If you’re like me, you missed Berkshire Hathaway’s annual shareholders cult-gathering meeting. The weather was too nice and I’ve been cooped up inside my house too damn long not to enjoy the day. Instead of watching 3rd-grade level slide-shows, I played corn-hole.

My buddy beat me 21-0 in the third game. I know, I need to step my game up.

Anyways, before we dive into this week’s letters, check out our newest podcast episodes below.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Laughing Water Capital

- Alluvial Capital

- Alta Fox Capital

Let’s get to it!

—

May 06, 2020

Books on Credit / Bond Investing: Last week I linked to an Elliott Management report about Perspectives. In it, Elliott noted vast opportunities in the credit space. This prompted me to think about various credit/bond books that might be useful to investors new to the credit side (myself included).

Here’s a list of books I found via Amazon. Note this isn’t an exhaustive list. It’s merely my own meandering through the loins of Amazon’s recommendations:

-

- The Bond Book, Annette Thau

- Distressed Debt Analysis: Strategies for Speculative Investors, Stephen G. Moyer

- Step by Step Bond Investing: A Beginner’s Guide to the Best Investments and Safety in the Bond Market, Joseph Hogue

- The Handbook of Fixed Income Securities, Frank J. Fabozzi

If you know of any more please shoot them my way. Trying to add to this list if I can.

Alright, let’s get to the letters.

__________________________________________________________________________

Investor Spotlight: Three More Bangers

GIFs by tenor

GIFs by tenor

Laughing Water Capital: -20% Q1 2020

Matt Sweeney runs Laughing Water Capital (LWC). His fund lost 20% during Q1. Matt’s one of my favorite investors to follow. I always get amped when I see a new quarterly letter.

He starts with two questions that every investor should ask right now:

-

- If a company is essentially a box of cash, plus a ~50% ownership stake in a business where cash inflows typically don’t slow all that much during downturns, but cash outflows typically slow dramatically, why should the stock trade at a market cap that is a fraction of the company’s cash?

- If a company is in the business of selling a recession proof essential service online, and their main competitors rely on personal interaction, why should the stock of the online business get cut in half at a time when face to face interaction has all but stopped?

- If a company is in the business of manufacturing recession proof goods from domestic locations, and pundits are calling for the re-shoring of similar goods due to potential shortages during a pandemic, why should the stock of the domestic businesses get cut in half?

From a rational perspective, the answer is easy: no these businesses shouldn’t be cut in half. But Mr. Market doesn’t care in the short-term.

Sweeney didn’t mention any specific investments, but he provided a three-pronged framework for thinking about markets in the current state.

Framework #1: Balance Sheets > Income Statements

Balance sheets should always matter. But sometimes, they matter more than nearly everything else in a company’s financials. Now is that time. Sweeney expands on this idea, saying (emphasis mine):

“While I always focus on owning businesses that can survive or even thrive during a weak economy and thus generally eschew leverage, I admit I had not considered the possibility of revenues at any of our businesses temporarily going to zero. The market has been swift to punish companies with leverage, but it is also a fact that the more predictable a business is, the better it is, and the more debt it can handle.”

Read that last sentence again. Leverage in-and-of itself isn’t evil. Instead, one should think about the dangers of leverage as a function of the durability of the model and the allocation skill of management.

How do you manage leverage and cyclical businesses? Mid-cycle earnings. Mid-cycle earnings paint a picture of what a leveraged / cyclical earns on a “normalized” basis. Like any cyclical, there will be times of plenty and times of famine.

Not doing this brings in the risk of buying a company at peak earnings — or buying right at their cyclical top.

Remember: cyclical stocks are cheap when they look expensive, and expensive when they look cheap.

Framework #2: Pick Businesses That Improve Themselves in Downturns

This framework is one of the most powerful tools at an investors disposal. Strong businesses that survive economic downturns usually clean house when the recovery rolls around. Why is that? Let’s look at Sweeney’s explanation (emphasis mine):

“Almost all businesses are feeling pain in the current environment, but by focusing on strong balance sheets, strong competitive positions, and properly incentivized management teams, we are focusing on businesses that are likely feeling less pain than their competitors, meaning that our businesses can take market share or otherwise improve their position vis a vis their competitors during this downturn.”

