Last week’s essay covered AI in Education and the myriad companies attacking the space. I ended the post by saying we’d cover AI in Finance this week. That changed when I looked closer at Pearson (PSON). The stock had everything we look for at Macro Ops:

-

- Improving fundamentals

- Long-term industry/secular tailwinds

- Technical confirmation from the tape (price chart)

I sent this write-up to our Macro Ops Collective members over the weekend to prepare them for a potential buying opportunity this week. The opportunity is here and we wanted to share our thoughts with you as well as how we’re reading the tape.

But before we dive in I want to tell you about our premium service, the Macro Ops Collective.

The Collective is our full-kit soup-to-nuts service that provides research, theory, actionable trades and a killer community that consists of dedicated traders, investors, and fund managers from around the world. We’ve been told that there’s nothing else like it on the web.

If you’d like to tackle markets with our group (whom I should say has been having a great year in markets). Just click this link and sign up. And, as always, don’t hesitate to shoot me any Qs!

Alright, let’s get to our turnaround idea!

Pearson PLC (PSON): From Overpriced Textbooks To A Digital-First Platform

Pearson (PSON) built its legacy business selling overpriced textbooks to college students. Then Chegg came along and eliminated the need for those expensive hunks of paper. The company recognized this and is now leading an effort to turnaround the antiquated model.

Elevator Pitch: If it works, PSON will transform from a publisher of overpriced books to a fully digital learning platform powered by AI and massive amounts of student data. Mr. Market still values PSON like a textbook publisher as the stock trades <2x EV/Sales and <10x EV/EBIT.

