Before I get to my three picks I want to remind all fellow Collective members that our 2020 Stock Picking Competition officially kicks off next Monday. The deadline to get your three picks in is by end of day Friday. If you want to play just shoot me an email at alex@macro-ops.com or post your picks to the Comm Center and tag me and I’ll throw them on the board.

The only rules are that the picks have to be stocks (no futures, options, FX). ETFs are allowed as long as they aren’t levered. That’s it. There are no liquidity or country requirements. And the rules of the game are simple: the Operator who’s basket of three stocks (all equally weighted) sees the highest return from Jan 13th through the close of December 31st, 2020, will win.

We haven’t figured out what the prize will be yet but we’ll come up with something good. Maybe some MO swag and an expensive bottle of scotch, not to mention all the bragging rights.

That’s it… Looking forward to seeing your picks!

Now it’s time for me to share my three dark horses. Let me give you fair warning. Two, if not all three of my picks will probably make you dry heave once you see the companies that I’m backing.

I’m fine with that. In fact, that’s the kind of response I’m going for.

Here’s the criteria I used for my selection.

- The stocks had to be companies that I’m not already holding for no other reason than I just wanted to make this game a bit more fun. And with the hope that I’d find some new interesting plays (which I think I accomplished).

- I wanted picks with crazy asymmetry. Stocks that have the potential to at least double if not 3x or more within 12-months time. I’m playing for keeps here. Either I’m winning this thing or taking a distant last place and eating large helpings of humble pie.

- To accomplish the above I needed to find stocks that were either totally and utterly hated or completely and absolutely forgotten, dismissed and disregarded. Preferably, they would have a low float (small supply = higher potential for sharp runs) and a reasonable catalyst for positive change on the near horizon. If they had a really large technical base from which to launch from, even better.

I sifted through hundreds of stocks. My initial list after my first pass through using technicals and a few key fundamental criteria gave me a stack of about 45 tickers. I then dug through the fundamentals for each one of these and was able to kick out the total garbage companies leaving me a solid group of eight stocks.

From this list, I read through transcripts and assigned ratings for technicals and fundies and most importantly, gave a grade to the company’s positive skewness — remember, this isn’t about picking the stock most probable to have a good year but rather about finding three stocks that have the most potential to have an insanely good year (ie, massive convexity).

With that said, I think I accomplished my aims. Now, whether or not they’ll perform or break their legs right out of the gate is to be seen. Either way, I’m excited about the picks. And with that, let’s dive in…

