I’ve got some bad news…

According to this guy, there’s at least a 70% chance we enter a recession next year, maybe sooner.

It’s not just James of “Financial Education”. It’s literally every popular social media influencer on youtube predicting a major slowdown in the economy over the next 12-months.

I guess it’s time to sell our longs and leverage our shorts guys, and gals. Praise be to these high-minded Tubers who bless us with their all-knowing economic wisdom…

Alright, enough sarcasm.

I’ll be honest, the probability of a recession has increased since the start of the year. It’s gone from basically nill to maybe 35% odds we’ll see one in the next 12-months — these are very fudgy numbers just fyi. I should note that I will adjust these numbers dramatically and without shame, if the data significantly deteriorates or improves.

And therein lies an important point. What’s up with everybody’s obsession in trying to predict a recession, anyway?

I get it if you’re a business owner and you don’t want to take on too much leverage before an extended slowdown in the economy or something. But as traders and investors who mostly deal in highly liquid instruments why spend so much time and effort on trying to play Nostradamus and predict what’s going to happen to something as complex and dynamic as the US’s $20trn economy 12-months out?

I’m not saying it’s not important to pay attention to the macro trends — of course, it is, we’re macro traders after all and I’ll walk you through our basic recession dashboard here in a sec. What I am saying is that I think there’s a not too small population of traders and investors out there (maybe even the majority) who see a recession around every corner and react to every dip in the market as if it’s the BIG one.

I’m guessing they’re playing the “let me show everybody how smart I am versus making money game” that we talked about earlier this week. That or they’re trying to sell a newsletter. Hey… being bearish sells. That’s why you see so many unapologetic bears on Twitter who’ve been spewing doom and gloom for the last 7-years. It’s making them money, not investing money, but loads of subscription money…

Thank GOD these people exist because they create the wall of worry that drives the beautiful bullish trends for us to exploit.

I digress…

Here’s how I think about recessions.

Actually, first, a quick PSA.

Recessions are not two consecutive quarters of negative real GDP growth as most think. Rather, the NBER defines them as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.” Formal recessions aren’t identified until well after the fact.

Now that we have that out the way. Here’s how I think we should think about them.

Traders and investors don’t trade recessions. We trade the market. The market performs poorly in a recessionary environment. Dips that were once bought, tend to be sold. And a consecutive number of lower highs and lower lows in the indices, spawn a bear market. During this time we want our bias to be to the short-side.

The market is one of the “best predictors of recession” as Stanley Druckenmiller likes to say. Our collective wisdom is actually pretty intelligent — and sure there’s a reflexive self-fulfilling component in there too. This is why the SPX peaks on average 7-months before a recession hits. And yeah, the market will give false signals from time to time but that’s where the rest of our “weight of the evidence” comes in handy; to tell us if this dip is really the start of a new cyclical trend or just another vanilla bull market retrace.

I guess that’s the point I’m trying to make. We play the technicals in front of us while keeping an eye on what’s on the horizon. But we’re limited in how far we can see. Things are always a little hazy when they’re further out in time. It’s counterproductive to spend much time or energy playing the prediction game (again, unless you’re trying to raise AUM or sell a newsletter) when instead you should be teeing off what’s happening in the market and its internals, now.