The Problem: College Textbooks Are A Scam

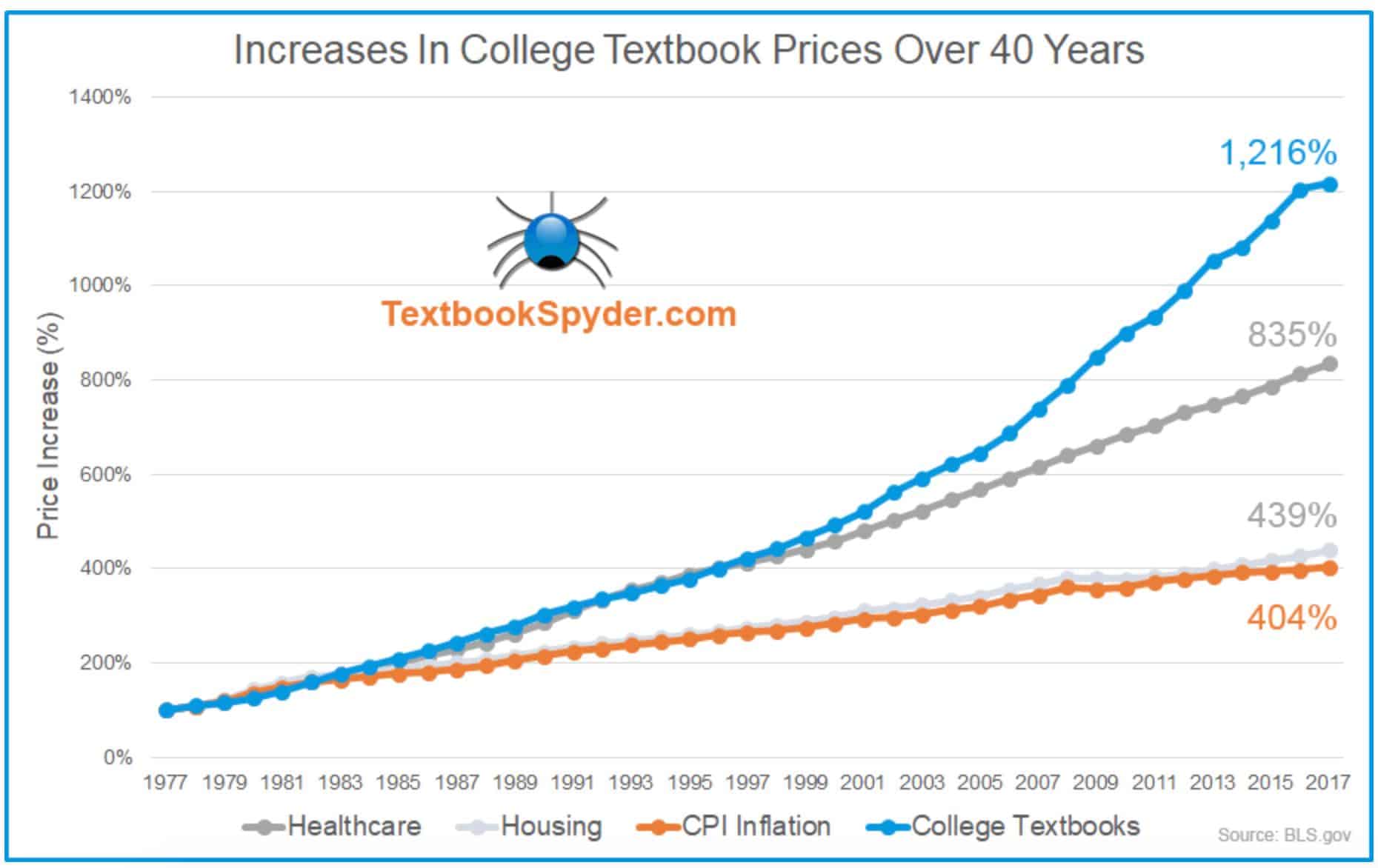

College textbook prices are one of the largest scams in the US. Prices have risen a cool 1,216% since 1977. For context, healthcare prices increased 835%, housing increased 439% and inflation another 404%. The reason for the price increase is equally sinister. College professors mandate certain textbooks (usuall written by the professor) as prerequisites to pass a class. Don’t have a textbook? You won’t pass the course.

prerequisites to pass a class. Don’t have a textbook? You won’t pass the course.

This forced students (or their parents) to pay whatever cost for that “required” textbook. Not to mention paying for the class itself.

And we can’t forget the classic “updated” textbooks. You know the ones with an extra chapter for brand new material? Or an updated version that rearranges pages and chapters. These tactics ensure publishers and professors get paid at the expense of students’ wallets.

The Workaround Solution: Re-used Books and E-Books

Students eventually adapted to the highway financial robbery. They bought used textbooks and shared notes on Chegg. This led publishers to introduce e-textbooks, which seemed like the logical thing to do. Yet the early e-books weren’t made for a digital-first world.

They were clunky with terrible user interfaces (UI). E-textbooks also Ied publishers to include one-time activation codes in physical textbooks. That meant students had to buy the physical copy of the book to get access to the online edition.

The one-time activation codes led to the same problem students encountered with “next edition” physical textbooks. You can’t resell a one-time activation code.

The one-time activation codes led to the same problem students encountered with “next edition” physical textbooks. You can’t resell a one-time activation code.

Against this backdrop it’s easy to see why Chegg’s (CHGG) stock price rocketed over 500% since IPO. CHGG has generated a 50% CAGR since IPO.

At the same time, traditional hard-copy publishers like Pearson experienced declining sales and lower stock prices. Check out the 10YR stock chart of PSON below. It’s ugly.

So now textbook publishers have a choice. They can either stick with the hard-copy book sales and one-time fees that rob students.

If they do that they don’t have to overhaul their business plan. They can keep the status quo. That puts them at risk for insolvency as companies like CHEGG take more market share over time.

The other option is to accept that the future of textbook/learning material is fully digital. While this seems like the smart choice, it’s a difficult one to make. Accepting that reality means entire organizations rearranged to optimize in a digital-first world.

Pearson Bites The Bullet

PSON accepted this reality in 2012 under the direction of then-CEO John Fallon. Fallon’s 2012 Shareholder Letter revealed insights into how PSON thought about the initial transformation.

