where Wagenhals loaned POWW $3.5M at 12% annual interest. You know how the old Mohnish Pabrai proverb goes: “Heads I win, Tails you pay me 12% interest annually.”

Urvan’s Six Step Recovery Plan

Along with a new Board of Directors, Urvan outlined his six initiatives for improved company governance, balance sheet strength, and profitable growth. Let’s break each down.

Initiative 1: Enhance Corporate Governance

The low-hanging fruit includes better disclosures around capital allocation decisions, little-to-no related party transactions, and fewer insiders on the board. Urvan also plans to separate the Chairman and CEO roles (Wagenhals is currently both Chairman and CEO).

Initiative 2: Optimize Balance Sheet

POWW management has long touted its strong balance sheet and ample cash reserves. However, Urvan believes the company can improve its financial footing with strategic, non-dilutive financing and leasing versus owning physical real estate.

Initiative 3: Assess Management and Improve Human Capital

Hopefully, this initiative will completely overhaul POWW’s existing management team.

Nothing is official, but I wonder if Urvan has eyed James Debney, former Smith & Wesson (SWBI) CEO, for the CEO role. Debney would come with some hair after leaving SWBI due to “misconduct.”

Initiative 4: Strengthen Existing Ammunitions and Marketplace Segments

Urvan sells/divests the ammo manufacturing business in a perfect world and pushes every chip into the online marketplace business. We’re encouraged by Urvan’s thoughts on this subject (emphasis mine):

“Even when factoring in the Marketplace segment’s strong performance and stripping out assumed one-time costs for the new manufacturing facility, the Company’s margins continue to dramatically lag logical firearms peers even as it gets to scale. Our nominees believe this reinforces the need to slow further investment in Ammunitions and prioritize higher-growth, higher margin opportunities in ecommerce.”

Initiative 5: Explore Accretive M&A to Supplement Organic Growth

Urvan envisions GunBroker as a platform for all things firearm, self-defense, and sport shooting enthusiasts. GunBroker can leverage its position as the world’s leading online firearm marketplace to buy adjacent marketplaces and e-commerce players in categories like sporting goods, apparel, and collectibles.

My stomach churns whenever I see a company expanding beyond its core competency in the name of revenue and profit growth. GunBroker dominates the firearm marketplace niche. What gives it the right to win in sporting goods, collectibles, or apparel?

Initiative 6: Prioritize Transparent Investor Relations

POWW’s recent quarterly conference calls are worthless. The company has a stable of analysts that softball questions on things that don’t matter to long-term shareholder value.

Last quarter’s call was the pinnacle of such charades. I was the last caller in the Q&A after a handful of high-fiving on the “fantastic spin-off news” and “great quarter guys, keep it up” crowd. I asked management why they flipped their stance on the combination of GunBroker + Ammo Inc and why anyone would buy the manufacturing business post-spin-off.

You can listen to their response below (via QUARTR).

Transparent Investor Relations means more time allotted for difficult questions.

Concluding Thoughts: $80M On The Line

Urvan owns 17% of POWW. He isn’t buying more stock nor wants to own the entire company. According to his letter, he’s “not seeking to acquire all or part of the Company. I am not seeking to take any steps that are counter to your interests. I am investing my own energy, money and time in a campaign to ignite a brighter future for all of the Company’s stakeholders.”

He has $80M of his money on the line and doesn’t want to see it vanish.

Also, I’d love to host a Twitter Spaces with Steve Urvan to discuss his plans for POWW and what he thinks the company could look like in 3-5 years. So Steve, if you’re reading this, I’d love to make it happen.