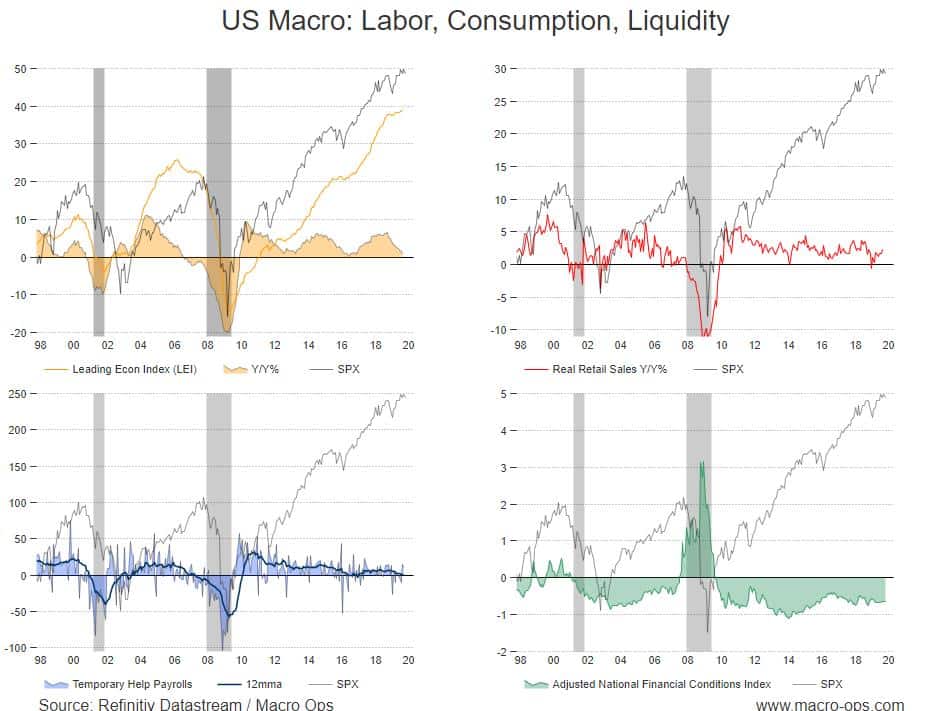

You can do better by spending just a few minutes every month going through the Recession Dashboard below. Flip through our leading and coincident indicators and then put them in context with what the market is saying (which I talked about earlier this week).

We want to look at this data holistically. Remember, it’s about the weight of the evidence. Not what one or two indicators are doing.

As of right now, the odds of a recession are fairly low. The LEI, which has led every recession (median lead time is 10-months) since its creation roughly 50-years ago, is at cycle highs. So is New Housing Starts. Initial claims troughed 5-months ago but they haven’t started trending up and are still well below their 36-month moving average. The 2s10s yield curve only briefly inverted 2-months ago and that one tends to have a long lead.

*** Click on the indicators to see the charts***

| Early U.S. Recession Indicators | ||||

| Indicator | Median Lead Time | Current Cycle | Key Recession Level | Current Level |

| Conference Board LEI Peak | 10-months | New cycle high | Negative YoY% | +1.08 |

| Yield Curve Inverts (2s10s) | 19-months | 2-months | NA | NA |

| Initial Claims (4wk avg) Trough | 8-months | 5-months | 36-month MA crossover | Well below |

| SPX Peak | 7-months | 2-months | Below 50-week MA | Above |

| New Housing Starts Peak | 28-months | New cycle high | NA | NA |

| Leading/Coincident U.S. Recession Indicators | ||

| Indicator | Key Recession Level | Current Level |

| Consumer Confidence Index | 36-month MA crossover | Above |

| Breadth of Philly Fed State Leading Indexes | Below 0.7 | 1.4 |

| ISM Manufacturing Index | Below 44 | 47.8 |

| ISM Non-Manufacturing Index | Below 51 | 52.6 |

| Conference Board’s Business Confidence Index | Below 43 | 34 |

| Unemployment Rate | 12-month MA crossover | Below |

| Real Retail Sales YoY% | Negative YoY% | +2.3% |

| Adjusted National Financial Conditions Index | Above 0 | -0.65 |

| Kansas Fed Financial Stress Index | Above 0 | -0.35 |

The real weakness has been in the soft data. The ISM and Conference Board Surveys. The CB CEO survey is abysmal. No doubt some, or much, of that weakness can be attributed to the trade war. The rest of the data shows a slowing though still positive growth economy.

Financial conditions remain incredibly loose. Consumers are still spending and the labor market isn’t showing signs of serious deterioration.

If more of these indicators begin to flip red and we start to see the US market turn down along with participation begin to crumble, then we’ll want to update our odds. Until then, focus on the market trend.

One final thought that I want to leave you with today.

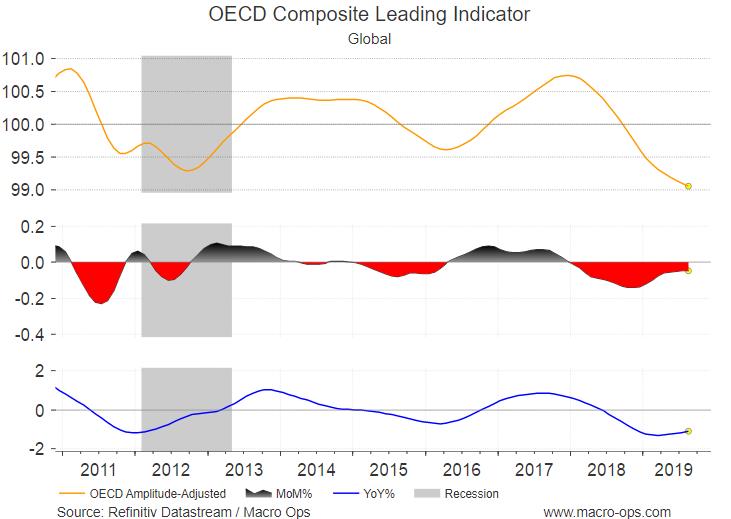

The US and rest of the world (RoW) decoupled about 18-months ago. Growth in the US and ex.US began to fade going into 18’ due to decelerating Chinese credit growth and the US moving to the backend of a large fiscal impulse (tax cuts) — yeah sure, the trade war mattered too but not as much as everybody thinks. And while the US stayed buoyant, mostly thanks to a strong consumer. The RoW flipped over on its belly…

