Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot Alex an email at alex@macro-ops.com and I’ll share it with the group.

Articles I’m reading —

Dan Loeb, manager of the hedge fund Third Point, put out his latest investor letter (here’s the link). He gives his current macro take (which I mostly agree with), discusses moves he’s making in his portfolio, then pitches the bull case for American Express (AXP). Here’s a cut from the letter (emphasis by me).

While current US growth remains above-trend, helped by fiscal stimulus, this positive impulse is peaking now, and will combine with an increasing drag from tightening financial conditions. This means that current above-trend growth will slow over the next year. Growth outside the US is tepid, driven by Chinese tightening still percolating through the system as markets wait for the country’s recent stimulus to take effect. While these two together imply stable growth for now, the direction in 2019 will be driven by the interplay of slowing US growth and the extent to which Chinese stimulus can lift non-US growth. Continued slowing seems more likely than reacceleration but the US economy should grow at trend. Given lack of financial imbalances and limited signs of an outbreak in inflation despite low unemployment, we still do not see any signs of an impending recession.

Thus, it is important to stay balanced and not get overly negative. The market has just been through its sharpest P/E multiple de-rating since the 2011 sovereign debt crisis. While the current 10% consensus EPS growth forecast for 2019 is probably too high, the current multiple of 16x is already discounting cuts to the 2019 consensus… We have delevered our portfolio, reduced our tech exposure meaningfully, and grown our short book. We expect to be net sellers over the next few months if markets rally but, while we recognize that we are far along in the cycle, late-cycle and end-cycle are not the same.

My sole point of disagreement with Loeb is over there currently being “Chinese stimulus”. I’m seeing a lot of people talk about this. And yes, China is actively boosting lending in certain parts of its economy but it’s massively deleveraging in others, primarily the off-balance sheet/shadow banking market. On net, I’m not seeing any meaningful stimulus at all. If somebody can show me data that says otherwise, please shoot it my way.

This is a great piece from Reuters on the increasing levels of censorship and party meddling in China’s tech sector and how its beginning to stifle innovation (link here). Xi is proving to be a lot more authoritarian than many had expected. And as China digests its enormous debt burden and its economy slows, there’s a growing chance we’ll see Xi’s despotic tendencies really flourish. Here’s a section from the piece.

“Investments into the tech space have definitely cooled down, measured by almost every metric: number of deals, deal size or fundraising,” said Zhang Chenhao, Shanghai-based Managing Partner at technology-focused Prometheus Fund.

“I think this year is the first time over the last 30 years when greed yields to the fear.”

On that note, take a few minutes and read through this interview (link) with Scott Bessent. Bessent has one of the best resumes in the business. He’s worked with Soros, Druck, and Chanos and now runs his own fund, Key Square Group. He talks Geopolitics and macro. Here’s a section from the piece where he’s referring to the Trump administration’s trade war with China.

Bessent says the key to understanding what is next is to work out how the Chinese leaders are likely to respond and react to further developments.

“They had taken on a lot of debt and they were going to try to de-lever. I think they have been surprised by the aggression of the administration so now will they re-lever?“

The other big shift is a change in attitudes among the Chinese Communist Party towards its bright young entrepreneurs. He points to Jack Ma ceding the leadership of Alibaba and the disappearance and re-emergence of movie star (and Swisse vitamins ambassador) Fan Bingbing.

“You had had this co-existence between this brutal autocratic regime and this incredibly entrepreneurial technology ecosystem,” he says.

“Maybe we have seen peak China free-market tech. They have this huge advantage because data is the new oil and they have everyone’s data.”

I agree on both points.

And finally, take a minute and read this great overview on Modern Monetary Theory (MMT) by my friend Kean Chan. Like I’ve been saying, MMT is gaining in popularity amongst policymakers and will for better or worst, likely become a major variable in the macro game next cycle. So best to study up (here’s the link).

Video I’m watching —

First, if you’ve got an hour to spare and want to hear one of the greatest living investors speak, then watch this recent CNBC interview with Liberty Chairman John Malone. He gives a masterclass on investing and how to think about the current media landscape; he also talks Disney (my largest holding). Here’s the link to the video and a link to a good summary of the talk via Josh Wolfe on the Twitter.

And if you don’t have an hour, then take just 10 minutes and watch this short presentation from one of my favorite up and coming managers, Steven Wood of Greenwood Investors. He talks about his “Builders Approach” and the commonalities amongst leaders of great public companies (link).

Book I’m reading —

I just finished reading A World Lit Only By Fire – The Medieval Mind and the Renaissance, written by WIlliam Manchester. The book reads like a gossip column of the Middle Ages. It’s filled with all types of wretchedness and depravity. I really enjoyed it.

