MMS owns, manages, and maintains hospitals, medical centers, drug stores, and pharmacies in Saudi Arabia. They provide nearly every medical service under the sun. From pediatrics to orthopedics. Neurology to cardiology. You name it — they do it.

MMS is a high-quality company with a history of high-teen Return on Capital (ROC). The company compounded its share price at 23.3% CAGR for the last decade, returning 713% since 2011. The S&P during that time returned a modest 184.4%, or ~14% CAGR.

Hospitals and medical centers are great businesses. They offer high barriers to entry and substantial competitive advantages at scale. The incentive feedback loops within hospital care ensure that those at the top stay at the top.

In this write-up, we’ll reveal why hospitals have such strong incentive feedback loops, how MMS will do to retain its position as the top hospital manager, and what value investors might place on the company in 3-5 years.

Hospitals: A Case Study in Feedback Loops & Perceived Value

Hospitals generate increasing returns to scale in proportion to the perceived quality of healthcare services provided. In other words, the better the care, the more people visit. The more people visit, the better the perceived care.

We see this in everyday life. We perceive the barber with a long waitlist as a better barber. Just like we perceive a restaurant’s most famous dish is also the tastiest on the menu. Even old-fashioned run-on-the-bank operations use perception and feedback loops. Someone sees a line out the door at the bank. They hear whispers of insolvency. They step in line. Which leads others to notice the line. Etcetera.

No story depicts this better than the 1985 Hong Kong bank panic (shout-out to Cliff Sosin for highlighting the story in our podcast). Here’s a blog post detailing the events of that day (emphasis mine):

“I once heard a story that in 1985, panic hit a Hong Kong bank when a line extended out of the door of a nearby bakery and across the front of the bank. Depositors passing by simply feared for the solvency of the bank and began to withdraw their funds.”

The above story illustrates the dangers of perception and value. But what about other areas besides “tourism” (barbers) and banking.

Perceived value creates lasting competitive advantages in industries where approval by committee reigns — like healthcare.

