Alex here with your latest Friday Macro Musings.

Latest Articles —

Your Monday Dirty Dozen [CHART PACK] — We look at more short-term sell signals indicating further downside ahead, a massive collapse in global auto demand, a profit contraction in Germany and a possible recession in Mexico, plus some unprofitable IPOs and 230-years of global debt.

Value Hive: Spooky Times for WeWork, Zero Fees and More! — Brandon discusses the Forever 21 bankruptcy, WeWork’s dropped IPO and the race to zero in brokerage commissions.

Articles I’m reading —

This New York Magazine interview with Scott Galloway is straight fire… Galloway talks WeWork and the crumbling of the collective delusion surrounding Softbank funded zeros. Take a few minutes and give this thing a read (link here). Here’s a clip from the piece.

“There’s going to be a lot of fallout here, but one of the things, there’s going to be an overdue immune reaction. We’ve decided the narrative has superseded numbers. I think that’s going to change. It’s already changed. Basically Uber started the decline and WeWork has massively increased the momentum. It’s like we’ve had this cocaine-fueled party at Studio 54, Uber was the lights starting to go on, and now they’ve gone on so bright it’s like you’re in an operating room. Endeavor couldn’t get out. Basically, these guys have totally shit in the IPO pond.”

Tim Duy writing over at his blog Fed Watch put out a short note this week saying that the data now calls for the Fed to cut rates again this month. I agree and think they need to surprise the market with a 50bps cut if they want to get any bang for the easing buck. Here’s the link and an excerpt.

“To prevent another rate cut, the Fed needs a reason to believe that they have eased enough to offset the forces weighing down the US economy. It is difficult to see that they can reach such a conclusion without an improvement in the data flow. It is almost impossible how they can reach this conclusion now that it appears the negative forces on the economy are intensifying. By only the first week of October, the stage will likely be set for a third rate cut at the end of the month.”

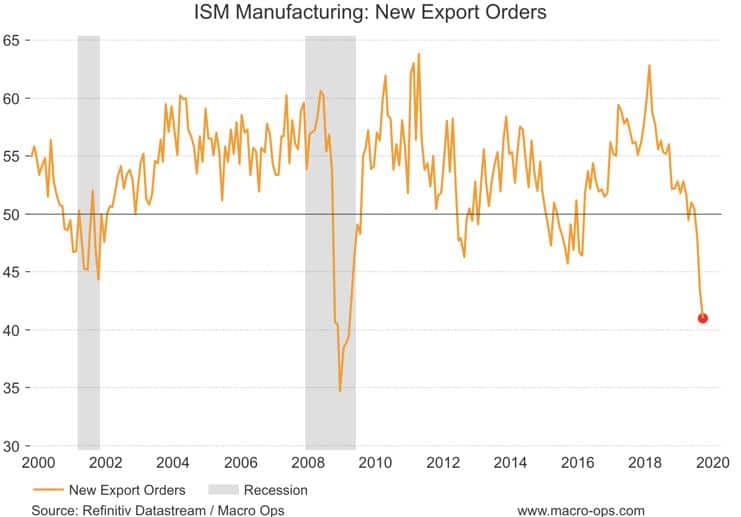

The ISM Manufacturing index sunk to its lowest level since the GFC last month. This has led to an increase in the general claims that we’re now, or very soon about to be, in a recession. While these weak numbers — especially the horrendous export orders print (chart below) — are nothing to sneeze at. Many are pointing out the contrast between these latest ISM numbers with those by IHS Markit, who constructs a more reliable indicator of our manufacturing health — at least in your author’s opinion. This post from Markit explains the key differences between the two indexes.

Lastly, give this great profile on Doyne Farmer, a physicist who specializes in the field of complexity, a read. Farmer is an interesting cat. He was one of the first people to hack roulette by building a small wearable computer device. Later, after someone suggested he apply his knowledge of non-linear systems to the market, he — without any prior investing or market knowledge — set a goal of “making $5 million in five years — a sum he’d substantially surpass.”

He ended up starting a hedge fund that averaged risk-adjusted returns “about five times the S&P 500s” before selling out to UBS for $100 million in 05’. He’s now working with a band of global central bankers on applying agent-based modeling to untangle the world of global finance and expose vulnerabilities.