If you’re buying a great, competitively advantaged business, downturns are exciting. Your business has a chance to scoop up over-leveraged competition and expand market share.

That said, notice how Sweeney didn’t say “strong stocks.” He said strong businesses. Stocks of great businesses get hammered just as hard (and in some cases, harder) as stocks of bad businesses.

Mr. Market’s a voting machine in the short run, after all. Yet over time, as the economy comes back, the market will realize the company’s dominant share and value it appropriately.

Framework #3: Getting To “Enough” on Future Potential Returns

Humans are hard-wired to focus on the short-term. As Sweeney explains, “If our paleolithic ancestors did not place more weight on meeting their immediate needs such as food, water, and shelter, then any long-term plans would be completely useless.”

But how cheap is cheap enough? Can we pick the bottom-tick in the markets? Nope. And if we happen to, credit it to luck — not skill.

Let’s revert to Sweeney’s example of buying a company at 3x mid-cycle earnings. If that company goes from 3x to 2x earnings, how bad do we feel? We thought it was cheap at 3x. Seeing it at 2x makes us nervous — and that short-term mindset takes over.

The point is you can’t pick bottoms and you can’t wait until the dust settles. Take credit card stocks during 2009 as an example (from the letter, emphasis mine):

“For example, during the financial crisis, credit card delinquencies did not peak until 6-8 months after the March 2009 low. By the time the worst of the data presented itself, credit card stocks had rallied 300-400%.”

Here’s a recap:

-

- Focus on balance sheet strength over income statement profits

- Pick businesses that improve (survive) during economic downturns

- Don’t try and pick bottoms

_________________

Alluvial Capital: -17.70% Q1 2020

Dave Waters runs Alluvial Capital. His letters are frequent guests during our quarterly letter review. And for good reason. Dave hunts for stocks in places few fund managers venture. His letters bring to light stocks living in the dark corners of the market.

If you haven’t had a chance, check out my podcast with Dave here.

One thing I like about Dave’s letters is the amount of actual stock/business discussion. I don’t know if it’s COVID-19, but I’ve read a ton of letters with pages on herd immunity rates and nothing on stocks.

Dave features myriad stocks in his letter, so we’ll focus on the following:

-

- Tower Properties Corp (TPRP)

- Crawford United (CRAWA)

- Intred S.p.A. (ITD)

Let’s roll!

