Remember this: When you are doing nothing, those speculators who feel they must trade day in and day out, are laying the foundation for your next venture. You will reap benefits from their mistakes. Speculation is far too exciting. Most people who speculate hound the brokerage offices or receive frequent telephone calls, and after the business day they talk markets with friends at all gatherings. The ticker or translux is always on their minds. They are so engrossed with the minor ups and downs that they miss the big movements. ~ Jesse Livermore, “How To Trade In Stocks”

In this week’s Dirty Dozen [CHART PACK], we talk no landings and hard landings, cover dying disinflation, discuss Chinese demand, economic surprises, bond volatility, and SPX levels, plus more…

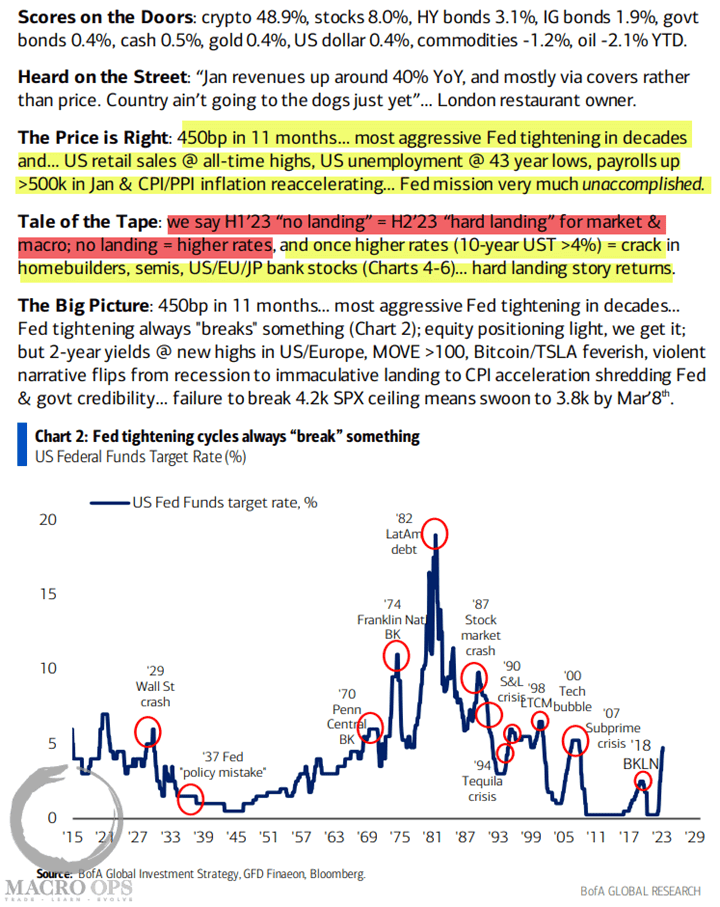

- H1’23 “no landing” = H2’23 “hard landing” via BofA’s Flow Show… (highlights by me)

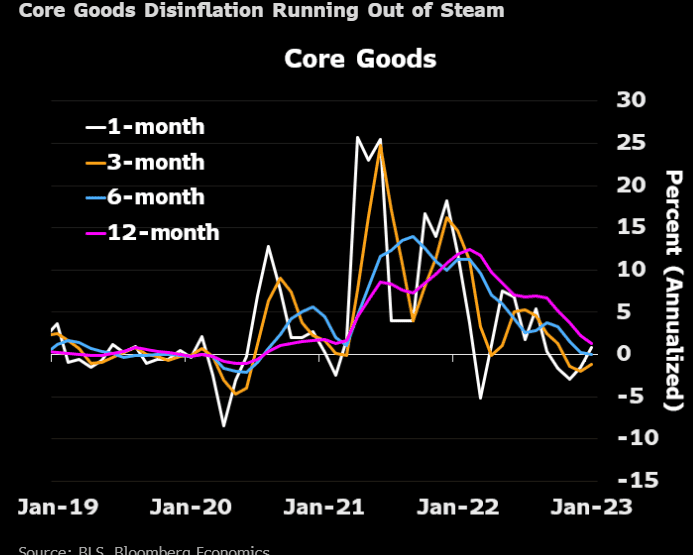

- Disinflation no more… via BBG “the January CPI data showed that core goods disinflation, which has been a drag on inflation in recent months, is running out of steam. Core goods prices rose 0.1% month on month in January. Together with resilient services spending and persistent shelter inflation, the risks to the inflationary outlook are once again skewed to the upside.”