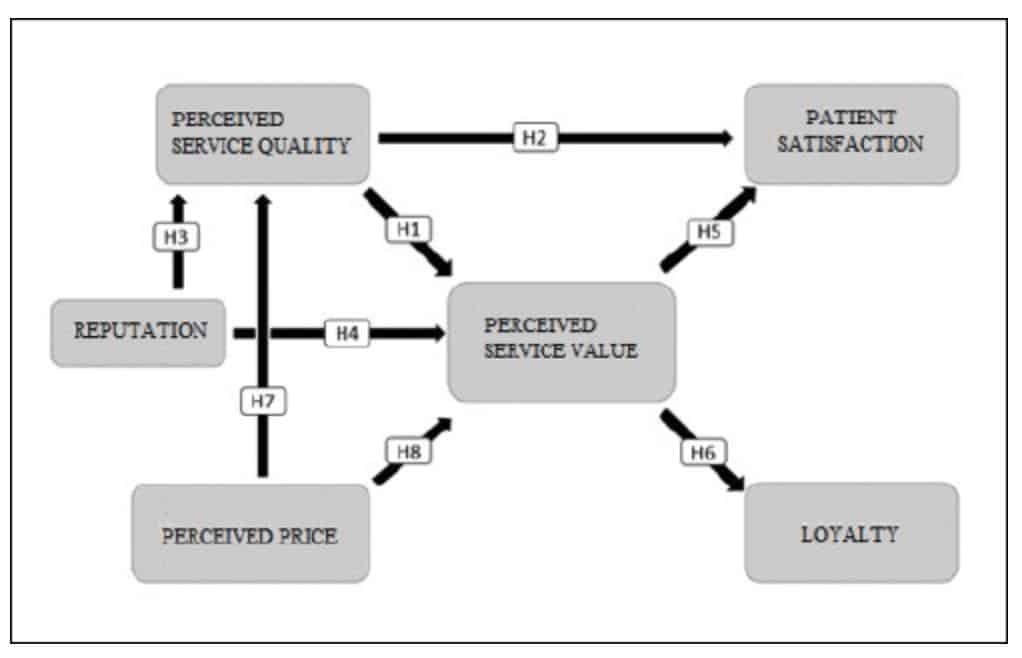

Teodor Pevec and Aleksandra Pisnik wrote a paper in the Slovenian Journal of Public Health analyzing this exact idea. Their conclusion supports our initial hypothesis that hospitals benefit from positively reinforced feedback loops based on perceived quality. Here’s an excerpt (emphasis mine):

“The major conclusion of this paper is that an especially higher reputation and higher perceived service quality can contribute to perceived service value and therefore to more satisfied patients.“

We can create our mental loop with the following ingredients: reputation, service quality, patient satisfaction, and patient loyalty.

Here’s what that looks like in practice:

Higher perceived reputation –> higher perceived service quality –> higher patient satisfaction –> higher patient loyalty –> higher perceived reputation.

The study showed two significant relationships within the healthcare service space:

- Patient Satisfaction and Patient Loyalty

- Reputation and Perceived Service Quality/Value

These two relationships are vital if healthcare service providers want long-term competitive advantages. Satisfied patients become loyal patients that recommend their hospital to friends/family.

Obtaining High Perceived Value: Chicken & Egg Problem

Hospitals/medical care centers face a chicken-and-egg problem regarding perceived value. To reach a higher perceived value, you need greater customer satisfaction and loyalty.

To do that, you need more patients and higher levels of care. But to do that, you need a high perceived value to attract the top talent.

And you can only employ the top talent by having the ability to pay that talent what they ask. Which means you need more customers. Wash, rinse, and repeat.

Solving this equation is hard. It takes time and millions (hundreds of millions?) in investment.

Luckily MMS already solved this equation. As the leading hospital and medical care manager in KSA, MMS cracked the feedback loop and now benefits from immense competitive advantages. Advantages that scale exponentially with time. And the best part? They spend very little to maintain this perceived value edge.

Let’s see how they did it.

Al-Mouwasat Medical Services: A (Near) Impenetrable Healthcare Provider

MMS was founded in 1975 by Mohammed Sultan Subaie. Subaie remains with the company as Chairman of the Board. He (along with the CEO and Managing Director) owns 17.5% of the company. Together management owns 52% of the business.

MMS has an extensive network of healthcare services and facilities. A few statistics to help see the size of their network:

- Six hospitals

- 1,200 beds

- 260 critical beds

- 400 clinics

- 60 operating rooms

- 4,500 employees

Each hospital boasts the highest quality medical equipment and luxury hotels for guests/patients. The company provides nearly every type of medical practice conceived, from skincare to ICU to Pediatric neurology.

Along with the hospitals, MMS has specialized care centers for skincare, fertility, and obesity.

They also have a pharmaceutical segment that centralizes drug distribution to allow for more efficient management and control for patients and doctors.

The company sports a laundry list of accreditations and quality awards. Most of the accreditations are Saudi-hospital firsts. For example, MMS is the first Saudi hospital awarded a “Stage 7” on the EMRAM (Electronic Medical Record Adoption Model). This social status signaling amplifies their perceived value status.

But don’t take my word for it. Here’s John Rayner’s (regional EMEA director of HIMSS (Healthcare Information and Management Systems Society)) opinion of the hospital (emphasis mine):

“This is such a great hospital that has made significant progress in such a short space of time. The degree of clinical engagement and the way that technologists and clinicians work together to improve patient safety and the overall quality of clinical care is truly impressive.”

In effect, MMS created its positive feedback loop of perceived value and patient satisfaction. Patients visit MMS because it’s one of the largest, most well-known hospitals in the country. It’s one of the largest hospitals because patients report high satisfaction and perceived quality of care and service.

