I think this is one of the more interesting charts in markets right now. It’s a monthly of the MSCI Emerging Market Index (EEM). The chart shows EEM breaking out to the upside of a 10-year wedge last year before reversing back down and testing the upper line of support. It’s down approximately 12% on the year.

The big question is whether this retest offers an excellent risk-to-reward buying opportunity or if this is the start of a larger downward trend.

I believe it’s the latter. Here’s why…

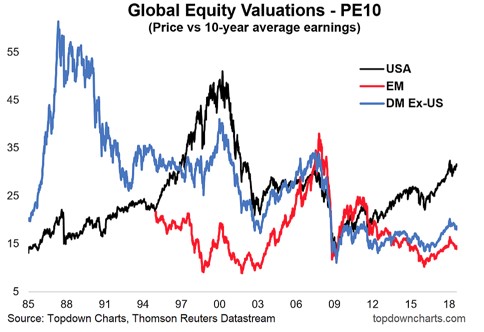

The selloff has widened the US/EM valuation gap, making EM stocks very attractive on a purely relative valuation basis (chart via Topdown Charts).

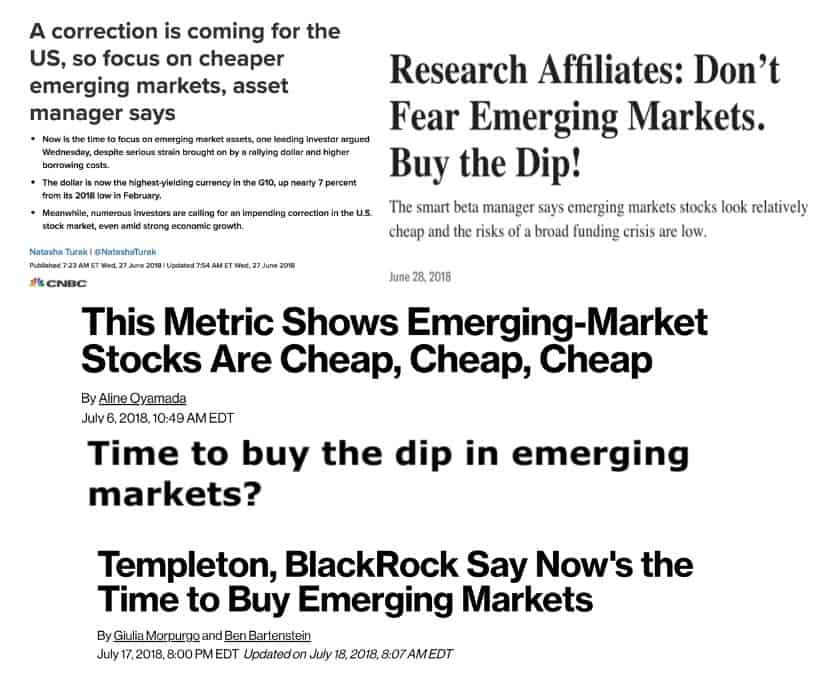

This notable valuation gap has spawned the popular market narrative that buying the EM dip is the ‘prudent’ to thing to do. Here’s some financial headlines from over the last few months.

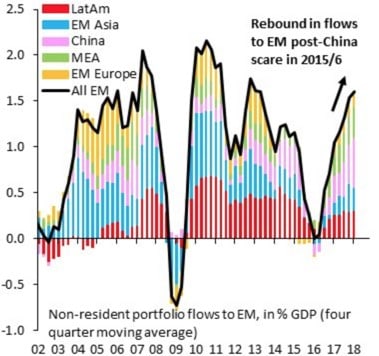

This narrative has led to a large amount of capital flowing back into EM following the 2015/16 China scare (chart via IIF).

And here’s the big tell… Capital flowed out of EM from 14’ to 16’ as China was trying to slow its debt growth. That capital then came rushing back into EM as China injected massive amounts of liquidity into its economy in early 2016.