Charts I’m looking at—

Since there’s plenty of bearish charts being passed around, I thought I’d share this contrarian one from the veteran market technician, Martin Pring (@martin_pring).

The chart is of the Pring Turner Leading Economic Indicaotr (LEI) which according to his accompanying post, is “a weighted ROC for three key economic sectors and a financial one. These are construction, consumer spending, employment and the stock market.” Pring notes that this indicator “has led every recession since its inception in the 1950’s. To be fair, it also signaled the non-recession of 1966. Signals are triggered by the “Recession Caller” in the lower window dropping below the red trigger line. The latest data point to the indicator moving away from that line in the direction of renewed recovery and away from a business contraction.”

Video I’m watching —

Here’s a short interview with forecasting expert, Dr. Phil Tetlock, on how to apply super-forecasting skills to the dynamics of investing in markets. The talk was put on by Greenwood Investors. It’s a short 14-minutes and worth a watch.

Podcast I’m listening to —

Do yourself a favor and go and give the latest Bloomberg Odd Lots podcast with economist Michael Pettis a listen (here’s the link). Pettis understands international capital flows and national accounting identity better than almost anyone. His ideas about what really drives trade imbalances and high national savings rates will sound counterintuitive to many but are how things actually work.

Collective members can read my detailed explanation of this concept in our Vault. I wrote about it in the paper titled “We Will Bury You” where I explained the idea in the context of China’s current macro situation.

Here’s a short summary of the talk from co-host Joe Weisenthal.

Book I’m reading —

I’ve enjoyed following the renowned technician Walter Deemer (@walterdeemer) on the twitters and so I decided to pick up one of his books “Deemer on Technical Analysis”.

Walt has been in the trading game forover 50-years. He’s learned a few lessons along the way and shares many of them in this book — along with some great trading war stories from the past. At roughly 300 pages with big type, it’s a relatively short and easy read. I’m maybe halfway through it so far but have read enough to recommend it to those looking for a good book on trading and technical analysis. Here’s a cut from the chapter on timing and selection.

“How Do You Know When the Market Has Topped? How Do You Know When to Sell?

First and foremost, gauge market sentiment. When the time comes to sell, you won’t want to.

At some point, everyone who wants to buy has bought, and pricess will stop going up. That is a bull market top.

At a bull market top, the market advance usually slows over a lengthy period of time. No one wants to sell. Everyone is happy. Everyone thinks that the market will keep going higher. The newspapers are full of glowing headlines and reports. It takes a bit of intestinal fortitude to say that this news is the reason why the market has already gone up, and it, therefore, may be time to back away and do some selling.

When everyone who wants to buy has bought, there is usually not much for sale. But unlike, say, commodities, where fear of scarcity causes price spikes, prices tend to remain steadier than seems normal.

Market tops usually take a while to form. There is usually time to get out. But always remember: When the time comes to sell, you won’t want to; the news is always good — very good — at a top.”

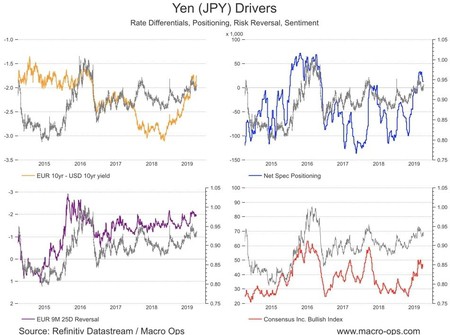

Trade I’m considering —

Short USDJPY (long JPY).

The technicals are set up nicely. The chart below is a weekly. It’s overextended on a short-term basis so I’d wait for a bounce to enter. But if we’re entering a period of risk-off, as I think we are, then we should see the yen strengthen from here.

The trend in rate differentials is moving in its favor. Net spec positioning has just moved to being a little long after being very short for the better part of the last few years. Risk reversals are trending in the right direction and sentiment is neutral.

Quote I’m pondering —

Why focus on the process when the world is outcome driven? Don’t results matter?

Yes, results do matter.

But if you optimize for the outcome, you win one time.

If you optimize for a process that leads to great outcomes, you can win again and again. ~ James Clear

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.