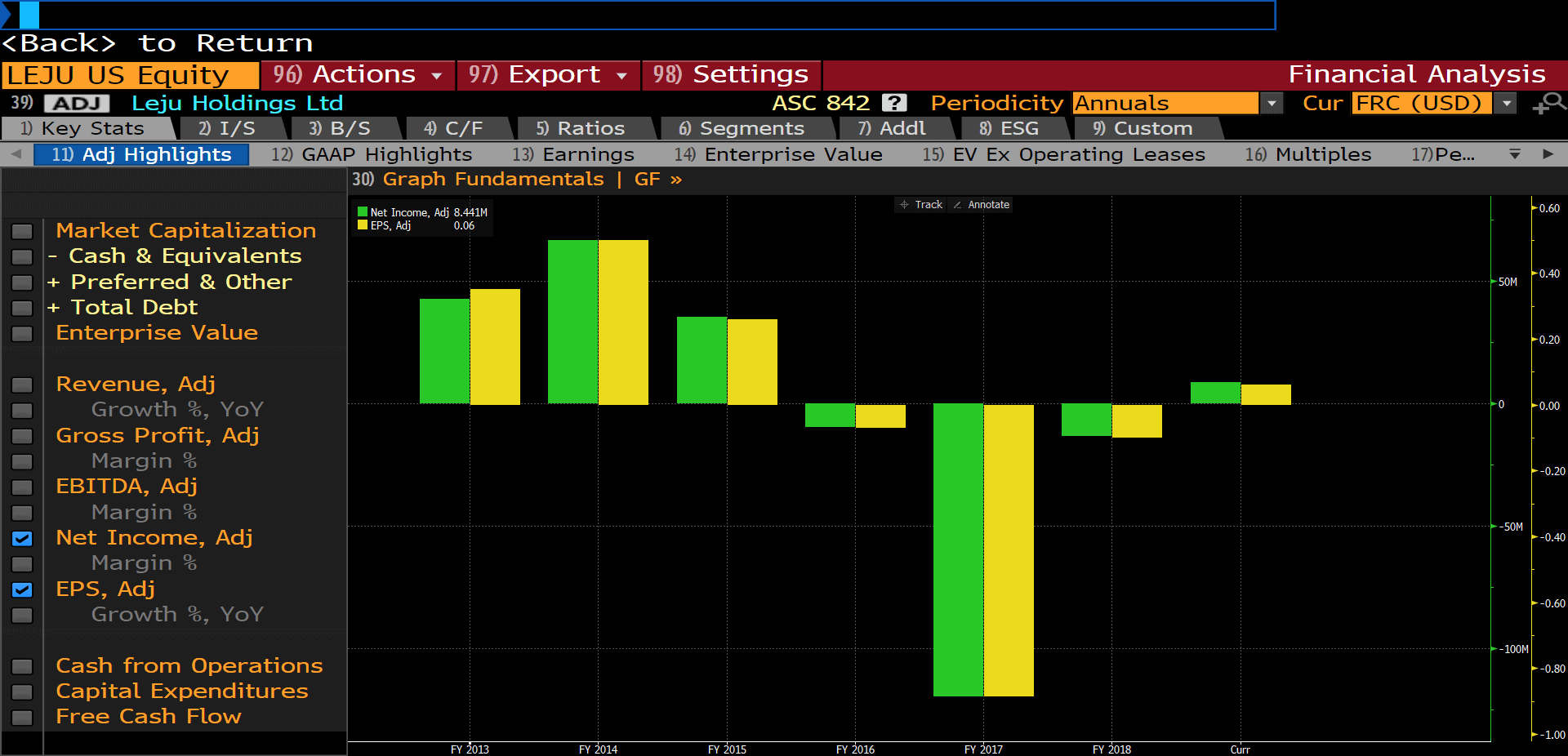

Leju Holdings (LEJU)

If you were to ask someone what was one of the riskiest areas in the global market, they’d very well may say “the Chinese property market”, and rightfully so. Legendary short-seller, Jim Chanos, calls it “the MOST important asset in the world” and not because he thinks it’s a great value.

So, why then did I pick Leju Holdings; a US-listed Chinese ADR that calls itself the leading “online-to-offline (O2O) real estate services provider in China”? Well, I told you I wanted downright disgusting stocks, didn’t I? But, like many things in life, sometimes you have to peer beneath the surface to find that there’s more than what initially meets the eye.

Here’s what I like about LEJU. And why I think it could easily be a 5x’r or more if, of course, it doesn’t end up being a total fraud — I mean, you never really know with these Chinese ADRs.

First off, the chart.

The stock has spent most of its time in a perpetual downtrend since it listed in 2014 after hitting an initial high of $18 a share. At one point, the stock was down over 94% from its all-time highs. For the last three years though it’s been trading in a tight consolidation range.

This is an excellent base… The stock has done nothing for three years. Those who are still sitting in this thing are likely strong hands if they’re willing to hang on through years of… nothing.

What exactly does LEJU do?

You can think of LEJU as a Chinese version of Zillow (ZW). In fact, the two have partnered together (link here). The company has a market cap of $330m, a small float, holds hardly any debt, carries roughly half its market cap in cash, is expected to do $670m in revenues this year which makes for top-line growth of 45% — nearly doubling last years growth rate of 27%. It has positive earnings growing at over 40% YoY, and is trading for approximately half times sales.

CEO Yinyu He, says the slowdown in the property market over the last two years has in-fact been beneficial to their business because instead of developers/owners holding onto units in hopes of price appreciation they’re being forced to move inventory which makes for greater demand for LEJU’s services.

This stock has smooth sailing until $3.50 where it’ll hit some technical resistance. I think it punches straight through that roof and goes to $5+.

