The best trades are the ones in which you have all three things going for you: fundamentals, technicals, and market tone. First, the fundamentals should suggest that there is an imbalance of supply and demand, which could result in a major move. Second, the chart must show that the market is moving in the direction that the fundamentals suggest. Third, when news comes out, the market should act in a way that reflects the right psychological tone. ~ Michael Marcus

Michael Marcus is one of the original market OGs. He cut his teeth at Commodities Corp where he was one their star traders alongside PTJ, Kovner, and Ed Seykota.

Marcus combined fundamentals, technicals, and sentiment — what we refer to as the ‘Marcus Trifecta’ — to analyze markets. This allowed him to turn $30,000 into $80 million over a 20 year period. Not too shabby.

This is the approach we use here at MO to view markets. In this piece, I’m going to share an excerpt from two Market Briefs that went out to members of our Collective recently. The hope here is to first show you some of the tools and processes we use to assess markets. And secondly, to give you an update on what we’re currently seeing through this ‘Trifecta’ lens (this is complimentary info to the note we sent out yesterday).

The following excerpt is from our Brief titled “A Roadmap” published May 29th.

~~~~~~~~~~~~~~~~

Let’s quickly layout where we are and how we got here. And then we’ll get to where we’re headed in the weeks ahead.

In our April 23rd Brief “Japan Going On Leave” we began noting how the rally had gotten “long in the tooth” and there were increasing “signs of growing complacency and technical divergence”. We talked about how the Russell small-cap index had “failed to confirm the broader market rally” and that not only had credit and spreads “turned over a bit” but sentiment and positioning were becoming stretched, writing:

The majority of investors have been on the outside looking in at this rally since the start of the year. We’ve talked about how this move will persist until it finally creates enough FOMO (fear of missing out) to suck in these players who’ve been sitting on the sideline.

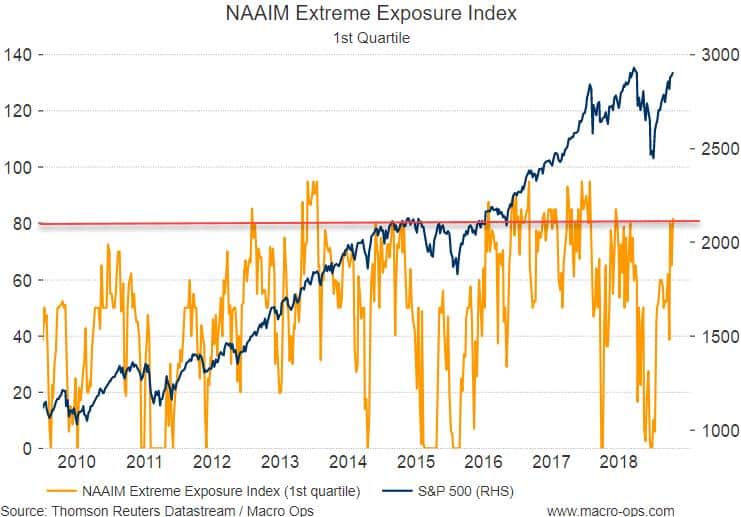

While we likely have a bit more to go before we get total capitulation from the bears. There’s an increasing number of signs that we’re getting close. Take the NAAIM Extreme Exposure Index which measures the top quartile of investor’s weighting to risky assets. It recently pierced the 80 level (horizontal red line). Readings above this point suggest a number of investors are getting over their skis a bit which makes the market more susceptible to a pullback.

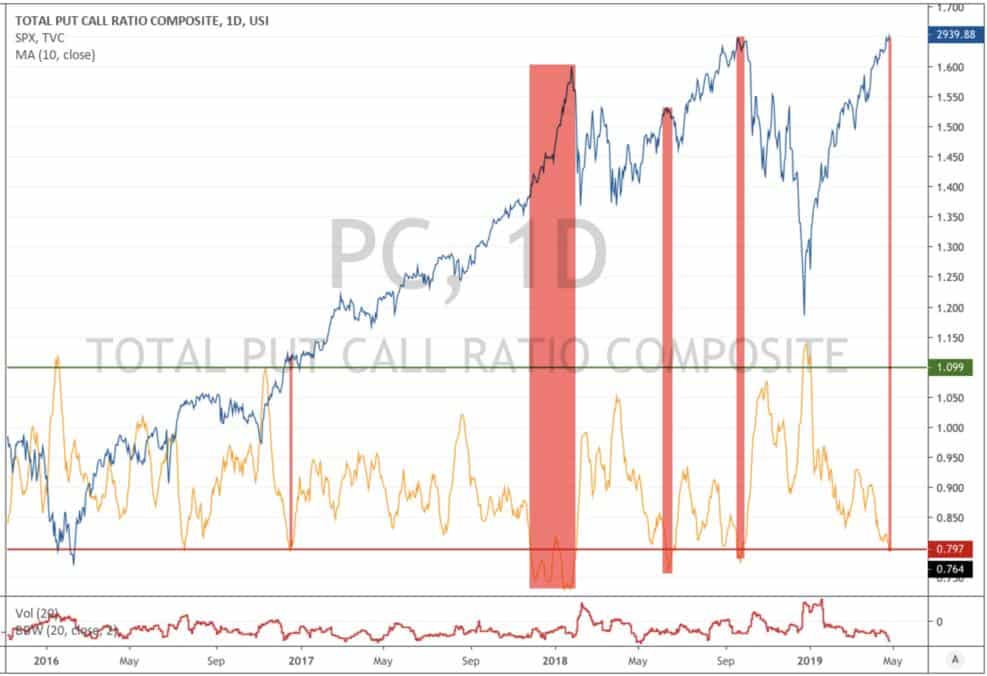

Then in our following Brief “Creeping Complacency” we pointed out that “ Our 10-day moving average Total Put/Call indicator crossed below the 0.8 level (marked by the horizontal red line below) triggering an official sell signal on Friday. Investors are buying less downside protection and are becoming complacent. The lower this indicator moves the greater odds are that we’ll see a sizable correction in the coming weeks.”

We concluded with “My general market take remains the same. The rally is getting long in the tooth and there are some increasing signs of FOMO — note the resurgence of the “Melt-Up” narrative that last became popular in the runup to the Jan 18’ blow off. But momentum and technicals still favor more upside for the time being.