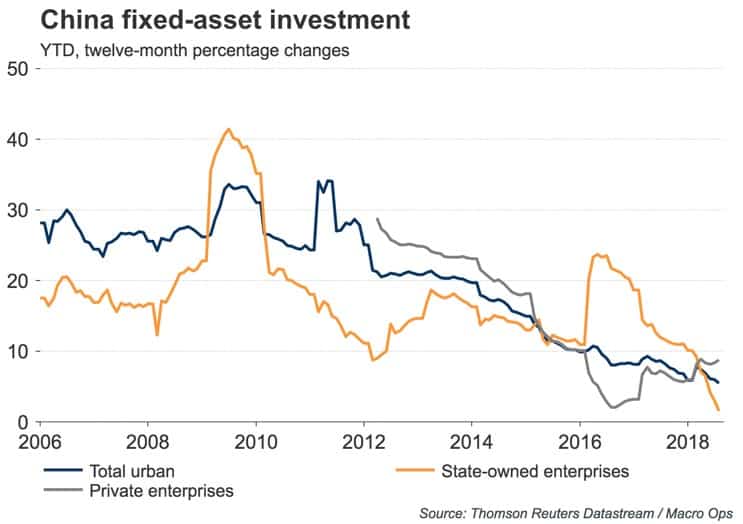

Looking at China’s fixed asset investment (FAI) by state owned enterprises (SOEs) provides a good measure of their fiscal policy, as SOEs are their preferred channel for juicing economic growth by building more high speed rail, bridges, and even entire cities.

You can clearly see the instances where China opened the FAI spigots (orange line) in 09’, 13’, and 16’. Following each of these instances, investment flows came pouring back into emerging markets.

There are two reasons for this (1) China is a large economy and comprises roughly a third of the MSCI EM index and (2) China has become such a large source of global commodity demand that when it slows its leveraging (ie, reduces its frenetic pace of building) that drop off in demand reverberates throughout the rest of the world, hitting EM growth particularly hard.

The graph below via KoyFin shows how Asian, and in particular Chinese stocks, dominate the top 10 weighted holdings of the index.

Knowing how important China is to the wellbeing of EM, it should be concerning that its preferred method of adjusting demand has collapsed from 23.5% yoy growth last year to just 1.5% growth today — its lowest level in 15-years.

This slowdown in China’s leveraging — we can’t call it a deleveraging yet because it appears their rate of debt growth is just stalling and not reversing yet — is largely what’s behind the diverging economic growth projections for the US and EM.

While everybody is focused on the Fed raising interest rates and quantitative tightening— an important variable because of its effect on the USD exchange rate — hardly anyone is talking about the potential impact of a critical drop in Chinese growth and demand.

This is probably because (1) The China bear argument suffers from “Chicken Little” syndrome. People have been calling for China to implode for nearly two decades now and yet the country has managed to keep trucking along and (2) Everyone assumes that China will just keep mainlining credit at each hint of economic instability.

But there’s increasing evidence that things are different this time around. That, in fact, Xi and the CCP are committed to fixing the imbalances in their economy and stomaching the necessary pain that goes along with doing so.

If we’re correct, this will have critical second and third order impacts on the rest of the world.

Hedge fund manager, Dan Loeb, once said that “A key rule in investing is that you don’t necessarily need to understand a lot of different things at any given time, but you need to understand the one thing that really matters.”

China is that one thing that really matters now in global markets….

This month we’re kicking off what will be a three part Macro Intelligence Report (MIR) series where we’ll dive into the investing implications of a wide scale China slowdown, covering everything from its impact on commodities and precious metals, to currencies, and the housing bubbles in places like Canada and Australia.

In this month’s report we’re going to start off by discussing how China and emerging markets in general have exhausted their easy growth channel of expanding their share of global exports. And then we’re going to dissect how China’s economic “miracle” is no miracle at all but rather the result of a standard cycle in the typical “Gerschenkron model” of economic development; one which has occurred time and time again throughout history and which has always, in every instance, resulted in a large, painful, and prolonged economic crisis.

We’re then going to dive into Chinese policy and share with you the evidence from Xi, the CCP, and underlying data on why we think this time is different, and the signals we need to look for going forward.

Then of course, the trading and investing implications… We’ll layout the case why gold is going to $1,000, oil is going to sub $56bbl, and AUDUSD is going to 0.60.

We’re also going to talk about why we are still bullish US stocks and then pitch two beaten down misunderstood US tech companies that offer extremely attractive asymmetric opportunities to the long side. Finally, we’ll cover a highly contrarian short trade on a popular US listed Chinese tech stock.

If you want the scoop on China be sure to sign up for the MIR at the link below.

Click Here To Learn More About The MIR!

There’s no risk to check it out. We have a 60-day money-back guarantee. If you don’t like what you see, and aren’t able to find good trades from it, then just shoot us an email and we’ll return your money right away.

China’s the most important macro situation to understand right now. Getting it wrong can mean years of subpar returns and underperformance. Don’t get caught on the wrong side of the boat! By reading this month’s MIR, you will be prepared for the worst and positioned to profit off of a full out Chinese collapse.

Click Here To Learn More About The MIR!