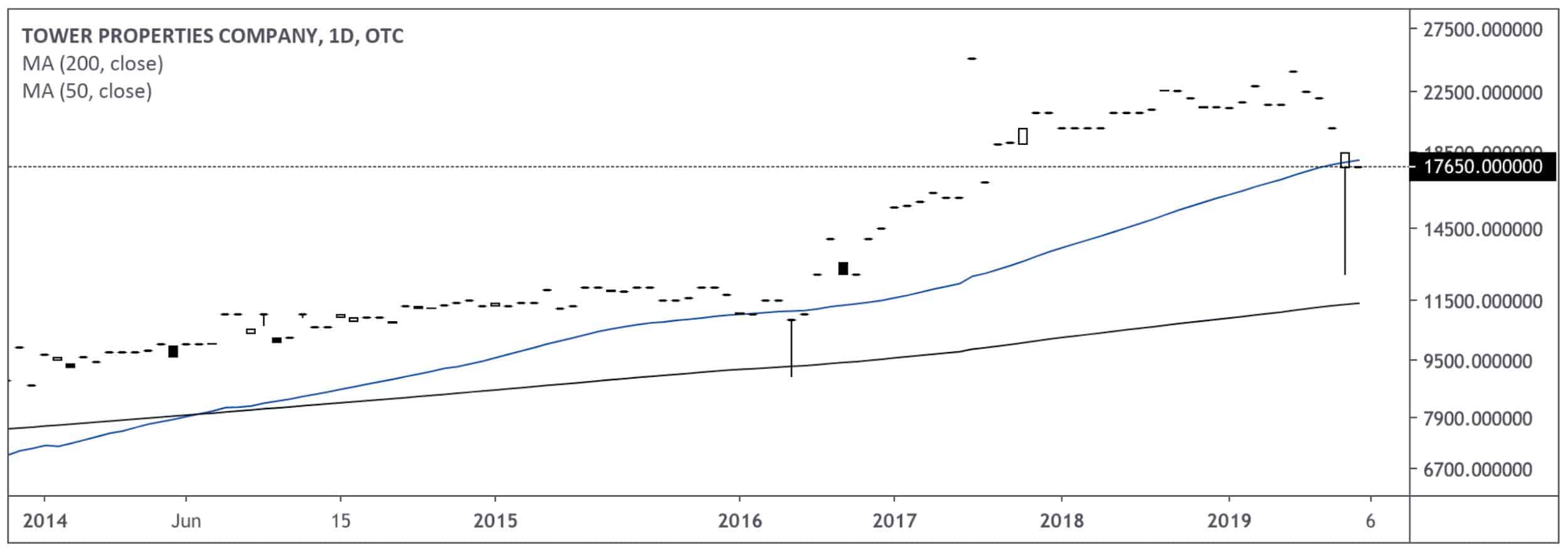

Tower Properties Corp (TPRP)

Business Description: Tower Properties Company engages in owning, developing, leasing, and managing real property. It owns office buildings, apartment complexes, a warehouse/office facility, and land held for future sale or development. – TIKR.com

What’s To Like:

-

- Well-run business

- Produces normalized funds from operations of $3,400 per share, fully taxed (5x FCF)

- Highly illiquid

What’s Not To Like:

-

- Highly illiquid

- Low share count

- High share price ($17K/share)

Here’s the chart …

Look at that illiquidity. As a proxy, one share traded yesterday. One. Do you notice that huge tail on the end of March 27th’s candle? Here’s Dave’s commentary (emphasis mine):

“On some of the worst market days in March, the fund was able to acquire shares of Tower at prices ranging from $12,500 to $13,500.”

It pays to have limit orders in, folks! I bet Dave had a limit order of around $13K and never dreamed he would get filled at that price again. But markets are strange things!