PSON accepted this reality in 2012 under the direction of then-CEO John Fallon. Fallon’s 2012 Shareholder Letter revealed insights into how PSON thought about the initial transformation.

The letter also puts things in perspective. By 2012 PSON generated nearly 50% of its revenue from digital sales. A turnaround of this magnitude for a company of PSON’s size takes time.

The company became the first education publisher to take a digital-first approach to textbook publishing and education content delivery.

Here’s a few of my favorite quotes from the letter (emphasis mine):

“We wanted to make a radical shift from traditional print products to digital and services businesses, and, for the first time in Pearson’s history, those now account for half of our revenues. We aimed to become a significant player in the world’s most dynamic education markets, and Pearson is now a meaningful education company in China, India, Brazil and Southern Africa.”

“This shift to digital is profoundly changing the business model for content: it means one-off sales will diminish while subscription sales, most bundled with services, will grow. That same shift to digital causes considerable change and consolidation in the retail channel, with a dramatic shift to online sales and different sales patterns for physical and digital formats.”

“We need to shift resources more quickly from textbook publishing activities, primarily in the developed world, where demand is flat or declining, so we can invest more quickly in our fast-growing digital and services businesses, with a special emphasis on emerging markets.”

Despite this commitment to digital transformation, the company’s struggled to grow revenue and profits. Check out the declines in each category since from 2012-2019:

-

- Revenue: -$1B

- Gross Margin: -$761M

- Operating Profit: -$214M

There’s a few reasons to explain the decline in PSON’s operating metrics. First, the company continues to churn print sales to digital sales. Print sales commanded 80% of PSON’s business in 2010.

A legacy revenue base that high takes time to flow through the income statement. Second, digital sales look different than print sales. PSON could charge hundreds of dollars per physical textbook. Under a digital subscription-based platform PSON relies on textbook rentals, which they charge roughly $40/book. That’s a huge difference.

In other words, you wouldn’t see the business’ transformational success if you only look at the financials.

The company’s determined to see the transformation through. Less than two weeks ago PSON sold its Institute of Higher Education to Stellenbosch Graduate Institute and EXEO Capital. This sale fits with PSON’s mission to shift from physical, large-scale textbook delivery to digital-first platforms.

Eventually PSON needs to grow revenues, expand margins and increase profits to command higher market multiples.

Let’s see how they plan to do that.

The Pearson of Tomorrow: Digital First

PSON grew its digital sales from 20% of revenue in 2012 to 66% in 2019. The company expects its core US Higher Education Courseware (largest segment) to be ~100% digital by 2022. To catalyze the transition to fully digital, Pearson will rely on three product innovations:

-

- Aida: The world’s first AI-enabled Calculus app

- Pearson Learning Platform

- Next Generation Pearson eText Textbooks

In fact, we can distill PSON’s future success down to its Pearson Learning Platform (PLP). The PLP acts like an operating system for students and teachers. A way to share educational content and learning material in a one-stop-shop environment.

It feels like a Netflix distribution model. Pearson provides the platform for viewers (students) to consume content (ebooks, interactive learning, etc.) on the platform. It also allows teachers and authors to revise texts and material on an “as needed” basis.

By slashing costs and controlling distribution, PSON’s model becomes a lot more attractive to students and investors.

This allows them to generate more data on students than any other learning company. How? Because they’re the largest publisher of education content on the planet. And that entire library (1,500+ titles) becomes digital and data-able (made-up word?). Over time, that creates a Data Dominance amongst students and universities that other companies can’t copy.

The idea of PSON as the “Netflix of Education” isn’t new. CIO Albert Hitchcock mentioned this in a2018 Forbes Interview. Here’s a snippet of the conversation (emphasis mine):

“The intention of the message was to have the viewpoint that we needed to move to a platform type of model where we have all our products, services, and capabilities that we deliver to our customers in a single ecosystem. A great deal has been written around this model at Pearson, and that is especially relevant as our company grew through acquisitions. Ours is a diverse business that is over 170 years old and has had many different types of companies under the umbrella of Pearson for many years.”

