This world’s spooky. There’s lots of uncertainty in life. Yet there’s four things that remain true:

-

- Death

- Taxes

- Bill Belichick owning rookie QBs

- Value Hive producing killer content

Here’s what we’ve got in store this week. More of our favorite value manager Q3 letters. Tiffany receives a premium takeout offer. A 16-page article on everything Jim Chanos. TechCrunch has an ‘oopsie’ with SnapChat, and more!

Housekeeping: Some of you may have noticed we didn’t include the Idea of The Week section in last week’s letter. The reason is that we’re profiling at least 1-2 investment ideas with each quarterly letter we cover. Once the Q3 holiday season wraps up, we’ll presume with our normal content.

And if you haven’t already, make sure to subscribe to this newsletter. You’ll receive Value hive every week, completely free. Straight to your inbox.

Let’s rock and roll!

—

October 30, 2019

A Thief In The Night: What profession prides itself on deception, misdirection and charisma? No, I’m not talking about the CEO of Tesla Motors. I’m referring to magicians. This week’s trivia is simple. Which famous magician died on Halloween night?

You know the drill. House rules, no Google. Good luck!

_____________________________________________________________________________________________

Investor Spotlight: Arquitos Capital & Massif Capital

Last week we received two of my favorite letters: Arquitos Capital and Massif Capital. Steven Kiel (of Arquitos) and Chip Russell (of Massif) are exceptional investors. I had the pleasure of meeting Chip in Vail, CO. at the ValueX Vail conference. He’s a fantastic human and investor.

If I recall, he also beat me in corn-hole. So Chip, if you’re reading this. Yes, I am ready for a rematch.

Both letters offer thoughts on the markets and ideas on individual companies.

Let’s dig deeper.

Arquitos Capital: Staying Patient

Kiel’s fund returned -12.6% net of fees in the third quarter. YTD the fund’s returned -12.5%. Since inception (2012), Arquitos has compounded capital at an annual rate of 16.9%. That ain’t bad!

Kiel spends the letter discussing his three favorite ideas: MMAC, WED.V and SYTE. These are companies that Kiel would “own over the next decade even if there were no share price quoted.” That’s some serious conviction.

How can Kiel have that kind of conviction? Kiel believes the operations of each business provides potential exponential increases in value. He outlines this belief through his thesis on MMAC.

MMAC is Arquito’s largest position. MMAC invests in debt associated with renewable energy infrastructure and real estate.

The company’s darn cheap.

It trades less than 4x earnings, 15% discount to book value and sports 24% ROE. Along with those figures, the company generated $22M in FCF last year. That’s good enough for a near 13% FCF yield.

What Arquitos Likes: High Returns on Capital

Kiel reveals one of the main reasons why he’s bullish on MMAC:

-

- Generating high rates of return on low-interest debt

According to Kiel, MMAC recently borrowed up to $175M at sub 5% interest rates. The company will then use that debt to invest in MMAC’s solar lending portfolio. The solar portfolio has generated “better-than-mid-teens annualized returns over the past several years.”

For those following along, here’s what the equation looks like:

-

- Borrow $175M at <5% interest

- Invest the $175M into a portfolio generating >15% returns

- Print cash at ~10% return net of interest

Cherries on Top

The company halted their share buyback program to borrow the $175M. Once acquired, MMAC reinstated their buyback. If history is any predictor, MMAC could buy back 8-10% of their outstanding shares over the next year.

A Word on Investment Styles

Kiel ends his letter with an ode to Ben Graham. He notes that investment styles fall in-and-out of favor from time to time. Ben Graham-style value investing, unfortunately, continues to disappoint. Kiel reminds investors that, “The markets will be challenged in the future again, and these strong balance sheet types of companies will be a safe haven for stock investors.”

We just don’t know when that shift will occur.

Massif Capital: Gold, GrafTech and The Oil Markets

Will Thomson and Chip Russell run Massif Capital, which returned -7.47% in Q3. YTD they’ve returned -5.72%. Massif’s letter focuses on gold, a few shorts, GrafTech and an outlook on the oil industry.

The Oil Markets: Massif Sees Risk

Massif estimates that ~16M barrels of oil in the Persian Gulf are at risk due to potential conflict in the Middle East. The letter cites the troubles in Libya, Egypt and “a brewing conflagration between Syria, Russia, the Kurds, and Turkey.”

Massif notes that OPEC production is down ~4M barrels per day. US production in the lower 48 states is down. And US inventory levels are in a YoY deficit.

Yikes.

Pack a change of underwear if you’re investing in oil-related companies.

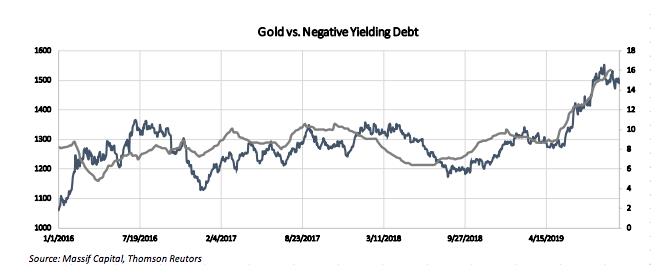

Gold as a Currency

Massif added their first gold miner stock last October. Since then, gold’s appreciated against the dollar more than any other ‘currency’.

Thinking about gold as a currency is interesting. Something I hadn’t heard of until reading this letter. Yet this rise in gold is a bit odd when compared with the other currency pairs.

