Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Latest Articles/Podcasts/Videos —

Your Monday Dirty Dozen [CHART PACK] — I look at the latest prints of some leading US economic indicators, then talk SPX technicals, some Democratic polling numbers, virus growth, and BofA Global Fund Manager Survey, plus more.

Articles I’m reading —

This post from Ensemble Capital does a great job relating how we, as traders/investors, should think about the virus and its impact on markets. Here’s the link and a section from the report.

“But while it is perfectly reasonable to be concerned about the long-term economic impact of the virus, it is also perfectly reasonable to recognize that the virus may have little to no economic impact beyond 2020. Right at this moment in time, after such a sharp drop in the stock market, it is hard to believe that this might all fade in economic importance over time. But it is notable that in fact this is exactly what has happened with almost all past global virus outbreaks.

“Here’s David Quammen, the author of “Spillover: Animal Infections and the Next Human Pandemic” writing in the New York Times:

‘[This outbreak is] possibly even more dangerous to humans than the other coronaviruses. I say “possibly” because so far, not only do we not know how dangerous it is, we can’t know. Outbreaks of new viral diseases are like the steel balls in a pinball machine: You can slap your flippers at them, rock the machine on its legs and bonk the balls to the jittery rings, but where they end up dropping depends on 11 levels of chance as well as on anything you do.

Nobody knows where the pinball will go… Six months from today, Wuhan pneumonia may be receding into memory. Or not.’”

The key here is that nobody knows. It’s impossible to have an edge on this one. The coronavirus could end up being the Spanish Flu redux “or not” as Quammen writes.

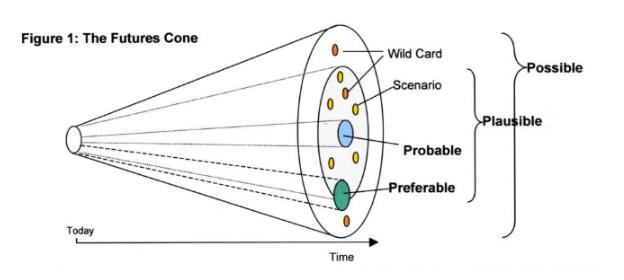

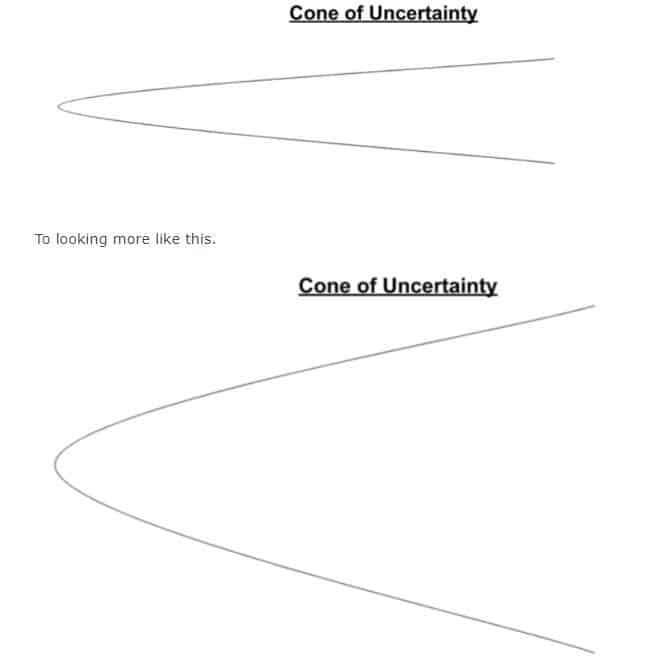

In markets, we’re always dealing with uncertainty. Sometimes that uncertainty is relatively low and the range of plausible outcomes is more narrow than not. And sometimes that range blows out and assessing probabilities with any level of confidence becomes a crapshoot. Here’s some nifty diagrams from older posts that I’ve written on the subject, which you can find here, here, and here.

The coronavirus blows this cone out completely. That’s why the market is selling off as hard as it is — though some of this was inevitable due to crowded sentiment and positioning. But how do you properly discount a global pandemic in a world that’s as intricately connected as ours; where over 43 countries are involved in the making of a single iPhone?

It’s impossible… at least at this point in its evolution. Nobody can say with any level of conviction how things will progress going forward.

Maybe that’ll change in a week, or a month, or a couple of quarters… I have no clue. And that’s the point.

