Seemed like May flew by (along with the rest of 2020!) didn’t it?

The markets continue to confuse professional managers. Robinhood investors are minting money. Riots in the streets, S&P futures up pre-market. Nothing really makes sense.

If there’s one shred of consistency in your life, it’s a fresh new copy of Value Hive in your inbox every Wednesday.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Massif Capital Long Thesis on Bakkafrost (BAKKA)

- Bonhoeffer Capital Q1 Letter

- Interview with RA Capital on Healthcare Companies

- Bill Ackman Sells Berkshire

Let’s dive in!

—

June 3rd, 2020

Meme Of The Week:

FinTwit right now. pic.twitter.com/iCJOmi76we

— Trevor Scott (@TidefallCapital) April 8, 2020

__________________________________________________________________________

Investor Spotlight: Bonhoeffer Capital & Maran Capital

This week’s Investor Spotlight features Bonhoeffer Capital Q1 Letter and Massif Capital’s latest long idea: Bakkafrost (BAKKA).

Bonhoeffer Capital (-33.7% in Q1)

Keith Smith of Bonhoeffer Capital returned -33.7% in Q1. It was a rough quarter for value investors. I love reading Keith’s letters because his fund is so different. As of the letter, his top countries (by allocation) are:

-

- South Korea

- Italy

- South Africa

- Hong Kong

- United Kingdom

- Philippines

Don’t see the US on that list do ya? That’s because Keith fishes where the fish are!

Keith spends most of the letter discussing Strategic Framework Investing.

What is Strategic Framework Investing?

Here’s Keith’s take: “Valuation models have evolved over time from valuation multiples—which work well with mature companies (Graham)—to discounted cash flow models—which work better for growth companies (Buffett)—to distress-weighted models for declining businesses (Damodaran), and finally to strategy/business models—which focus on market size, growth (including network effects), customer lock-in, economies of scale, and probability of survival for young growth companies (venture capitalists).”

Valuation changes over time. So, the framework through which we view our valuations should change with it.

It doesn’t make sense to value a money-losing start-up company based on P/E ratios. An investor that only uses one valuation method is the same as a man wielding only a hammer. To him, every company looks like a nail.

Why does it matter that we adjust and adapt to the constantly changing business environment? Let’s tap-in Keith for this one:

“With the introduction of disruptive internet capital-light models by young growth companies, current profitability (under the assumption of the presence of either large unreproducible investment or network effects) has been less important than future profitability supported by a business model that can generate strong customer growth, recurring revenue with small amounts of customer attrition due to customer lock-in and/or creating network effects.”

Issues With New Business Models

Keith reeles off a few issues with these new network-effect businesses:

-

- LTV, CAC and Churn are hard to estimate

- Some of the business models are dependent upon outside financing when they are in the growth phase of development

The letter shifts focus to discuss the multiple (P/E, EV/EBITDA) valuation method and mean-regression. I encourage you to read the whole thing — it’s great.

But we’ll end with two ideas from the letter: Telecom Italia (TIT.IT) and KT Corporation (KT.US).

Telecom Italia (TIT.IT)

Business Description: Telecom Italia S.p.A., together with its subsidiaries, provides fixed and mobile telecommunications services in Italy and internationally. The company operates through Domestic, Brazil, and Other Operations segments. – TIKR.com

What’s To Like:

-

- 54% Gross Margins

- Long history of profitability

- ~$2B 3YR FCF average

- Trades <6x EBITDA

- Owns most extensive telecom network in Italy

What’s Not To Like:

-

- Low normalized net income margin

- Net Debt/EBITDA is 3.69x

- France’s Illiad may cause price war

What’s It Worth:

Let’s assume the company grows to $17.2B euros by 2024. Using historical EBITDA margins (40%) we get almost $7B euros in EBITDA, 2.5B euros in FCF and $37B in Enterprise Value.

Subtract net-debt and you’re left with around $12.7B in market cap (0.60 euros/share). That’s assuming a 9% discount rate and 3% perpetuity growth. If you take a multiple approach (EBITDA or FCF) you’d realize a higher per-share value.

Chart Analysis:

TIT’s showing sideways consolidation below the 50MA. Our price-action base case is a breakdown below support and further price decline. But we’re looking for a reversal given the fundamental background.