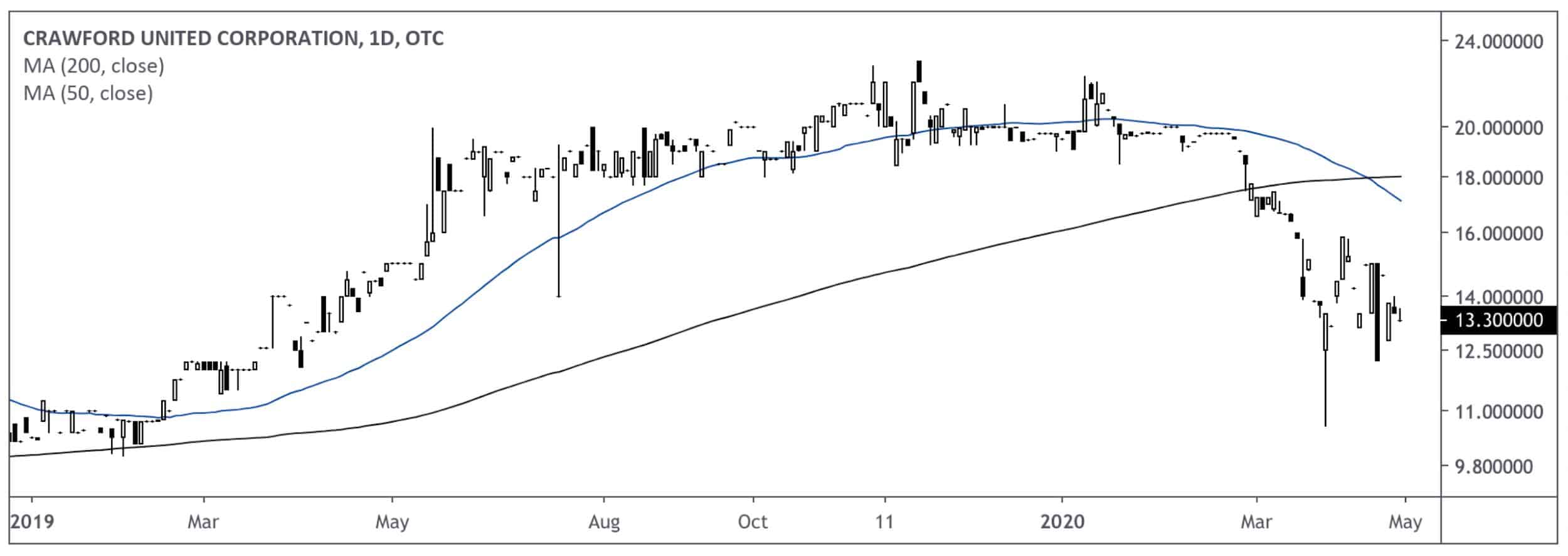

Crawford United (CRAWA)

Business Description: Crawford United Corporation, together with its subsidiaries, engages in aerospace components, commercial air handling, and industrial hose businesses in the United States. The Aerospace Components segment manufactures precision components primarily for customers in the aerospace industry. This segment provides complete end-to-end engineering, machining, grinding, welding, brazing, heat treat, and assembly solutions. The Commercial Air Handling segment designs, manufactures, and installs large-scale commercial, institutional, and industrial custom air handling solutions. – TIKR.com

What’s To Like:

-

- Insider Ownership (Skin in the game)

- Down 30%+ from Feb. highs

- Great business model with long runway

- Highly illiquid

- High ROE

What’s Not To Like:

-

- Cyclical business

- High deferment rate with products/services in downturn

- Steady gross profit margin decline

I chose as part of the list because it’s such an interesting company. In short, CRAWA buys small, niche players in the HVAC industry, rolls them up, and uses the cash to buy more of those businesses.

Here’s Dave’s take (emphasis mine): “With the application of a judicious amount of debt financing, the returns on equity can be impressive and value compounds quickly. There are thousands of these acquisition candidates, many of them run by founders approaching retirement age and looking for an exit.”

Here’s the chart …

At $13.30 you can buy CRAWA for 9x 10YR normalized earnings. That includes a few years of negative earnings as well. If you zoom in, say the last five years, you’re looking at roughly 4x normalized earnings.

Given their “buy and build” strategy, it’s important to look at debt and balance sheet health. CRAWA has $14M in long-term debt and another $4M in current short-term borrowings. They have over $16M in receivables against that debt, and another $2M in cash.

The company generates enough EBIT to cover interest expense 9x over.