Charts I’m looking at —

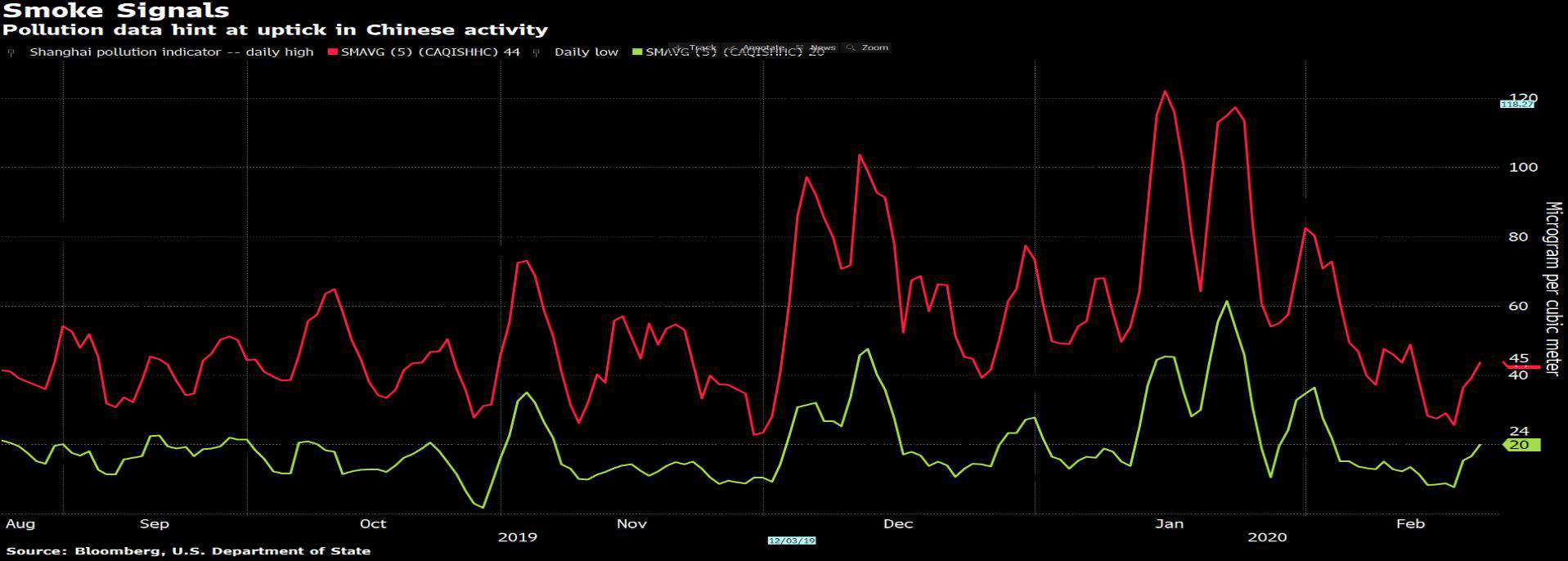

Copper, the CRB Raw Industrial Metal Index, the Shanghai Pollution Index, are a few of the charts I’m tracking to get a leg up on when economic activity in China returns to more normal levels. There’s been a slight bounce over the last few days but hardly does a few data points make a trend.

Video I’m watching —

Watch the first 20-minutes or so of this panel discussion on COVID-19 from Johns Hopkins. It’s the best discussion I’ve seen on the topic. The main takeaway is that COVID-19 has likely crossed the threshold of what constitutes a technical pandemic and that there’s still a ton of unknowns about the virus and how it’ll progress. A positive is that they believe the mortality rate will likely drop once our means of testing for the virus improves. Here’s the link.

Also, I highly recommend giving this Real Vision interview with hedge fund manager Dan McMurtrie (I shared his latest letter in last week’s Musings). They cover a range of subjects in the talk, things like how he approaches investing, the attractiveness of SAAS stocks, the evolution of financial markets and more. But my favorite bit was what he had to say about inequality and what it’s doing to our politics. Here’s the link and a clip.

“You can chop the numbers a lot of different ways, but the reality is half the country right now is either financially, I would say close to insolvent, really just trying to get by and it’s a tight wire act or is just currently on the tight wire and they see that and that’s creating a lot of anxiety, a lot of anger, a lot of blame. I think for a lot of people, I think one of the reasons Bernie Sanders is doing so well and the reason that Trump is doing so well is in the last two years, first premiums went up and then deductibles spiked. As we saw premiums and deductibles spike, we saw all the polling data starts to correlate and what’s important to understand is because of the desperation people are in, it is forcing them to become single-issue voters.