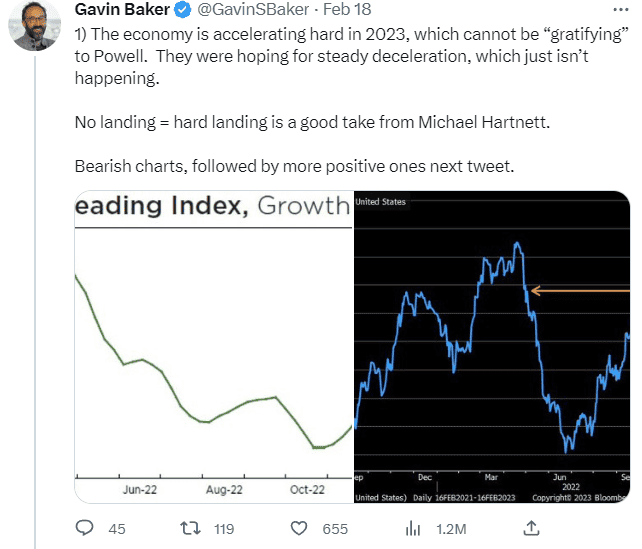

- Gavin Baker posted a good thread to the twitters (link here) outlining what we at MO have been writing about for the last few months, which is that no landing now means a harder landing later via higher for longer rates and tighter liquidity.

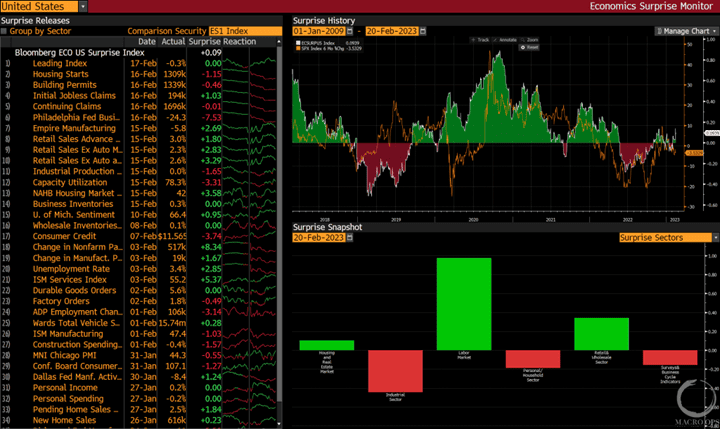

- Positive surprises: BBG’s ECSU function shows the sectoral breakdown of economic surprises (prints relative to consensus expectations). The index is in the top plotted with the 6-month change in SPX (orange line). And the bottom panel shows the positive contributors are housing and real estate, labor, and retail with the biggest detractor coming from the industrial sector.

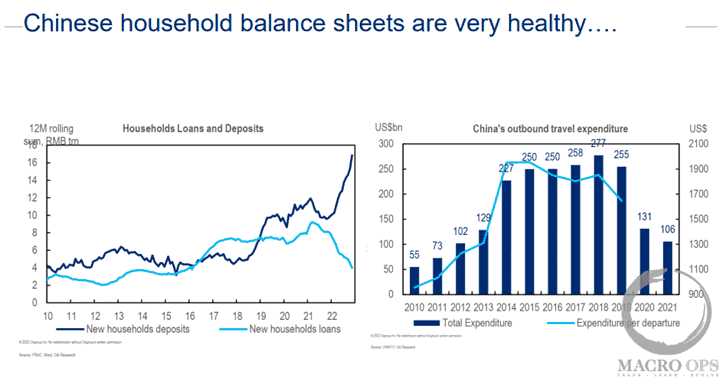

- Extended widescale draconian lockdowns mean that the Chinese are coming out of their homes with a lot of savings to spend. The pent-up demand is estimated to be in the ballpark of $2trn USD equivalent according to BBG (charts from Citi).