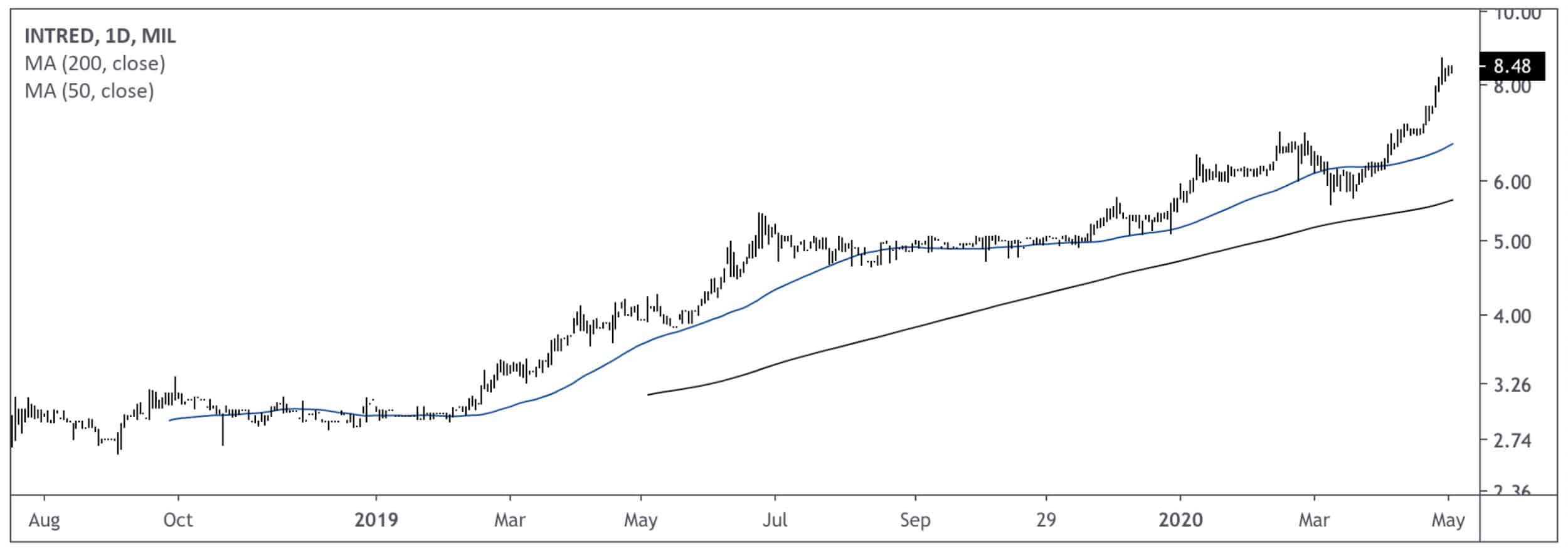

Intred S.p.A (ITD)

Business Description: Intred S.p.A. provides various telecommunication services in Italy. The company offers broadband connectivity services, including ADSL and HDSL connections; ultra-broadband connectivity services, such as fiber to the home and fiber to the cabinet connections; and RDSL connectivity services. It also provides landline telephone services; cloud services comprising hosting, such as domain registration, email, Web, etc., as well as data center and virtual services; and ancillary services consisting of rental services for line termination equipment, technical support, ancillary charges, etc. – TIKR.com

What’s To Like:

-

- 20%+ 5YR Revenue CAGR

- 70% Gross Margins

- 27% Operating Margins

- $9M Net Cash

What’s Not To Like:

-

- Low float

- 78% owned by insiders/company

Let’s take a look at the chart …

ITD did an IPO in Italy at 6x EBITDA with net cash on the balance sheet and 20%+ top-line revenue growth. That’s the power of venturing outside the US. You’re not going to find many IPOs with those metrics here. Heck, if an IPO is profitable it’s a reason to celebrate — let alone cheap.

_________________

Alta Fox Capital: -26.77% Q1 2020

Connor Haley runs Alta Fox Capital. Since inception, he’s generated 7.98% annual returns. This compares favorably to the S&P and Russell indices.

Haley’s fund lost nearly 27% in Q1. You can read his letter here.

Connor covers three names in his letter:

-

- Mamamancinis Holdings (MMMB)

- Gan, Plc. (GAN)

- Evolution Gaming (EVO SS)

Let’s dive in.

Mamamancinis Holdings (MMMB)

Connor’s Take: “They provide meatballs and other pasta/Italian products to grocery stores. It is a boring and non-sexy business. It is also an “essential service” and sells items that can be stored in freezers around the country as people hunker down in their homes. We bought it at 6x our estimate of forward earnings despite revenue growing 30%+ organically. The stock is already up 60% from our publish date, but we believe there remains potential for 100%+ upside over the next three years in an eventual sale of the company.”

What’s To Like:

-

- Insider ownership (skin in the game)

- 20%+ top-line revenue growth

- 30% EBITDA growth

- Leveraging fixed costs to improve operating margins

- CEO has successful history of operating businesses

What’s Not To Like:

-

- Current high customer concentration

- Promises of high growth & failed in past

- Key man risk (CEO)

Here’s the monthly chart …

What’s It Worth: Here’s Connor’s estimate of future value:

“At current prices ($1.02) we have the business trading at 6.1x our FY2021 EPS (calendar year 2020) which we believe is far too cheap for a business showing this type of growth and margin expansion. Note that the business has ~$9.7m in NOLs, which we expect them to fully utilize by 2023.”