The move here is to stay long but begin to trim risk and take some profits off the table. Once momentum fades and more technical cracks appear we’ll move to more aggressively reduce our equity exposure and put on some shorts.”

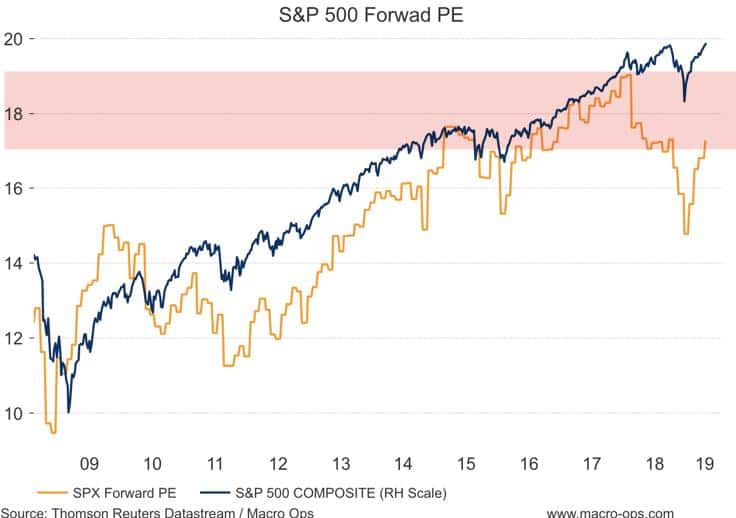

The following week we wrote in the MIR that “The Forward PE ratio of the SPX is back up in the 17+ range. A level which has caused some instability for the market in the past.”

And ended with:

My indicators are telling me that we’re headed for a broader market correction in the coming weeks. I’m not expecting this to be a big selloff like the one we experienced in Q4 of last year but it could be significant in some of the individual overstretched names.

…We’ve been writing since last December that the majority of the market has been on the outside looking in at this rally and that the time to get defensive will be when those on the sidelines begin giving into FOMO and piling stocks. It looks like that is starting now. Momentum may carry us higher for a bit longer but we’ll be taking this time to begin reducing our exposure to some of our more richly valued growth names and allocating more to our value names above.

Sentiment, technicals, and macro… The “Marcus Trifecta” is a very useful approach for hitting broader market turning points. The signs for this current selloff were there for all to see who knew where to look.

***Here’s the conclusion to our most recent Market Brief “The Market is Teeing Up…” from which yesterday’s macro indicator discussion was pulled.***

…. We have macro fundamentals which are slowing but still positive and far from signaling a recession is nigh. Depressed yields fatten the risk premia on offer from risk assets, making stocks appear more attractive. The consensus earnings estimates have been driven down to very manageable levels which should make for easier ‘beats’. Sentiment, positioning, and technicals are all pointing to a significant market bottom in the coming weeks. On top of all this, we have a US dollar that looks like its breaking down. A lower dollar = a tailwind for US earnings and easier financial conditions for EM stocks, not to mention a big positive for commodities.

Back at the end of March, I wrote There’s a Big Macro Move Brewing in Markets noting the record low asset volatility we were seeing in major dollar pairs and precious metals. I laid out how these compression regimes usually lead to expansionary ones (ie, BIG TRENDS). I think we’re going to see that start very soon.

There are a number of trades setting up that are making me excited. There are energy and shipping names trading at 1x normalized free cash flows and I’m seeing signs that investors are FINALLY starting to allocate money to the sector — I’ll write more about both soon. There are fantastic shorting opportunities lining up in the overvalued tech names. And we have bonds that are in the process of putting in what looks like an intermediate blow-off top.

I’ll be putting out a series of notes and trade alerts for Collective members in the coming weeks to update you on things as they unfold and as we make moves in our portfolio.

There is a tide in the affairs of men,

Which, taken at the flood, leads on to fortune;

Omitted, all the voyage of their life

Is bound in shallows and in miseries.

On such a full sea are we now afloat,

And we must take the current when it serves

Or lose our ventures.

~Shakespeare

Time to take the current…