Centrus Energy Corp (LEU)

LEU is a US-based supplier of nuclear fuel and services to the nuclear power industry, both in the US and internationally.

The company has a $62m market cap, only 9m shares outstanding with just 4.5m floated (high insider ownership). Management expects to finish out FY2019 with total revenues in the range of $205-230m putting the midrange estimate at low double-digit growth YoY — marking the company’s first year of positive top-line growth in seven years.

The chart makes my mouth water…

The stock is down over 99% from its all-time highs hit way back in 07′. It’s been trading sideways for roughly 6-years and is just now making an attempt to break out of this range and doing so with strong volume.

Management expects to return to profitability this year — they just put in their first profitable quarter in a loooong time.

They recently lowered their LT debt from $247m to $74.3m (a reduction of more than 70%) and extended the remaining maturity all the way out to 2027.

Lastly, LEU recently signed a contract with the DOE to demonstrate the production of high-assay low-enriched uranium or HALEU. If successful, this would mark the first-ever commercial production of this advanced nuclear fuel which one day could be used in advanced next-gen nuclear reactors.

Dan Poneman, LEU’s chief executive, was deputy of the DEO from 09’-14’, so he’s well connected to get these types of deals done.

I’m uber-bullish on uranium’s long-term prospects. Governments are starting to go raving mad for “green” energy. And there’s no feasible future where we lower our carbon footprint without nuclear making up a LARGE part of our baseload energy supply.

Oh… and here’s a screenshot of the Q&A from their last call. Not a single analyst following this one… Totally under the radar.

Deutsche Bank (DB)

No 2020 contrarian stock list would be complete without the perma-bears absolutely favorite whipping boy, Deutsche Bank.

Somehow this company seems to find a way to be at the bottom of every money-laundering and trading scandal in town. Plus, their business has pretty much been stuck in the dumps ever since the GFC.

So why am I adding DB to my stock trio?

Two reasons… (1) DB has fallen over 90% from its 07’ highs. This stock has already passed through the five stages of investor grief and is now totally written off. I think the market has WAY overdone it and think DB is set for a massive rerating (2) all European banks have been in the pooper, largely due to Europe’s anemic economy and… this is is important… the ECB’s negative interest rate policy. One of my big macro thematics this year is that we see further rate convergence between the US and DM/European countries (meaning, US rates will hold steady to lower while other DM rates converge up). This trend is going to rocket boost European banks.

This chart shows that US banks are trading at ALL-TIME highs relative to their European counterparts (yellow line).

Fiscal policy is coming to the EU in the near future. This will not only boost domestic growth but also raise rates and steepen the curve — which is good for a bank’s net interest margin (NIM). Also, I think at some point this year Christine Lagarde looks at Sweden, who just ended their 5-year experiment with the mind-numbingly stupid experiment that has been negative rates, and sees that their economy is doing fine, in fact, better without NIRP and soon follows in their footsteps.

DB’s chart looks great. The stock just broke out of a 6-month bottoming wedge and has clear skies to $15.

DB’s new CEO, Christian Sewing, is doing and saying all the right things and the company is making good progress on their long-term “plan of transformation”.

I think all the bad news and then some is baked into this sauerbraten. It’s time for this turd to shine.

So there you have it. These are my three stocks to ride for the year. If you like ’em, have questions, or think I’ve completely lost my noodles, just respond and tell me so. I love hearing your feedback. Also, shoot me your picks. I’m excited to see what stocks y’all are amped about.

Oh… and I’ve also added these picks to my book. I’m putting my money where my mouth is. Details for the trades that I executed this morning are below.

Symbol: LEJU Holdings (LEJU)

Size: 100 bps

Entry: $2.40

Risk Point: $2.00

Target: $6+

Symbol: Centrus Energy Corp (LEU)

Size: 100 bps

Entry: $6.69

Risk Point: $4.81

Target: $14+

Symbol: Deutsche Bank (DB)

Size: 100 bps

Entry: $8.45

Risk Point: $7.55

Target: $15+

Your Macro Operator,

Alex