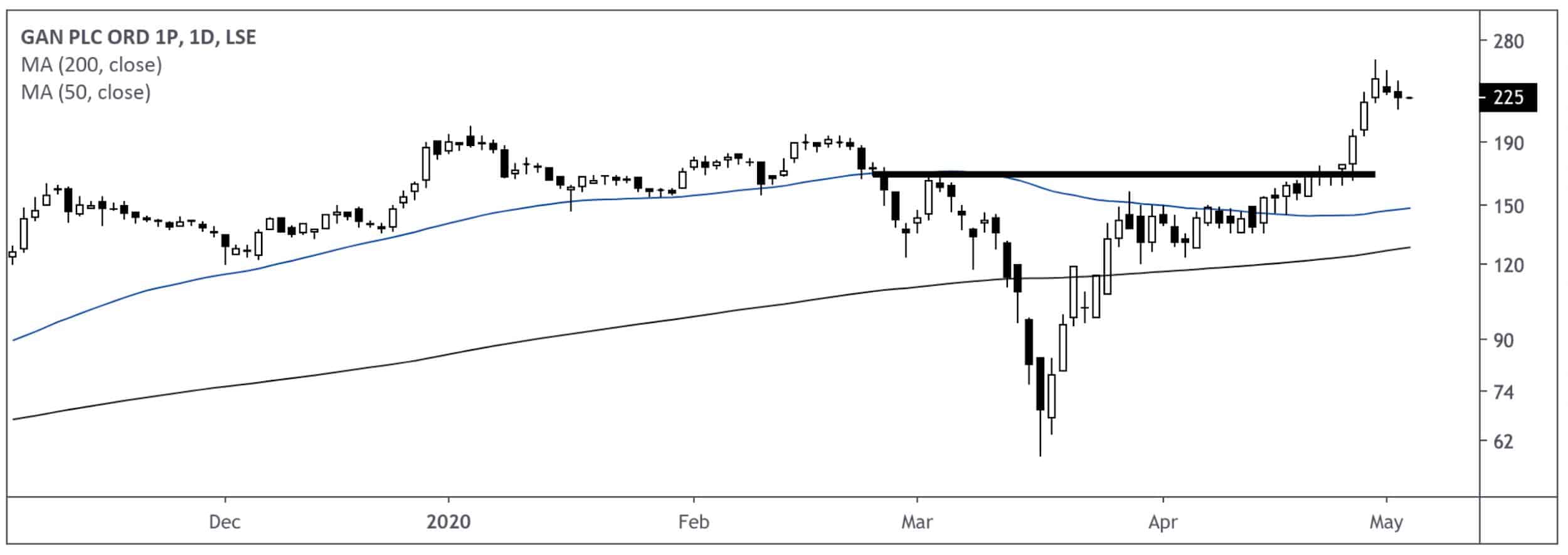

Gan Plc. (GAN)

Business Description: GAN plc provides enterprise online gaming software, operational support services, and online game content development services to the casino industry. The company operates through Real Money Gaming Operations (RMG), and Simulated Gaming Operations (SIMGAM) segments. It licenses GameSTACK, an Internet gaming system to online and land-based gaming operators for regulated real-money and simulated gaming online. – TIKR.com

Connor’s Take: “GAN grew revenue 114% in 2019 yet traded at a high single digit FY20E EBITDA multiple when we entered our position. We then increased our position significantly when the stock sold off sharply amidst the cancellation of sports and broader COVID-19 induced panic selling. While sports betting is roughly 10% of GAN’s revenues and its cancellation would be a headwind, the market was reacting as if all of GAN’s revenues were at risk.”