KT Corporation (KT)

Business Description: KT Corporation provides telecommunications services in Korea and internationally. The company offers local, domestic long-distance, and international long-distance fixed-line and voice over Internet protocol fixed-line telephone services, as well as interconnection services; broadband Internet access service and other Internet-related services; and data communication services, such as leased line and broadband Internet connection services. – TIKR.com

What’s To Like:

-

- Strong FCF generation

- 40%+ Gross Margins

- Declining SG&A % of Revenue

- Improving Current Ratio

- Net Debt/EBITDA: 1.18x

- Largest amount of 5G Infrastructure in South Korea

What’s Not To Like:

-

- Legacy business still dominates revenues

- Tensions with North Korea

- Declining real estate values in KT’s portfolio

- Failure to spin-off non-core (non-teleco) businesses

What’s It Worth:

KT is a sum-of-the-parts (SOTP) story. They have a hodgepodge of businesses, each with varying degrees of value.

Keith summarized his view on KT’s value in a 2018 post with MOI Global (emphasis mine):

“The shares recently traded at a “look-through” FCF multiple of 5.8x, and look-through EV/EBITDA of 1.5x … If the shares traded at 6x EBITDA with a holding company discount, the stock would be more than a triple, not including dividends, buybacks or cash flow gains from a growing telecom business.”

Someone call Dave Waters, he loves this stuff.

Chart Analysis:

There’s nothing we can glean from this chart right now. Look for the 50MA to act as resistance over the next few weeks.

Massif Capital: Bakkafrost (BAKKA) Long Thesis

Massif Capital’s back with their latest long thesis: Bakkafrost (BAKKA). You can read their entire report here.

Let’s dive in.

Business Description: P/F Bakkafrost, together with its subsidiaries, produces and sells salmon products under the Bakkafrost and Havsbrún brands in the United States, Europe, China, and internationally. The company operates through four segments: Fish Farming FO; Fish Farming SCT; Value Added Products; and Fishmeal, Fish Oil, and Fish Feed. – TIKR.com

What Massif Likes:

-

- Family owned and operated with 19% ownership

- Consistent 70% Gross Margins

- Ideal location for growing salmon

- Commands 15% pricing premium against global competitors

- 20%+ Operating Margins

Risks:

-

- Long-term erosion of salmon prices

- New diseases / pandemics affecting salmon health

- Consumer taste changes

What Massif Thinks It’s Worth: BAKKA’s balance sheet has a long-term interest-bearing debt of 𝑘r2.3 billion vs. a cash balance of ~𝑘r1.3 billion. Gross margins are remarkably steady at around 70%. A discounted cash flow analysis, assuming a 10% discount rate, results in a valuation of ~𝑘r741 NOK per share, producing an expected return of 32% at current prices.