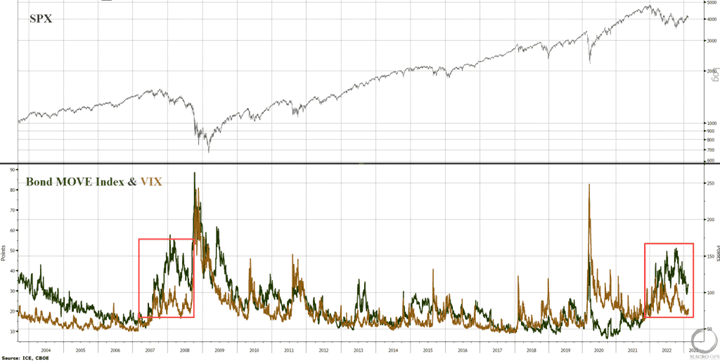

- Volatility in bonds tends to precede volatility in equities. This makes sense as UST yields are the basis for valuing everything else. This is why the elevated level in BofA’s MOVE index (a measure of bond volatility) needs to be watched closely (green line below). Higher for longer likely means higher vol, which makes me wonder if we’ll see a similar VIX/MOVE conversion as we did in 08’.

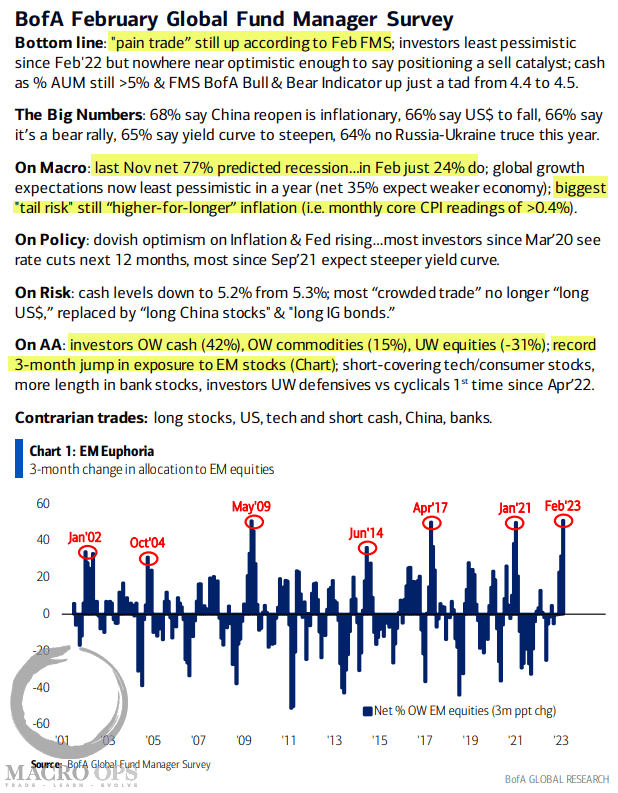

- On the positive side though, sentiment and positioning remain supportive of this bear market rally, for now. Here’s the summary from the latest BofA Global Fund Manager Survey with highlights by me.

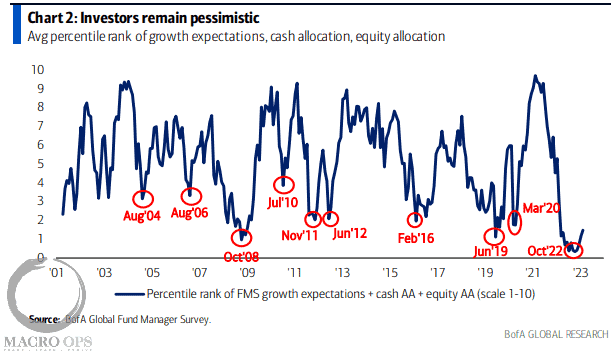

- Average percentile rank of growth expectations, cash allocation, and equity allocations via BofA…

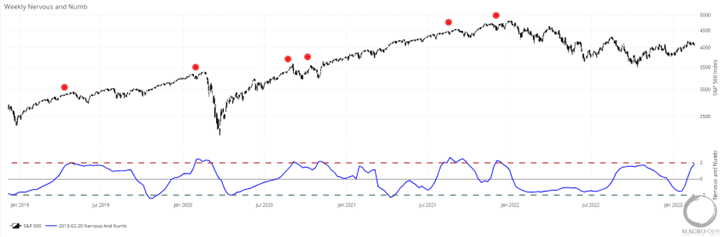

- Our weekly Nervous & Number Indicator, which is a measure of the relative changes in SPX and the VIX, looks like it’ll trigger a sell signal this week. Red circles mark past signals.