What’s It Worth (from the letter): “GAN recently issued market guidance of $100M in sales in three years with EBITDA margins of 30%+. Their sales in 2019 were ~$30M and EBITDA was ~$8.4M. Today investors can buy GAN prior to listing on the Nasdaq at <10x our estimate of FY22E EBITDA. This seems very cheap given their strong growth, scalable model, and the valuation of other US internet gambling focused peers”

Here’s the chart:

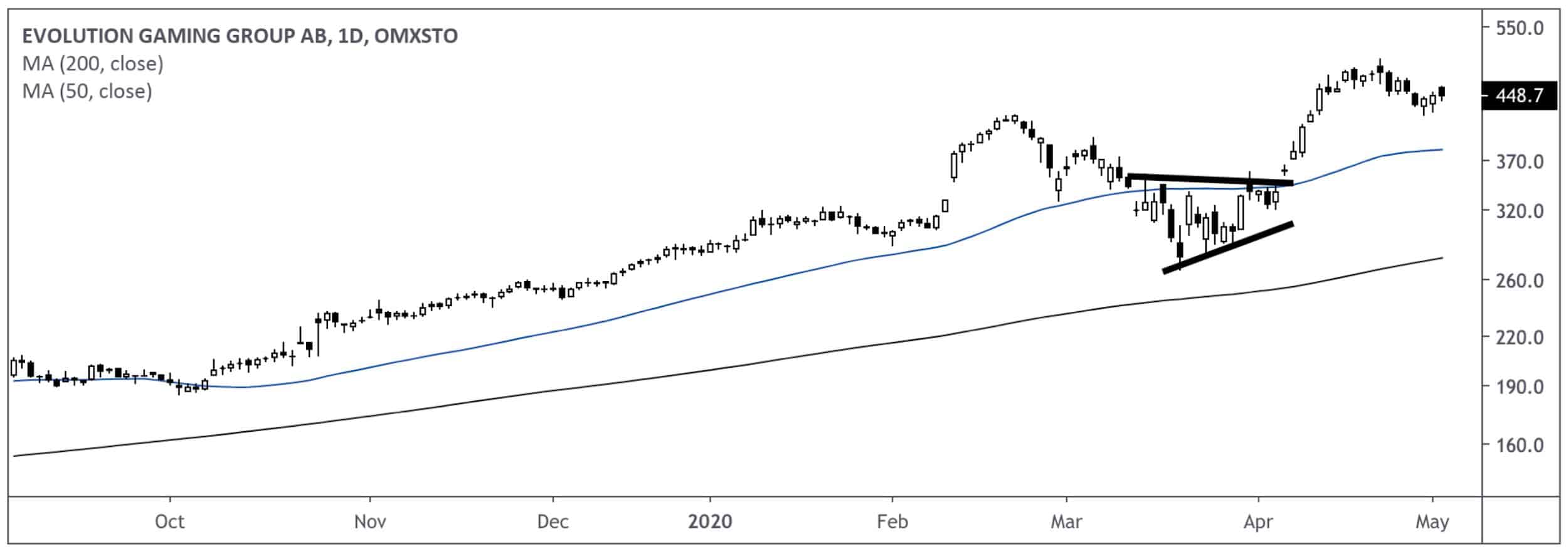

Evolution Gaming (EVO SS)

Business Description: “Evolution Gaming Group AB (publ) develops, produces, markets, and licenses live casino solutions to gaming operators primarily in Europe and the United States. The company runs the game from a casino table, which is streamed in real time and end users make betting decisions on their devices, such as desktops, smartphones, tablets, etc. It also runs on-premise studios at land-based casinos in Belgium, Romania, the United Kingdom, and Spain.” – TIKR.com

Connor’s Take: “This is a phenomenal business with 50%+ EBITDA margins and 35%+ organic revenue growth in each of the last three years. It is also very under the radar for a ~$7B EUR market cap, likely due to the lack of any U.S. research coverage. EVO is a B2B provider of live casino games. They work with land-based and online casino operators to enable casino games played with a live dealer that are streamed from one of EVO’s many global studios.”

What’s It Worth: “We were able to purchase EVO at 9x FY22E EBITDA. With increased investor awareness and given EVO’s competitive advantages, attractive unit economics, and high growth, the business could easily trade at double the valuation today (12x FY22E EBITDA), even after the recent rally.”

Here’s the chart …

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!