Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Latest Articles/Podcasts/Videos —

Your Monday Dirty Dozen [CHART PACK] — I look at signs of a global rebound in growth, green shoots in Europe, trouble ahead for US bonds, check-in on the four drivers of gold, and check out oil extraction costs in different parts of the world, plus more.

Trading Politics [Part 1] — Tyler lays out how to use services like PredictIt to profit from mispricings in the betting market which is good stuff to know with election season drawing near.

Value Hive: Q3 Letters and LEGOs as Investments — Brandon dives into the latest investor letters, including those from Loeb’s Third Point and Einhorn’s Greenlight Capital and more.

Articles I’m reading —

I’ve been digging into the oil and gas sector quite a bit lately. It’s going through a much-needed culling and as is often the case in a widespread industry downturn, I’m seeing many babies getting tossed out with the bathwater. This is great since it takes periods like these of long drawn out value destruction to create total investor apathy and hence amazing value opportunities for those willing to come in and sift through the rubble.

Sam Zell, the man known as the “Grave Dancer” since he’s made his fortune in the distressed debt market, seems to be thinking the same. In a recent Bloomberg article (link here) Zell is quoted saying:

“The amount of capital available in the oil patch is disappearing… I compared it to the real estate industry in the early 1990s, where you had empty buildings all over the place, nobody had cash.”

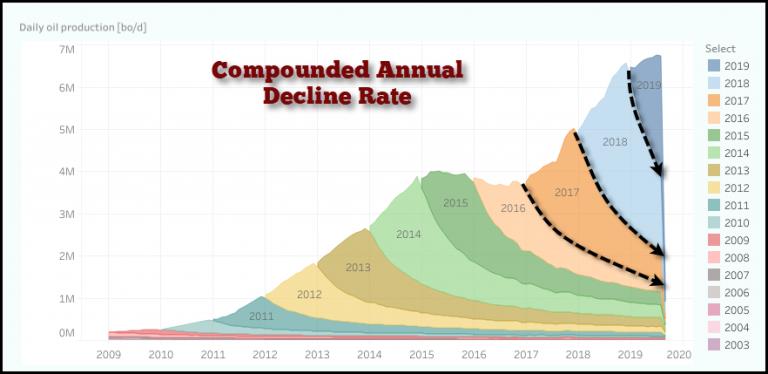

A recent report by SRSrocco titled “The U.S. Shale Industry Hit A Brick Wall in 2019” lays out in very stark terms the inflection point in which the industry is currently going through (link here). Here’s a cut from the article which is worth reading in full.

“There several factors that have negatively impacted the U.S. Shale Industry in 2019; the compounded annual decline rate, the massive debt–inability for shale companies to raise money, and the stunning amount of new wells necessary to increase overall production. While shale experts are knowledgeable of the typical 60-70% first-year decline rate of shale wells, not much is mentioned about the “compounded annual decline rate.’”

The commodity fund Goehring & Rozencwajg explained in a recent letter (link here) how out-of-whack the valuations have gotten in the space, writing:

“In particular, the bear market in oil exploration and production companies has created value that can hardly be believed. We analyzed the universe of all US-listed E&P companies with market capitalizations over $100mm and proved reserves that are at least 50% oil. We then compared the current stock price to the net-debt adjusted SEC PV-10 measure from their 2018 10Ks. As you may recall, a company’s PV-10 measures the discounted cash flow of all proved reserves at the prevailing oil and gas prices. Under normal market conditions, E&P stocks trade at a premium to their SEC PV-10, reflecting the expected value of any future reserves not yet “booked” in the reserve statement. However, due to the overwhelming bearishness among energy investors, the average company now trades at a 12% discount to its net-debt adjusted SEC PV-10 per share value.

While we have seen individual companies trade at a discount, we cannot recall a time when the industry average was less than its SEC PV-10 value. We should point out that the price used in most companies’ SEC PV-10 analysis for 2018 was $55 per barrel, not materially higher than today’s price.”

If you’d like to read my long-term take on the energy sector then give this piece I wrote a while back (link here) as well as this great follow-on update put together by Evergreen Gavekal (link here).

I think there’s going to be incredible opportunities in this space. I have a basket of offshore E&Ps that I’m tracking closely. All have solid balance sheets, great long-term assets, and generate tons of free cash flow even in this low pricing environment.

These companies are not only going to benefit from the oncoming culling with all the uneconomic supply getting taken out to the woodshed. It’s also going to give them the opportunity to pick up great assets from forced sellers for pennies on the dollar. In an illiquid environment, those flush with cash are kings.