That status as a leading hospital allows the hospital to attract and hire the best doctors and medical staff, further increasing their perceived (and actual) patient value.

Remember, these advantages grow exponentially with time — barring some disastrous medical malpractice. When MMS becomes the status symbol of “fantastic healthcare,” why would consumers choose anywhere else?

How MMS Makes Money

The company generates revenue via three primary sources:

- Outpatient services

- Pharmaceuticals

- Inpatient Services

Inpatient accounts for 45% of revenue, outpatient another 41%, and pharmaceuticals the final 14%, per the 2019 annual report.

MMS generates 86% of its revenue from high gross margin services, with inpatient/outpatient generating ~48% GM. The pharmacy business does ~28% gross margins.

Collectively the company did $495M in revenue and $218M in gross profit (44% margin). They’ve grown revenue at a 15% 5YRCAGR

Thanks to low SG&A spending, nearly 60% of gross profit flows through to operating income ($125M in 2019 at 25% margins).

After deducting interest, taxes, and minority interests, you’re left with $112M in NOPAT (22% NOPAT margins). NOPAT’s grown at a 19% 5YR CAGR.

The financials show the durability and power of MMS’s competitive advantages and perceived value for patients and doctors. We see high-teens growth rates in revenue and after-tax profits with an average 19% ROC.

Thinking About Valuation

MMS is a fantastic business growing revenues and earnings in the high-teens. The company should continue to generate double-digit growth rates in sales and profits for the next three-to-five years. Saudi Arabia is home to a fast-growing population and expanding healthcare industry.

ResearchAndMarkets.com‘s report estimates a 7.9% healthcare CAGR growth until 2024.

Furthermore, a USSaudi.org healthcare report indicated a 36.3% projected increase in demand for healthcare services by 2030. The numbers make sense as the country’s population slowly ages, with the elderly population (65+) expected to hit 8% by 2030 — compared to ~4% in 2020.

Let’s assume the company grows revenues ~12% per-year till 2024. That gives us $870M in sales. Next, let’s take MMS generates historical EBITDA margins or 34% on that 2024 revenue. This gives us $298M in 2024 EBITDA. Adding back D&A and subtracting taxes gets us $228M in NOPAT (or 17x current EV). Assuming ~14% of revenues spent on cap-ex (historical is ~17%), we get $146M in free cash flow (3.6% yield).

What a reasonable price for a private investor to pay for this business? The company trades ~26x normalized earnings, yet it’s growing those earnings at an average 19% CAGR.

Let’s say someone’s willing to pay 26x normalized NOPAT for this business. That gets us $5.9B in enterprise value by 2024. Subtract ~$170M in net debt, and you get $5.8B in shareholder value or $58/share. That’s ~52% upside from current prices.

Risks & Concluding Thoughts

There are myriad ways the company fails to generate shareholder value over the next five years. First, they could stall in quality of care and report dangerous medical malpractice. It’s taken decades to create the perceived value with patients. A string of medical malpractices could shake patients’ trust in the company.

Second, a shakeup in C-suite leadership would raise a red flag. The company’s had one Executive Chairman since 1975. Should the executives either sell shares or leave the company, it would signal further due diligence and apprehension.

Third (and most concerning) is that the Saudi Government could nationalize the business. They could claim it as a way to diversify from their traditional oil-related enterprises.

MMS isn’t “cheap” by traditional valuation metrics. Yet part of me thinks it’s the type of company Terry Smith would buy. Great businesses are rarely cheap. And the current price offers investors a chance to buy the company at ~1.36x PEG, assuming historical earnings growth.

Despite its “rich” valuation, its peers trade at an average of 25x earnings and 45x FCF. MMS is a much better business than its peers and trades slightly higher on an earnings basis but significantly cheaper on an FCF basis (31x).

MMS is one of the highest-quality businesses in Saudi Arabia. If you don’t end up investing, they’re a great case study on the power of perceived value, positive feedback loops, and the psychology of a healthcare consumer.