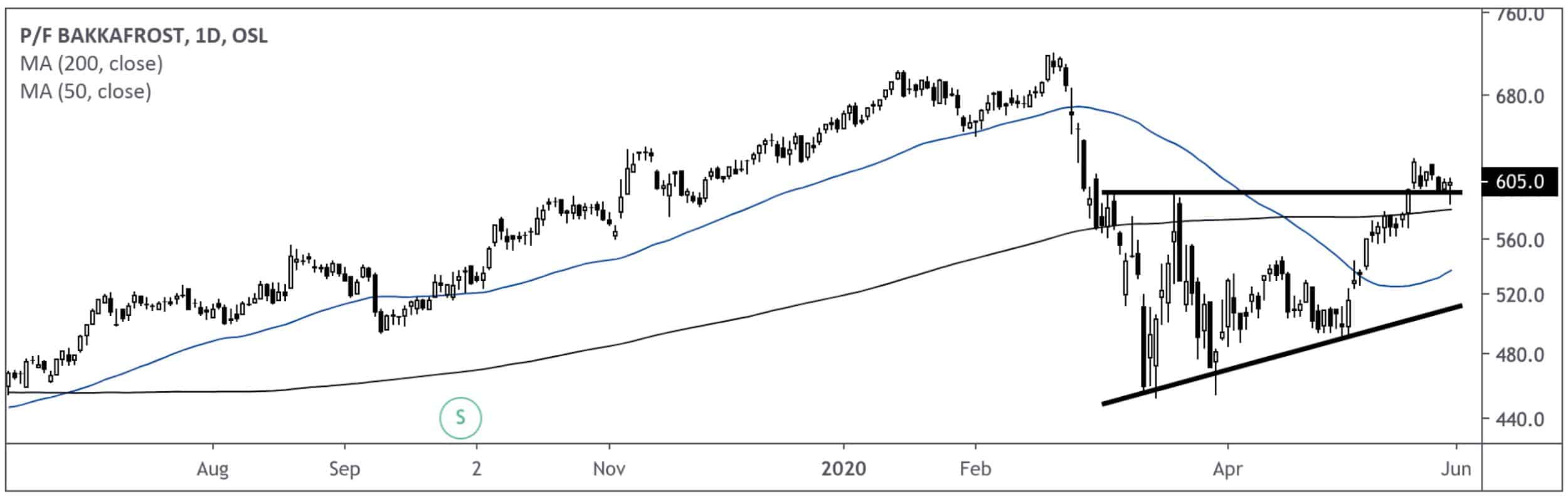

Chart Analysis:

BAKKA broke out of its ascending right triangle last week. A brief pullback has us up against the new-found support line. Price remains above the 50MA and 200MA, a bullish sign. __________________________________________________________________________

Movers & Shakers: Bill Ackman Sells Berkshire!

GIFs by tenor

GIFs by tenor

Bill Ackman isn’t afraid of the spotlight. We’ve heard his name referenced numerous times during this COVID crisis. Who could forget his live-action sob story on CNBC?

This time, he’s in the news for selling Berkshire Hathaway (among other investments).

My reaction: Who cares? There’s tons of ideas out there that are better than the BRK thesis.

Ackman brought up some good points during the interview (emphasis mine):

The one advantage we have versus Berkshire is relative scale. Berkshire has the problem, if you will, of deploying $130 billion worth of capital … Pershing Square, on the other hand, has about $10 billion of capital to invest and therefore can be more nimble … We should take advantage of that nimbleness, preserve some extra liquidity, in the event that prices get more attractive again.”

And that’s my biggest issue with the BRK bull thesis. Buffett is so capital constrained it makes it damn near impossible to find deals. Meanwhile, there’s plenty of opportunities for less capital constrained investors/funds. Look at Poland, Egypt or Italy (to name a few).

__________________________________________________________________________

Interview of The Week: Healthcare Investing with RA Capital’s Peter Kolchinsky

GIFs by tenor

GIFs by tenor

Evercore describes RA Capital as, “ one of the leading dedicated healthcare investment funds and has been built over nearly two decades with a unique approach to analyzing therapeutic categories.”

My circle of competence in the healthcare space is pitifully small. This interview helped expand it a bit.

Let’s dive into the meat of the interview (emphasis mine on the responses).

Q: How have your private company investments changed your view of the field?

RA Capital: “The public markets don’t get to see how the sausage 4 is made, which is just as well because it can be harrowing. But we have come to appreciate the way driven, talented people can work through most any challenge to keep programs going. That makes us more patient public investors.”

I loved this quote. We’ve heard similar things from Scott Miller in some of his past interviews. Working in the belly of a company makes you a better investor. Period.

Q: How do you choose which companies or fields to drill into?

RA Capital: “We’re always mindful of the risk that we might overlook a great investment and are constantly refining our methodology to minimize that risk. For example, because we have someone tracking everything that’s going on in lupus, we know which companies in that landscape are working on something potentially compelling. Either we’ll reach out to those companies about financing them, even if they aren’t talking to investors yet, or, when they reach out, we’ll know to assemble a team of people, including senior members of our investment team, to get a deep update and make a rapid decision.”

Q: What do you see as the biggest risks/opportunities for the sector?

RA Capital: “I think that the risks of drug development are shifting from probability of technical or clinical success, which quantify the risks of – for example – a clinical trial failing, to those of strategic complexity. Historically, the chessboards have been so empty that making any drug that works has been considered a win. However, with more and more drugs coming to market, it’s no longer enough to make a drug that simply works.”

If this interview made me realize anything, it’s that I will always be the patsy at the poker table in that space.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!