Here’s Massif’s take on gold’s appreciation against other currencies (emphasis mine):

“Of the 32 currencies we track, seven have appreciated against the dollar, and gold has outperformed the others by more than 2x. This is a bit of an oddity given that the US Dollar and gold tend to move in opposite directions.”

And here’s a chart showing Gold vs. Negative Yielding Debt (via Massif Q3 letter):

You might be thinking, “that’s nice and all Brandon, but what stocks in the gold space should I look at?” Unfortunately I can’t answer that for you, and neither can Massif. But if you’re looking for a place to kickstart your research, here’s Massif’s current gold thesis holdings:

-

- Barrick Gold (GOLD)

- Continential Gold (CNL)

- Equinox Gold (EQX)

Massif sees a 38% average upside to these positions at an average gold price of ~$1,300/ounce.

Portfolio Review

Massif offers insight into part of their portfolio. I won’t provide all the details (as it would take up too much space here). But read the letter!

Here’s some of Massif’s current holdings:

Longs

-

- Diamond Offshore (DO)

- Massif’s Take: “At today’s prices, our potential expected return has increased substantially, and we expect to average down to capture this reality … We expect to exit the position with a 10% – 15% annualized return three to four years from now.”

- Teekay Offshore (TOO)

- Massif’s Take: “We wrongly viewed Brookfield’s involvement in the company, at the time of investment, as a positive. We expect to close out the position in the fourth quarter this year. We will incur a 28.9% loss in the position when we are bought out by BBU.”

- GrafTech (EAF)

- Massif’s Take: “GrafTech is our largest position at the current time … At our average entry price, given the new timeline, we expect to exit the position in just shy of 2.5 years with an annualized return over the life of the position of 19%.”

- Diamond Offshore (DO)

Shorts: UNP, CSX, DE, NCLH

Closed Positions: Consol Coal Resources LP (CCR)

_____________________________________________________________________________________________

Movers and Shakers: TechCrunch’s Whoopsie & Tiffany’s Payday

GIFs by tenor

GIFs by tenor

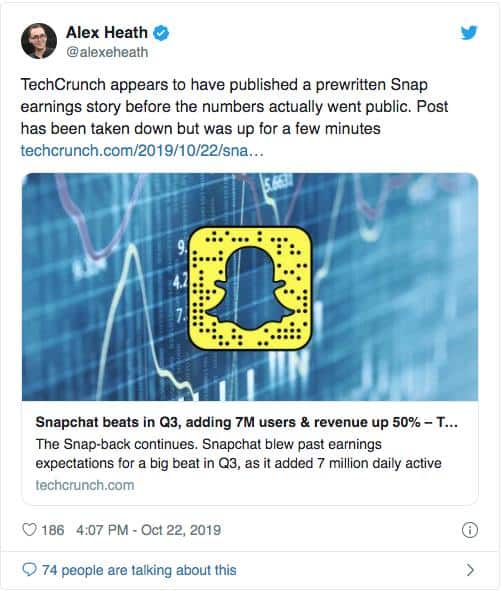

Last week, technology website TechCrunch released Snapchat’s earnings results. This isn’t news, right?

Well, that is until you realize they released earnings AHEAD of Snapchat’s earnings call.

Pour one out for the formerly-employed TechCrunch editor. That writer would fail the delayed-gratification marshmallow test too.

This gaff brought up a lot of questions on “the twitters” as Alex likes to call it. People questioned the legality of releasing earnings figures to journalists ahead of the public.

Public companies do this all the time. Writers have articles waiting in the batter’s box. All they need is a couple bits of information so they can hit “Publish” before everyone else.

That would’ve been a hell of a short, though. Shortly after releasing earnings, SNAP’s stock fell over 18%.

Mind The Gap: Tiffany’s Gets a Bid

Early Monday, luxury goods conglomerate LVMH threw its hat in the ring to buy-out Tiffany’s & Co. (TIF). LVMH isn’t messing around, either. Their offer? $120/share in an all-cash deal.

A successful deal would mark LVMH’s biggest takeover since buying Christian Dior for $7B. How do you top your biggest deal ever? You double it, of course.

Shares of TIF shot up on the news and currently trade at a premium to the $120/share offer. If the deal goes through, LVMH would pay close to 30x earnings, 4x sales and16x EBITDA for the company.

To all TIF pre-announcement bag-holders, I congratulate you. Cash in and buy your significant other a TIF bag with those winnings.

_____________________________________________________________________________________________

Resource of The Week: Acquirer’s Multiple Podcast

Tobias Carlisle’s podcast The Acquirer’s Podcast is quickly becoming one of the best. His most recent interview with Connor Haley is no exception.

Connor Haley manages Alta Fox Capital. The fund focuses on micro-cap and special situation-type stocks. Connor’s currently the #1 ranked contributor on MicroCapClub.com. He’s also a member of the elusive Value Investors Club website.

Also, do yourself a favor and give Tobias and Connor a follow on Twitter. They post great content.

_____________________________________________________________________________________________

Bonus Round — Jim Chanos 16-page Article & Horizon Kinetics

Jim Chanos is the world’s most popular short seller. I always find myself learning something new whenever I listen to him speak.

Intelligent Investor Share Advisor released a 16-page special report on Jim Chanos. It’s a masterclass on how he started his fund, his strategy and more. It’s a gold-mine. The report was first released in 2014, yet only recently made its way across the value interwebs.

Also, Horizon Kinetics released their Q3 letter. Horizon packs their letters full of interesting macro thoughts, quantitative ways of thinking and more. This letter is no different.

_____________________________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!