We’re still in the early stages of this game and there’s likely more downside than upside in the very near-term. It’s going to take some large scale bankruptcies (see CHK) and the funding tap to get completely turned off in order for a durable bottom to be put in. Plus, I’d like to see a confirmed cyclical top in the dollar as well.

I’m thinking this is a 2H 2020 play. But the opportunity is so great it’s worth keeping a very close eye on now.

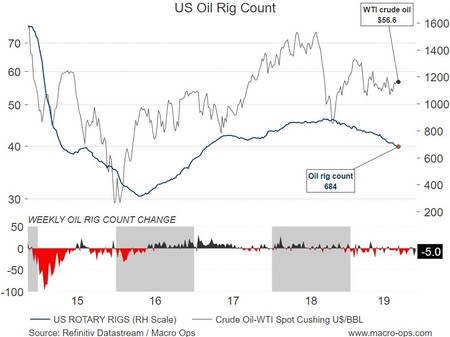

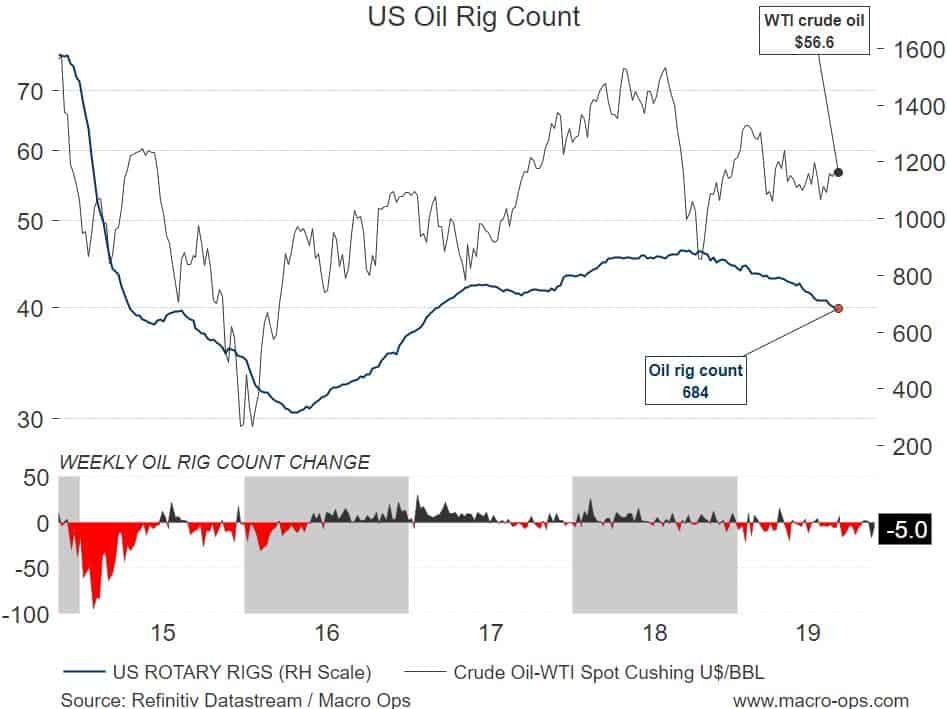

Charts I’m looking at—

The extended bear market in oil was caused by two things (1) China’s growth story hitting a brick wall and (2) unproductive US frackers funded by cheap money and over-eager investors.

China has entered a period of decline which will not end anytime soon. But… India and other parts of Asia are not burdened by Everest sized piles of debt and happen to be hitting the knee of the Wealth S-Curve. This is going to drive a secular exponential rise in energy demand. And to our second point, as investor willingness to fund unprofitable producers declines so too is drilling activity, which we can see by the steady fall in rigs over the last year.

Podcast I’m listening to —

The journalist Bethany McLean published a book last year titled “Saudi America” that I recommend reading. She does a good job telling the origin story of the US fracking industry as well as explaining the inherent structural problems that the sector is now dealing with.

She was on the podcast circuit promoting the book earlier this year. Here’s a good short (30 mins) interview she did with NPR where she summarizes the main points from the book (link here).

Video I’m watching —

Not at all trading related but I really enjoyed this so I thought I’d share. Here’s a short clip of Steve Jobs talking about how he thinks about marketing (click on the image to see the video) in terms that advertising genius Rory Sutherland would approve. Jobs explains that building a brand and marketing products is not about logic but about invoking feelings and imparting values. Give it a watch, it’s great.

Quote I’m pondering —

What matters isn’t how well you play when you’re playing well. What matters is how well you play when you’re playing badly. ~ Martina Navratilova

As true in markets as it is in tennis…

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.