“For a lot of Americans, they have to be a single-issue voter on health care. It’s not about ideology. It’s not about anything else. This could ruin their lives, it could bankrupt them. It’s a very serious problem. That introduces really serious political risk. The biggest risk for any country is when people within the country start acting not out of their own self-interest, but out of hate for the other.”

Book I’m reading —

A big hat-tip to Brent Beshore for sharing this one. The book’s name is “The Fish That Ate the Whale” by author Rich Cohen. I’d heard of it before but never got around to ordering it, though I quickly resolved that error after reading this excerpt from the book here.

The book is about Sam Zemurray. A penniless Russian immigrant who through sheer will and hustle created a banana empire, where he literally raised armies and overthrew governments. Here’s an excerpt from the excerpt.

“Zemurray had stumbled on a niche: ripes, overlooked at the bottom of the trade. It was logistics. Could he move the product faster than the product was ruined by time? This work was nothing but stress, the margins ridiculously small (like counterfeiting dollar bills), but it was a way in. Whereas the big fruit companies monopolized the upper precincts of the industry—you needed capital, railroads, and ships to operate in greens—the world of ripes was wide open. Within a few weeks of his return to Selma, Zemurray set out again, then again, then again. It was in these months, on train platforms and in small towns, that Zemurray first came to be known as Sam the Banana man.

“Historians later described the young Zemurray as a fruit peddler, no different from other poor Jews who pushed carts through Manhattan’s Lower East Side, except instead of a wagon, Sam worked out of a boxcar. (He was “Sam the Banana Man,” according to Life, “who once used railroads as pushcarts.”) It made sense, but only in a shallow way. In truth, Sam Zemurray was more interesting and unique—as a salesman of a perishable product, he was a kind of existentialist, skirting the line between wealth and oblivion, health and rot, a rider of railroads, a chaser of time. It was life: Move the fruit now or you’re ruined forever. He became a gambler by necessity—a risk-taker, a salesman, a brawler. “The little fellow,” as the big wheels in Boston called him, but the little fellow would build a kingdom from ripes.

“Sam eventually went into turnings, yellows, even greens. By 1912, he was living in the jungle in Honduras, where, working with mercenaries, banana cowboys, he had overthrown the government, empowering a president more friendly to Cuyamel, the company Sam led to victory against United Fruit. In the end, he would live in the grandest house in New Orleans, the mansion on St. Charles that is now the official residence of the Tulane president. He continued to wield tremendous influence into the mid-’50s, a powerful old man who threatened, cajoled, explained, a mysterious Citizen Kane-like figure to people in his city. When he died in 1961, the New York Times called him, “The Fish That Swallowed the Whale.” But part of him would always remain that big kid peddling ripes from a boxcar on the Illinois Central.”

Really looking forward to reading this one.