Here’s an example of what you’ll find within its pages:

“Once he became Pope Alexander VI, Vatican parties, already wild, grew wilder. They were costly, but he could afford the lifestyle of a Renaissance prince; as vice chancellor of the Roman Church, he had amassed enormous wealth. As guests approached the papal palace, they were excited by the spectacle of living statues: naked, guilded young men and women in erotic poses… One [fete] known to Romans as the Ballet of the Chestnuts, was held on October 30, 1501… [According to Burchard’s Diarium] After the banquet dishes had been cleared away, the city’s fifty most beautiful whores danced with guests, “first clothed, then naked.” The dancing over, the “ballet” began, with the pope and two of his children in the best seats. Candelabra were set up on the floor; scattered among them were chestnuts, “which,” Burchard writes, “the courtesans had to pick up, crawling between the candles.” Then the serious sex started. Guests stripped and ran out on the floor, where they mounted, or were mounted by, the prostitutes. “The coupling took place,” according to Burchard, “in front of everyone present.” Servants kept score of each man’s orgasms, for the pope greatly admired virility and measured a man’s machismo by his ejaculative capacity. After everyone was exhausted, His Holiness distributed prizes – cloaks, boots, caps, and fine silken tunics. The winners, the diarist wrote, were those “who made love with those courtesans the greatest number of times.”

Interesting times, huh?

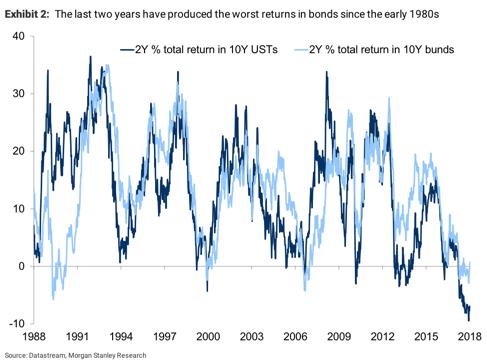

Chart I’m looking at —

Check out this chart from Morgan Stanley. It shows that the last 2-years have produced the worst total return in bonds & bunds since the early 1980s. That’s pretty amazing.

I don’t know what exactly to make of the chart, other than maybe bonds are oversold? Idk…

Trade I’m considering —

I’m seeing a LOT of great charts setting up at the moment. It looks like a bottom might be in place or will soon be (maybe one more dip lower?) and there are some stocks on firesale with nice looking tapes.

I really like some of the energy proppant stocks here, like: CRR, HCLP, SLCA, CVIA. I’ll be writing more about some of these names in my weekend Market Brief for you MO members.

But… another stock that I’m thinking about taking a swing (again) at is the Chinese online retailer JD.com (JD).

I know, I just shared all this negative stuff on China. And I am becoming more suspect of China as a viable source for long-term investing opportunities…. But, that doesn’t mean that some of China’s horribly beaten down tech names can’t rally hard in the interim.

JD, along with Tencent (TCEHY), Weibo (WB), iQiyi (IQ) to name just a few, all look like they’re geared up for a rally. What will the catalyst be? I don’t know, maybe some dovish talk out of the Fed — which we saw a bit of from Powell this week — or agreement over a framework for further trade negotiations between the US and China, who knows… The point is, there’s a ton of negative sentiment and lack of positioning baked into the China/EM pie already and it won’t take much to drive a run higher — for a short while at least.

JD bounced off a long-term support level this week (grey area below).

It’s only traded slightly lower once since its IPO. And that was in mid-2016 when revenues were nearly half of what they are today. Now JD trades at a price-to-sales ratio of just 0.6x. Yet, the company is growing revenues over 20% YoY. That’s nuts.

These kinds of multiples make sense if you have high conviction that China is on a fast-track to becoming a North Korean/Venezuelan communist backwoods. I think that’s a real possibility but I wouldn’t say I have high conviction nor do I think it’s going to happen quickly… So maybe JD or some of these other China tech names are worth a punt?

Fred Liu, manager and value investor at Hayden Capital, remarked the following on JD in his latest investor letter. Actually, his whole letter is worth a read if you get a chance. There’s a really interesting bit on position sizing and portfolio risk in it, but I digress… Here’s the link to the report and some of his thoughts on JD.

The broader thesis outlined in our previous letters remains largely intact. Simplistically, the company is on track to do ~$70BN in sales this year, and $100BN in 2020. Electronics and appliances make up ~75% of JD’s revenue mix, which due to the nature of the categories carry lower-margins vs. say apparel or general merchandise (see below for Alibaba’s TMall take-rates, as an example). If JD can simply maintain a 2-3% margin on this category, the profits by 2020 would reach at least $2BN. This would equate to a 16x EV/EBIT multiple, growing at 20% y/y.

Additional levers, such as category expansion into FMCG (similar margins, smaller order sizes, but higher order frequency / volume) or general merchandise (higher margins, smaller order sizes) would give the stock considerable upside optionality. This gets even more attractive if we back out the logistics and finance divisions, which have both raised external funding and may be individually listed at some point. Excluding these divisions, with JD’s stake worth ~$24BN (at the last round valuations), the core retail part of the business comes down to just a ~5x multiple.

I’m not one for pair trades but short BABA (trading at over 9x sales) and long JD doesn’t seem like such a bad idea here.

Quote I’m pondering —

There are no limits. There are plateaus, but you must not stay there, you must go beyond them. If it kills you, it kills you. A man must constantly exceed his level. ~ Bruce Lee

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. Alex posts his mindless drivel there daily.