~~~~~~~~~~~~~~~~

Honma Munhisa, the 18th-century Japanese rice trader who invented Candlestick charts, is believed to have amassed a fortune of over $100B in today’s money trading rice futures. He learned early on that making money in markets is as much about “Playing the Player” as it is about understanding the fundamentals. He wrote:

When people run to the West, I turn to the East. When the rice price starts going up, orders rush in from everywhere all at once, and soon the Osaka market becomes part of the show as well. The rice price goes up faster when people place orders even for stored rice and it becomes more evident that a buying spree is taking place. But when you wish to be in the position to place buy orders like everybody else, it is important to be on the side of those who place sell orders. When people move in unison, running towards the west with determined intention to be part of the rally, it is time for you to head to the east and you will discover great opportunities.

Looking at the market it seems like there are a lot of people crowding to one side or “running to the west”.

The last time I saw sentiment hit similar levels relative to the fundamentals was in late December of last year. On December 18th, I wrote the first of many bullish notes titled “The Bullish Case for US Stocks” commenting on the extremes in sentiment and narrative, ending with “I believe US stocks are setting up for an extraordinary buying opportunity in the next 1-3 weeks. I see a LOT of amazing deals in stocks and I’ll be putting out our Macro Ops shopping list later this week.”

The Trifecta of data tells me we’re about to see a similar bottom very soon.

It might be time we start running to the East…

Before you go, we’re currently doing an open enrollment for our premium macro research offering called The Macro Ops Collective. If you want access to our latest and greatest stuff click the link below and make sure to sign up by June 9th at 11:59PM EST!