Trade I’m looking at —

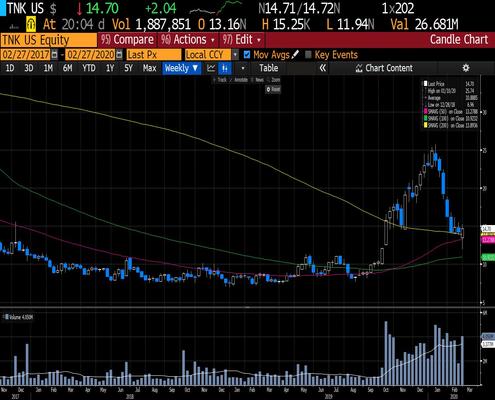

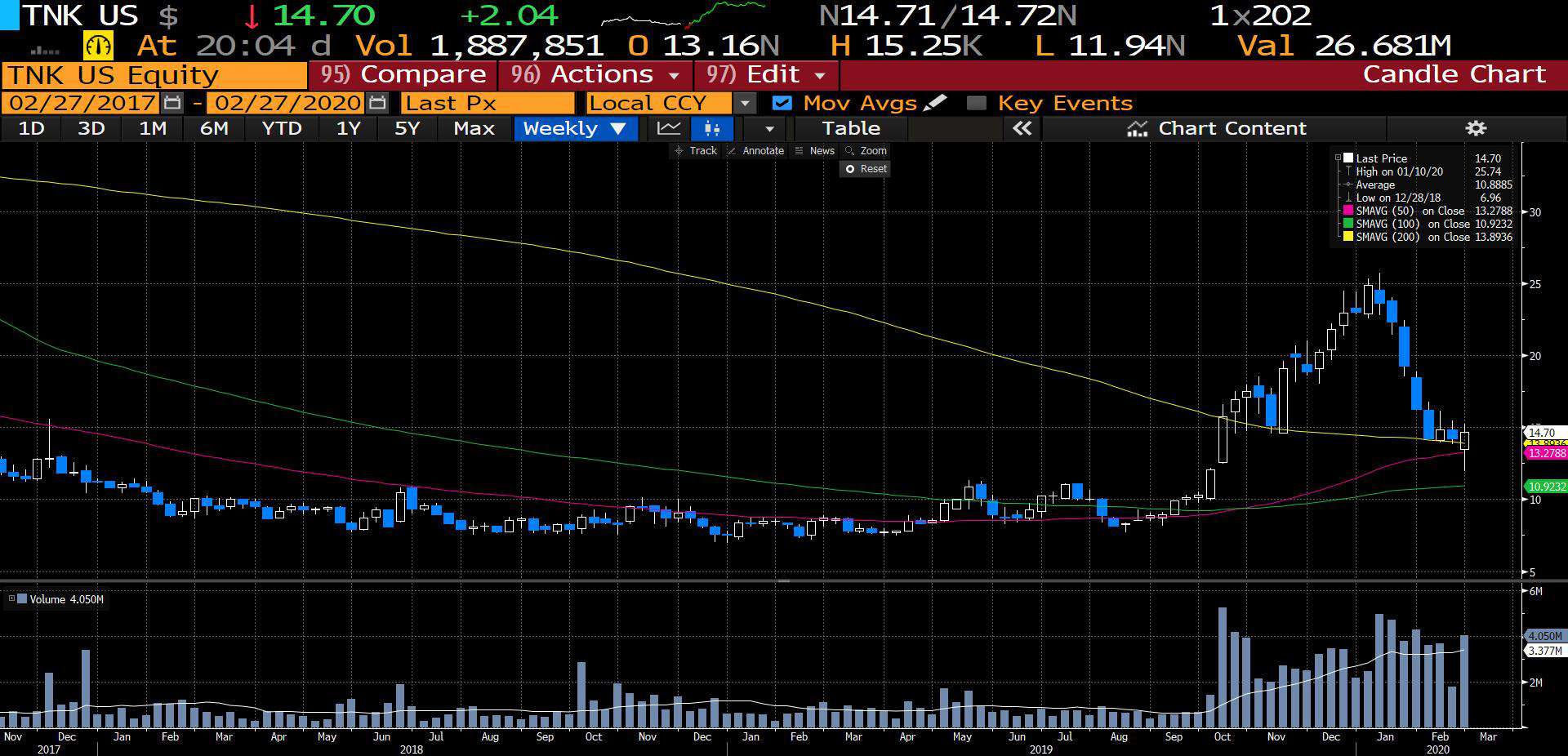

Shipping stocks have taken repeated punches to the mouth since the start of the year. They’re an obvious victim of the virus; virus kills economic growth, trade slows down, and shipping rates fall. Now if the virus ends up petering out sooner than later then there’s some incredible offers to be had. But… as we discussed above, pretending to have certainty now can get you killed.

So what I propose doing is to size small and cut your risk when the tape tells you “not now”. TNK reversed back above its 200w MA yesterday on the back of a great earnings report, where the company announced they brought in $83m, or $2.47 per share and knocked their debt down by 15% last quarter. Not bad though the real tell will be next quarter when the virus’s impact begins to show up in the numbers more. Either way, I think the asymmetry of the trade makes it worth some repeated attempts. I may put on a long early next week if the tape holds into the close on Friday.

Quote I’m pondering —

There is always a divergence between prevailing expectations and the actual course of events. Financial success depends on the ability to anticipate prevailing expectations and not real-world developments. But, as we have seen, my approach rarely produces firm predictions even about the future course of financial markets; it is only a framework for understanding the course of events as they unfold. If it has any validity it is because the theoretical framework corresponds to the way that financial markets operate. That means that the markets themselves can be viewed as formulating hypotheses about the future and then submitting them to the test of the actual course of events. The hypotheses that survive the test are reinforced; those that fail are discarded. The main difference between me and the markets is that the markets seem to engage in a process of trial and error without the participants fully understanding what is going on, while I do it consciously. Presumably, that is why I can do better than the market. ~ Geroge Soros

“Financial success depends on the ability to anticipate prevailing expectations and not real-world developments”. This is especially true in the current environment where the veil of the future is so thick. Instead of trying to figure out how bad this virus is going to get, focus instead on what the main narratives of the market are; where there’s consensus that’s not being reflected in the price and try and anticipate how that consensus will evolve going forward.

Unlike the virus, you can model that within a reasonable range of probability.

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.