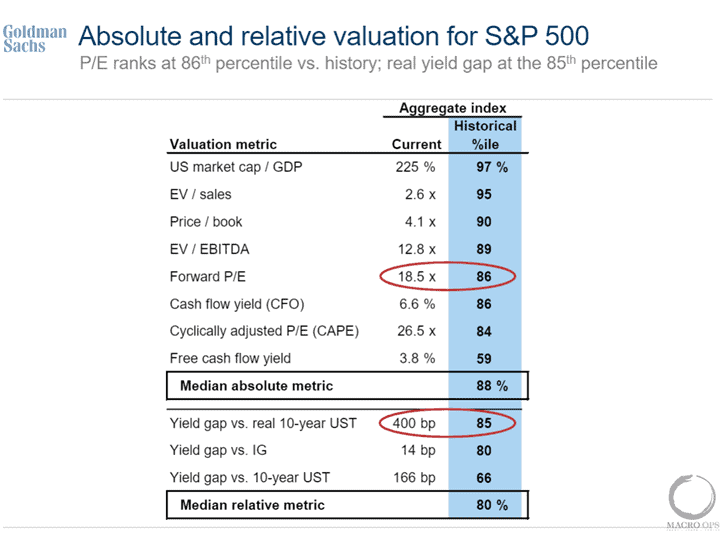

- This one is for the mouth breathers who think we’ve started a new cyclical bull market. I appreciate your optimism, but no… That is not how this works… You don’t have cyclical bottoms when aggregate median valuations are in the 88th percentile and the Fed is still in the midst of its most aggressive hiking cycle in decades (table via GS).

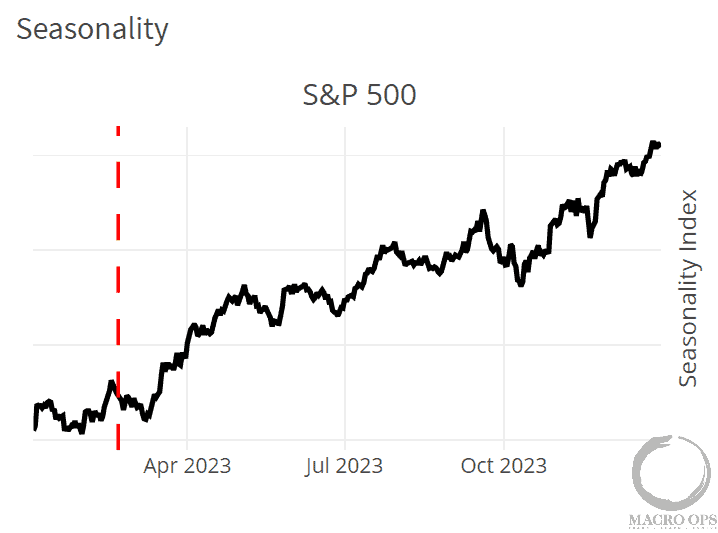

- We turned cautious two weeks ago for a number of reasons (short-term extension, significant resistance, yields breaking down, etc…) Another one of these reasons is seasonality, which is quite negative for the SPX until March 10th.

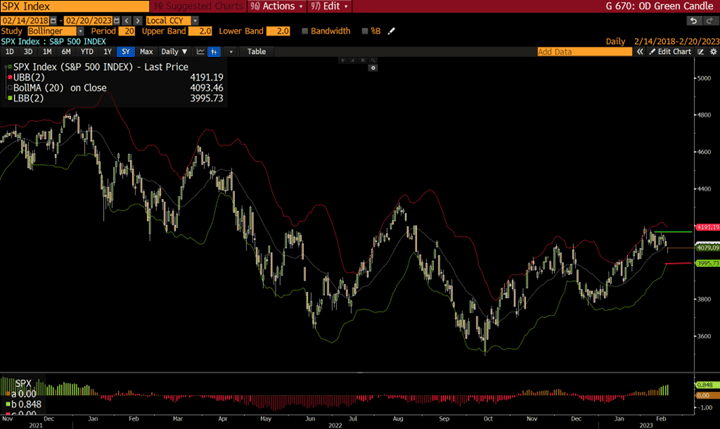

- While the weight of the evidence is still supportive of further upside in this bear market rally. The rise in yields and bond volatility has to dampen our short-term optimism. In an effort to keep this simple, we’re in neutral territory. A daily close above the green line, say 4,150 would be game on for the continued bull rally. A close below the lower Bollinger Band (around 4,000ish) would mean we’re likely rolling back over into the next bear market leg.

Thanks for reading.

Stay frosty and keep your head on a swivel.