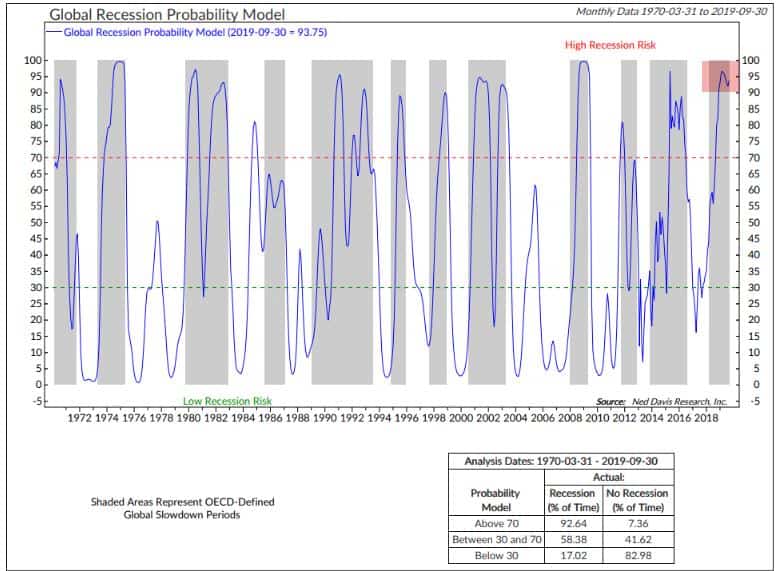

This is why most ex. US markets have spent the last 21-months or so in a bear market downtrend or, at best, sideways range (as I noted here). Much of the world was in a recession as shown by NDR’s Global Recession Probability Model below.

This slowdown began in earnest in the spring of 18’. Ex. US slowdowns tend to last 14-months on average which would put this one ending sometime around now, give or take a few months.

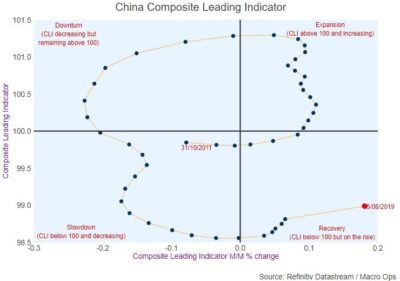

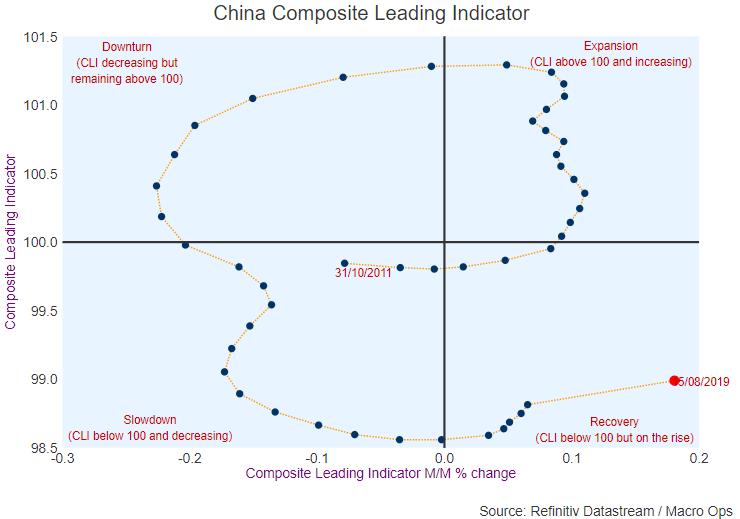

Now China is a black box and I prefer to consume a large helping of salt when I look at their numbers (and why I like to check their data against 3rd party sources). But, there are tentative signs that growth may be in the process of bottoming.

We shouldn’t expect to see global growth hockey stick as we saw in 16’. The CCP has made it clear they’re serious about reigning in leverage so a flood of Chinese credit probably isn’t on the way. But… the CCP is even more concerned with keeping Chinese unemployment low and social sentiment elevated. So maybe we see some more easing at the margins from them which makes for a decent if underwhelming bounce in global growth.

If this ends up being the case… well, let’s just say there’s a lot of money that’s offsides and will need to be put back to work…

But then again, who knows… maybe Jeremy and all the other Tubers end up being right. Maybe we do get hit with a recession in 2020 — it’d be the first time that I know of where we all saw the big one coming.

Really, that’d be fine too. The tape will tell give us a heads up and our data will confirm the tape.

P.S. Fall enrollment for the Macro Ops Collective has begun! We regulate the number of new signups because we’re going for quality over quantity and want to make sure we’re able to provide the most value to our fellow Collective members as possible and keeping the inflow limited helps us do that. If you’re interested in checking us out then go ahead and click this link here to see what’s on offer or feel free to shoot me an email with any Qs you may have at alex@macro-ops.com.

Either way, thanks for being a reader and good luck in the markets.