Last we discussed R&D costs and whether we should expense or capitalize such investments. You can check that out here.

This week we’re shifting gears and focusing on a reader’s request: Other Income (OI, for this article)

I love this topic and can’t wait to dive in.

Let’s go!

What Is “Other Income”?

Remove line items on an income statement and you see nothing but revenues, expenses and bottom-line income. If that were the case, we’d have no hierarchy of income streams.

But GAAP does separate the income statement by line items. And we do have a hierarchy of income streams.

This is where we see the term other income. What is OI? In short, its earnings generated outside normal business operations. The keyphrase here is normal business operations.

Such earnings include:

-

- Interest

- Gains on investments

- Sale of long-term fixed assets

- One-time gains on credits

It’s one thing to know this exists. But why does it matter?

Why Should We Care?

It’s important to know where and how a company generates profits. The more a business earns outside its normal operations, the less reliable the income.

If a company can’t generate profits from its core business we shouldn’t buy it. But many investors buy companies that look cheap thanks to one-time other income gains.

Why do they buy them? Quantitative value screens. Think about it. Screens don’t discern between “OI” and “core income”. All they see is the bottom-line number. A company that generated a large OI gain will look cheap on that basis.

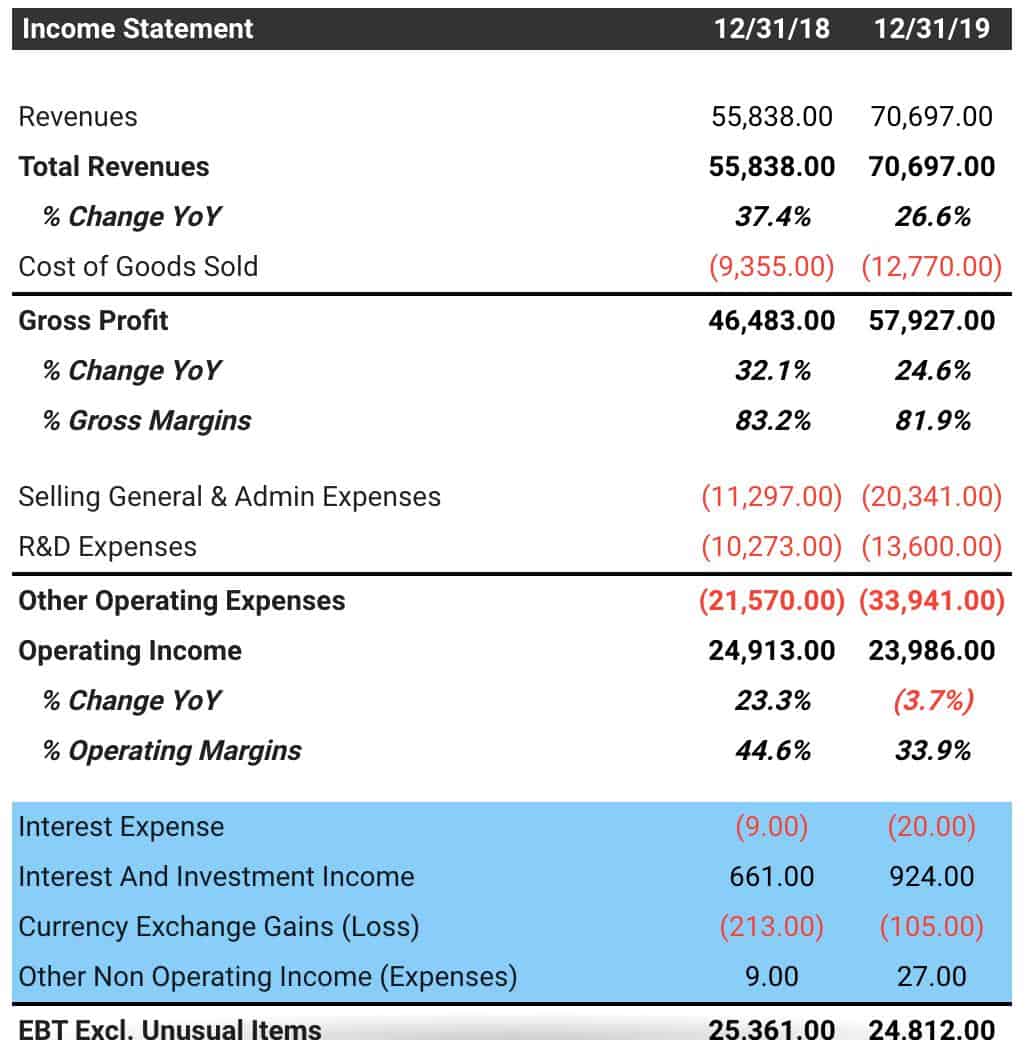

“OI” Example: Facebook (FB)

Let’s use FB as an example for OI. Check out FB’s last two years’ income statement numbers (via TIKR):

The line items highlighted in blue are sources of OI.

You can see that it doesn’t matter in FB’s case. They generated nearly $24B in core operating income in 2019. $800M in OI is a simple rounding error.

But that’s not the point. The point is to train your eye to look for these line items. Because not every company looks like FB.

How To Gauge Other Income Severity

OI analysis is important. It tells us whether a company generates most of its earnings from its core business. Or if other (unreliable) streams of income bolster the bottom-line.

Here’s a quick heuristic to gauge whether a company’s OI is something to worry about.

OI Ratio: “Other Income” / EBIT

This ratio reveals how much of a company’s total operating income comes from its other earnings sources. Higher ratios signal less reliable income streams.

But again, everything comes with a caveat.

The best way to run this ratio is over time on a rolling basis. We shouldn’t punish companies for true one-time asset sales or restructurings.

Examine this ratio over the last five years. What’s the trend? Is it consistent? These questions help pinpoint exactly how the company truly makes their nut.

If you have any questions feel free to reach out.