Hitchcock elaborates further, saying “It would be game-changing for not only Pearson, but for the entire industry if we could create that single platform, similar to Netflix, Spotify, and Amazon. This platform would be highly scalable, global in nature, high-quality, and a platform that could deliver all our experiences around the world to millions of learners.”

Let’s dive deeper into Pearson’s Learning Platform. Jack Graham, who ran UI/UX for Pearson’s REVEL product was tapped to help Pearson’s Learning Platform. He has an entire blog post about his journey with PSON. Here’s what we learned:

“We created a series of definition statements across the three main user roles expected to exist in the software. From these, we were able to derive focused “How might we?” questions to advance during ideation. Based on what we learned during the discovery process, we felt it would be a high priority to improve the experience for creating new courses and assigning material within them over past products.“

“In a marketplace where premium products are subject to disruption by free alternatives, proving the efficacy of their products was key to Pearson’s strategy. Equipping instructors with timely feedback on student mastery of learning objectives was one way of implementing this strategy.”

On one hand we can say PSON’s platform benefits from “Netflix-like” distribution capabilities. But there’s another competitive advantage at play: Name Recognition.

Like Moody’s or S&P for bond ratings, the Pearson name carries weight in the education community. As the world leader in education publications, the PSON name brings with it a sense of quality and dominance. When people think of college textbooks, they think of Pearson. This helps explain why PSON controls nearly 43% market share as of 2018.

Numbers To Narratives

PSON has an opportunity to take share as the go-to digital learning platform for the next generation of learners and educators. If they do, they’d rapidly transform their business from a lower-margin print business to a high-margin software company.

Let’s assume the company can turn things around and complete this transformation. What would their run-rate margins and cash flow look like? What type of multiple would the market pay for that type of company?

We can use Blackboard as a proxy for what a digital-first education company’s margins would look like. Blackboard generated ~21-25% operating margins. Let’s assume PSON gets to 25% OM by 2025. Revenues will take a hit this year (-10%), but should bounce back in 2021 forward. BY 2024 PSON would generate 4.27B in revenue.

The transition to a digital-first business brings with it higher margins. We’re assuming PSON grows GM % from the low-mid 50s to the low 60s. This gives us 2.65B in 2024 Gross Profit. At the same time, they’ll spend less in SG&A, decreasing from mid-40% to low 40%. That gets us to 22% operating margins by 2024, or 940M in OI, 779M in after-tax income and 800M in FCF.

This gives us 7.3B in PV of Terminal Value. Adding our cash flows gets us 9B in EV. Subtract net debt and we’re left with $12/share in shareholder value (100% upside).

If the company manages the turnaround, they’d increase Operating Cushion from 8% to 22% and sport a 17% FCF Growth Profile.

Risks

PSON is a turnaround with myriad risks. The company hired Andy Bird to replace John Fallon, indicating a bit of a CEO carousel. While rotating CEOs isn’t ideal, Andy Bird’s early stats show promise. 84% of employees approve of the new chief.

The company also sports a -2 NPS rating. We think this improves as the company transforms to a digital-first platform better able to serve customers. Glassdoor ratings show 60% of employees would recommend the company to a friend.

Finally, price is in a sustained downtrend. This makes it harder for the stock to turnaround as it faces overhead selling pressure.

Reading The Tape

There’s no hiding the fact that PSON is a turnaround story fraught with difficulty. Turnaround stories can frequently make new lows and end up on 52-week low lists. As such, we want to ensure we’re buying at an inflection point in the market.

PSON’s chart tells the story of a company whose shareholders are seeing the benefits of their transformation. The stock is breaking out of a 11-month symmetrical triangle reversal pattern above the 50MA.

We’re watching the 200MA as potential resistance but like the long-term Reward/Risk set-up if the stock closes above the chart pattern boundary line on the weekly timeframe.